Luci Ellis: The current global expansion

Speech by Ms Luci Ellis, Assistant Governor (Economic) of the Reserve Bank of Australia, at the Australian Business Economists (ABE) Lunchtime Briefing, Sydney, 20 September 2017.

Thanks to Peter Rickards and Rochelle Guttmann for assistance in preparing this speech.

I'd like to thank the organisers of today's event, the Australian Business Economists, for giving me the opportunity to speak to you today. It really is a pleasure.

Today I'd like to talk about an important driver of future prospects for the Australian economy: the pick-up in global economic activity that began in the second half of last year. How did we pick up that this was happening? And how might conditions evolve over the period ahead?

An apparently gloomy starting point

During 2015 and early 2016, the tone of commentary about the global economy was quite negative. Yes, there had been a slowing evident in the data, particularly from China. Yet this alone would not explain it. Things seemed fragile. Growth forecasts were revised down.

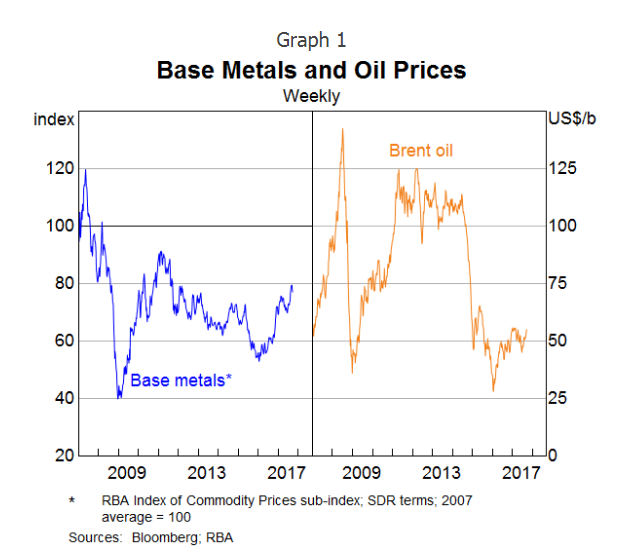

Experience suggested that the mood should have been more buoyant. Policy was accommodating the recovery from the global and European financial crises. There was a fall in commodity prices, particularly oil prices (Graph 1). Declines in oil prices are typically seen as expansionary, because they often imply that supply has increased, and this was precisely what OPEC was doing. Lower oil prices also often support growth. Most of Australia's major trading partners are net oil importers and are better off if the price of oil declines relative to other prices.1

But rather than being a catalyst for growth, lower oil prices were an indicator of weakening global demand. This in turn spurred an unusually large pull-back in energy-related business investment in some economies and this exacerbated the downturn in global activity.

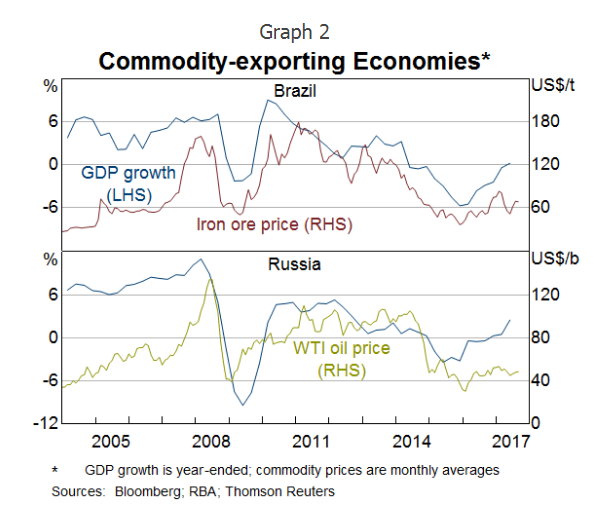

For commodity-exporting emerging markets, growth was impeded by lower commodity prices, on top of any domestic factors driving growth (Graph 2). Previously, the negative effects of lower oil prices on producers would have been outweighed by the positive effects on spending by net oil-importing countries. This time around, the opposite occurred: the net effect was negative. Commodity exporters' demand for traded goods produced elsewhere declined noticeably over 2015 and early 2016. This had spillover effects on other economies highly exposed to global trade, particularly in Asia. The Asian region was also affected by concerns circulating about risks in China.

It's worth contrasting the experience of these commodity exporters with Australia, or with an economy more exposed than Australia to oil prices, such as Canada. Falling commodity prices reduced Australia's terms of trade, and thus our income. There was a debate about whether the Australian dollar had depreciated by enough to offset that effect. But the net effect of lower commodity prices and the exchange rate was smaller than in some other economies. The lower exchange rate had gone some of the way to cushioning the income effects of the lower terms of trade. It also contributed to helping some parts of the non-mining economy pick up.

The 2016 turnaround

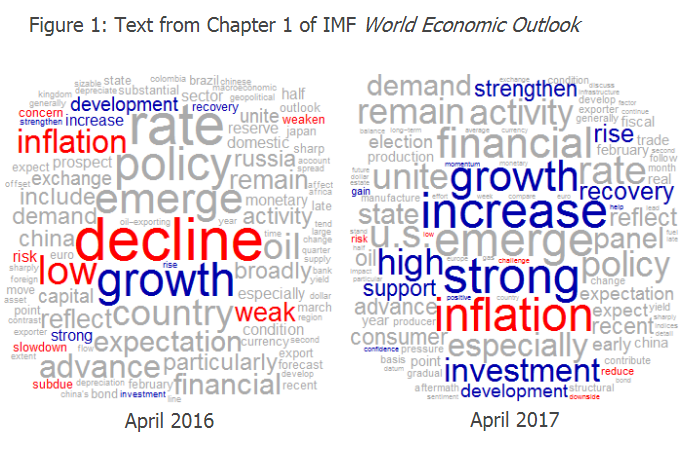

Late last year, the negative sentiment and rhetoric around the global economy started to turn around. Clearly there was a recovery in the data, but the recovery in the accompanying rhetoric was even more marked. To the extent that perception affects people's expectations, this had the potential to influence actual outcomes.

Perhaps one way to show this is to look at the text from reports by key economic agencies. If you contrast the words most frequently used in the first chapter of the April 2016 IMF World Economic Outlook, with the same chapter in the issue from a year later, you can see how the tone has changed.2 Another way to characterise this change in tone is that in the April 2016 edition, around 6 per cent of the key words coded as positive and 10 per cent as negative. A year later, more than 13 per cent of the words were considered positive, compared with about 5 per cent negative.

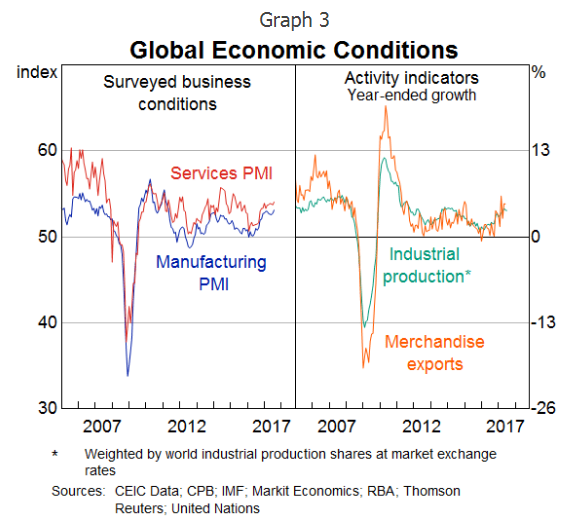

At first, the turnaround seemed to be only in 'soft' indicators of sentiment, such as business surveys and financial market prices. The global Purchasing Managers Indices - a commonly used measure of surveyed business conditions - hit bottom and started to turn around in late 2016 (Graph 3). Commodity prices also started to lift.

Over time, however, clearer signals started to emerge that this was more than just people feeling optimistic. There was something real happening as well. Growth in global merchandise exports was the next to pick up. Soon afterwards, it became clear that growth in industrial production was also increasing (Graph 3). It should be noted that throughout this period, the swings in the actual data were never very large, certainly not relative to the crisis period.

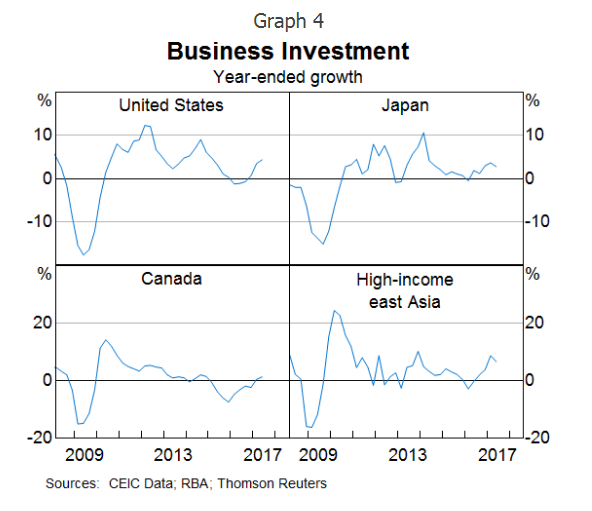

By the time we reached early 2017, there were further signs that the pick-up in trade and other high-frequency indicators were flowing through various countries' national accounts. Particularly welcome was the recovery in investment growth, which can now be seen in a range of major economies and regions (Graph 4).

As well as broadening across different measures of activity, the expansion also broadened across countries and regions. In the latest Statement on Monetary Policy, the Reserve Bank emphasised the broad-based nature of the pick-up, across both sources of exports and destinations of imports. The boost to incomes from rising commodity prices has also helped economic prospects of commodity exporters. Some of them have emerged from recessions and are now increasing their demand for production from the rest of the world.

How people saw it happening

The sequence of events that I have just described is a turning point. As any economic forecaster could tell you, a turning point is essentially impossible to predict. But it does seem that many observers, including the Bank, managed to notice that turning point in near real-time. In the Overview of the November 2016 Statement on Monetary Policy, the first sentence read:

'Growth in Australia's major trading partners remains a bit below average and is expected to decline a little over the forecast period, reflecting a further moderate easing in growth in China.'

Shortly after its publication, markets rallied following the US election outcome. It wasn't clear that the policies of the incoming Administration would be expansionary overall. The expected fiscal stimulus would have been, but the announced trade policies were rightly seen as likely to harm global growth. Many observers thought the election outcome would be negative for financial market pricing. So it was understandable to downplay reactions when markets instead rose.

Then, over the southern hemisphere summer, it became clear that this was more than a financial market reaction to political events in one country. The outlook had become more positive. The first sentence of the February 2017 SMP Overview read:

'The global economy entered 2017 with more momentum than earlier expected.'

The facts had changed, and we had changed our minds. The nature and pattern of the pick-up in the data convinced us.

The first aspect of the shift that helped convince us was the broadening of the pick-up from sentiment indicators (including financial market pricing) to measures of physical activity. Growth in global trade was the first place this became apparent. Industrial production data in a range of countries followed soon afterwards. The second aspect was the broad-based spread of the pick-up across countries and regions. If it had just been one country - say, China - demanding all the extra imports, there would have been less reason to revise the outlook.

To identify a turning point as it happens, you need to have a sound analytical framework for thinking about how the economy works, and how all the various indicators fit together.

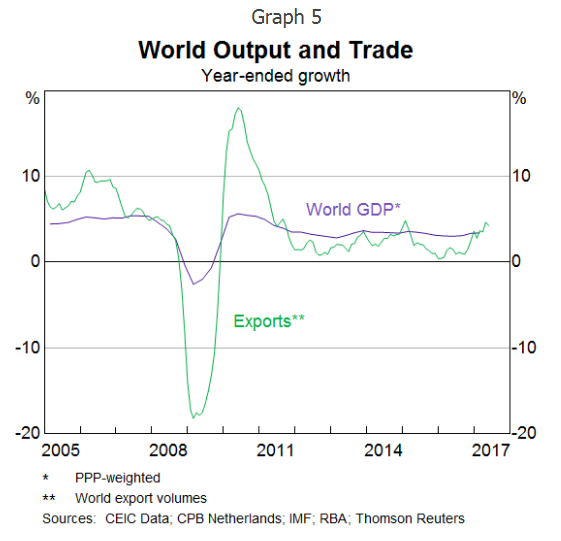

One thing to bear in mind is that trade is often - though not always - highly leveraged to global activity (RBA 2017). When global activity picks up, trade picks up by more (Graph 5). This is partly because demand for traded merchandise tends to be a bit more cyclical than the services sector, where much output is not traded across borders. It is also a result of the structure of global supply chains. You can imagine a situation where final-stage production increases by one unit, but almost all of the value-added crosses three borders before reaching its destination. Global exports (or imports) would then pick up by close to three units. It is also reasonable to expect that in the first instance, an unexpected increase in demand for goods and materials might be met on global markets, because often not every product or input is produced in every country.

Another point to bear in mind is that in recent upswings, investment has usually come later. This wasn't always the way. But in recent times, businesses have tended to wait until they see evidence of increased demand before they invest in expanding capacity. They are even less likely to invest to expand when there is plenty of spare capacity, a legacy of the crisis.

We also know that businesses are more likely to invest in things that boost labour productivity when the labour market is tight, not when there is considerable slack. So in the current environment, we would not expect business investment to be at the leading edge of a pick-up in economic activity. And we have to be willing to call the pick-up before we see it in business investment.

A third point to be mindful of is that data are noisy and can be revised. So we need to triangulate multiple data sources against each other. Survey measures of sentiment and other supposed leading indicators are not the whole story. They tell you something, but shouldn't be taken as gospel on their own. But neither should you wait until you see the whites of the national accounts' eyes before you change your view. All data are noisy, including the national accounts. By the time you have seen something in the national accounts and are sure it isn't just noise, several quarters will have passed. If you wait that long, you will be well behind the curve in catching a change in economic momentum.

Portents for the future

Now that we've seen this pick-up in global activity, we must then ask: what next? Will the expansion continue at its current rate, pick up further, or peter out? Part of the question here is whether expansions can continue unabated or whether something forces them to 'die of old age'. While one could argue that this is a relatively new upswing, many economies have in fact been expanding ever since the end of the Global Financial Crisis, and are now quite close to being at full capacity. Countries such as the United States and Japan are generally regarded as being already at full employment. Does this mean that they can't keep going like this for much longer?

The academic literature, at least, seems to suggest that long-lived expansions are no more likely to end than shorter ones, at least beyond some point (Rudebusch 2016). I think we can take some comfort from that. We should then ask whether we would expect the current expansion to be any different from past expansions. A common pattern is that expansions end because they came together with an unsustainable build-up in leverage. Globally, leverage does not seem to have increased much this time around. At least, it hasn't increased to the extent seen in the lead-up to the Global Financial Crisis. Of course there are some areas where debt has increased rapidly, in ways that deserve further investigation. Whether credit expansions pose a problem isn't always clear-cut, except in hindsight. So we should be cautious when we see them, and should factor them into our assessments of how long an expansion might last.

In thinking about how long and how strong the global expansion could be, a lot will depend on productivity growth. This isn't the place to dwell on the 'secular stagnation' debate in detail. But I will note that productivity itself can be cyclical. Productivity growth has been weak in some major advanced economies. It's not clear that this will continue once spare capacity in these economies has been fully absorbed.

I also note that some of the pessimism about productivity is happening alongside great optimism in some quarters about a new Industrial Revolution built on better algorithms. The truth may well lie somewhere in the middle. It might also take a while to assert itself. Those of us who remember the 1990s would recall that there have been previous episodes where considerable innovation seemed to be happening, but this took a while to be evident in the productivity data. This is because firms take a long time to adapt their business models and processes to the new technologies. And the greatest spur to change is capacity constraints. Tight economies spur process innovation. When there is plenty of spare capacity, not even strong competition necessarily induces higher rates of adoption of new technologies.

Risks to the outlook

Taking all that into consideration, there seems a reasonable prospect that - as long as nothing really bad happens - this global expansion could continue for a while. This is especially so if the technology optimists are right about the implications of recent innovations. But of course there are risk scenarios that have the potential to derail the current economic momentum.

Foremost of these at present would be geopolitical risks. These are particularly difficult risks to integrate into a macroeconomic analytical framework. We aren't political analysts. And I question whether anyone can truly know what the odds of certain events occurring might be. But we can at least think about what those risks might be and whether they might be increasing or receding.

I think it is fair to say that geopolitical risks in Europe and specifically the euro area have receded. While it remains to be seen how Brexit will play out from a practical perspective, an existential crisis for the euro area and the EU more broadly no longer seems so close. Against that, geopolitical risks in Asia have increased. These are the low probability, high-impact events that can only ever be a risk to one's forecasts. Until something actually happens, they do not and should not affect the central scenario. Even if you knew for sure that an event happened, the economic effects are often difficult to predict.

Financial risks will also be ever-present as risks to a macroeconomic outlook, and they are almost as hard as geopolitical risks to quantify. One that seems to be becoming less pertinent at the moment is the international risk posed by ongoing low interest rates and the resulting search for yield by investors. Now that policy interest rates globally are starting to rise, if only slowly, the urgency of the search for yield surely becomes less pressing.

On the domestic front, the Bank has repeatedly pointed to the issues associated with household sector balance sheets. These are probably best regarded as a potential exacerbating factor. That is, if some other shock should come along, debt would make it worse. Of itself, the level of indebtedness is unlikely to be a triggering factor that sparks a negative outcome. But it is an important consideration in the context of other triggers. The risk profile of recently originated debt has improved as a result of various actions by the regulators, the evolving risk environment and the lenders' responses. The level of debt owed matters most when the borrower is facing a large negative shock. Strong lending standards mitigate the effects of moderate shocks, and can help prevent a shock turning into a default event. But in the face of a large, economy-wide shock, even the best lending standards might not be enough to protect borrowers and lenders. At that point, the absolute amount of debt owed becomes the binding consideration.

A final risk to mention is the global monetary policy environment, together with the economic and market reactions to it. Expansionary monetary policy and less contractionary fiscal policy have supported economic recoveries. Some economies are now thought to be close to full employment and productive capacity. Yet so far, growth in both prices and wages has remained quite low.

We believe that, ultimately, the forces of supply and demand do assert themselves. Wage growth and inflation should therefore pick up in these economies at some point. However, it could take a while. If productivity growth is indeed cyclical, it will start to pick up over time in these economies. So it will take longer to hit the capacity constraints that induce price rises. On the other hand, stronger potential growth is clearly a positive for economic welfare more broadly. If this scenario happens, and inflation stays low despite reasonable growth in a range of economies, policymakers will face a challenge. In that scenario, policy still needs to remain appropriately expansionary while avoiding further build-up of leverage and financial risk. Calibrating the pace of withdrawal of stimulus will be no easy task. Policy will therefore need to adapt to the evolving momentum in national and global economies.

Concluding remarks

To sum up, the global economy is looking better than it did a year ago. The turning point was around the end of last year. While it doesn't seem to have picked up further recently, neither is this expansion a flash in the pan. That is positive news for the Australian economy, too.

Noticing that change in momentum required economic forecasters to be alert to the right indicators, and have the right framework for thinking about the signals these indicators send. Nothing is ever clear-cut. There are always uncertainties about the data. There are times when you have to be willing to make a call, because waiting until you are 100 per cent sure things have changed means waiting too long. And that means taking a view and being willing to evolve that view as new data come in, just as we always have done.

Thank you for your time.

Bibliography

RBA (2015), 'Box C: The Effects of the Fall in Oil Prices', Statement on Monetary Policy, February, pp 46-48.

RBA (2017), 'The Recent Pick-up in Global Merchandise Trade', Statement on Monetary Policy, August, pp 13-14.

Rudebusch G (2016), 'Will the Economic Recovery Die of Old Age', Federal Reserve Bank of San Francisco.

1 A sentence along these lines was included in several of the Bank's Statements on Monetary Policy over this period. See also RBA (2015).

2 The colouring of the words as red for negative and blue for positive has been done manually, based on the consensus of a number of colleagues. Standard packages for sentiment analysis do not handle the nuanced communications of central banks and international agencies particularly well. It should also be noted that some nouns that are coded as positive (such as 'growth' or 'investment') can sometimes be mentioned in negative contexts, for example with verbs such as 'slowed' or 'declined'. That is certainly the case in the April 2016 issue. The cited proportions of words coded positive or negative does not include common 'stop words' such as 'the', 'and' and 'with'.