Benoît Cœuré: Trade as an engine of growth - prospects and lessons for Europe

Speech by Mr Benoît Cœuré, Member of the Executive Board of the European Central Bank, at the NBRM High Level International Conference on Monetary Policy and Asset Management, Skopje, 16 February 2018.

I thank you for inviting me to speak here in Skopje today1. I would like to take this opportunity to discuss an issue which I believe is key for the economic future of Europe and particularly relevant here, in the Western Balkans: the prospects for trade as an engine of growth.

For several years now, global trade growth has puzzled many observers. While global trade grew at about twice the rate of GDP before the crisis, it has slowed measurably since then and has often grown at the same rate as, or even below, that of global output. However, in 2017, world import growth once again outpaced world GDP growth. The euro area is benefiting from this recovery, with export growth the highest in many years.

In my remarks this morning, I will argue that the rebound in trade mainly reflects cyclical factors. Accommodative monetary policies worldwide have succeeded in boosting growth and investment and, with them, global imports. Structural headwinds remain, however. Maturing global value chains, geographical shifts in trade and an accelerating push towards more automation make it less likely that trade can again expand at the pace observed during the pre-crisis boom.

To the extent that trade helps lift growth, policymakers have a role to play in providing an environment that is conducive to trade. At the same time, they need to ensure that appropriate systems are in place to support workers affected by secular shifts in both trade flows and labour demand.

Rebound in world trade

Let me start with a few facts and charts.

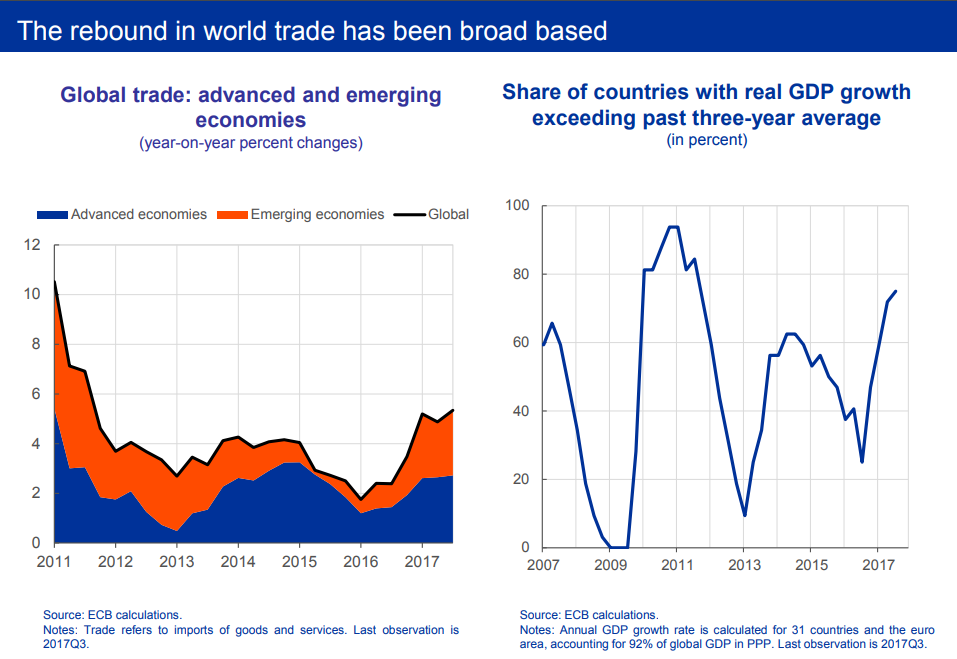

Last year, global imports expanded by 5%, the strongest growth in seven years. On the left-hand side of my first slide you can see that the rebound in global trade was broad-based, with both emerging and advanced economies contributing in roughly equal proportions. On the right-hand side you can see that this by and large reflects the fast broadening of the global economic expansion. At the end of last year, 75% of the economies worldwide experienced growth above their three-year averages. In 2016, this share was below 30%. So, the global economy is in a much more robust state today than it was just a few years ago.

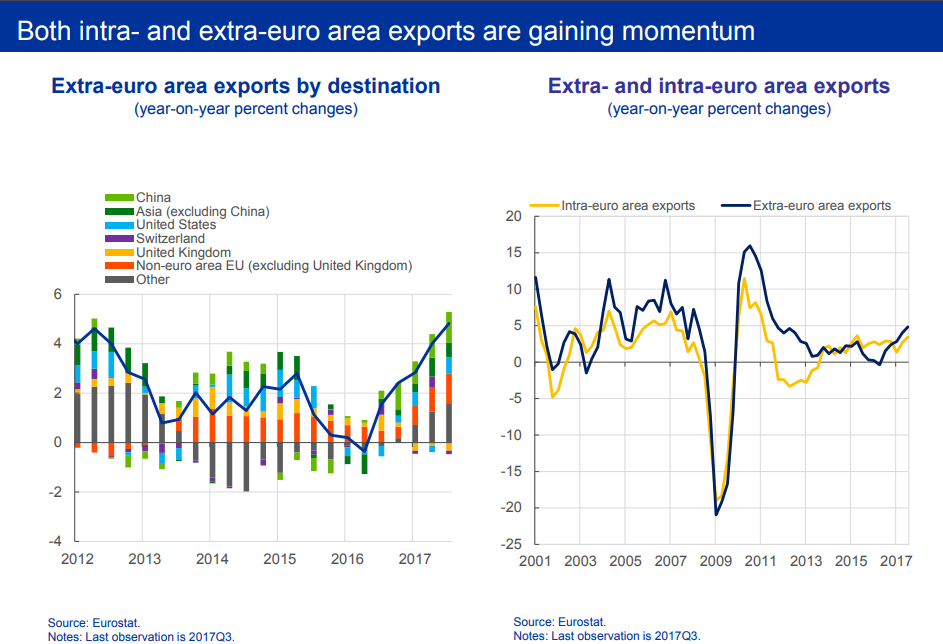

The breakdown of extra-euro area exports also shows that the current synchronous expansion is fertile ground for a strong rebound in trade. You can see this on the left-hand side of my next slide. By the end of last year, euro area exporters had expanded their business with virtually all of our main trading partners.

Growing demand from China, and emerging Asia more generally, as well as recovering demand from commodity exporters are once more contributing to, rather than subtracting from, export growth. One exception to this benign picture is the United Kingdom, where Brexit repercussions might already be showing through in the data.

Trade has also gained momentum within the euro area. You can see this on the right-hand side. Although intra-euro area export growth is currently somewhat weaker than extra-area growth, we can see that exports are today contributing more evenly to growth across euro area countries. It is no longer only a few Member States that are benefitting from a booming global economy.

In particular, structural reforms and internal devaluation in formerly stressed economies, together with a protracted period of weak domestic demand during the crisis years, have prompted more firms in these economies to improve their competitiveness and thereby profit from a rise in foreign demand, both inside and outside the currency union.

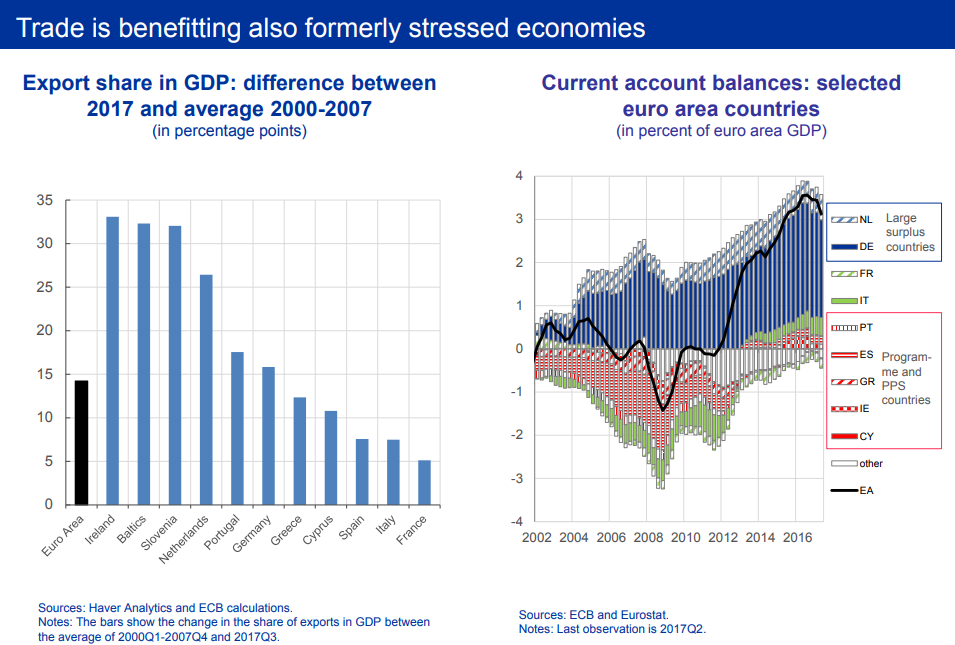

This is perhaps best illustrated by the share of exports in GDP on the left-hand side of my next slide. Last year, compared with the period 2000 to 2007, this share rose strongly in Ireland and Slovenia, while Portugal, Greece and Cyprus also managed double-digit gains. This supported the economic recovery and helped to reduce unemployment.

A natural side effect of these changes was a notable widening of the euro area's current account surplus. You can see this on the right-hand side. Almost all Member States that entered the financial crisis with large current account deficits are today reporting current account surpluses. Of the euro area's 19 Member States, 13 have current account surpluses.

But the chart also illustrates clearly that the rebalancing has remained limited to formerly stressed economies. Up until recently, current account surpluses have continued to rise in Germany and in the Netherlands, the two export powerhouses in the euro area. While these surpluses undoubtedly reflect strong underlying fundamentals in terms of competitiveness, they also reflect an imbalance between domestic savings and investment. Higher domestic investment would therefore be a constructive way to address large current account surpluses and, at the same time, to prepare for future challenges.

Now, does the current trade recovery bode well for the future? What are the prospects for global and euro area trade? Will we return to an environment where trade growth persistently outpaces GDP growth?

In answering these questions, I will distinguish between cyclical and structural factors.

Cyclical factors affecting trade growth

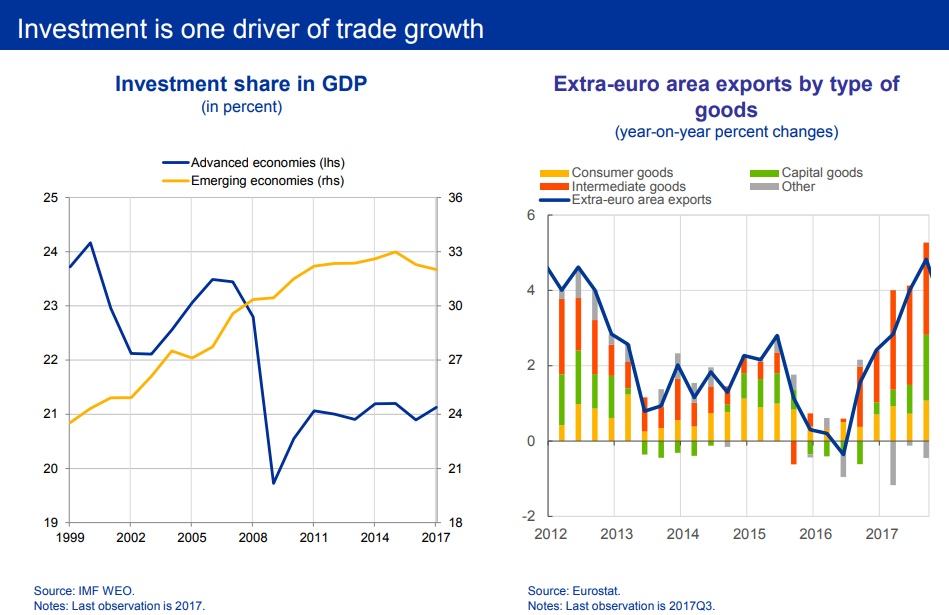

As for the cyclical factors, empirical evidence suggests that economic growth alone is often not a sufficient condition for strong trade growth. Indeed, trade did not start to lift off before we saw a nascent recovery in global investment, which had weakened significantly after the Great Recession.

On my next slide you can see that in advanced economies the share of public and private investment in output declined sharply with the advent of the crisis and has remained well below pre-crisis levels since then. For emerging markets, the investment share had been rising but it has plateaued in recent years.

So, the composition of growth matters for trade. Investment in particular has a relatively high import intensity.2 As a result, a slowdown in investment demand typically has a disproportionately large adverse impact on trade, relative to other GDP components. It is therefore no coincidence that the recovery in trade last year was led by exports of capital goods and intermediate goods, both key inputs to investment. You can see this clearly in the case of the euro area on the right-hand side.

The implication is that future trade growth will depend to some extent on the sustainability of the current investment recovery. For sure, continued accommodative financial conditions and business optimism will continue to support investment and hence trade. The United States has also just lowered its taxation of capital, which can be expected to further boost growth in capital formation. In the euro area, investment is expected to remain robust due to rising corporate profits, high levels of expected earnings, and an increasing need to modernise the capital stock. Indeed, according to Eurosystem staff projections, investment in the euro area is expected to increase by just over 10% until the end of 2020.3

So, overall, we can be confident that investment growth, and the current broad-based economic expansion more generally, will continue to support international trade in the coming years.

Structural factors affecting trade growth

Yet, while the cyclical pick-up in trade remains supportive, structural headwinds may prevent rates of trade growth returning to the levels we observed in the two decades prior to the crisis. In short, empirical evidence suggests that the factors that have supported extraordinary trade growth rates in the past were special and are likely, by and large, to have run their course.4

For example, rapid financial deepening in emerging economies, and better access to capital markets, has helped boost trade growth in the past. But research suggests that there are likely diminishing marginal effects of finance on trade growth.5 In other words, there appears to be a threshold - when private sector credit reaches around 100% of GDP - beyond which financial deepening no longer contributes meaningfully to trade growth.

But by far the strongest factor behind the boost in trade growth prior to the crisis, but which now appears to be waning, is the international outsourcing of production processes via so-called global value chains.

I would like to focus on this factor in the remainder of my remarks.

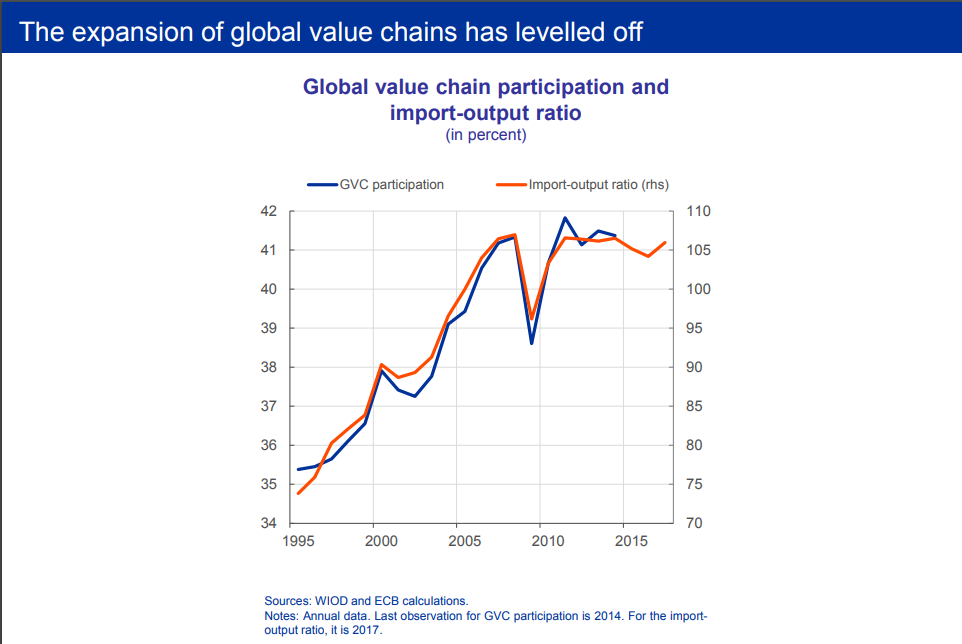

Global value chains involve production processes being split into a number of intermediate steps, mainly in order to exploit international factor income differences. As a result, production has become dispersed across countries, and mechanically increased the amount of trade that took place for a given final output. You can see this clearly on my next slide. In the past, we have seen a close relationship between global value chain growth and the share of imports in total output.

The global integration of China, for example, not only increased its exports to developed economies, but it also increased its imports of raw materials and intermediate goods from neighbouring emerging economies. This boosted overall world trade relative to output.

However, as you can see on the same slide, since the crisis we have seen a levelling-off of participation rates in global value chains. In other words, the share of global value chain related exports and imports in total trade has stabilised. This means that the support for world trade from global value chains has recently faded.

The important question to ask then is whether this levelling-off will be temporary or more permanent. In the view of ECB researchers, there are at least three factors that suggest that the slowdown in global value chain formation is likely to persist, at least in the short term.

The first factor relates to supply-chain risks.

You will recall that the 2011 earthquake and tsunami in Japan caused severe supply disruptions. Some companies discovered, the hard way, that supply chains were not transparent, rather like the fault lines in securitisation that caused the great financial crisis. In short, suppliers hired sub-contractors, who themselves hired sub-contractors, and so on. As a result, an OECD report suggests that supply chains are increasingly designed to contain risks as well as costs.6 Often, this implies shorter and more transparent value chains. And given the intimate relation between digitalisation and trade, this trend could be amplified further in the future by rising cyber risk and risks to data integrity.

The second factor relates to shifts in comparative advantages.

In the past, wage differentials for unskilled labour made the international fragmentation of production processes worthwhile. Some of those wage differentials are now less marked as emerging economies continue to develop. In China, for example, real wages have increased by a factor of ten since 1995.

The implications for trade are twofold. First, as the Chinese and other emerging market economies mature and incomes grow, there is a rising shift from investment to consumption. This results in a lower trade intensity of demand. We already see that Chinese import growth has slowed markedly.

The second implication is that outsourcing of production processes has become less profitable. In the short term, this is unlikely to unravel existing value chains that also benefit from important supplier network effects - that is, from local upstream and downstream inputs and services. But in the long run it might lead to businesses reconsidering their offshoring practices.

This brings me to my third point.

Shifts in comparative advantage could simply mean that other, less developed economies will take over from the more mature economies at the lower end of global value chains, following the traditional "flying geese" pattern. Like nomads, firms move on and global value chains move with them. Lumpy technological change could even help some of these economies leapfrog and jump directly to the most advanced stage of technology - the so-called "advantage of backwardness".7

I would like to suggest, however, that the fourth industrial revolution - and the associated increase in automation and the use of artificial intelligence - may mark a move away from this model.

The reason is that the increased use of robots has the potential to modify the relative factor intensities in the production of certain goods and services and may thereby sever the link between, say, cheap labour and the location of unskilled manufacturing activities.8 Put simply, if robots can deliver the same output more cheaply, more efficiently and closer to the consumer, then firms may have fewer reasons to spread production across countries.9

In other words, robots could turn global value chains on their head and cause firms to reconsider offshoring practices. A survey by the Boston Consulting Group, for example, revealed that more than 70% of senior manufacturing executives in the United States consider that robotics improve the economics of local production.10

Lower automation costs are a key ingredient of this rethinking. Indeed, while the cost of labour is rising in traditional low-cost developing economies, the cost of robots has fallen sharply. By some estimates, the average price of industrial robots has declined by about 40% over the past ten years and is projected to decline considerably further.11

And the potential for automation is enormous. A recent McKinsey report suggests that 60% of global manufacturing activities, and 81% of manufacturing hours, could be automated using existing technology.12 This is not just a topic for the future. We are already seeing clear signs of accelerating automation.

According to data from the International Federation of Robotics, the global supply of industrial robots grew by 19% on average between 2009 and 2016. It is forecast to increase further by almost 80% by 2020, bringing the total stock of robots to around three million.

Of course, technological progress also changed the way we produced goods and services in the past. But because the current breakthroughs - just think of 3D printers, autonomous vehicles or cognitive computing - are virtually unprecedented in scope and scale, the "march of the machines" may potentially render a significant share of the international fragmentation of trade redundant, particularly in the manufacturing sector.

The rise of automation may therefore accelerate a process that Dani Rodrik termed "premature deindustrialisation" in developing economies.13 This term describes a pattern whereby developing economies see their manufacturing base shrink at a level of income that is far below the level attained by advanced economies before they started to deindustrialise.

This means two things. First, the impact of reshoring and the automation of unskilled manufacturing processes on developing countries' labour markets could be significant. The International Labour Organization recently estimated that around two-thirds of jobs in the textile, clothing and footwear industry in Indonesia are at risk of automation.14 For Cambodia, the figure is 90%.

Second, automation may become a headwind to the catching-up process of developing countries. Historically, productivity in the manufacturing sector has tended to converge to the global frontier more easily than that in other sectors. Manufacturing was thus traditionally a sector that allowed developing economies to catch up with advanced economies. China is certainly a case in point. But to the extent that automation accelerates the decline in manufacturing, it may force countries to consider the development of other growth models.

None of this is to say that technological progress is bad and should be stopped. On the contrary, if managed wisely, the fourth industrial revolution has the potential to lift global income levels and to improve the quality of our lives. After all, technological progress remains the engine of both growth and aggregate employment, although often in an increasingly disruptive way.

Historical evidence provides some cause for optimism. A recent study on German manufacturing, for example, finds that automation accounts for around a quarter of the manufacturing jobs lost between 1994 and 2014.15 But these jobs were fully offset by higher employment in the services sector. Moreover, manufacturing workers in positions with greater exposure to robots were more likely to stay at their current workplace, although not necessarily in the same job and usually at the cost of lower wages.

Such compositional changes have taken place in the past too. For instance, the share of US employment in agriculture fell by 56 percentage points between 1850 and 2015. New technologies may bring new opportunities too. The McKinsey report I mentioned estimates that by 2030, around 10% of labour demand will be for positions that barely exist today, for example AI specialists and big data analysts.16

This transition is unlikely to be swift or easy, however. History also provides many examples of how changes in relative sectoral demand can create large and long-lasting divergences in labour market outcomes. The European Union is a case in point. There are regions where high rates of unemployment have persisted for decades following the decline of employment in certain industries, such as coal mining and steel production.

In the end, the transition will be governed by the extent to which employment creation in new sectors keeps pace with the automation of jobs in existing sectors. And it will depend on the ability of workers to acquire new skills, and potentially to relocate geographically, so that they can transfer between sectors - and on how they can be empowered to do so.

Policy implications and conclusions

With this in mind, let me conclude with some policy implications.

The first is that automation implies that protectionist policies aimed at preventing - and reversing - job losses among low-skilled workers in manufacturing are unlikely to achieve their aim.

This is because reshoring, forced or not, is ultimately the outcome of regained competitiveness and changes in relative factor intensities. Production then becomes more capital and skill-intensive and is unlikely to create many new jobs for low-skilled workers. Higher tariffs are also less effective than they were in the past, given that intra-firm trade has grown substantially. As a result, higher tariffs may well reduce domestic profitability.

In other words, policymakers need to adapt to the changing nature of global trade. As Richard Baldwin points out in his recent book, the focus on the flow of goods between countries is misplaced. The current round of globalisation relies on the flow of know-how across borders.17 As such, whereas previous industrial revolutions tended to affect mainly low-skilled workers, the current information revolution makes even mid-skilled jobs insecure.

The second implication is that policymakers need to help new industries to grow and develop. This is particularly important for services, which already account for two-thirds of global GDP and employment, and represent many of the potential growth sectors in the age of digitalisation and automation. Research by the ESCB's CompNet research network shows, for example, that many EU services sector firms are far behind the productivity frontier.18 Reallocating capital and labour towards more productive firms would help boost overall competitiveness and support employment.

For the EU, this means completing the Single Market for services. The same CompNet research points to the potential benefits of increased trade in services. Firms that have just started to export are, on average, about 15% more productive, 30% larger and pay 10% higher wages than non-exporting firms in the same narrowly defined sector. Not only are exporting firms more productive at the outset, they increase their productivity in their first year of exporting by more than comparable non-exporting firms.19

But policy actions must go beyond trade initiatives. In Europe, we need comprehensive policy action, at both EU and national level, to support workers who have lost their jobs due to technological shifts and facilitate employment in emerging industries. Certainly, this involves ensuring adequate education and retraining programmes to help smooth the transition to new employment. But it also means continuing to address structural rigidities in labour markets that may prolong and amplify secular shifts in labour demand. This includes fostering labour mobility across EU countries. Freedom of movement of workers is undoubtedly an engine of growth.

But we should also be realistic. Not everyone will benefit from the technological changes, and new solutions are needed to address these challenges. Continued high structural unemployment in some European countries shows that this is an area where policymakers have not been successful in the past.

The third implication is that the challenges of automation go far beyond employment. History corroborates this view. Technological progress in the early part of the 19th century was accompanied by a long period of stagnation in real wages, even though output per worker increased sharply.20 The late 19th century also witnessed a prolonged period of deflation brought about by technological improvement that was unpopular at the time, even though it was accompanied by strong output growth.21

The Western Balkan economies share many of the opportunities and challenges that I have discussed. Lower GDP per capita raises the opportunity to leapfrog and jump directly to the digital economy, as well as the risk of being hurt by reshoring and premature deindustrialisation. Trade openness in the region remains below that of other comparable economies in central, eastern and south-eastern Europe. This may in part reflect institutional factors, such as the effectiveness of the judiciary system or infrastructure development needs, but may also reflect competitiveness bottlenecks, including of the type I mentioned earlier. Addressing these bottlenecks at a national and at a regional level will foster trade, improve access to new, larger markets and, ultimately, accelerate convergence and income growth in the region.

Thank you.

1 I would like to thank A. Al-Haschimi for his contributions to this speech. I remain solely responsible for the opinions contained herein.

2 See e.g. Bussière, M., G. Callegari, F. Ghironi, G. Sestieri and N. Yamano (2013), "Estimating Trade Elasticities: Demand Composition and the Trade Collapse of 2008-2009," American Economic Journal: Macroeconomics 5(3): 118-151.

3 See Eurosystem staff macroeconomic projections for the euro area, December 2017.

4 See e.g. ECB (2016), "Understanding the weakness in global trade: what is the new normal?", Occasional Paper No 178, IRC Task force, September.

5 Gächter, M. and I. Gkrintzalis (2017), "The finance-trade nexus revisited: Is the global trade slowdown also a financial story?", Economics Letters, 158(C): 21-25.

6 See OECD (2013), "Global value chains: managing the risks," in Interconnected Economies: Benefiting from global value chains, Paris: OECD Publishing.

7 See Gerschenkron, A. (1962),Economic Backwardness in Historical Perspective: A Book of Essays. Belknap Press of Harvard University Press, 1962.

8 See also United Nations Conference on Trade and Development (2016), "Robots and Industrialization in Developing Countries", Policy Brief No 50.

9 In some ways, this insight is similar to the assertions made by Paul Samuelson in his famous 2004 paper, where he argued that productivity gains in one country can benefit that country alone, while permanently hurting the other country. Unlike in Samuelson's example, however, it might be developing economies that would suffer from productivity shifts today. See Samuelson, P. (2004), "Where Ricardo and Mill rebut and confirm arguments of mainstream economists supporting globalization," Journal of Economic Perspectives 18(3): 135-146.

10 See Boston Consulting Group (2015), "Made in America, Again: Fourth Annual Survey of U.S.-Based Manufacturing Executives", December.

11 See, e.g., Sirkin, H., M. Zinser and J. Rose (2015), "How Robots Will Redefine Competitiveness", Boston Consulting Group, September.

12 See McKinsey Global Institute (2017), "Jobs lost, jobs gained: Workforce transitions in a time of automation", December.

13 See Rodrik, D. (2015), "Premature Deindustrialization", NBER Working Paper No 20935.

14 See Chang, J-H., G. Rynhart and P. Huynh (2016), "ASEAN in transformation. Textiles, clothing and footwear: refashioning the future", Bureau for Employers' Activities (ACT/EMP), Working Paper No 14, International Labour Organization.

15 See Dauth, W., S. Findeisen, J. Südekum and N. Wössner (2017), "German Robots - The Impact of Industrial Robots on Workers", CEPR Discussion Paper No 12306.

16 McKinsey Global Institute (2017), op. cit.

17 See Baldwin, R. (2016), The Great Convergence: Information Technology and the New Globalization, Harvard University Press.

18 See ECB (2017), "Firm heterogeneity and competitiveness in the European Union",Economic Bulletin, Issue 2, 2017.

19 See ECB (2017), ibid.

20 See Allen, R. (2009), "Engels' pause: Technical change, capital accumulation, and inequality in the British industrial revolution", Explorations in Economic History, Vol. 46(4), pp. 418-435.

21 See Bordo, M., J. Lane. and A. Redish (2004), "Good versus Bad Deflation: Lessons from the Gold Standard Era", NBER Working Paper No 10329.