Viral V Acharya: The unfinished ageda - restoring public sector bank health in India

Speech by Dr Viral V Acharya, Deputy Governor of the Reserve Bank of India, at the 8th R K Talwar Memorial Lecture, organised by the Indian Institute of Banking and Finance, Mumbai, 7 September 2017.

I would like to thank Vaibhav Chaturvedi, B Nethaji and Vineet Srivastava for valuable inputs, as well as my co-authors, Tim Eisert, Christian Eufinger and Christian Hirsch (parts of the Japanese and the European stories are based on joint work with them). All errors remain my own. Views expressed do not necessarily reflect those of the Reserve Bank of India.

Good evening, friends. I am grateful to the Indian Institute of Banking and Finance (IIBF) for inviting me to deliver the 8th R K Talwar Memorial Lecture. Every institution must remember, venerate and celebrate the immense contributions of those who helped lay down and solidify its character for future generations to build upon. Principles, careers and lives such as those of Mr Talwar inspire us, as in Henry Wadsworth Longfellow's The Psalm of Life:

Lives of great men all remind us

We can make our lives sublime,

And, departing, leave behind us

Footprints on the sands of time;

Footprints, that perhaps another,

Sailing o'er life's solemn main,

A forlorn and shipwrecked brother,

Seeing, shall take heart again.

I hope that I can do some justice today to the rich legacy left behind by Mr Talwar, considered as the State Bank of India (SBI)'s greatest Chairman, the father of Small Scale Industries in India, a banker ahead of his times who put tremendous emphasis on a comprehensive credit appraisal culture at SBI, and someone who had the courage to stand up against political pressure on his bank to undertake targeted lending to undeserving borrowers (an episode recollected in a booklet by another stalwart of Indian banking, Mr Narayanan Vaghul).

I was originally planning to speak on "Monetary Transmission in India: Issues and Possible Remedies", but I have since had a change of heart. The Reserve Bank's internal committee on improving monetary policy transmission will be finishing its report by the last week of September. I should neither pre-judge nor pre-announce its findings. Therefore, and at the cost of belabouring some of my remarks earlier in the year, I will focus on what remains, to my mind, the most important unfinished agenda in the journey we have embarked upon to resolve our stressed assets problem, viz., that of restoring public sector bank health in India. I will indirectly end up conveying why bank credit growth and transmission are weak at the present.

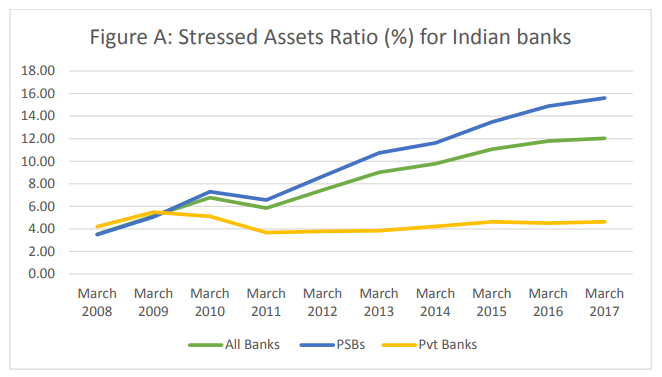

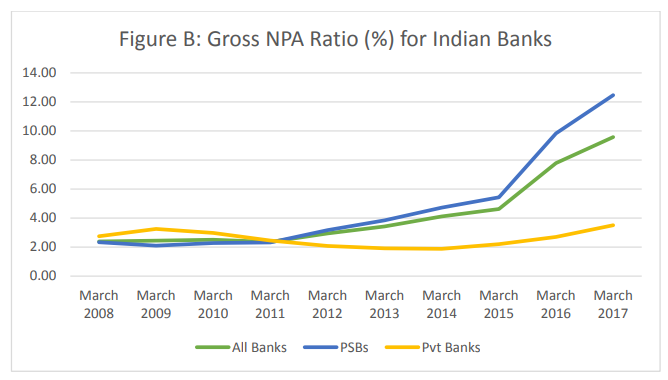

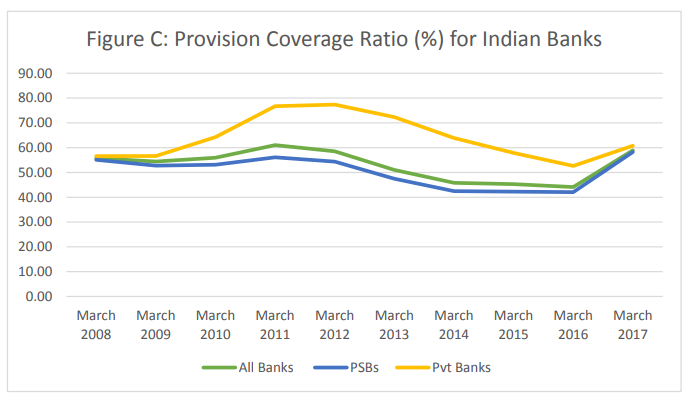

I would like to contend that a primary cause for the recent slowdown in our growth is the stress on the banking sector's balance-sheet, especially of public sector banks. As Figures A and B show using the Reserve Bank's data, the stress in bank assets has been mounting since 2011 and has now materially crystallized in the form of non-performing assets (NPAs). Some banks are under the Reserve Bank's Prompt Corrective Action (PCA) having failed to meet asset-quality, capitalization and/or profitability thresholds; others meet these thresholds for now but are precariously placed in case the provisioning cover for loan losses against their gross non-performing assets (Figure C) is raised to international standards and made commensurate with the low loan recoveries in India.

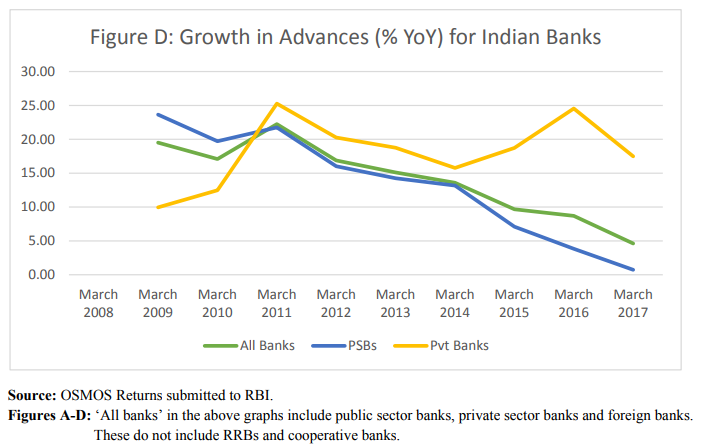

When bank balance-sheets are so weak, they cannot support healthy credit growth. Put simply, under-capitalized banks have capital only to survive, not to grow; those banks barely meeting the capital requirements will want to generate capital quickly, focusing on high interest margins at the cost of high loan volumes. The resulting weak loan supply (see in Figure D, the steady decline in loan advances growth since 2011 for public-sector banks), and the low efficiency of financial intermediation, have created significant headwinds for economic activity.

A decisive and adequate bank recapitalization, options for which I will lay out (again) at the end of my remarks, is a critical intervention necessary to address this balance-sheet malaise.

In a recent study from the Bank for International Settlements, Leonardo Gambacorta and Hyun-Song Shin (2016) document that bank capitalization has a strong effect on bank loan supply: a one percentage point increase in a bank's equity-to-total assets ratio is associated with a 0.6 percentage point increase in its yearly loan growth. In fact, if a banking system remains systematically undercapitalized and new lending is not kept under a tight supervisory watch, then the economy can suffer significantly from a credit misallocation problem, now commonly known as 'loan ever-greening' or 'zombie lending'. In particular, undercapitalized banks have an incentive to roll over loans from financially struggling existing borrowers so as to avoid having to declare these outstanding loans as non-performing. With these zombie loans, the impaired borrowers acquire enough liquidity to be able to meet their payments on outstanding loans. Banks thus avoid the short-run outcome that these borrowers might default on their loan payments, which would lower their net operating income, force them to raise provisioning levels, and increase the likelihood of them violating the minimum regulatory capital requirements. By ever-greening these loans, banks effectively delay taking a balance-sheet hit, while taking on significant risk that their borrowers might not regain solvency and remain unable to repay, now even larger loan payments. While unproductive firms receive subsidized credit to be just kept alive, loan supply is shifted away from more creditworthy firms.

Adequate bank, more generally, financial intermediary, capitalization is thus a pre-requisite for efficient supply and allocation of credit. Its central role in supporting economic growth is consistent with what other economies and regulators have experienced in the past episodes of banking sector stress. I will cover briefly the Japanese crisis in the 1990s and early 2000s, and the European crisis since 2009. Professor Ed Kane (1989), Boston College, had reached similar conclusions for the United States based on the Savings and Loans crisis of the 1980s.

The Japanese story

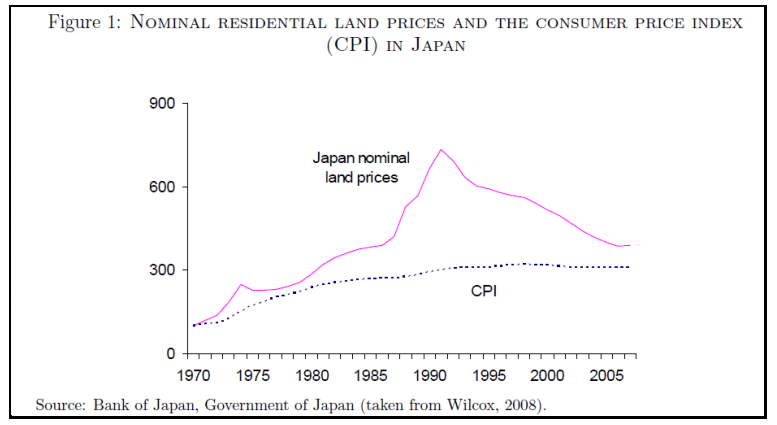

In the early 1990s, a massive real estate bubble collapsed in Japan (see Figure 1). This caused problems for Japanese banks in two ways: first, real estate assets were often used as collateral; second, banks held the affected assets directly, so that the decline in asset prices had an immediate impact on their balance sheets. These problems in the banking system quickly translated into negative real effects for borrowing firms along the lines I laid out above.

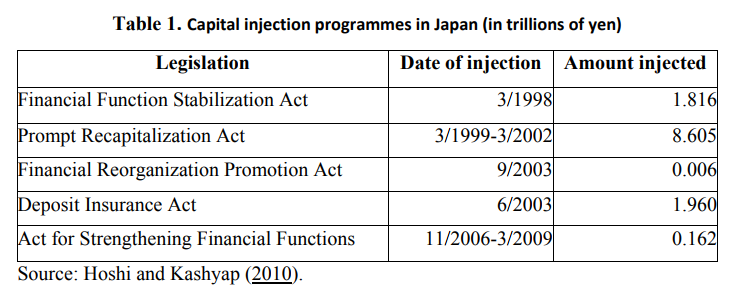

Subsequently, the Japanese government introduced several measures to stabilize the banking sector and spur economic growth. Among these measures were a series of direct public capital injections into impaired banks, mostly in the form of preferred equity or subordinated debt. However, as conclusively shown by Table 1from Takeo Hoshi and Anil Kashyap (2010), bulk of the injections came after 1999, close to a decade after the collapse; the economic scale of earlier recapitalizations was small relative to that of banking sector's real estate exposure so that these half-hearted measures failed to adequately recapitalize the Japanese banking sector.

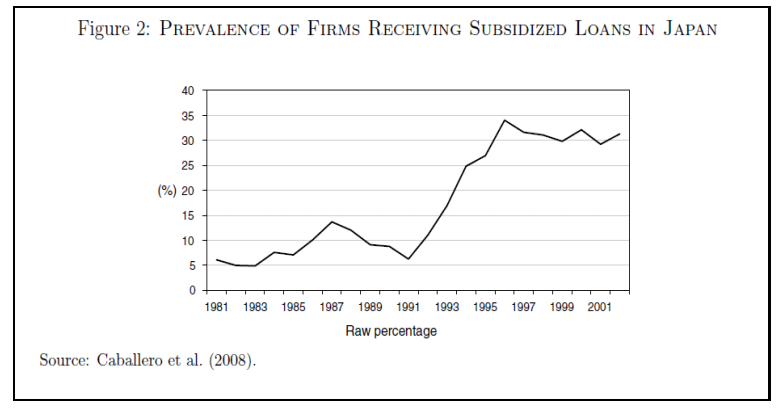

In turn, this misallocation of loans translated into significant negative effects for the real economy. Because zombie lending kept distressed borrowers alive artificially, the respective labor and supply markets remained congested; for example, product market prices were depressed and market wages remained high. Sectoral capacity utilization also remained low, which destroyed the pricing power and attractiveness of investments for healthy firms competing in the same sectors. Ricardo Caballero, Takeo Hoshi and Anil Kashyap (2008) showed that, as a result of these spillover effects, healthy firms that were operating in industries with a high prevalence of zombie firms had lower employment and investment growth than healthy firms in those industries that did not suffer from zombie firm distortions. They estimated that due to the rise in the number of zombie firms, typical non-zombie firm in the real estate industry experienced a 9.5% loss in employment and a whopping 28.4% loss in investment during the Japanese crisis period.Joe Peek and Eric Rosengren (2005) were among the first to provide evidence that this inadequate recapitalization of the Japanese banking sector had major consequences for the allocation of credit to the real economy. Specifically, they showed that firms were more likely to receive additional loans if they were in fact in poor financial condition. They interpreted this finding as being consistent with the 'zombie lending' incentives of undercapitalized banks. Figure 2 shows that the percentage of zombie firms increased from roughly 5% in 1991 to roughly 30% in 1996. In related work, Mariassunta Giannetti and Andrei Simonov (2013) found that banks that remained weakly capitalized after the introduction of the recapitalization programmes provided loans to impaired borrowers, while well-capitalized banks increased credit to healthy firms. The authors estimated that the credit supply to healthy firms could have been 2.5 times higher in 1998 if banks had been recapitalized sufficiently.

The European story

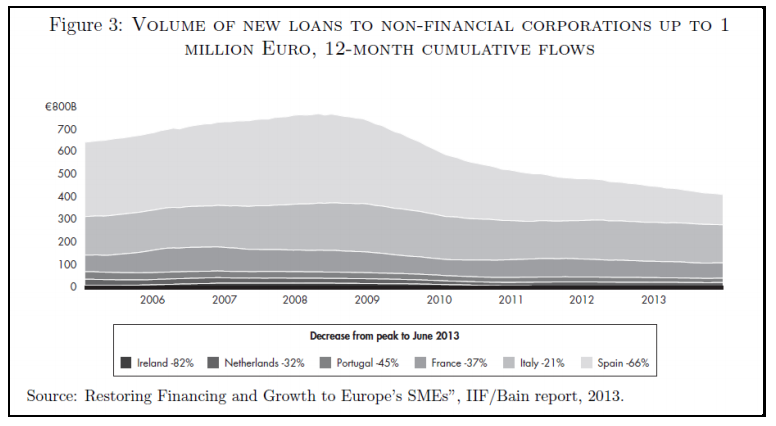

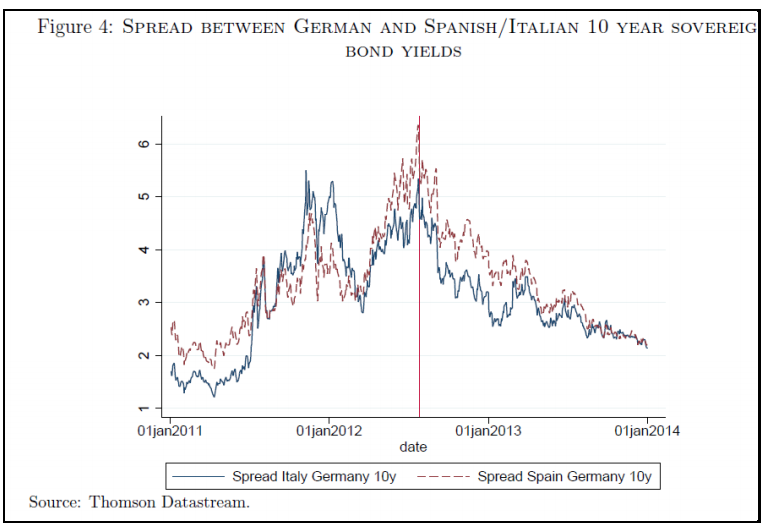

In recent years, the Eurozone has been following a similar path to that of the Japanese economy in the 1990s and early 2000s. Starting in 2009, countries on the periphery of the Eurozone drifted into a severe sovereign debt crisis. At the peak of the European debt crisis, in 2012, anxiety over excessive levels of national debt led to interest rates on government bonds issued by countries in the European periphery that were considered unsustainable. For instance, from mid-2011 to mid-2012, the spreads of Italian and Spanish 10-year government bonds increased by 200 and 250 basis points, respectively, relative to German government bonds. Since this deterioration in the sovereigns' creditworthiness fed back into the financial sector (Acharya et al, 2015), lending to the private sector contracted substantially in Greece, Ireland, Italy, Portugal, and Spain (the 'GIIPS' countries), as shown in Figure 3. In Ireland, Spain, and Portugal, for example, the volume of newly issued loans fell by 82%, 66%, and 45% over the 2008-13 period, respectively.

However, the impact of the European debt crisis on bank lending is more complex than in the case of the Japanese banking crisis, which was mainly caused by the bursting of an asset price bubble and the resulting impairment of banks' financial health. While the European debt crisis also caused a hit on banks' balance sheets due to the substantial losses on their sovereign bond-holdings, in addition it created gambling-for-resurrection incentives for weakly capitalized banks from countries in the European periphery. These banks sought to increase their risky domestic sovereign bond-holdings even further as they were an attractive bet to rebuild capital quickly given zero risk-weights. This incentive led to a crowding-out of lending to the real economy, thereby intensifying the credit crunch (Acharya and Steffen, 2014).

This vicious cycle of poor bank health and sovereign indebtedness became a matter of great concern for the European Central Bank (ECB), as this cycle endangered the monetary union as a whole. As a result, the ECB began to introduce unconventional monetary policy measures to stabilize the Eurozone and to restore trust in the periphery of Europe. Especially important in restoring trust in the viability of the Eurozone was the ECB's Outright Monetary Transactions (OMT) programme, which ECB President Mario Draghi announced in his famous speech in July of 2012, saying that "the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough."

There is now ample empirical evidence that the announcement of the OMT programme significantly lowered sovereign bond spreads, as shown by Figure 4. By substantially reducing sovereign yields, the OMT programme improved the asset side, the capitalization, and the access to financing of banks with large GIIPS sovereign debt holdings.

Due to its positive effect on banks' capital, it was expected that the OMT announcement would lead to an increase in bank loan supply, thus benefiting the real economy. However, when Mario Draghi reflected on the impact of the OMT programme on the real economy during a speech in November 2014, he noted that "[T]hese positive developments in the financial sphere have not transferred fully into the economic sphere. The economic situation in the euro area remains difficult. The euro area exited recession in the second quarter of 2013, but underlying growth momentum remains weak. Unemployment is only falling very slowly. And confidence in the overall economic prospects is fragile and easily disrupted, feeding into low investment."

An important reason why the positive financial developments did not fully transfer into economic growth is as follows: An indirect recapitalization measure like the OMT programme produced Treasury gains for banks (much like our policy-rate cuts do); such a measure allows the central bank to benefit banks that hold troublesome assets, but it does not tailor the recapitalization to banks' specific needs. As a result, some European banks remained significantly undercapitalized from an economic standpoint even post-OMT.

In joint work with Tim Eisert, Christian Eufinger and Christian Hirsch (Acharya et al, 2016), I have confirmed that zombie lending is indeed the likely explanation for why the OMT programme did not fully translate into economic growth. Our study shows that banks that benefited more from the announcement but remained nevertheless weakly capitalized, extended loans to existing low-quality borrowers at interest rates that were below the rates paid by the most creditworthy European borrowers (high-quality public borrowers in non-GIIPS European countries, e.g., Germany), a strong indication of the zombie lending behaviour.

Such lending did not have a positive impact on real economic activity of the zombie firms: neither investment, nor employment, nor return on assets changed significantly for firms that were connected to the under-capitalized banks. Similar to the spillovers during the Japanese crisis, the post-OMT rise in zombie firms had a negative impact on healthy firms operating in the same industries due to the misallocation of loans and distorted market competition. In particular, healthy firms in industries with an average increase in the proportion of zombie firms invested up to 13% less capital and experienced employment growth rates that were about 4% lower compared to a scenario in which the proportion of zombies stayed at its pre-OMT level. At extremis, for an industry in the 95th percentile increase in zombie firms, healthy firms invested up to 40% less capital and experienced employment growth rates up to 15% lower.

The Indian story: Can we end it differently?

In many ways, the problems experienced in Japan and Europe have been rather similar. Both regions went through a period of severe banking sector stress (although triggered by different causes) and failed to adequately recapitalize their struggling banking sectors. Bank and other stressed balance-sheet problems were neither fully recognized nor addressed expediently.

In Japan, a likely explanation for the cautious introduction of recapitalization measures is that the authorities were afraid of strong public resistance when announcing large-scale recapitalization, as initial smaller support measures had already caused public outrage. In addition, Japanese officials generally feared sparking a panic on financial markets when disclosing more transparent information about the health of banks.

In Europe, introducing proper recapitalization measures has been challenging due to the political circumstances and constraints of the Eurozone. In contrast to a single country like Japan, 19 member states have to come together in the Eurozone and decide on a particular policy measure. In addition, even if a particular policy is helping the Eurozone as a whole, it might not be optimal for each individual country experiencing divergent economic outcomes.

While our initial conditions look ominously similar to these episodes and there are many parallels with how things have played out at our end, we may be fortunate in not having many of these constraints. Hence, I believe we can, we should, and in fact, we must do better. We are at a substantially lower per-capita GDP than these countries and a sustained growth slowdown has the potential to really hurt economic prospects of the common man.

With this overall objective, let me first turn to what I consider the positives of the balance-sheet resolution agenda that the Reserve Bank and the Government of India have embarked upon. I will then highlight the unfinished part of this agenda - its Achilles' heel - the lack of a clear and concrete plan for restoring public sector bank health.

Resolution of stressed assets

To address cross-bank information asymmetry and inconsistencies in asset classification, the Reserve Bank created the Central Repository of Information on Large Credits (CRILC) in early 2014. To end the asset classification forbearance for restructured accounts, the Reserve Bank announced the Asset Quality Review (AQR) from April 1, 2015. The objective was to get the banks to recognize the hitherto masked stress in their balance sheets. The AQR is now complete. The Reserve Bank is neither denying the scale of the NPAs nor trying to forbear on them. Instead, it is fully focused on resolving the assets recognized as NPAs.

In the absence of an effective, time-bound statutory resolution framework, various schemes were introduced by the Reserve Bank to facilitate viable resolution of stressed assets. While the schemes were designed, and later modified, to address some of the specific issues flagged by various stakeholders in individual deals, the final outcomes have not been too satisfactory. The schemes were cherry-picked by banks to keep loan-loss provisions low rather than to resolve stressed assets. It is in this context that enactment of the Insolvency and Bankruptcy Code (IBC) in December 2016 can be considered to have significantly changed the rules of the game. It is still early days but the number of bankruptcy cases which have been filed by operational as well as financial creditors is encouraging. Many cases have been admitted and the 180 day clock (extendable by further 90 days) for these cases to resolve has already started.

The promulgation of the Banking Regulation (Amendment) Ordinance 2017 (since notified as an Act) and the subsequent actions taken thereunder, have made the IBC a lynchpin of the new resolution framework. There were legitimate concerns that if the Reserve Bank directs banks to file accounts under the IBC, it would enter the tricky domain of commercial judgments on specific cases. However, the approach recommended by the Internal Advisory Committee (IAC) constituted by the Reserve Bank for this purpose has been objective and has allayed these misgivings. The IAC recommended that the Reserve Bank should initially focus on stressed assets which are large, material and aged, in that they have eluded a viable resolution plan despite being classified as NPAs for a significant amount of time. Accordingly, the Reserve Bank directed banks to file insolvency applications against 12 large accounts comprising about 25% of the total NPAs. The Reserve Bank has now advised banks to resolve some of the other accounts by December 2017; if banks fail to put in place a viable resolution plan within the timelines, these cases also will be referred for resolution under the IBC.

The Reserve Bank has also advised banks to make higher provisions for these accounts to be referred under the IBC. This is intended to improve bank provision coverage ratios (see Figure C) and to ensure that banks are fully protected against likely losses in the resolution process. The higher regulatory minimum provisions should enable banks to focus on what the borrowing company requires to turnaround rather than on narrowly minimizing their own balance-sheet impacts. This should also help transition to higher, and more countercyclical, provisioning norms in due course.

Going forward, the Reserve Bank hopes that banks utilize the IBC extensively and file for insolvency proceedings on their own without waiting for regulatory directions. Ideally, in line with international best practice, out-of-court restructuring may be the right medicine at 'pre-default' stage, as soon as the first signs of incipient stress are evident or when covenants in bank loans are tripped by the borrowers. Once a default happens, the IBC allows for filing for insolvency proceedings, time-bound restructuring, and failing that, liquidation. This would provide the sanctity that the payment 'due date' deserves and improve credit discipline all around, from bank supply as well as borrower demand standpoints, as borrowers might lose control in IBC to competing bidders.

Whither are we headed on restoring public sector bank health?

So far so good. Oft when on my couch I lie in vacant or in pensive mood, the realization that we have put in place a process that not just addresses the current NPA issues, but is also likely to serve as a blueprint for future resolutions, becomes the bliss of my solitude! A whole ecosystem is evolving around the IBC and the Reserve Bank's steps have contributed to this structural reform. I smile and rest peacefully at night with this thought- But every few days, I wake up with a sense of restlessness that time is running out; we have created a due process for stressed assets to resolve but there is no concrete plan in place for public sector bank balance-sheets; how will they withstand the losses during resolution and yet have enough capital buffers to intermediate well the huge proportion of economy's savings that they receive as deposits; can we end the Indian story differently from that of Japan and Europe?

The Government of India has been infusing capital on a regular basis into the public sector banks, to enable them to meet regulatory capital requirements and maintain the government stake in the PSBs at a benchmark level (set at 58 per cent in December 2010, but subsequently lowered to 52 per cent in December 2014). In 2015, the Government announced the "Indradhanush" plan to revamp the public sector banks. As part of that plan, a program of capitalization to ensure the public-sector banks remain BASEL - III compliant was also announced. However, given the correctly recognized scale of NPAs in the books of public sector banks and the lower internal capital augmentation given their tepid, now almost moribund, credit growth, substantial additional capital infusion is almost surely required. This is necessary even after tapping into other avenues, including the sale of non-core assets, raising of public equity, and divestments by the government.

The Cabinet Committee on Economic Affairs has recently authorised an Alternative Mechanism to take decision on the divestment in respect of public sector banks through exchange-traded funds or other methods subject to the government retaining 52% stake. Synergistic mergers may also be part of the broader scheme of things. The Union Cabinet has also authorized an Alternative Mechanism for approving amalgamation of public sector banks. The framework envisages initiation of merger proposal by the Bank Boards based on commercial considerations, which will be considered for in-principle approval by the Alternative Mechanism. This could provide an opportunity to strengthen the balance sheets, management and boards of banks and enable capital raising by the amalgamated entity from the market at better valuations in case synergies eventually materialize.

All of this is good in principle. There are several options on the table and they would have to work together to address various constraints. What worries me however is the glacial pace at which all this is happening.

Having embarked on the NPA resolution process, indeed having catalysed the likely haircuts on banks, can we delay the bank resolution process any further?

Can we articulate a feasible plan to address the massive recapitalization need of banks and publicly announce this plan to provide clarity to investors and restore confidence in the markets about our banking system?

Why aren't the bank board approvals of public capital raising leading to immediate equity issuances at a time when liquidity chasing stock markets is plentiful? What are the bank chairmen waiting for, the elusive improvement in market-to-book which will happen only with a better capital structure and could get impaired by further growth shocks to the economy in the meantime?

Can the government divest its stakes in public sector banks right away, to 52%? And, for banks whose losses are so large that divestment to 52% won't suffice, how do we tackle the issue?

Can the valuable and sizable deposit franchises be sold off to private capital providers so that they can operate as healthy entities rather than be in the intensive care unit under the Reserve Bank's Prompt Corrective Action (PCA)? Can we start with the relatively smaller banks under PCA as test cases for a decisive overhaul?

These questions keep me awake at nights. I fear time is running out. I worry for the small scale industries that Mr Talwar cared the most about, which are reliant on relationship-based bank credit. The Indradhanush was a good plan, but to end the Indian story differently, we need soon a much more powerful plan - "Sudarshan Chakra" - aimed at swiftly, within months if not weeks, for restoring public sector bank health, in current ownership structure or otherwise.

References

Acharya, V.V., T. Eisert, C. Eufinger, and C.W Hirsch (2015), 'Real effects of the sovereign debt crisis in Europe: Evidence from syndicated loans', CEPR Discussion Paper No 10108.

Acharya, V.V., T. Eisert, C. Eufinger, and C.W. Hirsch (2016), 'Whatever it takes: The real effects of unconventional monetary policy', Working Paper, New York University Stern School of Business.

Acharya, V.V. and S. Steffen (2014), 'The greatest carry trade ever? Understanding Eurozone bank risks', Journal of Financial Economics 115, 215-36.

Bain & Co and Institute of International Finance (IIF) (2013), Restoring Financing and Growth to Europe's SMEs, Washington, DC.

Caballero, R.J, T. Hoshi, and A.K. Kashyap (2008), 'Zombie lending and depressed restructuring in Japan', The American Economic Review 98(5), 1943-77.

Gambacorta, L. and H.S. Shin (2016), 'Why bank capital matters for monetary policy', Working Paper.

Giannetti, M. and A. Simonov (2013), 'On the real effects of bank bailouts: Micro evidence from Japan', American Economic Journal: Macroeconomics 5, 135-67.

Hoshi, T. and A.K. Kashyap (2010), 'Will the U.S. bank recapitalization succeed? Eight lessons from Japan', Journal of Financial Economics 97, 398-417.

Kane, E.J (1989), The S & L insurance mess: how did it happen? Washington, DC: Urban Institute.

Peek, J. and E.S. Rosengren (2005), 'Unnatural selection: Perverse incentives and the misallocation of credit in Japan', American Economic Review 95, 1144-1166.

Wilcox, J.A. (2008), 'Why the US won't have a "lost decade"', Working Paper.