Hiroshi Nakaso: Evolving monetary policy - the Bank of Japan's experience

Speech by Mr Hiroshi Nakaso, Deputy Governor of the Bank of Japan, at the Central Banking Seminar, hosted by the Federal Reserve Bank of New York, New York City, 18 October 2017.

Introduction

This year marks an important milestone. Nine years have passed since the collapse of Lehman Brothers in 2008, which was one of the most visible flashpoints of the global financial crisis, and ten years have passed since what should be considered as its foreshock - the emergence of the subprime mortgage problem in 2007. The global financial crisis, which brought about severe disruptions in the global financial markets and a significant downturn in the global economy, has had various impacts on the global economy to date, including the European debt problem in the 2010s. During the decade, central banks around the globe have been facing many challenges. In addressing these challenges, central banks not only conducted conventional monetary policy such as reduction of short-term policy interest rates, but also devised and proactively adopted new policy measures called unconventional monetary policy. This reflects the fact that the monetary policy framework of each central bank has evolved in accordance with their respective economic conditions, in order to overcome the zero lower bound on short-term interest rates. At the same time, however, central banks' initiatives have a lot in common, and there are many cases where similar policies have been adopted. Such similarities in the evolution of monetary policy are largely affected by the fact that the economies have been facing the same policy challenges during the same period in the wake of the global financial crisis, which brought about a significant shock on a worldwide scale. However, what seems more important is that central banks in the meantime have been strengthening their ties and establishing a relationship that has allowed them to learn from each other, which I think has served as the driving force for many of their monetary policies to evolve in the same direction during this period.

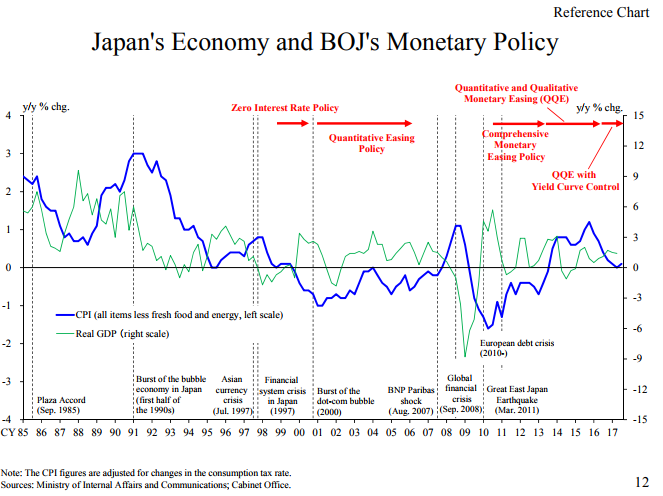

In my speech today, I would like to express my views on the evolution of monetary policy, while looking back at the Bank of Japan's experience to date, and then talk about the importance of cooperation among central banks. As some of you may not be familiar with Japan's economy and the Bank of Japan's monetary policy conduct, I have provided for your reference a chart entitled "Japan's Economy and BOJ's Monetary Policy" that shows major events for Japan's economy and monetary policy since 1985. Please refer to it as needed.

I. Japan's monetary policy before the global financial crisis

The challenge faced by central banks worldwide in conducting their monetary policy since the global financial crisis can be expressed in one phrase as "how to overcome the zero lower bound." Before the crisis, the zero lower bound was discussed among academics but was not widely recognized as an actual serious policy challenge.

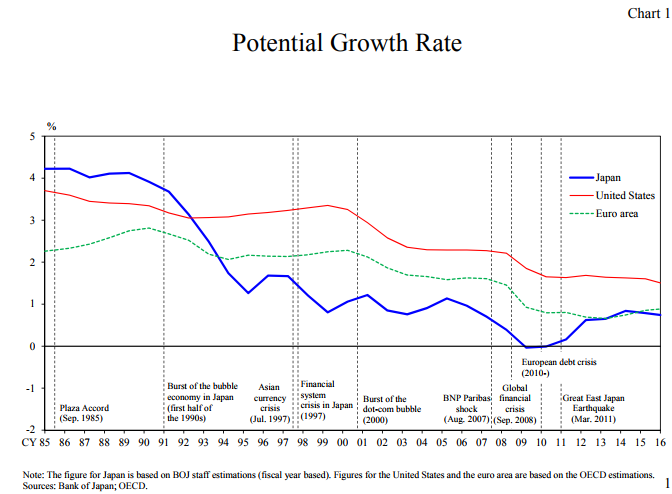

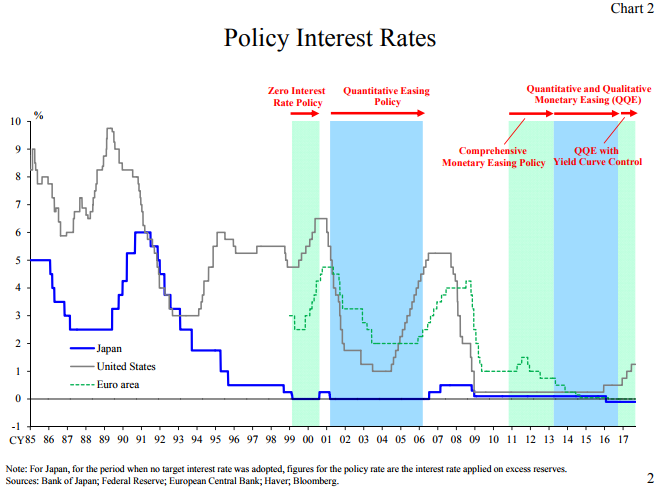

However, Japan was in an exceptional situation. Let us turn back the clock to the 1990s. At this time, Japan's potential growth rate had already started to decline, due mainly to the adverse effects of the burst of the bubble economy and the aging population (Chart 1). The potential growth rate, which had been around 4 percent in the early 1990s, declined to around 1 percent at the end of the 1990s. Along with this, the natural rate of interest, which is the real interest rate neutral to economic activity, also declined. Needless to say, the basic mechanism of monetary easing consists of driving the real interest rate below the natural rate of interest, thereby stimulating economic activity. Amid a decline in the natural rate of interest, the Bank reduced the policy interest rate incrementally, in pursuit of monetary easing effects. This is how we came to introduce the zero interest rate policy in 1999 (Chart 2). Specifically, the Bank decided in February 1999 to encourage the uncollateralized overnight call rate to move "as low as possible," which means at virtually zero percent, by providing the market with more funds than necessary for financial institutions to meet their reserve requirements. In addition, it explicitly committed to continuing with the zero interest rate policy "until deflationary concern is dispelled." While the impact of that policy was called the policy duration effect at the time, the policy is based on the same idea as what later was to be called forward guidance, in that it enhances monetary easing effects by guiding the future policy path.

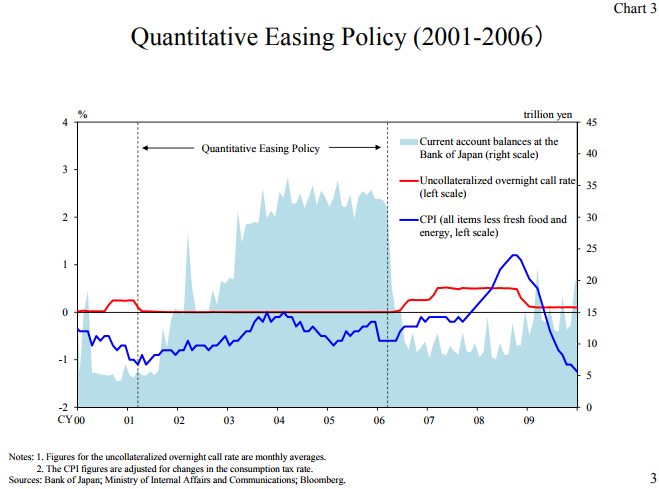

Thereafter, judging that Japan's economy was showing clear signs of recovery, the Bank lifted the zero interest rate policy in 2000. However, toward the end of that year, the economy started to decelerate again, mainly because of the effects of the burst of the dot-com bubble in the United States. In response to this, the Bank in March 2001 introduced the quantitative easing policy, which set the outstanding balance of current accounts at the Bank as the operating target (Chart 3). This policy was unique, in that it focused on the current accounts, which are on the liability side of the central bank's balance sheet. However, it paved the way for the introduction of large-scale asset purchases in many economies as well as quantitative and qualitative monetary easing (QQE) in Japan, which I will explain later, as it set not interest rates but quantity as the operating target. In addition, under the quantitative easing policy, the Bank committed to continuing the policy "until the annual rate of change in the consumer price index (CPI) registers zero percent or above in a stable manner." This new commitment was an evolution of the previous version of the commitment that had been adopted alongside the zero interest rate policy, as it linked the condition of that commitment to the observed CPI and thereby aimed at gaining more powerful monetary easing effects.

Looking back, the policy approaches at that time are applicable to the current environment, and I suppose you may not have much doubt about that. Yet, at that time, it was rather difficult to make the objectives and effects of these policies well understood. As I recall, they were considered as unique prescriptions for a certain economy, like Japan, with little implications for other economies. In fact, as we were a frontrunner of such monetary policy, we had no reliable precedents or textbooks - it was like navigating uncharted waters. I am aware that whether the policy had produced the effects as intended is open to debate. However, I take some pride in the fact that, in the face of severe economic and price developments, our strong sense of responsibility as a policy authority led to the development of new policy instruments, and that this in turn significantly affected monetary policy making around the globe in later years, both in terms of theory and practice.

II. Evolution of monetary policy since the global financial crisis

Let us now set the clock forward to 2008. Suffering a severe economic downturn triggered by the collapse of Lehman Brothers that year, central banks in major economies successively embarked on the introduction of unconventional monetary policies. At the outset, the Bank of Japan's policies, such as the zero interest rate policy and the quantitative easing policy, drew attention and often were referred to by other economies. However, as the economic downturn persisted in many economies, central banks started to accumulate their own experiences, which then allowed them to learn from each other. In the course of this process, various attempts were made to overcome the zero lower bound, accelerating the evolution of monetary policy. The direction of this evolution can be broadly described by the following four approaches.

The first is shifting the operating target to longer-term interest rates. With the zero lower bound on short-term interest rates, this measure aims to pursue a decline in real interest rates by setting the longer-term interest rates, for which room remains for a further reduction, as the target for monetary policy. As the longer-term interest rates are essentially the average of the future path of short-term interest rates plus the term premium, there are two possible ways of reducing these rates. One is to compress the term premium through longer-term lending and the purchases of government bonds by a central bank, and the other is to affect long-term interest rates by making commitments to the future path of short-term interest rates and maintaining them at lower levels. The latter is called forward guidance, which I mentioned earlier. In tackling the global financial crisis, the Federal Reserve and the European Central Bank (ECB) worked to enhance the influence on longer-term interest rates through a combination of several methods such as large-scale asset purchases and the introduction of forward guidance on short-term interest rates.

The second approach is influencing risk premiums mainly through purchases of risk assets, amid a situation of less room to reduce interest rates on risk-free assets including government bonds. This measure, referred to as qualitative easing in Japan and credit easing in the United States, aims to further reduce firms' and households' funding costs by facilitating declines in risk premiums of such assets as corporate bonds, CP, and equities. It also is an attempt to break the limit to monetary easing effects resulting from the zero lower bound.

The third approach is removing the zero lower bound by applying a negative short-term nominal interest rate. A central bank in Scandinavia for the first time after the global financial crisis developed a method to apply a negative interest rate to the central bank's accounts held by private financial institutions. Some central banks including the Bank of Japan introduced this thereafter, while making their own modifications as appropriate. As is often pointed out, interest rates cannot be reduced to arbitrarily negative levels, given the presence of banknotes in circulation. In addition, we also need to take into account various costs and risks, including the impact on financial institutions' profits. However, I think it is of notable significance that the long-held belief that nominal interest rates cannot be negative was overturned, and that the idea evolved into an actual policy option.

The fourth approach is reducing real interest rates by influencing people's inflation expectations, instead of by cutting nominal interest rates. In the case of Japan in particular, where deflation has persisted and the deflationary mindset has become entrenched among people, it is necessary to re-anchor medium- to long-term inflation expectations by exerting influence on people's expectations. This will require the central bank's strong commitment to achieving the inflation target, clear and consistent communication to the public, and determined actions to realize the commitment.

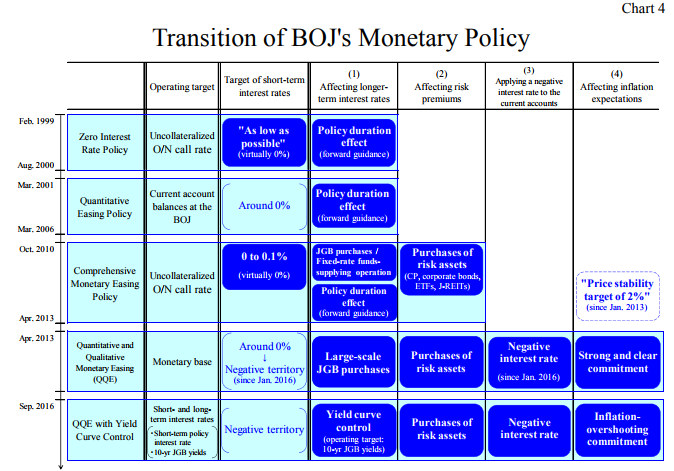

Let me now explain the Bank of Japan's monetary policy after the global financial crisis, while bearing in mind the four measures composing the evolution of monetary policy to overcome the zero lower bound that I just mentioned (Chart 4). In response to the collapse of Lehman Brothers in 2008, the Bank immediately reduced short-term policy interest rates, as did other central banks. As the pace of economic improvement remained sluggish, the Bank in October 2010 decided to introduce the comprehensive monetary easing policy. Specifically, it reduced the target level of short-term interest rates to 0 to 0.1 percent and committed itself to maintaining the virtually zero interest rate level "until it judges that price stability is in sight." In addition, it established the Asset Purchase Program, through which it provided longer-term funds at a fixed rate and purchased various financial assets such as Japanese government bonds (JGBs), corporate bonds, and exchange-traded funds (ETFs). As these measures show, in order to overcome the zero lower bound, the Bank affected longer-term interest rates through JGB purchases and forward guidance, and started to compress risk premiums through purchases of corporate bonds and ETFs. In terms of the four approaches that I explained earlier, the Bank adopted the first two.

Although the Bank continued to provide accommodative financial conditions through measures such as an expansion of the Asset Purchase Program and strengthening of forward guidance, this did not result in a significant improvement in economic activity and prices. Thus, the Bank newly introduced an extremely powerful policy package in April 2013 - namely, QQE. Under this framework, the Bank shifted the main operating target from interest rates to the monetary base, and incorporated all of the four approaches that I outlined earlier. First, it encouraged a decline in long-term interest rates more powerfully than before through large-scale JGB purchases of which the amount far exceeded that under the comprehensive monetary easing policy. Second, the purchase amount of assets, such as ETFs, was expanded substantially, thereby significantly strengthening the effects on risk premiums. Third, while this was introduced at a later date, in January 2016, with reference to measures taken by central banks in Europe, the zero lower bound itself was removed and a negative interest rate of minus 0.1 percent was applied to a portion of the Bank's current account balances. Fourth, the Bank aimed to drastically change people's expectations and thereby increase inflation expectations, by making a strong and clear commitment to achieving the price stability target of 2 percent. This commitment also was underpinned by the change in the main operating target to the monetary base and the announcement of its large-scale expansion.

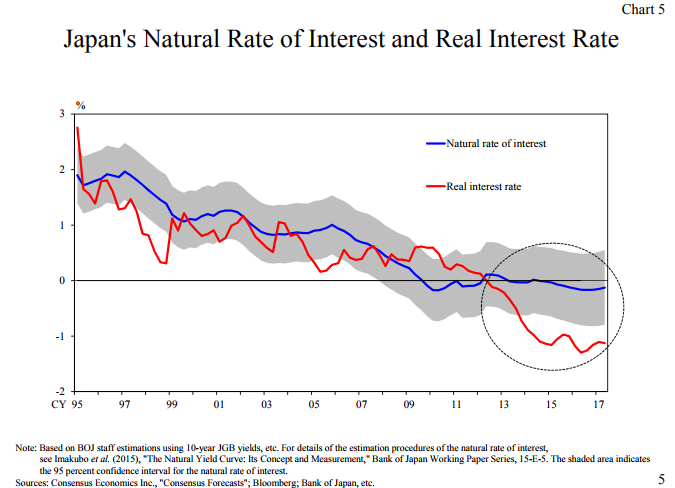

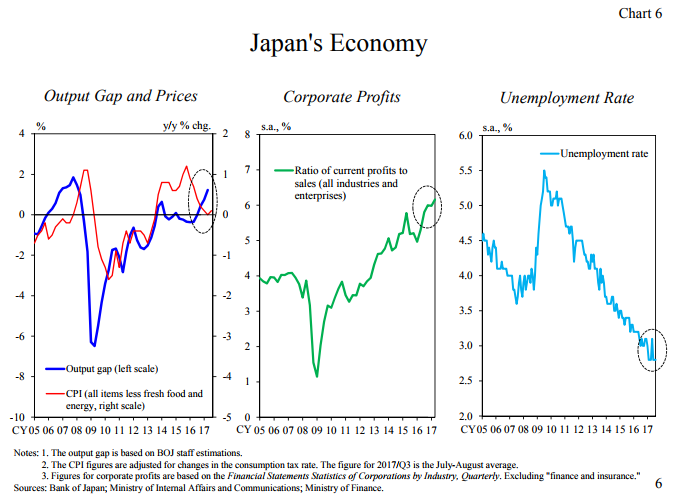

QQE has produced remarkable effects. Through the large-scale purchases of 10-year JGBs and a rise in inflation expectations, the Bank has succeeded in reducing real interest rates to levels well below the natural rate of interest for the first time in its two-decade-long battle with the zero lower bound on the short-term policy interest rate (Chart 5). As a result, Japan's economy has improved significantly over the past four and a half years (Chart 6). As the output gap improved steadily, corporate profits have been at historically high levels and the labor market is very tight, at virtually full employment. Wages have increased steadily, albeit at a moderate pace. On the price front, the year-on-year rate of change in the CPI excluding fresh food and energy has been positive as a trend for about four years. This is the first time since the end of the 1990s that such positive developments are being observed in Japan. We judge that the economy is no longer in deflation, which is generally defined as a sustained decline in prices.

III. Further evolution of monetary policy: QQE with yield curve control

As I just said, QQE has brought about a steady improvement in Japan's economy, but the price stability target of 2 percent is yet to be achieved. The main reason for this is that inflation expectations remain weak after having made a clear but temporary increase upon the introduction of QQE. Compared to the United States and Europe, inflation expectation formation in Japan is judged as being largely adaptive, meaning that the expectations are formed in accordance with developments in the observed inflation rate. Against this background, reflecting a substantial fall in crude oil prices since summer 2014 and a slowdown in emerging economies from 2015 through 2016 accompanied by turbulence in the global financial markets, the observed inflation rate declined, dragging down inflation expectations as well. The Bank aims to drastically convert the deflationary mindset entrenched among people and re-anchor inflation expectations at 2 percent, but this has met with difficulties.

Given that QQE is unprecedentedly powerful, due attention also has to be paid to side effects that could materialize going forward. If an excessive decline in and a flattening of the yield curve were to last for too long under powerful monetary easing, risks of a pullback in financial intermediation and of destabilizing the financial system through downward pressure on financial institutions' profits could not be ignored. If these risks were to materialize, the transmission mechanism of monetary easing would be hampered and it would become more difficult to achieve price stability and sustainable economic growth in a self-fulfilling manner. It was judged that the Bank has to achieve the most appropriate interest rate level with a view to containing such side effects to the minimum.

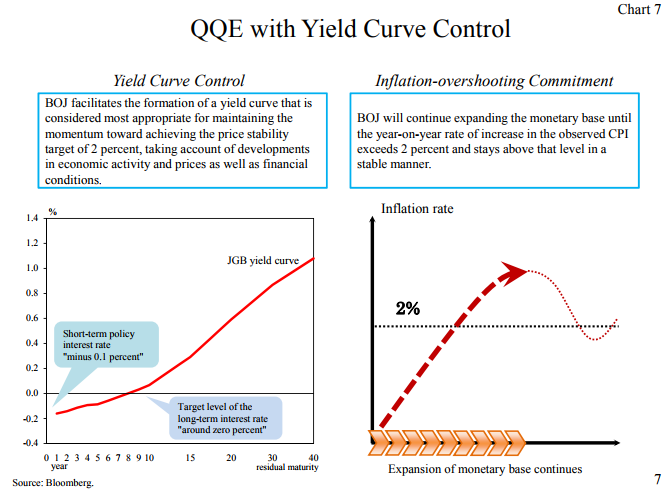

Bearing these issues in mind, the Bank introduced "QQE with Yield Curve Control" last September. This new policy framework was established through a further evolution of QQE, consisting of mainly two components (Chart 7). The first is yield curve control, which was introduced with the aim of realizing the combination of the levels of interest rates that are deemed most appropriate for maintaining the momentum toward achieving the price stability target of 2 percent, while also considering the effects on the functioning of financial intermediation. Under this framework, Japan's yield curve during this one year has been formed smoothly in a manner consistent with the guideline for market operations, in which the short-term policy interest rate is set at minus 0.1 percent and the target level of the 10-year JGB yields at around zero percent. The second component is an inflation-overshooting commitment, which aims at ensuring that inflation expectations will be anchored at 2 percent. This is a further powerful commitment by the Bank; namely, it is committing itself to expanding the monetary base until the year-on-year rate of increase in the observed CPI exceeds 2 percent and stays above that level in a stable manner. The key point is that the commitment is based on the observed CPI, not the outlook. We judged that, in Japan, where inflation expectation formation is largely adaptive, people's perception of prices cannot be changed without experiencing the inflation rate actually exceeding 2 percent for some time, and this is why this commitment was introduced.

The novelty of yield curve control lies in the feature that it more directly affects long-term interest rates with setting 10-year JGB yields as the operating target. This is a further reinforcement of the first approach of the aforementioned category of evolution. The inflation-overshooting commitment can be regarded as a further enhancement of the fourth approach, as the aim is to work on people's inflation expectations more strongly. With these two unprecedented and innovative policy tools, the Bank of Japan once again embarked on navigating the uncharted waters of unconventional monetary policy. As a matter of fact, I received many questions in the past year, such as those regarding the actual operation of yield curve control. Today, I would like to take the opportunity to answer some of those key questions.

The first question is whether the Bank's current operating target is quantity or interest rates. As I mentioned earlier, the current monetary policy aims to facilitate the formation of a yield curve that is deemed most appropriate for maintaining the momentum toward achieving the price stability target of 2 percent, so in that sense, the answer is "interest rates." The most appropriate shape of the yield curve cannot be formed by fixing the amount of JGB purchases as an operating target. This is because, even though the same amount is to be purchased, the degree to which interest rates will be lowered depends on the economic and inflation conditions as well as the conditions of the JGB market. In contrast, yield curve control enables the Bank to purchase just the right quantity of JGBs in a flexible and effective manner to achieve the operating target of the policy. Consequently, the amount of JGB purchases is determined endogenously. In addition, even if JGBs to be purchased by the Bank become scarce at some point in the future, the impact of a unit amount of its JGB purchases on long-term interest rates accordingly should become more significant, with all else being equal. This means that, under yield curve control, the Bank can achieve the same interest rate level with a smaller amount of JGB purchases. Yield curve control is designed to be flexible and highly sustainable, through which the most appropriate level of interest rates can be achieved in line with developments in economic activity and prices as well as financial conditions.

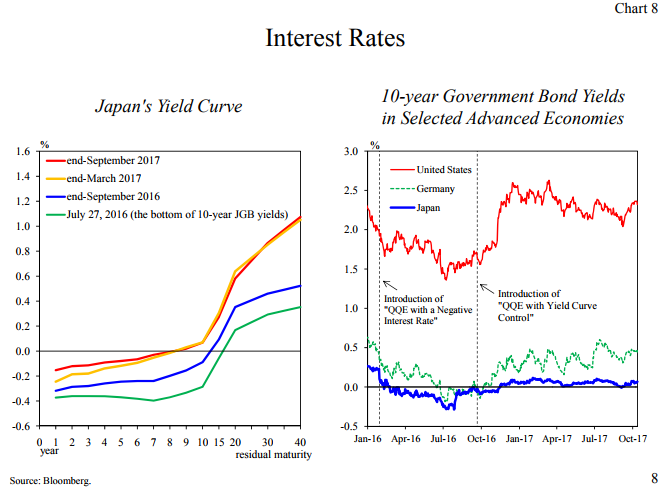

The second question, given that interest rates are set as an operating target, is whether controlling long-term interest rates is operationally feasible in the first place. It is obvious from the past year's experience that the answer is "yes" (Chart 8). While central banks have a dominant power to control short-term interest rates, which can be referred to as prices of the monetary base, long-term interest rates are determined by market participants' outlook for future developments in short-term interest rates as well as by various risk premiums. Therefore, the conventional view is that central banks can control short-term interest rates but not long-term interest rates. However, as I mentioned earlier, many central banks have been making efforts to exert influence on longer-term interest rates in order to overcome the zero lower bound, and yield curve control would be the ultimate example in terms of the range of maturity of interest rates to be controlled and the level of sophistication of such control. Admittedly, controlling the interest rates is a challenge. But the Bank of Japan has a dominant presence in the market and has built up its experiences of large-scale asset purchases for the past few years. It conducts purchase operations in different maturities across the yield curve and is equipped with a powerful supplementary tool - the fixed-rate full-allotment operations - through which it can purchase an unlimited amount of JGBs at a certain interest rate level. Therefore, I believe it is quite possible to continue to facilitate the formation of a yield curve that is deemed most appropriate for achieving the price stability target of 2 percent, although not as precisely as controlling short-term interest rates. That said, in order to form such yield curve smoothly, I want to underline the importance of closely communicating with market participants. I have full confidence in the operational skills, including this aspect, of our Market Operations Desk.

The third question, assuming that it is possible to control the level of long-term interest rates, is how to determine the desirable shape of the yield curve. Under the conventional monetary policies, various benchmarks have been devised to determine the desirable level of short-term interest rates. The Taylor rule would be one of the most famous benchmarks. However, the Bank of Japan needs to establish a new benchmark that can be applied to the entire yield curve, not to a single short-term interest rate alone. As part of devising such benchmarks, it has been proceeding with theoretical and empirical analysis from many aspects. These efforts include measuring the natural yield curve, which can be obtained from expanding the concept of the natural rate of interest, and comparing it with that during the past easing phase. Although not a few issues remain in terms of research, the Bank will make adjustments to the shape of yield curve as necessary, while making use of the outcome of analyses and taking into account developments in economic activity and prices as well as financial conditions.

IV. Expansion of monetary policy

Monetary policy and financial stability policy

I have explained so far how central banks overcame the zero lower bound and their monetary policy made progress. Let me add that the direction of our monetary policy evolution is not necessarily limited to what I have described thus far.

During the global financial crisis, the central banks were confronted with new challenges to maintaining financial stability. First, it was recognized that not only banks but also nonbanks can be sources of systemic disruption, as clearly demonstrated by the collapse of Lehman Brothers. Second, there is a possibility that, once market participants become extremely concerned about the creditworthiness of counterparties, an entire market could run out of liquidity as a result of having no counterparties in the market. This situation was realized with the collapse of Lehman Brothers in 2008. At that time, the liquidity squeeze spread from the interbank market to firms' major funding markets, including those for CP and corporate bonds. It was feared that the breakdown of corporate financing would stagnate business activities and thus the entire economy. Third, the central banks had to ensure access by foreign financial institutions in their own jurisdictions to not only the domestic currency liquidity but also foreign currency liquidity, in particular U.S. dollars. This was reflective of the fact that more financial institutions came to be engaged in operations in multiple currencies.

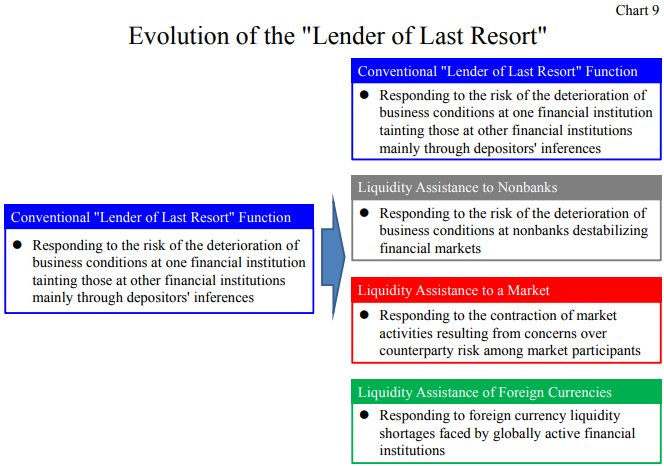

In order to effectively address these new challenges to financial stability, many central banks extended liquidity assistance as the lender of last resort beyond what had been considered the norm under the so-called Bagehot's rule (Chart 9). Specifically, they provided liquidity assistance to nonbanks to address the risk that deterioration of business conditions at nonbanks could destabilize the financial markets. As a counterparty to many market participants, they conducted funds-supplying operations to revive the markets that had become dysfunctional, and swiftly provided financial institutions with funding liquidity at a large scale in foreign currencies in addition to domestic currencies.

When one groups the functions of central banks into monetary policy and financial stability policy, central banks' policy responses since the global financial crisis fall under the heading of financial stability policy if one emphasizes the aspect of addressing systemic risks. On the other hand, since the financial market is one of the key transmission channels of monetary policy, repairing the impaired market functioning can be deemed part of monetary policy. However, taxonomy does not really matter; the important thing is what is to be done by the central banks, consistent with their mandates. The policy of central banks, either in the form of monetary policy or financial stability policy, is achieved through the provision of liquidity because it is only the central banks that can provide unlimited liquidity. This is why they are expected to keep evolving in order to carry out their mission as a central bank irrespective of which policy area they are categorized into.

Global cooperation of central banks

The significant advancement in global cooperation and coordination has been a big change for central banks in recent years. As I said earlier, during the global financial crisis, it was recognized that it was becoming difficult for the central bank of a home country alone to prevent a liquidity crisis if a financial institution with a global reach faces foreign currency liquidity shortages.

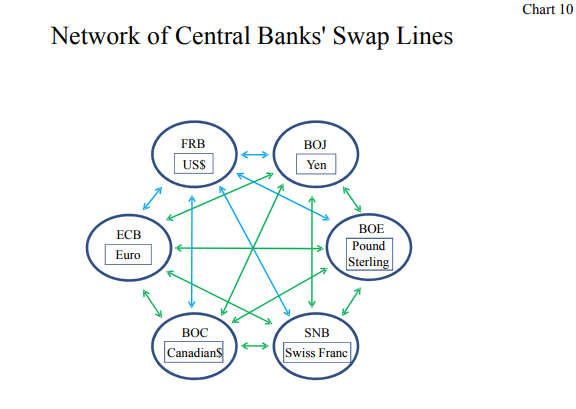

In the meantime, the Federal Reserve entered into a swap arrangement with the ECB and the Swiss National Bank at end-2007, establishing a scheme that could swiftly provide U.S. dollars. Right after the collapse of Lehman Brothers, the Bank of England and the Bank of Japan also entered into swap arrangements with the Federal Reserve, and largely contributed to a stabilization in the global financial markets as an effective backstop to contain the U.S. dollar liquidity crisis. In 2011, when the tension surrounding the European debt problem heightened, six major central banks established a network of bilateral liquidity swap arrangements so that liquidity could be provided in each jurisdiction in any of their currencies. In 2013, the arrangements converted to standing agreements, which remain in place (Chart 10).

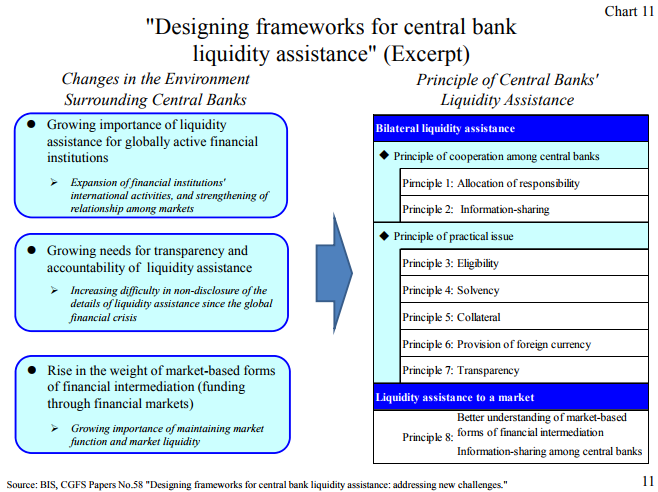

Although the collective efforts by the central banks resulted in substantial progress in addressing a financial crisis that is global in nature, we became aware of unsolved open issues. These include the allocation of responsibility among relevant central banks, the treatment of collateral, and information sharing, in the case of internationally active banks and nonbanks facing difficulty in funding. I have discussed these matters over the years with President Dudley of the Federal Reserve Bank of New York, who also serves as Chairman of the Committee on the Global Financial System (CGFS) of the Bank for International Settlements (BIS). Under his leadership, a report titled "Designing frameworks for central bank liquidity assistance: addressing new challenges" was compiled by a working group of the CGFS, at which I took the chair (Chart 11). This report analyzes in detail the issues that many central banks faced during the global financial crisis and highlights eight operational challenges that need to be addressed going forward. Assuming that the next financial crisis - if it were to occur - would have a global impact, I sincerely hope that central bankers in the next generation will address these challenges in advance.

Closing remarks

It seems we are almost running out of time. Based on the Bank's long experience of working on addressing financial crises and overcoming deflation, I would like to close my speech today by emphasizing the importance of becoming an experienced practitioner.

Over the past decade, central banks have faced various difficulties and the monetary policy framework has been changing dynamically. Every time central banks faced tough challenges and decided to introduce unprecedented policy measures - such as large-scale asset purchases and negative interest rates - the decision was made based on the operational feasibility, for example, of monetary operations and whether a close cooperative relationship between a central bank and market participants is well established. Needless to say, we, as central bankers, should study the latest theories and make efforts to enhance analytical ability. However, while that is necessary, it is not sufficient to swiftly deal with issues that actually unfold. Policymakers cannot run away from the challenges they face on the grounds that they do not have enough theoretical background. A central banker must be strongly mission-oriented in a manner consistent with the central bank's mandate and make necessary and timely decisions, fully being aware of policy effects and possible accompanying costs, while being accountable. To ensure the right decisions, we have to constantly upgrade our skills as practitioners while listening carefully to what market participants have to say.

Today, I have focused on unconventional monetary policy, although whether the policy is actually unconventional or not can only be determined on a relative basis and perhaps through the use of retrospective wisdom. After all, contemporary monetary policy has not yet allowed for the accumulation of sufficient experience to enable us to define conventional monetary policy. The evaluation of the experience gained over the decade in the course of monetary policy's evolution and the decision of how to move forward shall be made by you, who are responsible for the next generation.

The central banking community is a very special one in which common values and cultures are shared. That is why we say "once a central banker, always a central banker." Looking back at the almost 40 years of my service at the central bank, there was not a single moment when I regretted being a central banker. I can assure you that the cooperation and personal relationships with central bankers in other countries is irreplaceable and invaluable for all of you. I do hope that you will make the most of the opportunity, like today's seminar, to meet other countries' central bankers of the same generation in person and build ties within the central banking community. I would like to conclude my speech by once again welcoming you all to the central banking community and expressing my hope that your journeys in central banking life continue to be interesting and exciting.

Thank you.