Ravi Menon: Economic dynamism amidst demographic change

Transcript of remarks by Mr Ravi Menon, Managing Director of the Monetary Authority of Singapore, at the IPS Singapore Perspectives 2018, Singapore, 22 January 2018.

Ladies and gentlemen, good morning.

- I want to first thank IPS for the opportunity to share my thoughts with this large audience.

- I would also like to commend IPS for convening a conference on what is an important, existential topic: the implications of demographic change.

- I will focus my presentation on the economic implications of demographic change: what it means for economic growth and economic dynamism. The two are different.

My presentation will centre around two broad themes.

- First, I will describe our demographic trilemma - the constraints and the choices we need to make.

- Second, I would like to argue that demographics is not destiny - why economic dynamism is not a numbers game and how we can remain dynamic amidst this demographic challenge.

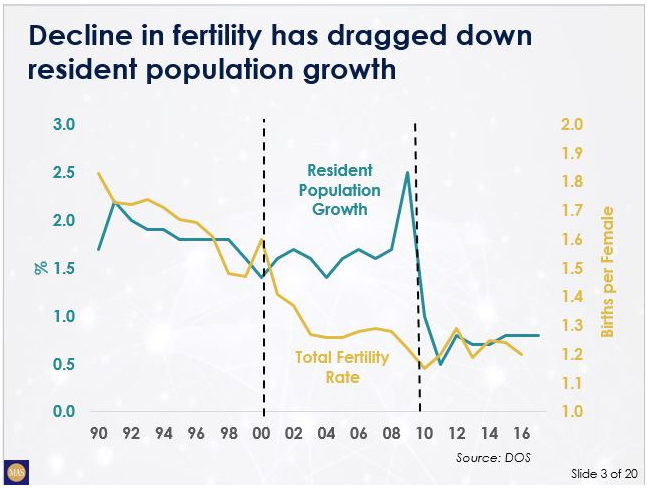

Let's start with the total fertility rate, or TFR.

- By the way, we must be one of the few countries in the world where most people know what TFR stands for! It is indeed an existential issue for us.

The TFR is the starting point of all demographic analysis.

- Singapore has had a sustained decline in its TFR.

- Our TFR fell from around 1.8 in the 1980s (which is already below the replacement level of 2.1) to about 1.3 in the early 2000s.

- This has weighed heavily on resident population growth as seen from the relatively close correlation with the TFR.

There appears to be three distinct phases in the last 30 years:

- In the 1990s, both the TFR and resident population growth declined in tandem.

- In the 2000s, the TFR continued to decline but resident population growth recovered. This reflected net positive immigration as the number of new citizens and Permanent Residents grew.

- In this decade, the TFR appears to have stabilised at around 1.2-1.3 while resident population growth fell sharply reflecting the tightening of immigration flows.

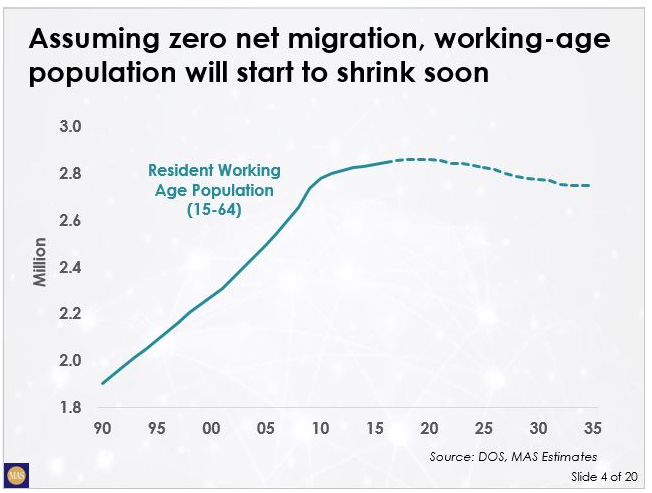

The next two slides are a thought experiment.

- They are not a forecast or prediction but aim to illustrate the implications of having very low resident population growth.

First, let us assume that we have zero net immigration starting from this year.

- The resident working-age population - this is defined as citizens and permanent residents between the ages of 15-64 - will begin to shrink from around 2020.

- The exact year is not key. What is important to note is that it is not far off.

- By 2035, the working-age resident population will possibly decline by a cumulative 3.5%.

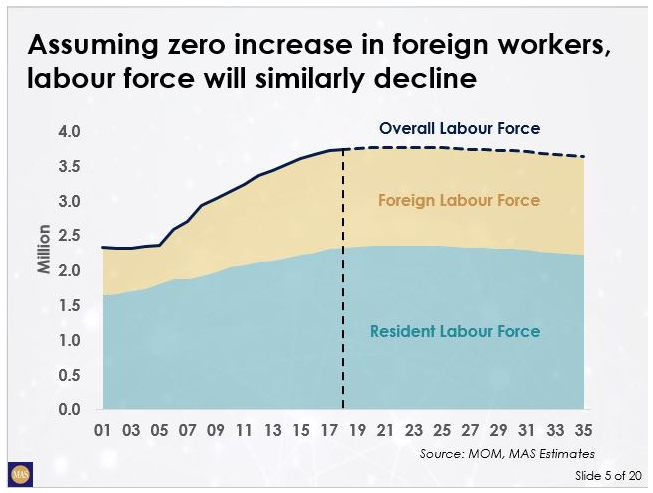

Second, let us assume zero net increase in foreign workers from now on.

- The overall labour force will decline gradually from around 2022, driven fundamentally by the shrinking resident labour force.

These two assumptions taken together - zero net migration (i.e. no additional new citizens or permanent residents on a net basis) and no additional foreign workers - will have important implications for economic growth.

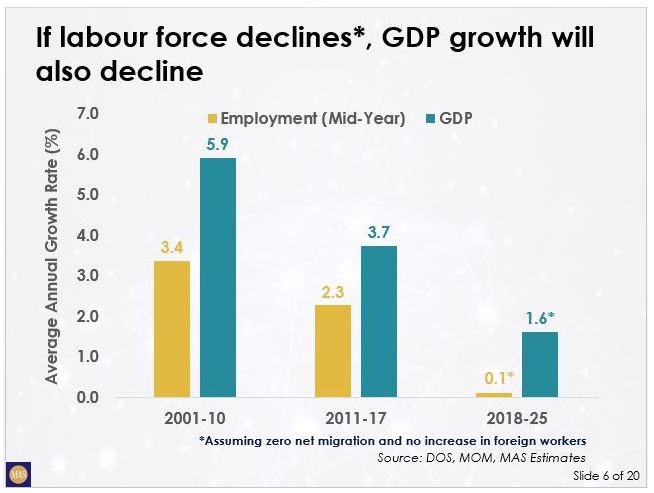

From the perspective of the supply-side capacity or potential of the economy, GDP growth can be seen as the sum of productivity growth and labour force growth.

- This means, holding productivity growth constant, a decline in labour force growth will have a direct impact on economic growth.

- This correlation appears to be borne out in the past empirically.

- If labour force growth falls to near zero, then the only source of GDP growth is productivity growth.

- If productivity growth stays at about 1.5%, which is what we have likely averaged over the last 7 years (based on mid-year employment), then GDP growth will approach that level.

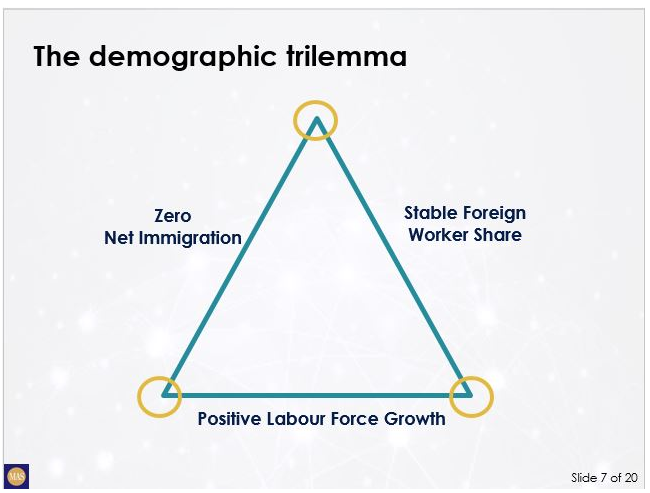

This then is the demographic trilemma.

- We have three possible objectives that various people in Singapore have advocated in the past.

- The reality is, at any one time, we can achieve only two out of the three objectives.

The three possible objectives are:

- Positive labour force expansion

- Zero net immigration, that some would prefer

- No increase in share of foreign workers in total workforce

So, what are the trade-offs? If you look at the corners of the triangle, that's where the trade-offs are:

- If we want labour force to grow and have zero net immigration, then we have to allow the share of foreign workers in the workforce to rise. That's the bottom left of the triangle.

- If we want the overall labour force to grow and the share of foreign workers to be stable, then we have to allow net immigration. That's the bottom right of the triangle.

- If we want zero net immigration and the foreign worker share to be stable, then we have to accept zero labour force growth. That's the top of the triangle.

The trilemma represents the constraints. I've put them in rather stark terms, to reflect vividly the trade-offs we face.

- Collectively, as a society, we have to decide which corner of the trilemma we want to be at, or which corner we want to be close to.

- I'll argue later on that we may be able to soften these constraints and reach more balanced outcomes.

- But the fundamental constraints and choices implied by the trilemma are real.

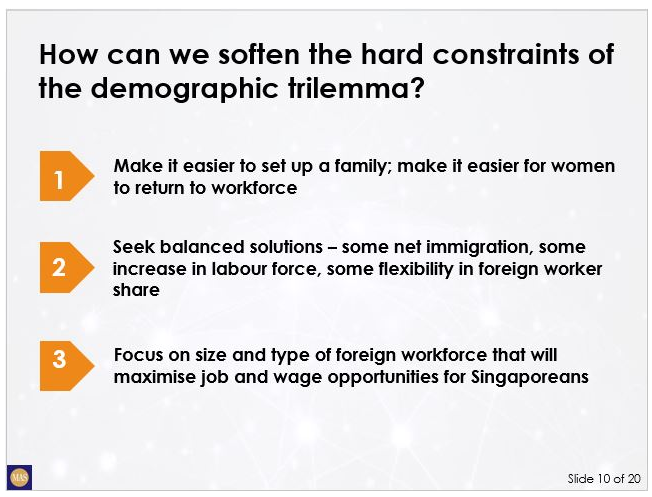

Are there ways to escape the trilemma? Or at least soften its hard constraints? There are two solutions that have often been mentioned.

- First, an increase in fertility.

- Second, an increase in resident labour force participation rate.

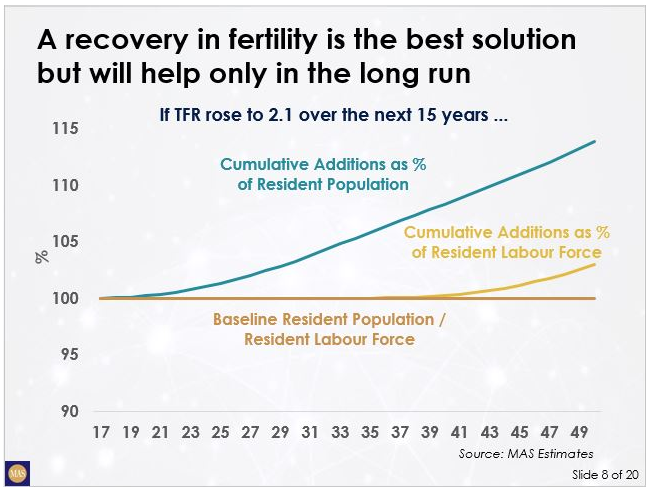

A recovery in Singapore's TFR is the best and most lasting solution that we can have, but its positive effects on labour force will only occur in the very long run.

So here's another thought experiment:

- Assume our TFR rises steadily from the current level of 1.2 to 2.1 (replacement rate) over next 15 years.

- Obviously, it will have an immediate impact on resident population and its effect will cumulate over time.

- That is shown by the blue line which is shooting up quite nicely.

- But crucially a recovery in the TFR will not have any perceptible impact on labour force and GDP growth until nearly 2040. This is shown by the yellow line.

- It will take time for the extra babies born in the next 15 years to start entering the labour force.

- So while it's the most lasting solution to our challenges, TFR effects will only impact the economy in the long run.

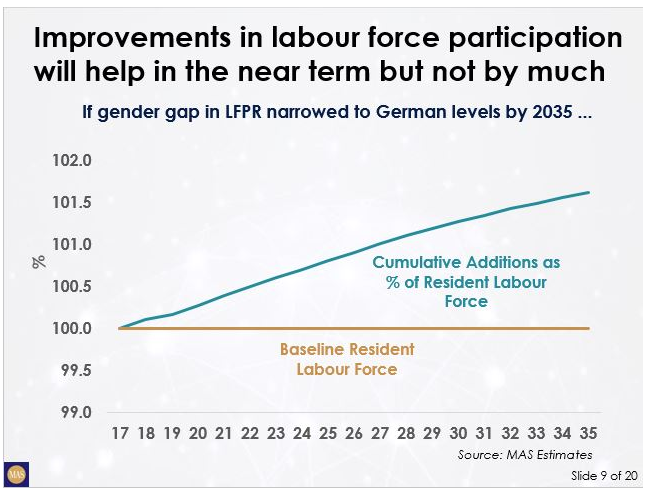

The second way to soften the trilemma is to increase our resident Labour Force Participation Rate (LFPR).

This will have more immediate payoffs.

But even at plausible stretch targets, its effects on resident labour force growth will be quite limited.

- Singapore's LFPR - defined as share of the resident population aged 15-64 who are in the labour force - is currently 76.1.

- It is not bad by OECD standards but there is scope to improve it. Japan is at 76.8; Germany is at 77.9; the Netherlands is at 79.9; Sweden is at 82.1.

- Our LFPR for older workers is not bad; it is female LFPR where we are lagging behind.

- There is currently still a fairly large gender LFPR gap between male and females in their 40s and 50s.

- This gap in Singapore is higher than that in leading OECD countries.

- In many advanced economies, women tend to return to the work force after their prime child-bearing years.

- In Singapore, this is much less prevalent.

- If we can make it easier for our women to return to the workforce after they have had their children, we can narrow the gender gap vis-à-vis the advanced economies.

- This slide demonstrates another thought experiment: assume we narrow our gender gap from the current 15% points to 11% points by 2035 - approximately the level seen in Germany and Netherlands.

- This will only translate into a cumulative labour force increase of about 2% in 2035.

The demographic trilemma presents the constraints and choices facing us.

We can soften it by raising the TFR and LFPR.

- Of course, having babies or returning to work are deeply personal choices.

- No one makes these choices in order to boost labour force growth or GDP growth, and we should not suggest doing so.

- The Government tries to facilitate fertility and labour force participation because that is what many people desire for their own fulfilment.

Many women would like to return to work, but they face a number of constraints.

- We must make it easier for them to do so.

- The government has made significant efforts in recent years to invest in childcare and facilitate more flexible working arrangements.

- We must continue to push on this front and collectively as a society enable more who want to work enter the workforce.

Likewise, many married couples want to have children - not for GDP but because children are a source of joy and fulfilment of love.

- Government policies on marriage and parenthood are guided by this higher purpose.

- And of course, a growing labour force is a happy, economic by-product.

We must make balanced choices in addressing the trilemma.

- We must accept a slower rate of labour force growth.

- The underlying demographic slowdown is so severe that it is neither feasible nor desirable to try to completely offset it through immigration or foreign workers.

- But we must also allow a certain rate of net immigration to augment our resident population.

- This is not just about numbers but about rejuvenation and expanding our talent base.

- And while we cannot keep increasing our share of foreign workforce indefinitely, we must be flexible in allowing fluctuations in the ratio according to economic cycles, changing circumstances, and opportunities.

- Finally, we must reframe our question on foreign workers.

- It is not about how many foreign workers industry wants or society can afford to have, but what number and kind of foreign workers we need to maximise the job and wage opportunities for Singaporeans.

- Foreign workers must be a complement to the local workforce.

Let me move on to the second broad theme: that demographics is not destiny.

- We can sustain our economic dynamism in the face of demographic change.

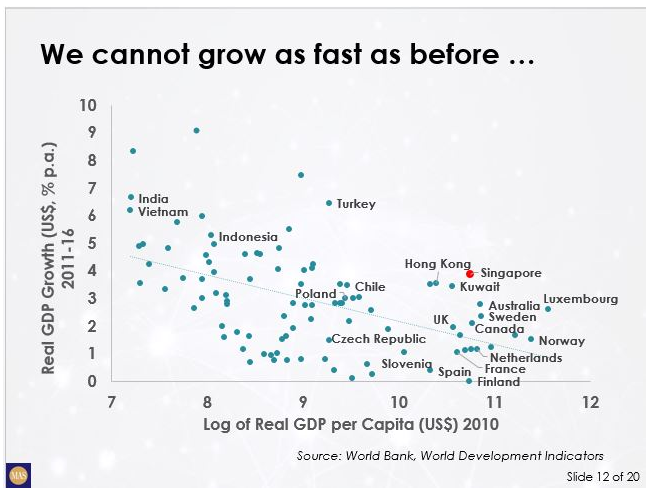

First, we should not grow despondent over our slowing rate of economic growth.

- The empirical experience of countries over time shows a negative relationship between level of income and the growth of income.

- It is not a perfect negative relationship as you can see from the scatter but it suggests that countries with low levels of GDP per capita tend to have higher rates of GDP growth. This is called "catch-up" in the literature.

- Meanwhile, countries with higher levels of GDP per capita tend to grow at slower rates as they are more mature.

- Singapore is a mature economy as you can see: it has one of the highest levels of per capita income in the world.

- We will not be able to sustain the 6-7% rates of growth that were seen a decade ago. And there's nothing to be unhappy about this.

- In fact, our position above the downward sloping line in the slide shows that we have managed to grow faster in recent years than countries with similar levels of per capita income.

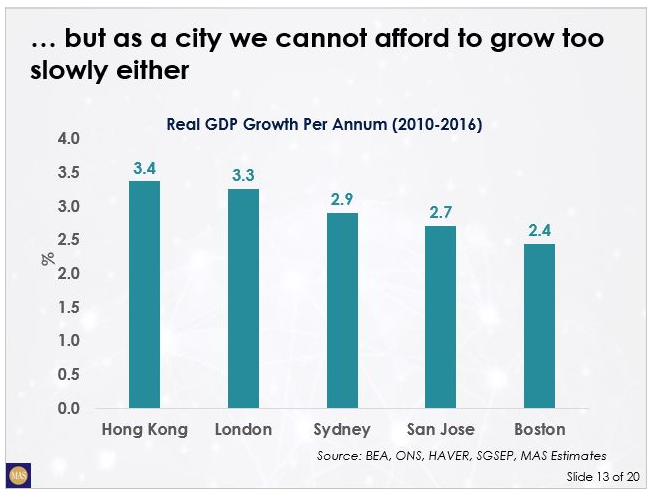

But while we must accept a lower rate of growth than before, as a global city, we cannot afford to grow too slowly either.

- It seems many leading global cities grow at rates between 2.5-3.5%, faster than the national average of the countries they are a part of.

- London has averaged 3.3% annual growth since the financial crisis while Sydney has averaged around 2.9%.

- San Jose (which encompasses Silicon Valley) has averaged 2.7% p.a.

- It is hard to imagine a dynamic city growing at less than 2% or worse still, 1.5%.

- It will be unattractive to investors and talent, including the city's own investors and talented people.

- A reasonably good rate of growth helps to create opportunities and preserve a sense of progress and hope, particularly among the young.

- It will also facilitate upward social mobility.

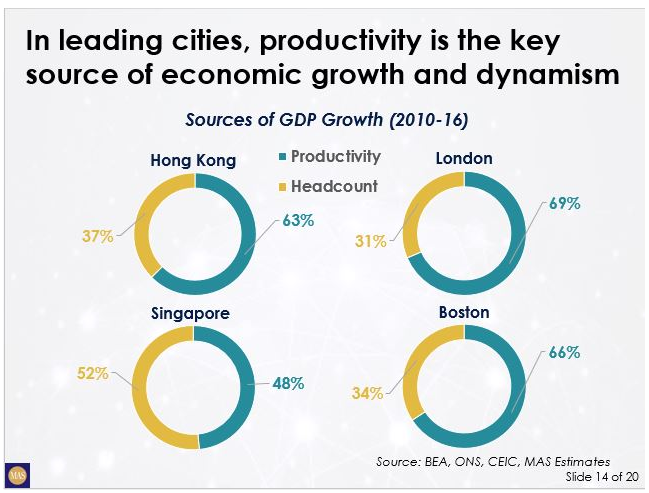

The experience of other leading cities suggests that demographics is not destiny.

- Yes, vibrant cities do attract people - and their additions to the labour force add to growth.

- But the main source of their growth and dynamism is not headcount but productivity.

- This is not an in-depth study but it appears that about two-thirds of overall GDP growth in the cities shown is due to productivity improvements.

- In comparison, productivity has accounted for about half of Singapore's GDP growth.

- There is clearly scope for us to do better and thereby sustain our dynamism.

How can we do this?

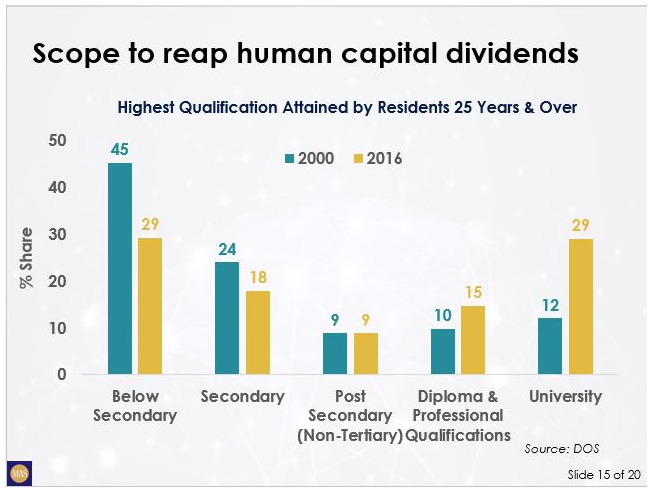

First, Singapore has scope to reap the human capital dividends that are arising from the continuous investments we have made in education and training in past decades.

- As recently as 2000, 45% of the resident workforce had below secondary school education, and only 12% had university education.

- In just one-and-a-half decades, those ratios have converged, reflecting the cumulation of efforts made over preceding decades:

- The proportion with less than secondary education has dipped below 30%;

- While the proportion of the university-educated has more than doubled to nearly 30%.

- The effects of this transformation in human capital will continue to be felt in the productive capacity of the workforce.

- With higher levels of education, the ability of the workforce to take on more complex tasks and to leverage on technology is substantially stronger.

There is more to come.

- The share of the university-educated may not continue to as rise sharply but there is still plenty of scope to increase the share of those with secondary, post-secondary and diploma & professional qualifications.

· They will be better placed to transform the nature of many jobs, raising standards and quality, thus enabling productivity and wages in these occupations to rise.

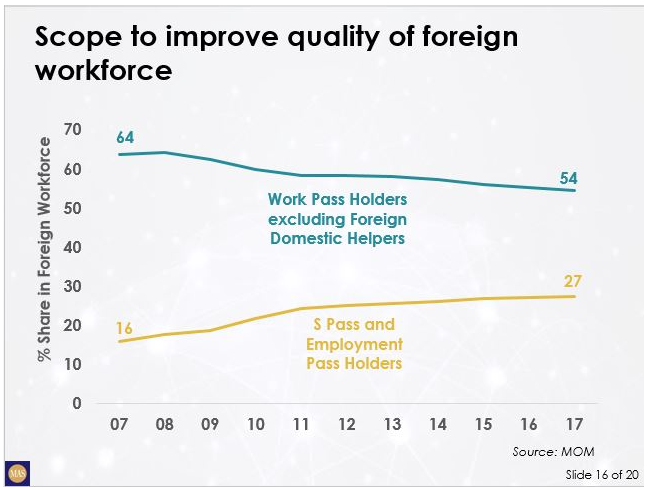

Second, there is scope to improve the quality of the foreign workforce.

- We should increasingly be concerned about the skills of the foreign workers that we take in, rather than just the numbers.

- In fact, more skilled foreign workers will mean that we will need less of them.

- The trend of improving quality in our foreign workforce has already begun.

- The proportion of work permit holders has declined by about 10 percentage points over last 10 years, while the proportion of S Pass and employment pass holders has increased by around 10 percentage points.

- This trend must continue as we restructure our economy towards higher value-added activities, seek deeper skills, and undertake more pervasive digitalisation.

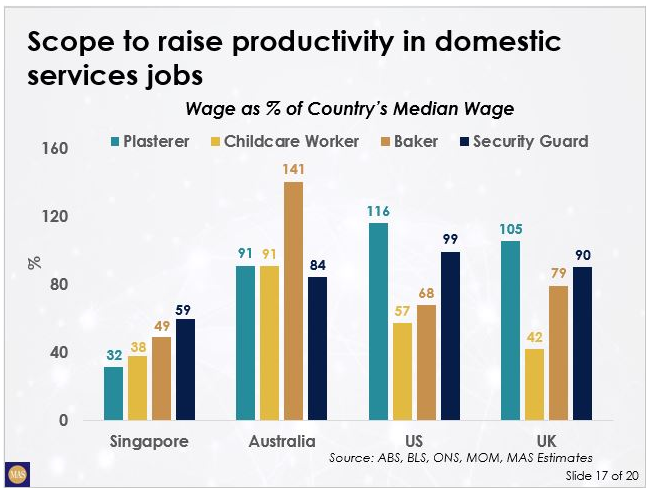

Third, there is scope to increase productivity and efficiency in many domestic services jobs.

Consider wages in four occupations (Plasterer, Childcare Worker, Baker, and Security Guard) across four countries (Singapore, Australia, US, UK).

- The slide shows the median wage in these occupations relative to the overall median wage in that country.

- In Singapore, the typical pay in these occupations range from 30-60% of the local median wage.

- In Australia, these occupations have wages much closer to the median wage.

- Wages in these occupations are also higher in the US and UK, though the pattern is slightly different across countries.

There is scope to further professionalise these jobs in Singapore.

- In particular, to increase the skills content, leverage on technology, improve business processes, and raise the quality of output.

- This will enhance productivity and help to support higher wages in these occupations.

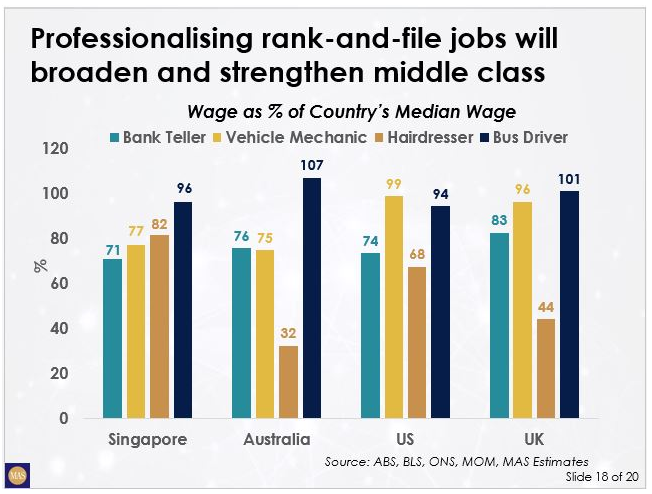

In fact, the professionalization of more of such so-called "rank-and-file" jobs in Singapore will help to strengthen and broaden the middle class, and make for a more equitable society.

- And Singapore can do this.

- We have good examples of jobs that have historically been perceived to be less skilled that have now been successfully upgraded.

- These jobs now command much relatively good wages, close to that seen in Australia, US, and UK, controlling for median incomes.

- This slide shows that our bank tellers, vehicle mechanics, hairdressers, and bus drivers earn a good (median) wage that is quite close to the median.

- In fact, our bus drivers appear to be paid just below the median in Singapore, comparable to their counterparts in Australia, US, UK.

- And hairdressers in Singapore are doing amazingly well.

- They earn much closer to the median wage compared to their counterparts in Australia, the US and the UK.

- The story of our bus drivers is interesting.

- Since the introduction of the Bus Contracting Model by the Ministry of Transport and the entrance of foreign bus operators, there has been greater competition in the bus industry, raising the game.

- Bus driving became more professional. The focus is on driving well, increasing fuel efficiency, and meeting the targets set by the Ministry of Transport on frequency and timeliness.

- More women have also been drawn into the industry with the introduction of flexible working arrangements and maternity leave.

- The result is that the dependency on foreign workers has been reduced, and productivity and wages have increased. Now our bus drivers are making close to the median wage in Singapore.

In sum, demographics is not destiny and economic dynamism is not about numbers.

- Dynamism is about quality - the quality of our workforce, the quality of our enterprises, and the quality of our institutions.

- It is about high levels of efficiency and productivity.

- It is about growing the Singaporean talent base as well as being a magnet for the world's talents.

- It is about a vibrant entrepreneurial and innovation base, characterised by a lot of start-ups, a lot of experimentation, and a lot of R&D.

A key aspect of dynamism is also high rates of churn in the labour and capital resources in our firms:

- There needs to be continuous flux and reallocation of resources in response to changing economic and market conditions.

- Both capital and labour need to be nimble and highly adaptive.

The structure of the Singapore economy is well suited for sustaining our dynamism.

- Singapore's strong advanced manufacturing and related trade and logistics activities are internationally competitive.

- In modern services, comprising financial, professional services, and info- communications technology, we enjoy an international hub status.

- Together, these sectors make up some 40% of our economy.

- If our domestic services can be further professionalised - job by job, each worker possessing deep skills and delivering a high quality of service, we will be a dynamic economy.

Finally, dynamism must be about our people.

- We must remain an open society.

- Not just in being open to foreign trade, investment, and talent, but being deeply connected to the rest of the world.

- Not just attracting foreign talent to Singapore but Singaporeans venturing abroad as our companies and industries internationalise.

- Most of all, being open in spirit and mindset, staying open to diversity, being comfortable working in multi-cultural settings, thriving in a globalised world.

- We must also remain a resilient society.

- Able to ride the ups and downs of business cycles and structural changes.

- Able to adapt, learn new skills, continually improve.

- We must become a more innovative society to be dynamic.

- Willing to experiment and accepting failure as a halfway house to success.

- Investing in R&D, leveraging on technology.

- Most of all, having an enterprising spirit - always seeking new and better ways to do things.

- In the end, we must be an inclusive society. It is probably not a coincidence that IPS has chosen to make the theme of this conference 'Together'.

- The two forces that offer the most promise for sustained economic dynamism are globalisation and technology.

- But how far we can reap the benefits of globalisation and technology will depend on how well we bring all our people together.

- The path of dynamism is also the path of continuous disruption, even dislocation.

- To sustain the momentum and consensus in favour of globalisation and technology, we must help those adversely affected by them and equip Singaporeans to succeed.

- And to maintain cohesion in the face of population ageing and growing healthcare burdens, those who have benefitted from our growth and dynamism must contribute to the larger society - through taxation, philanthropy, community service.

- We then become not just a dynamic people but also a compassionate one.

- Now that is a combination worth having, and I think the only one worth having.

Thank you.