Benoît Cœuré: Dissecting the yield curve - central bank perspective

Welcome remarks by Mr Benoît Cœuré, Member of the Executive Board of the European Central Bank, at the annual meeting of the ECB's Bond Market Contact Group, Frankfurt am Main, 16 May 2017.

Ladies and gentlemen,

Let me welcome you again and thank you for coming to Frankfurt to share your views and insights with us.1

As you might know, just a few weeks ago I gave a speech2 in Paris that addressed possible spill-overs from the repo market to the government bond market - a topic that you also discussed today and where I believe further work is needed to develop our understanding and guide policy deliberations.

In my remarks this evening I would like to address a different topic, but one that is no less important: how central banks interpret yield curve movements, and how this process might influence our monetary policy considerations.

Policy actions and the yield curve

Let me start by clarifying what I mean by "yield curve".

This is not a trivial discussion in a currency union with 19 different yield curves. Among these, we generally consider that two curves in particular provide us with insight and inform our policy decisions: the overnight index swaps (OIS) curve and the Bund curve, as these have become widely accepted proxies for risk-free yields in the euro area.3 As such, they serve as the bedrock for pricing virtually all credit products and related derivatives.

These curves are vital for the transmission of monetary policy, as they have a significant influence on broad asset valuations and the pricing of bank loans and, ultimately, they affect the investment and saving decisions of households and firms.

This means that we need to understand - as much as you do - what drives changes in these curves, so we can draw correct inferences regarding the appropriateness of our monetary policy stance. This has become all the more important in an environment where central banks no longer only control very short-term policy rates but also influence long-term yields through asset purchases.

In other words, we need to make a quantitative distinction as to what part of a given change in the yield curve is likely due to policy itself - our actions and often also our words - and what part is due to other factors, such as spillovers from abroad or improved growth expectations.

A natural starting point for such an analysis is the use of dynamic term structure models that divide yields into two key components - an expectations component and a term premium.

The expectations component reflects the average of current and future expected short-term rates over the maturity of the bond. If the pure expectations hypothesis of the term structure were to hold, this would be all that mattered in terms of explaining movements in long-term rates.

But broad empirical evidence suggests that the pure expectations hypothesis fails to hold true in practice, and that there is indeed a time-varying premium that investors require in order to hold a long-term bond instead of simply rolling over a series of short-term bonds.4

Monetary policy - and there we are increasingly certain - cannot only influence the expectations component, but also the term premium.

Three examples demonstrate this more clearly.

First, by changing our key policy rates, we can directly impact the short end of the curve - the footing of the expectations component. In normal times, medium to long-term rates would adjust to the extent that market participants would see a change in policy rates as the beginning of an incremental series of changes.

But with short-term policy rates approaching levels closer to zero during the early phases of the most recent easing cycle, this channel had become less effective. Markets - in the belief that rates could not enter negative territory - stopped short of pricing in the degree of accommodation they would normally have expected in the face of downside risks to our price stability mandate.

Our decision in June 2014 to introduce negative deposit facility rates restored our ability to steer market expectations and thereby also medium to long-term rates. Indeed, by signalling to the market that policy rates could go below zero, we ultimately succeeded in shifting downwards the entire distribution of future expected short-term rates, thereby providing important additional accommodation.5

Second, and related, by communicating about where we see the economy heading, and by clarifying our 'reaction function' - that is, by providing forward guidance - we can directly influence expectations regarding future short-term rates.

Forward guidance has served us well and has contributed to keeping the short to medium end of the yield curve well anchored at times when external shocks were threatening to unduly tighten financial conditions.

I will come back to this in a minute. But to the extent that forward guidance reduced uncertainty about the future path of interest rates, it has not only affected the expectations component but also the term premium.

Yet, the main channel through which we - and other major central banks - have recently exerted measurable downward pressure on the term premium, and this is my third example, is through asset purchases. We now have a growing body of evidence that suggests that central banks can lower long-term rates by removing duration risk from the market.

For example, according to ECB estimates, our monetary policy measures have contributed to reducing euro-area long-term risk-free rates by around 80 basis points since June 2014.6 Asset purchases have contributed significantly to this drop and have therefore been an indispensable tool to create the financial conditions necessary for inflation to move back towards levels consistent with price stability.

An assessment of recent long-term yield dynamics

So, you can now easily see that the increased use of non-standard measures also meant that there was a pressing need to upgrade our internal analytical toolkit. Standard term structure models alone were no longer sufficient.

We needed to broaden our set of models to also capture the effects that changes in the amount of bonds available for private investors would have on the term premium. And we needed to refine our event study methodologies and make use of other models and tools, with a view to developing our understanding of the extent to which our actions are reflected in yield movements.7

Put differently, these efforts were necessary in order to map (expected) purchases in billions of euro into long-term yields in basis points that would help the Governing Council calibrate the pace and size of our purchases.

The residual movement in rates - subject of course to the general large uncertainty one faces when relying on model-based analysis - would then be due to other forces largely outside our direct control. These include, for instance, spillovers from other major economies, flight-to-quality related movements into safe assets, or changes in investors' outlook for growth and inflation.

And as central bankers we also need to carefully disentangle those residual driving forces to help us understand the possible implications for our policy stance.

Let me give you a simple example: an unexpected increase in long-term rates. This is neither good nor bad, per se, from a monetary policy perspective. The implications for monetary policy depend, crucially, on the sources of this movement.

For example, if the increase reflects a re-pricing based on better current or prospective economic conditions, this would not be a source of concern for policy makers. However, if it were induced by markets overreacting to news or misunderstanding our policy intentions, this increase would be undesirable from a policy perspective.

It also matters for policymakers whether movements in nominal yields are driven by their real or inflation components, in particular at longer maturities. And changes in the inflation component, in turn, do not necessarily signal changes in expected inflation - they may also reflect changes to the inflation risk premium as I will explain in a minute.

The academic literature has come up with a range of techniques that we can draw from to separate these unobservable underlying driving factors from observable yield movements.8

However, unlike academic studies that have the luxury of looking at past events over extended periods to distinguish certain patterns and develop convincing economic stories, we have to make such judgements in real time.

Let me illustrate this by focusing on the repricing in bond markets that started around the end of September last year.

By that time, the ten-year OIS rate had reached a low point of slightly below zero. Since then - and looking through the occasional ups and downs - it has risen by about 65 basis points.

At face value, such tightening of financial conditions looks inconsistent with the stance required to bring inflation back to levels closer to 2%.

But the set of models currently in use by ECB staff generally tell one consistent story: for the most part, the steepening of yield curves over the past few months reflects an overall benign increase in the term premium - only around a quarter of the change in yields reflect changes in the expected future policy path. By and large this is also what we have seen in other major economies, in particular in the US.

We think two factors can mainly account for this. First, a decomposition of euro-based inflation-linked swap rates points to a measurable increase in the compensation for inflation risk from historically low and probably negative levels. So, from this angle, the increase in the term premium is likely to reflect a pricing out of deflationary tail risks. This in itself is certainly good news.

The second factor that is likely to have added to the increase in the term premium is uncertainty, mainly coming from outside the euro area. One reason might be that although markets have generally become more optimistic about global growth prospects - buttressed by the undeniable upswing in the global business cycle - they may have also become less certain about the future course of fiscal policy in some jurisdictions as well as about other policies, including trade and regulation. This, in turn, may increase uncertainty about future duration supply, impacting the term premium.

Uncertainty, by and of itself, is undesirable. But to the extent that the increase in the term premium likely reflected a reassessment of global economic conditions after a long period of subdued macroeconomic expectations - as also reflected in the adjustment of inflation risk premia - it may not constitute an unwarranted tightening.

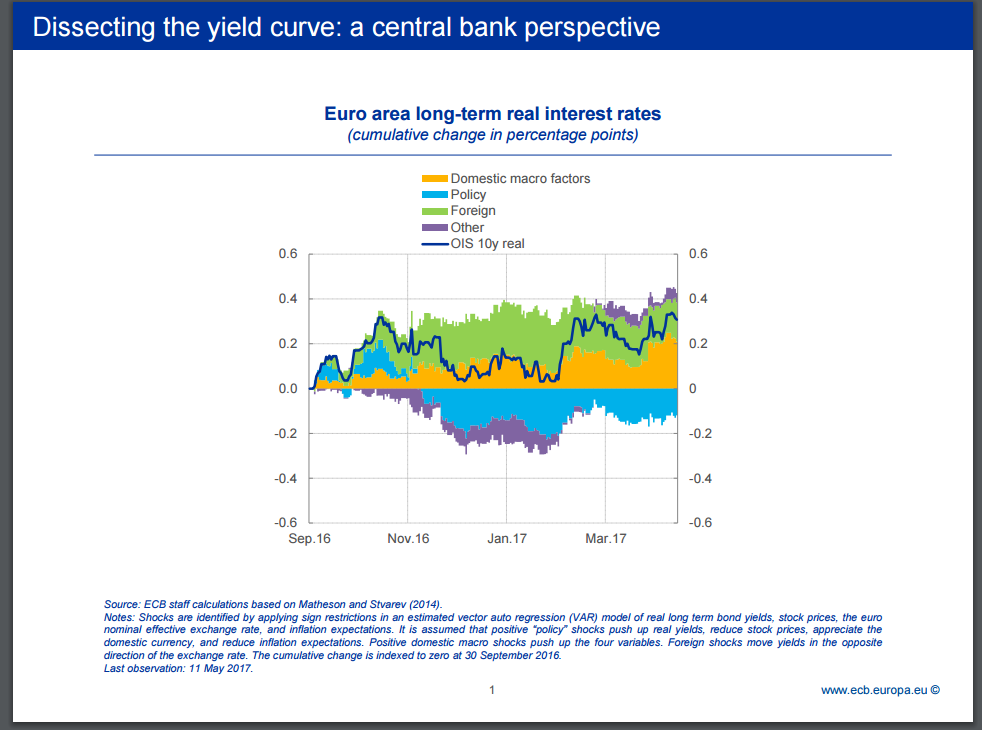

The role of foreign factors in driving euro area yields becomes clearer when considering the indications from another class of models: researchers at the IMF have developed a simple yet powerful methodology to identify yield curve drivers using cross-asset correlations involving stock, bond and exchange markets.9

And these models confirm - as you can see from the chart in front of you - that the bulk of the increase in euro area long-term yields initially came from shocks originating from outside the euro area - the green part.

You can also see, however, that after the first initial sharp upward movement in yields following the US presidential elections, it was increasingly an improvement in euro area domestic growth prospects that contributed to upward pressure on yields. You can see this reflected in the increasing contribution of the yellow component in the chart.

But what is even more important is that during this period, and despite stronger global and domestic growth prospects, expectations regarding our monetary policy have, on balance, had a stabilising effect on yields, according to our analysis. This is the blue part in the chart, which you can see shifted into negative territory after our decision in early December to extend the intended horizon of the APP by another nine months.

In other words, market participants understood our reaction function and agreed with our assessment in December last year that the absence of a sustained adjustment in the path of inflation warranted continued monetary accommodation.

Conclusion

This implies, and with this I would like to conclude, that the recent measurable increase in long-term yields has not affected our monetary policy stance: current financial conditions remain highly supportive of the ongoing recovery.

However, and this is what I wanted to convey in my short remarks this evening, identifying the drivers of yield curve movements in real time is a challenging task. For this reason, we look at a wide range of information and models to obtain a robust assessment. This also means that we don't want to over-interpret any uptick or downtick that we observe, but rather accept as a fact that some volatility is natural and healthy for the market to function.

At the same time, we don't want to contribute to that volatility ourselves. This is why we try to carefully explain the strategy underlying our actions and the resulting contingent plans. This is especially important when we are in uncharted territory with negative interest rates and asset purchase programmes.

I am convinced that clear and time-consistent communication on our part will avoid unwarranted volatility in financial markets and help preserve the financial conditions necessary for inflation to reach levels closer to 2% in the medium term.

Thank you for your attention and "guten Appetit".

1 I would like to thank W. Lemke and A. Saint-Guilhem for their contributions to this speech. I remain solely responsible for the opinions contained herein.

2 Cœuré, B. (2017), "Bond scarcity and the ECB's asset purchase programme", Speech at the Club de Gestion Financière d'Associés en Finance, Paris, 3 April 2017.

3 See also ECB (2014), "Euro area risk-free interest rates: measurement issues, recent developments and relevance to monetary policy", Monthly Bulletin, July 2014.

4 In principle the term premium can be positive or negative. Empirical studies find that recently the term premium has turned negative in certain regions.

5 For the effect of decreasing the lower bound on the yield curve see, e.g., Rostagno, M. et al. (2016), "Breaking through the zero line: The ECB's Negative Interest Rate Policy", Brookings Institution, Washington DC, 6 June 2016 (presentation available on the Brookings website) and Lemke, W. and A. Vladu (2017), "Below the zero lower bound: a shadow-rate term structure model for the euro area", ECB Working Paper No 1991.

6 See also ECB (2017), "Impact of the ECB's non-standard measures on financing conditions: taking stock of recent evidence", Economic Bulletin, Issue 2/2017; and Praet, P. (2017), "Calibrating unconventional monetary policy", Speech at the ECB and Its Watchers Conference, Frankfurt am Main, 6 April 2017.

7 See, e.g., Altavilla, C., G. Carboni and R. Motto (2015) "Asset purchase programmes and financial markets: lessons from the euro area", ECB Working Paper No 1864; Andrade, P., J. Breckenfelder, F. De Fiore, P. Karadi and O. Tristani (2016), "The ECB's asset purchase programme: an early assessment", ECB Working Paper No 1956; and Blattner, T. and M. Joyce (2016), "Net debt supply shocks in the euro area and the implications for QE", ECB Working Paper No 1957.

8 See, e.g. Joslin, S., K. J. Singleton and H. Zhu (2011), "A new perspective on Gaussian dynamic term structure models", Review of Financial Studies, vol. 24; and Abrahams, M., T. Adrian, R. K., Crump, E. Moench and R. Yu (2016), "Decomposing real and nominal yield curves", Journal of Monetary Economics, vol. 84.

9 See Matheson, T. and E. Stavrev (2014), "News and Monetary Shocks at a High Frequency: A Simple Approach", IMF Working Paper 167.