François Villeroy de Galhau: The future of the euro area - from the "impossible trinity" to the "growth triangle"

Text of the 6th Annual Tommaso Padoa-Schioppa Lecture by Mr François Villeroy de Galhau, Governor of the Bank of France, at the 6th Annual Tommaso Padoa-Schioppa Brussels Economic Forum 2017, Brussels, 1 June 2017.

I am grateful to Carine Bouthevillain, Bruno Cabrillac, Laure Carrel, Pavel Diev, Marine Dujardin, Pierre Jaillet, Eloïse Lecouturier, Céline Mistretta-Belna and Edouard Vidon for their assistance in preparing these remarks.

Ladies and gentlemen,

It is a pleasure to be here in Brussels and to speak in front of such a distinguished audience. For my generation of modest European architects - I was in Maastricht 25 years ago - Tommaso Padoa-Schioppa is one of those great - almost mythical - Italian figures who engaged in this "Kantian quest for European unity"1. So I am honoured to give a lecture named after him. He would certainly have been very pleased that the majority of French people clearly expressed their attachment to the euro on the occasion of the French presidential election. Giving fresh momentum to the European project is indeed one of the priorities of the new French President. And although I was invited several months ago, and although the Banque de France is fully independent of the government, I like to think that my presence here this morning is a sign that there is renewed interest for the voice of France in Europe.

Europe is once again standing at a crossroads. The 2007-2008 global financial crisis and the 2011 sovereign debt crisis in the euro area have left a legacy of foregone growth, high unemployment, and massive public debts. On top of that, Europe's security has been directly affected by the scourge of terrorism that targets our population and our values, and moreover we have not yet found lasting solutions to the refugee crisis.

And yet, despite all these challenges, support for the euro and the European Union is still high: according to the Eurobarometer survey, 72% of euro area citizens support the euro, the highest level since 20042, and more than half of EU citizens feel attached to the European Union3. The clearest signs of this continued support for the European project - despite Brexit, beyond Brexit - are the recent defeats of the nationalist parties and their euroscepticism in a number of European countries. Whenever the temptation of reverting to nationalism arises, we should remember Tommaso Padoa-Schioppa: he liked to remind us that the founding fathers of the European Union - among whom Robert Schuman, Konrad Adenauer and Alcide de Gasperi - shared the same motto: "never again a war among us." In the very uncertain world of 2017, and with the dangerous hesitations of the new American administration, this is sadly very relevant: peace remains the first European promise.

This is the reason why our common responsibility is to persevere along the path of European integration. But we cannot continue as before. People expect concrete results. What we need is not necessarily more Europe, but rather a "better" Europe: less words, more action. Europe must be more focused on a few projects, and more efficient. To put it briefly: "let's do little, but well, and until the end". There are naturally some non-economic priority areas such as defence, border security, climate change as well as youth education and training - for example an Erasmus-pro programme for apprenticeship for the unqualified and unemployed youth. But I will focus today on the economic field. This is obviously my area of expertise as a central banker. More importantly, there is a strong relationship between economic prosperity and citizens' attachment to Europe. The policy orientations that I will propose today build and elaborate further on some ideas that I presented here in Brussels just over a year ago. I am very pleased that the European Commission's future of the Eurozone paper published yesterday goes in the same direction, although with some understandable caution... In my view, this is an additional sign that we now have a unique momentum in Europe, that we should not let wane.

I would like today to elaborate on what I like to see as three economic triangles. First, we resolved a first incompatibility triangle 18 years ago by achieving our monetary union. Now, we are confronted with a second incompatibility triangle, due to the weaknesses of our economic union. Therefore, I think that we now need to implement a compatibility triangle to boost Europe's growth and revive the European project.

1. The European monetary union has been a successful answer to the "impossible trinity" challenge

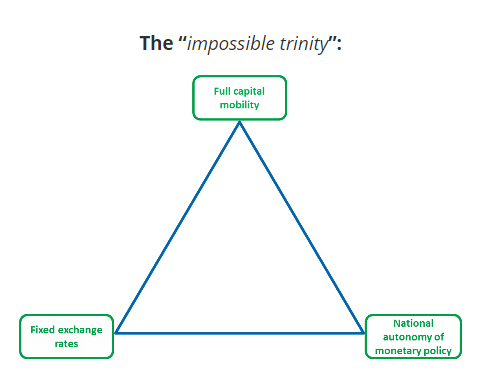

The first triangle I'd like to dwell on is the famous incompatibility triangle derived from the Mundell-Fleming model of the 1960's, also known as the "impossible trinity" or the "trilemma". This triangle has been used to argue that it is impossible to reconcile fixed exchange rates, full capital mobility and national autonomy of monetary policy.

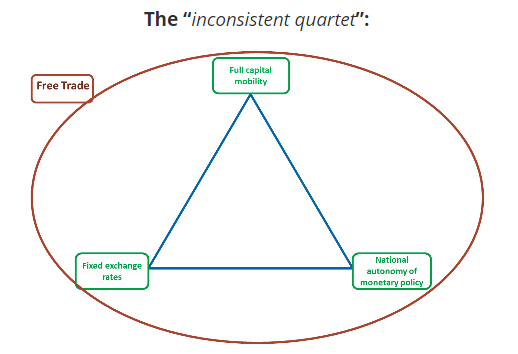

As early as 1982, Tommaso Padoa-Schioppa coined the term "inconsistent quartet"4 (quartetto inconciliabile), thereby enlarging the impossible trinity to a fourth goal, free trade - a pillar of the Treaty of Rome. Let me quote here an analysis by Banca d'Italia5: "At first sight this may appear to be a puzzling choice, since from the strictly analytical standpoint the inconsistency between the other three elements holds regardless of the presence or absence of free trade. But in a deeper economic sense, taking trade into consideration was essential, since the costs and benefits of different positions along that three-way trade-off depend crucially on the degree of trade integration." And as Tommaso Padoa-Schioppa wrote in 1988: "In the long term, the only solution to the inconsistency is to complement the internal market with a monetary union. [Otherwise] it would be unrealistic to expect the Community to be able to square a circle that has never been squared."6 The early 1990's were indeed difficult times for the European monetary system: several countries were forced to realign their exchange rate or to withdraw from the mechanism, like for instance Italy in 1992. It was that same year, with the Maastricht Treaty, that Europe chose to move forward towards a European monetary union.

Tommaso Padoa-Schioppa was right in his belief and in his recommendation to create the euro. The euro has proven to be a great success which has delivered material benefits. First, price stability, which is the main objective assigned to the Eurosystem, and which directly benefits euro area citizens' purchasing power. In the 18 years since the introduction of the euro (1999-2016), inflation has stood at 1.7% on average, compared with 4.6% in the 18 years preceding the introduction of the euro (1981-1998). Second, lower interest rates, which are the corollary to the confidence that investors place in our currency, and which can be measured by the decrease in long-term interest rate spreads vis-à-vis Germany, amounting to between -1.5% for France and -3.7% for Italy. Third, internal exchange rate stability, and a greater international role. Today, the euro accounts for 20% of international reserves, second only to the dollar. And an internationally recognised currency generates economic gains: financial markets are more attractive to domestic and foreign investors, more liquid, and thus more efficient. But it also carries a political weight: when Mario Draghi speaks at the G20, the whole world listens to what Europe has to say.

2. Yet, despite the success of monetary union, Europe's economy is now confronted with a new trilemma.

Weaknesses have materialised. Addressing people's expectations requires identifying the flaws of our Union in an open and honest manner. Regarding growth, we must distinguish between the snapshot of the present and the full movie that we have lived through. The present snapshot is positive: euro area growth is accelerating, and is now up to speed with the United States or the United Kingdom. However, this is not sufficient to make up the cumulative shortfall of past years: the full movie until today is that since 2011, the cumulated EU growth trajectory is 7.5 GDP points below the US'. Even when measured per capita, this underperformance amounts to 5 percentage points. And we see the same contrast regarding convergence between countries. The present snapshot, which is positive, shows that intra-area divergences have been significantly reduced and are at their lowest level since 1999. But the full movie up to today shows rather wider disparities in income per capita, as a result of the 2009-2012 crises.

To make matters worse, all too often, Member States tend to act in isolation, not taking into account the externalities and the impact that their policies have on others. This leads to a collective suboptimal situation: according to a study by Banque de France staff7, the opportunity cost of not sufficiently coordinating our fiscal policies in the aftermath of the crisis may have amounted to 1 to 2 GDP points in the euro area. Moreover, taken together, deficiencies in the coordination of both our fiscal and structural policies may have cost between 2 and 3 GDP points between 2011 and 2013. Although our common monetary policy works well, it cannot be a substitute for economic policy coordination or for the lack of reforms. In Maastricht, our aim was to build an Economic and Monetary Union. We have succeeded in Monetary Union, but we have not delivered on Economic Union.

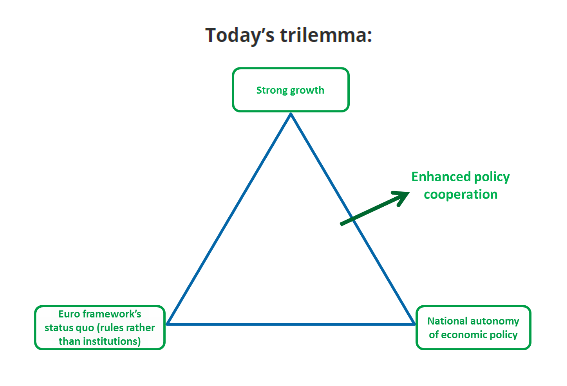

And so, in a nutshell, a new trilemma has emerged. It now seems impossible for euro area countries to achieve their full growth potential - the first point of the triangle -, if they wish at the same time to achieve the two other points of the triangle: on the one hand, keeping the autonomy of their economic policies at the national level; on the other hand, keeping the "Euro framework" of coordination unchanged, that is to say maintaining the status quo, with a cooperation between countries based only on rules without institutions and without a common strategy. We have to drop one of the points of this triangle in order to achieve the other two. To me, the solution is obviously for euro area countries to refuse the status quo and amend the "Euro framework" towards enhanced policy cooperation. Let me outline what I see as the possible way forward.

3. To boost European growth, this new trilemma has to be turned into a "growth triangle"

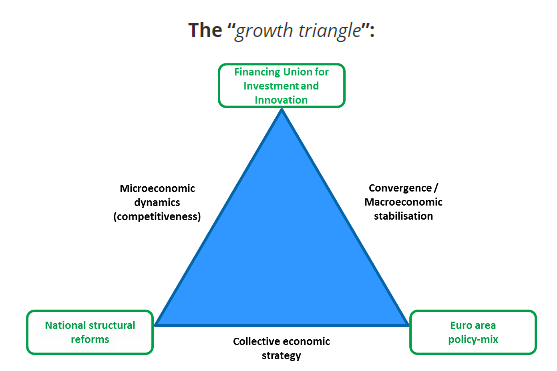

We have to get Economic Union moving forward again, thanks to what I call the "growth triangle". The peculiarity of this triangle is that it is not an incompatibility triangle but a compatibility triangle. This means that the three goals can and have to be pursued at the same time to deliver economic gains. These goals, or levers, are: national structural reforms; the Financing Union for Investment and Innovation; and a euro area policy-mix based on a better coordination of macroeconomic policies. They can be implemented quickly, as at least many of them do not require changing the Treaties.

As a central banker and steadfast European, this is what I believe is needed for a "better Europe". But of course, the decision does not fall to us but to political leaders. Our responsibility as the Eurosystem is to deliver a monetary policy that is in line with the mandate entrusted to us, and to make proposals for improving the efficiency of other economic policies.

The first point of my growth triangle is: national structural reforms. They are a prerequisite for each country to regain credibility in Europe and for unleashing our collective economic growth potential. Obviously, their intensity should vary depending on the countries. France and Italy for instance are lagging behind and have to catch up, whereas other countries like Germany, Spain or the Netherlands, among others, have succeeded in carrying out in-depth reforms and are now reaping the benefits in terms of GDP growth and employment. I wish to stress that these examples show that economic success is fully compatible with the European social model that we share, which combines high standards of public services and low levels of inequality - much lower than in American society for instance. And clearly we can now expect an acceleration of reforms in France: this will be welcome not only for my country, but for Europe as a whole.

The success of national reforms would be amplified if combined with two European reforms - the two other points of my triangle. The first one is microeconomic: the creation of a Financing Union for Investment and Innovation (FUII). The need for such a Financing Union comes both from a weakness, which is the persistent financial fragmentation in the euro area, and from an opportunity, which is the euro area savings exceeding investment by EUR 350 billion per year. An obvious way to boost growth is therefore to better steer our abundant savings towards the financing of investment and innovation across borders. And this implies providing businesses with more equity financing solutions. Europe is lagging far behind in this area: such financing only represents 68% of GDP in the euro area compared with 128% in the United States in the fourth quarter of 2016. Creating the Financing Union would magnify the impact of national reforms: whereas they foster firms' willingness to invest, the Financing Union would foster firms' ability to invest, and they would together foster microeconomic dynamics and competitiveness.

The efforts so far are going in the right direction, but work should now be accelerated. The building blocks already exist: the Juncker investment plan; the Capital Markets Union (CMU), which supports the diversification of private financing; and the Banking Union, which tackles the fragmentation issue. These initiatives have to be brought together into the FUII in order to go beyond administrative or bureaucratic borders, create synergies, and therefore give new impetus to this agenda. Think for instance of a real European venture capital.

To be more concrete, progress towards a Financing Union for Investment and Innovation requires fleshing out proposals in four key areas:

-

First, completing the Banking Union. This means, as a priority, finalising the Banking Union's second pillar, namely the single resolution. Within a strong Banking Union framework, banks in the euro area will thus be able to engage in cross-border consolidations on a sound and safe basis and therefore contribute to further reducing financial fragmentation. This also includes harmonising insolvency regimes for businesses.

-

Second key area: thoroughly reviewing the incentive schemes for cross-border investments, notably by promoting further convergence of tax and regulatory regimes.

-

Third area: expanding the supply of financial intermediation services, be it in the form of new savings products - more long-term and risk-oriented - or new market initiatives in green bonds or private placement for instance.

-

Fourth area: making sure that vital financial activities and risks for European economies are properly controlled. This requires in particular relocating certain activities in the European Union, such as euro-denominated clearing activities that are systemically important for the euro area.

The second reform at the European level is a macroeconomic ambition: a better euro area policy-mix. This would help offset the short-term pain of national structural reforms before achieving the long-term gains. Let me be crystal-clear: we should not abandon the existing rules that apply to each Member State, including the Stability and Growth Pact: rules are necessary, but they are not sufficient. What we currently lack is a common direction, despite the progress brought by the European Semester method. A proper euro area policy-mix requires a collective economic strategy, whereby Member States "seal a deal" involving each country. Let us aim, until the end of 2017, for an obvious progress: growth and employment will be stronger in Europe if we combine more structural reforms where they are needed - in France and Italy for instance -, and more fiscal or wage support in countries with room for manoeuvre - for example, Germany and the Netherlands.

Another relatively low-hanging fruit would be a common stabilisation fund equivalent to 1 to 2% of euro area GDP, which could provide us with a proper macroeconomic stabilisation capacity. I note that this largely converges with the Commission's proposal to create a macroeconomic stabilisation function for the euro area. This common stabilisation fund would be used under efficient rules - but not conditional to an adjustment program, contrary to the ESM - to support, through loans, Member States' counter-cyclical policies when they are faced with asymmetric economic shocks. The fund itself would be financed by borrowing.

To definitely succeed in this ambition, the euro area will need a common keystone: an institution that fosters confidence. Because, as Tommaso Padoa-Schioppa put it: "complete and systematic consistency of [national] policies achieved without any institutional infrastructure is a dream"8. This is why the new French President has proposed creating a euro area "finance minister", which probably requires modifying the existing Treaties. This finance minister would embody and bring to fruition the shared commitment of our Member States. As I also mentioned this idea before9, let me share some personal views on the issue. With great respect for the principle of subsidiarity, the finance minister would need to be: first, institutionally strong, by being both the Economic Commissioner and the President of the Eurogroup; second, democratically legitimate, by being accountable to the European Parliament in an adequate format; third, technically supported, by relying on a European Treasury - which would be largely based on the expertise of European Commission staff - and on an independent advisory Economic Policy Council, and coordinating the European Stability Mechanism and the crisis management framework; and finally, internationally recognised as the economic spokesperson of the euro area, alongside the ECB President for monetary policy.

In the longer term, as mutual trust between euro area countries increases, a last step will have to be considered to complete our common investment capacity: a genuine euro area budget, led by the finance minister. This would be a powerful tool. However in no way is this euro area budget to be confused with a one-way "transfer union" - and here I understand the German fears. It should potentially benefit all - not only the weaker - euro area countries, and would be rooted in increased economic convergence. The euro area budget would be used to finance certain "European public goods" such as digital technology, the energy transition or the integration of refugees. It could also include a European-wide unemployment insurance scheme. And to be effective, it would need to be able to directly issue common debt - for the future - and/or raise taxes. Obviously this would be a "quantum leap" in the nature of our Union, which would require resolute political will, but this is our chance to make a real difference.

***

Ladies and gentlemen, let me conclude by quoting a British citizen, who happened to be one of the greatest Europeans of the past century. Winston Churchill said in August 194910: "I am certain that it is within our powers to overcome the dangers still before us, if we so wish. Our hopes and our work point to an era of peace, prosperity and abundance and the inexhaustible wealth and genius of Europe will turn it once again into the very source and inspiration of the world's life." The European Union remains to this day a unique political and economic experiment that has no equivalent in modern history. And we have from 2017, following the electoral cycle in Europe, a unique window of opportunity. Nothing should be taken for granted, but much is open. We should not let this opportunity pass us by. Thank you for your attention.

1 "Tommaso Padoa-Schioppa: Economist, policy-maker, citizen in search of European unity", Speech by Lorenzo Bini Smaghi, European University Institute, Fiesole, 28 January 2011.

2 Source: European Commission, Reflection paper on the Deepening of the Economic and Monetary Union, May 2017.

3 European Commission, Standard Eurobarometer 86, Autumn 2016.

4 T. Padoa-Schioppa, "Capital Mobility: Why is the Treaty Not Implemented?", Address to the Second Symposium of European Banks, Milan, June 1982.

5 Pietro Catte, The Reform of the International Monetary System, Background note prepared for Conference in Memory of Tommaso Padoa-Schioppa, Rome, 2011.

6 T. Padoa-Schioppa, "The European Monetary System: A Long-Term View", in F. Giavazzi, S. Micossi, M. Miller, The European Monetary System, Cambridge University Press, 1988.

7 Banque de France, « Coût des carences de coordination des politiques économiques dans la zone euro », Bulletin de la Banque de France, n° 211, Mai-juin 2017. English version: "Cost of the lack of coordination of economic policies in the euro area", Quartely Selection of Articles no. 46 (Banque de France Bulletin), to be published in Summer 2017.

8 T. Padoa-Schioppa, "Capital Mobility: Why is the Treaty Not Implemented?", Address to the Second Symposium of European Banks, Milan, June 1982.

9 See for instance: speech at Bruegel in Brussels on 22nd March 2016 or speech before the Committee on Economic and Monetary Affairs of the European Parliament on 28 September 2016.

10 W. Churchill addressing the crowd on place Kléber in Strasbourg on 12th August 1949, day of the First Session of the Consultative Assembly of the Council of Europe.