Timothy Lane: How Canada's international trade is changing with the times

Remarks by Mr Timothy Lane, Deputy Governor of the Bank of Canada, at the Saskatoon Regional Economic Development Authority, Saskatoon, Saskatchewan, 18 September 2017.

Introduction

My theme today is international trade, which is the lifeblood of the Canadian economy. Throughout our history, we have successfully relied on our exports and imports, particularly during the vast expansion of global trade in the decades following the Second World War, to support our rising standard of living. Today, exports and imports represent about 65 per cent of our output, one of the highest ratios among the G7 countries.

Few places in Canada illustrate the importance of trade and innovation as vividly as Saskatchewan. Historically, people living on the Prairies relied on exporting grain-and, more recently, potash and oil-to markets outside Canada's borders. They imported many of the products they consumed and the tools they used, from T-shirts to tractors. In the first several decades of Confederation, they often chafed at the trade barriers that were put in place to protect and nurture the growth of the manufacturing industries of central Canada. What is remarkable is how nimble businesses in this province have been. They have adapted and innovated not only to grow market share but also to develop new products and markets for them.

In recent years, the pattern and drivers of trade both nationally and in Saskatchewan have evolved dramatically in response to forces that have been acting at the global level. Innovations in many areas, notably information and communications technologies (ICTs) and logistics, have given rise to the development of new products and new ways of producing and trading them. A particularly important trend has been the emergence of global value chains (GVCs), with various stages of production located in different countries.

In this context, the progressive lowering of trade barriers worldwide has had outsized effects. Trade agreements have enabled much closer economic integration, and trade flows have burgeoned, leading to increases in productivity and living standards.

These trading relationships are now being called into question. Populist movements in some of our major trading partners are demanding new trade barriers. However, such protectionist measures would undoubtedly mean less trade, which would reduce economic growth. While I can't comment on the specifics of any particular agreement, we have certainly been assessing this shift toward protectionism, how it might affect the outlook for growth in Canada and its trading partners and ultimately what it would mean for the conduct of our monetary policy.

In my presentation today, I'll review the changing nature of international trade, the factors, such as innovation, that are propelling it and the benefits to Canada. I'll discuss the challenges Canada faces in its international trade and how they affect our economic outlook. I'll conclude with what this means for monetary policy.

The great unbundling

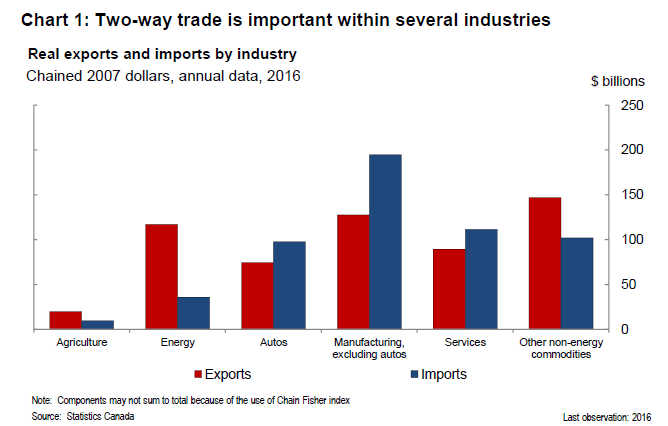

We used to think that the greatest benefits of trade accrued to countries with market dominance in specific industries. Think of Switzerland and watches or France and wine. Historically, Canada exported what we had in abundance-raw materials such as fur, fish and timber-and imported manufactured goods. Of course, this is still the case for much of our trade. But the biggest increase in world trade in recent decades has been intra-industry-that is, two-way trade within a given industry (Chart 1). Some of that simply reflects product differentiation: Canada exports rye whisky and imports scotch and bourbon. But, even more importantly, the expansion of intra-industry trade has been enabled by the unbundling of different stages of the production process.1

Consider the automobile industry: Canada both exports and imports auto parts at different stages of production as well as the finished product. The potential for this kind of unbundling was unleashed by technological innovations, particularly advances in ICT, which enabled the logistics needed to manage a supply chain that criss-crosses international borders. Bank of Canada research has shown that the separation of production into stages significantly increases the economic gains from trade.2

In a world of GVCs, easing trade restrictions can also have outsized, positive effects on the economy and on trade flows. This has been described as "leveraging" because every unit of the final product-say, every car-incorporates a great deal of trade in the intermediate products and any reduction in costs imposed on trade can have cascading effects. Lower trade barriers also make it less expensive for firms to allocate different stages of production to countries where they are most efficiently produced.3

What are the benefits to Canada of barrier-free, intra-industry trade within GVCs? Within any given industry, lowering trade barriers enables more efficient producers to expand to supply a wider market. That further lowers their costs as they move to a larger scale. Other, less efficient producers or plants may shrink or fail.

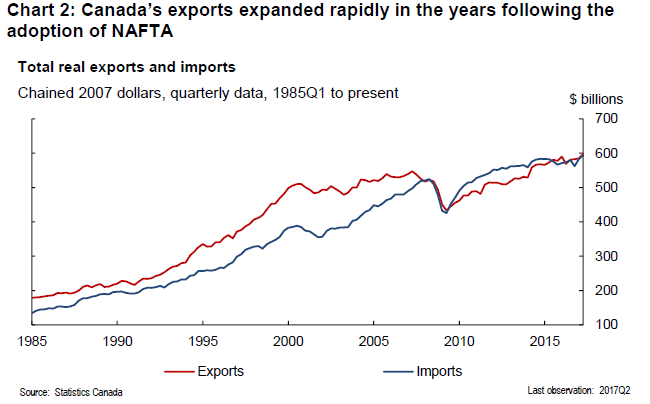

Canada's experience with the 1965 Auto Pact, the 1988 Free Trade Agreement with the United States and the 1994 North American Free Trade Agreement (NAFTA) are good examples of the economic impact of lowering trade barriers.4 The North American market opened in the wake of the agreements (Chart 2). Employment in manufacturing declined in the short term, but productivity rose and, in the longer term, the number of jobs in the economy increased. Efficient plants were able to expand to a scale that allowed them to capture even greater efficiencies. The improvement in productivity supported the growth in the overall earnings of workers.5

Exports and imports are a two-way street-and both help deliver the benefits of barrier-free trade. Canadian firms can compete in foreign markets partly by making use of lower-cost imported inputs, which raises their productivity.6 And their exports of intermediate products are linked to their trading partner's trade performance. For example, when we export machinery to the United States, it is an efficiency-enhancing input into their exports.

Benefits from opening trade may also come from increased competition.7 This is the result of both opening one's home market to imports and gaining access to foreign markets.

Creative destruction

More generally, innovation drives changes in trade patterns. This is economist Joseph Schumpeter's idea of creative destruction.8 The new replaces the old. Firms inventing new products may expand their exports by penetrating new markets. They can also develop new production processes that enable them to produce at lower cost.

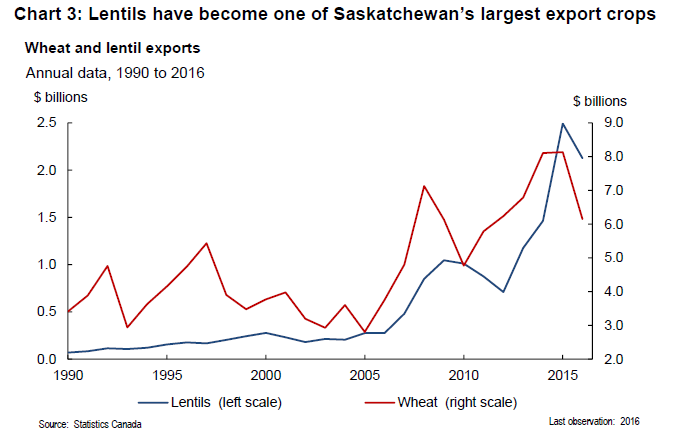

There are many such examples throughout the economy-in the high-tech industry as well as in many other sectors. For example, 45 years ago here in Saskatchewan, pulses such as lentils and peas were a small part of the province's farm economy.9 In the 1970s, however, researchers at the University of Saskatchewan began searching for a protein crop to complement wheat, which was suffering from an oversupply and low prices. They saw the opportunities in lentils and developed new varieties suitable to the climate and soils of Saskatchewan. Today, the province is the world's largest exporter of green lentils and the world's second largest producer (Chart 3). In 2016, exports of the crop generated more than $2 billion in sales.10

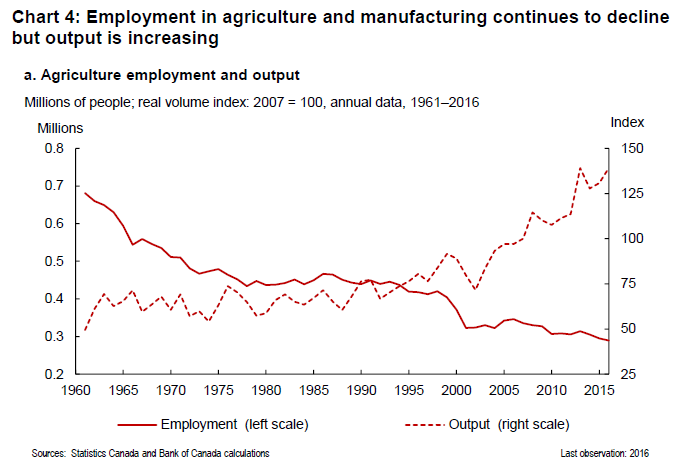

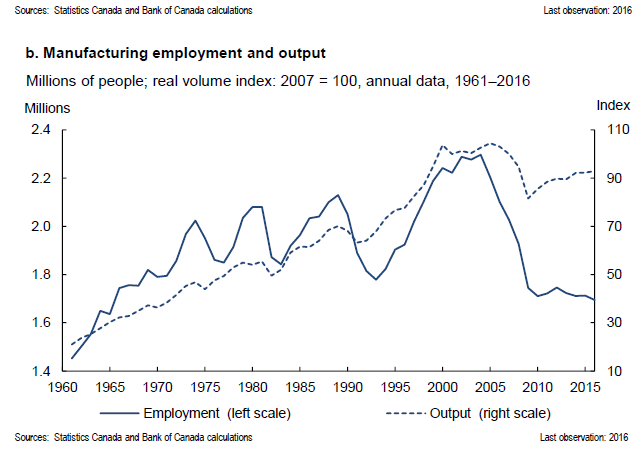

Innovations in the production process can also drive export growth. Historically, this has been a major part of the history of Saskatchewan. New technologies, such as farm machinery and seed varieties, drove the consolidation of Prairie farms to take advantage of the greater ability to cultivate and harvest crops on a larger scale. Saskatchewan's farm production and exports expanded massively, even while its population steadily declined. That freed up workers to move into job opportunities opening up elsewhere in the economy, while increasing the productivity and incomes of those who remained (Charts 4a and b). This is a story that has a personal connection for me: half of my great-grandparents were farmers in the Prairies, but none of their descendants is still farming.

I've been talking about how innovation drives trade, but the reverse is also true: trade openness drives innovation, too. This happens for two reasons. First, access to foreign markets exposes firms to new technologies and provides incentives for them to invest in producing more efficiently.11 And second, competition from trade encourages firms to innovate and invent new products to maintain market share. Trade is also an important channel for knowledge to spill over across borders: an operation in one country can become competitive by combining its home advantages with the best techniques developed elsewhere.12

While trade and innovation have always been interconnected, the nature of these interconnections is changing rapidly with recent advances in digital technology, touching virtually all sectors of the economy. We are only beginning to appreciate how new fields, such as artificial intelligence, cloud computing, additive manufacturing and big data, may play out in new trade patterns. Even calculating their economic impact is challenging. Returns from patented intellectual property (IP), such as software, are an increasing part of value added in electronic products, and these are hard to measure. That's also true of trade in IP services, which is becoming increasingly important. Google Chrome and Dropbox-distributed worldwide across the Internet-are good examples. Since they do not physically cross the border, there is no customs paper trail, and they are difficult to track. They are also provided free to many users, so it's hard to place a value on them.

This whole process of expanding two-way trade and technological advancement is playing out in myriad industries. It is one of the most important drivers of Canada's growth potential, which, in turn, underpins rising living standards for Canadians. While these are basically positive developments, they do pose important challenges for society and for policy-makers.

Both trade expansion and innovation are by their nature disruptive for firms and individuals. They spur growth by enabling more advanced and efficient activities and encouraging producers to expand, displacing less efficient activities and producers. This is an integral part of the whole process. Improved productivity is essential to compete internationally; without increases in productivity, the business itself and all of the associated jobs can be lost.

Historically, these changes have created many more job opportunities than they have eliminated. In particular, Canada's service sector, which has become an increasingly important source of exports, has created many new jobs paying above-average wages.13 But still, some workers have been left behind. Moreover, the rewards for innovation, particularly in the digital economy, often accrue to the few who own the related IP.

Can public policy help smooth the transition? I should make it clear that this is not part of the Bank of Canada's monetary-policy remit, which is to keep inflation low, stable and predictable, allowing Canadians to make spending and investment decisions with confidence. But the disruptive effects of trade and innovation have been major topics of discussion internationally. These are very challenging issues that do not offer easy solutions. Clearly, we can't turn back the clock on technological innovation; nor is the answer to try to limit its scope by closing our borders. What we can try to do is focus on supporting workers as they adapt to changing economic realities. That requires investments in retraining and lifelong learning as well as social safety nets. Another priority is to make sure that profits, including those derived from IP, can't be shifted to avoid taxation. This includes stronger international co-operation-an area where the G20 has made meaningful progress.

Trade and Canada's current economic situation

Now let me discuss the part international trade plays in Canada's current economic situation.

The period since the early 2000s has been challenging for Canadian exporters. The commodity supercycle not only created opportunities for resource exporters but also put upward pressure on the Canadian dollar, undermining the competitiveness of Canada's non-commodity exports. Then, during the Great Recession of 2007-09, foreign demand for our products collapsed, and our exports plunged by about 20 per cent. They rebounded quickly but then hit a long stretch of lacklustre growth. This was part of the broader global pattern: before the crisis, global trade had been expanding by more than 7 per cent a year-about twice as fast as the world economy. Since then it has been growing at a much more modest pace, closer to the rate of GDP growth.14

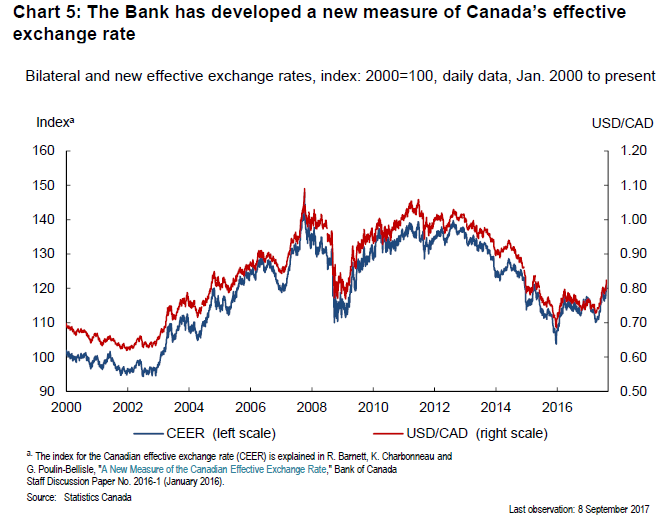

Because Canada's relatively weak export performance has been a central aspect of our economic situation, the Bank of Canada has examined it in increasing detail. New measures of external demand for Canadian exports have been constructed, which better take into account how Canadian industries are positioned in GVCs.15 Our staff have also constructed new measures of Canada's effective exchange rate that better capture Canada's competitiveness, not just relative to our export markets but also relative to third countries (Chart 5).16 This analysis contributes to a better diagnosis of Canada's loss of competitiveness.

Moreover, in keeping with the new concepts in international trade that I have been describing, our researchers have been examining Canada's exports at an increasingly disaggregated level, down to the individual firms involved. During the recession and its aftermath, many Canadian exporters went out of business. With those firms went many of their supply-chain linkages.

Another complex set of adjustments have been playing out during the past three years, with the plunge in prices of oil and other commodities. The economic and human costs to the resource-producing regions were huge. For Canada's economy to continue growing, the non-resource sectors-manufacturing and services-needed to grow faster and export more. Increasing foreign demand and the 25 per cent decline in the value of the Canadian dollar were forces supporting this adjustment. While this expansion of non-commodity exports did take place-exports of services were especially robust-the expansion was smaller than expected based on previous experience. Regaining market share was not just a matter of getting foreign customers to switch to a Canadian product. It often depended on a reassessment of where to locate production within a GVC-decisions that are typically not made often. To support the continuing growth of our international trade, many new linkages may need to be constructed as both new and existing firms emerge with new ideas and expand their activities to a sufficient scale. This process inevitably takes time and is still not complete.

The prolonged weakness of Canadian exports has meant that Canada's economy has needed to rely on other sources of demand to drive its growth. In particular, we have depended heavily on household spending, supported by very low interest rates.

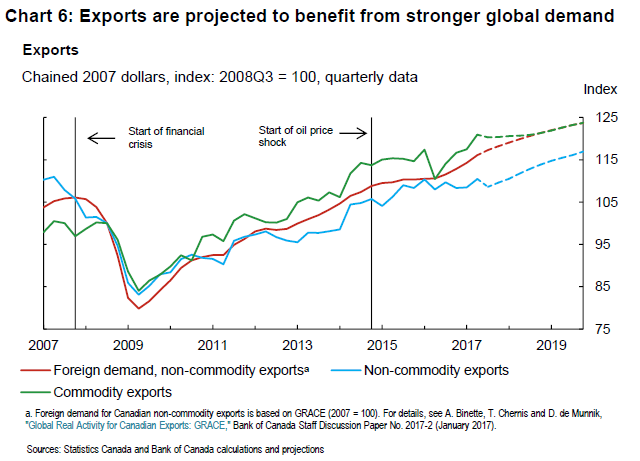

Now, economic data show that growth in Canada is becoming more broadly based and self-sustaining. We are seeing widespread strength in business investment and exports, in conjunction with a global economic expansion that is becoming more synchronous (Chart 6). Imports are also expanding; the increases we are seeing in imports of machinery and equipment and of various intermediate products are early signals of rising business investment. It was in this context that the Bank of Canada decided, in July and again earlier this month, to raise our policy rate. We will be paying close attention to how the economy responds to both higher interest rates and the stronger Canadian dollar.

Looking ahead, Canada's openness to international trade is an important determinant of Canada's economic growth potential-that is, of how fast the Canadian economy can grow without giving rise to inflationary pressures. That growth potential could be greater than we think-if businesses find new ways to engage with GVCs and develop new products and processes to make them more productive and competitive. As in the past, further expanding Canadian firms' access to markets and to imported inputs could unlock more opportunities. An example is the Canada-European Union Comprehensive Economic and Trade Agreement, most of which will be implemented in the next few days.

But some other developments are more concerning. With the rise in protectionist sentiment in some parts of the world, we have been entering a time of heightened uncertainty about the rules of the game on international trade. The possibility of a material protectionist shift-particularly regarding the outcome of negotiations on possible changes to NAFTA-is a key source of uncertainty for Canada's economic outlook.

Given the nature of international trade in the 21st century, the stakes are very high. As I discussed, the economic benefits we have experienced from trade liberalization were not only in expanding the markets for Canadian exports. We also benefit from the greater efficiencies that can be achieved by those exporters that do expand, the heightened competition and better access to imported inputs that come with greater openness to imports, and the resulting spur to innovation throughout the GVCs. If trading rules are changed in a way that undermines these benefits, the result would be both lost external demand for exports and lower potential growth for Canada as well as for the United States and other trading partners.

Conclusion

As an open economy, Canada's fortunes will continue to rise or fall with trade, as they have throughout our history. Global economic forces-the sharp movement of commodity prices; the Great Recession and the lacklustre global economy in its aftermath; and, for much of the past decade, a strong Canadian dollar-battered many of our export industries and splintered their supply chains. Rebuilding them requires the emergence of brand-new industries and the development of new linkages to international trade networks. While it will take time for many of these adjustments to play out, we are now seeing encouraging signs that exports and business investment are broadening and strengthening.

At the Bank of Canada, we have made a lot of progress in understanding the changing nature of world trade and especially why it has taken so long for our exports to recover. But as the dynamics of trade continue to evolve with technology and other forces, we will closely monitor and analyze these developments. This is essential, given the importance of trade to the economic well-being of Canadians.

I would like to thank Patrick Alexander and Karyne Charbonneau for their help in preparing this speech.

1 R. Baldwin, "Trade and Industrialization after Globalization's Second Unbundling: How Building and Joining a Supply Chain Are Different and Why It Matters," National Bureau of Economic Research Working Paper no. 17716, 2011.

2 P. Alexander, "Vertical Specialization and Gains from Trade," Bank of Canada Staff Working Paper No. 2017-17 (April 2017).

3 K. M. Yi, "Can Vertical Specialization Explain the Growth of World Trade?" Federal Reserve Bank of New York, Staff Report no. 96, January 2000.

4 D. Trefler, "The Long and Short of the Canada-U.S. Free Trade Agreement," American Economic Review, American Economic Association 94, no. 4 (September 2004): 870-895.

5 Ibid.

6 P. Goldberg, A. Khandelwal, N. Pavcnik and P. Topalova, "Imported Intermediate Inputs and Domestic Product Growth: Evidence from India," Quarterly Journal of Economics 125, no. 4 (2010): 1727-1767.

7 A. Atkeson and A. T. Burnstein, "Innovation, Firm Dynamics, and International Trade," Journal of Political Economy 118, no. 3 (2010): 433-484.

8 J. Schumpeter, Business Cycles: A Theoretical, Historical and Statistical Analysis of the Capitalist Process (New York, Toronto, London: McGraw-Hill Book Company, 1939).

9 University of Saskatchewan, "Leading the world in lentils."

10 Government of Saskatchewan, "Agriculture Fact Sheet.

11 P. Bustos, "Trade Liberalization, Exports, and Technology Upgrading: Evidence on the Impact of MERCOSUR on Argentinian Firms," American Economic Review 101, no. 1 (2011): 304-340.

12 R. Piermartini and S. Rubínová, "Knowledge Spillovers Through International Supply Chains,"

13 S. S. Poloz, "From Hewers of Wood to Hewers of Code: Canada's Expanding Service Economy" (speech to the C.D. Howe Institute, Toronto, Ontario, November 28, 2016).

14 S. S. Poloz, "A New Balance Point: Global Trade, Productivity and Economic Growth" (speech to the Investment Industry Association of Canada and Securities Industry and Financial Markets Association, New York, New York, April 26, 2016).

15 A. Binette, T. Chernis and D. de Munnik, "Global Real Activity for Canadian Exports: GRACE," Bank of Canada Staff Discussion Paper No. 2017-2 (January 2017).

16 R. Barnett, K. Charbonneau and G. Poulin-Bellisle, "A New Measure of the Canadian Effective Exchange Rate," Bank of Canada Staff Discussion Paper No. 2016-1 (January 2016). For details on the new measure, see Canadian Effective Exchange Rates.