Rodrigo Vergara: Chile's September 2016 Monetary Policy Report

Presentation by Mr Rodrigo Vergara, Governor of the Central Bank of Chile, of the Monetary Policy Report before the Honorable Senate of the Republic, Santiago de Chile, 7 September 2016.

The Monetary Policy Report of September 2016 can be found at http://www.bcentral.cl

Introduction

Mr. President of the Senate, Mr. Ricardo Lagos-Weber, honorable senators, ladies, gentlemen,

I thank you for inviting the Board of the Central Bank of Chile to present our Monetary Policy Report. As it does in September each year, this issue coincides with the Central Bank's Report to the Senate, presenting our vision of the recent macroeconomic and financial developments in Chile and abroad, together with prospects and implications for monetary policy conduct.

After more than two years above the tolerance range, last July the CPI's annual inflation descended to 4%. The baseline scenario that I will be sharing with you in a minute assumes, as do private expectations, that it will continue to approach the 3% target in the coming months, to close the year at 3.5%.

Why has it been so high for so long? We can blame it on the significant depreciation of our peso, driven by the much needed readjustment of an economy confronted with the end of the commodity price supercycle, the end of a very pronounced cycle of mining investment, and a domestic weakening associated with a decrease in the country's capacity for long-term growth.

The contribution of the Central Bank to this transition has been a more expansionary monetary policy that has smoothed the cycle and supported the depreciation of our currency, within a flexible exchange rate scheme. Although such depreciation has transitorily increased inflation, it has aided the necessary resource allocation across sectors. All this has occurred in a context where inflation expectations and monetary policy credibility have remained intact.

As I mentioned, this Report's baseline scenario foresees inflation declining further, to converge to 3% somewhat sooner than we thought in June. This assumption estimates that, in the short term, the exchange rate will remain around its levels prevailing at the last statistical cutoff date. But of course, there are significant degrees of uncertainty, so the risks are still there.

One of our concerns in June regarding the external scenario was the so-called Brexit. However, and quite unexpectedly, its approval increased the markets' perception that the developed world's monetary policies would stay highly expansionary for a longer period of time, driving global financial conditions, particularly those facing the emerging world, to be more favorable than we assumed in the first half of the year. Despite a partial reversal in recent weeks, the mood of the markets is better than anticipated, even considering that the Federal Reserve is expected to raise its monetary policy interest rate again.

Services inflation-typically associated with non-tradables-has not changed much and is expected to continue decelerating gradually. Second-quarter data for activity and demand brought no surprises either, and the projections for this and next year, which I will analyze in more detail in a while, show only marginal changes.

Considering this, we have kept the monetary policy rate (MPR) at 3.5% for several months. At the same time, we have changed the bias of our monetary policy by stating that, if the baseline scenario comes true, there will be no need over the projection horizon to follow through with the increases we had foreseen up to the latest Report.

On the domestic front, like in June, our main concern has to do with the slow growth that the Chilean economy continues to experience. For this year we expect growth to be in the 1.5% to 2% range, and for next year it should be between 1.75% and 2.75%. If this is the case, the economy will complete four years growing on average around 2%. This is definitely not satisfactory, and is something we must not only worry about, but assume with top priority.

It should be noted that, although in our baseline scenario we expect no further deterioration of the global economy, neither do we expect a significant recovery of output and demand. This, in some way, makes it ever more important that, as a country, we deepen our analysis of those domestic elements that could be holding back growth in our economy.

Let me now present in more detail the macroeconomic scenario we believe to be the most likely in the quarters to come and its associated risks.

Macroeconomic scenario

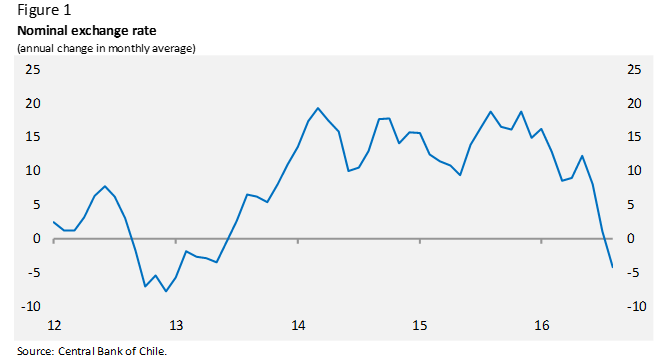

In July, annual inflation returned to the tolerance range. As I said, the behavior of the exchange rate has played a key role in this process, as it allowed us to leave behind the upward effects of the sharp depreciation the peso experienced in 2013-2015. Considering the average of the ten days prior to the statistical cutoff, the dollar was trading at somewhat less than 670 pesos, equivalent to a nominal appreciation of the peso of around 4% with respect to the close of the previous Report (figure 1).

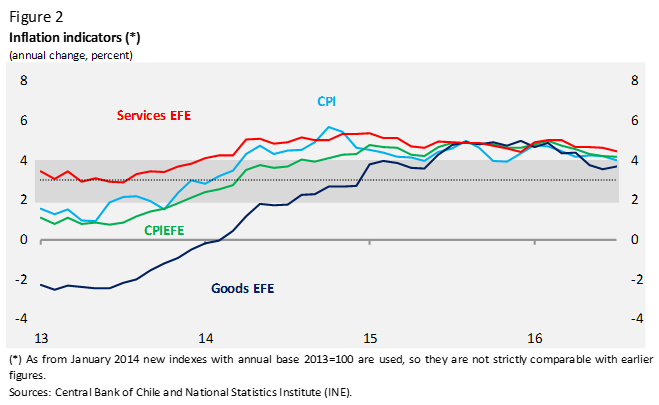

The evolution of the exchange rate has had visible effects on the goods component of core inflation (i.e., the CPIEFE, or CPI excluding foods and energy). In annual terms, it went from around 5% early the year, to 3.7% in its latest measurement. Inflation of the services component of the CPIEFE has made a smoother adjustment, from 5% to 4.5% annually in the same time span, reflecting its indexation to past inflation and output gaps that have not widened much. Accordingly, and as expected, the total CPIEFE has seen a reduction in its annual expansion rate. The more volatile items in the basket showed dissimilar movements in the past three months: while annual food inflation rose, energy inflation fell (figure 2).

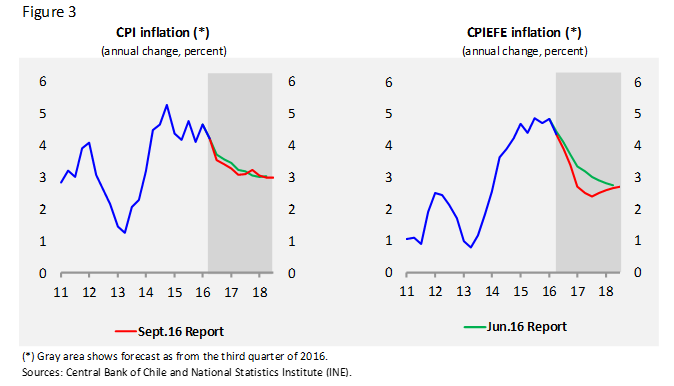

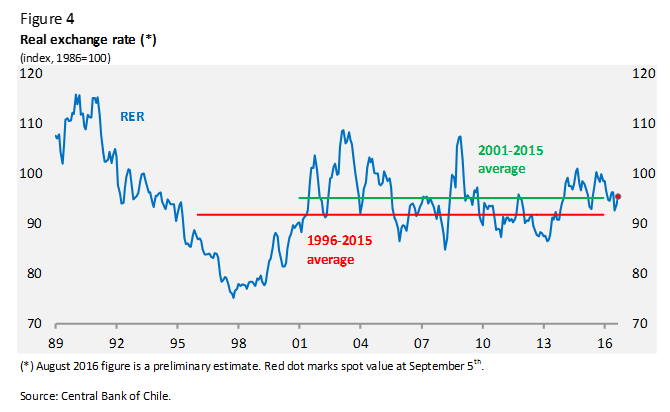

The baseline scenario of the September Report assumes that the CPI's annual inflation will continue to approach 3% in the coming months, closing 2016 at 3.5%. The CPIEFE will descend to 3% faster than will headline CPI, and by early 2017 it will be below this mark (figure 3). This scenario assumes that inflation will converge to the target somewhat sooner than we expected in June, which partly relies on the exchange rate remaining relatively stable over the short term. As I said, this is subject to significant degrees of uncertainty, as illustrated by the fluctuations that the parity has shown in recent months. As a working assumption, our projections consider that the real exchange rate (RER) will hover around its current levels throughout the projection horizon, in line with the assessment that today it is not far from what can be inferred from its long-term fundamentals (figure 4).

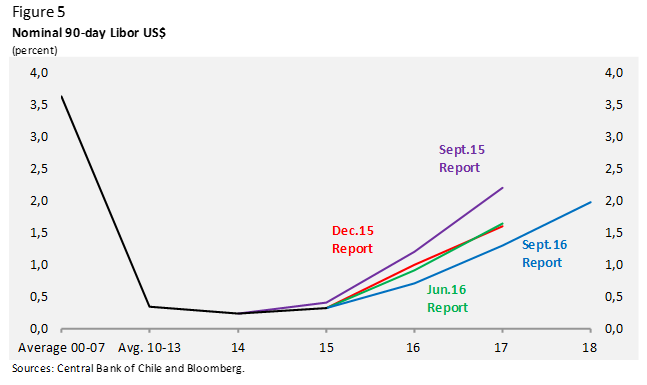

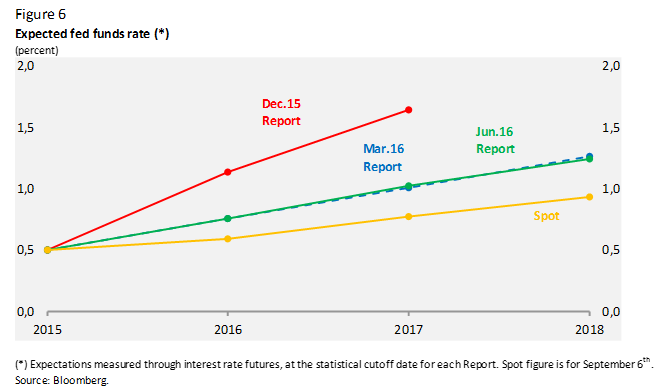

Globally, despite the reversal of recent weeks, external financial conditions facing emerging economies have outperformed our projections in earlier Reports (figure 5). This improvement has been accompanied by the markets' perception that the expansionary monetary policies in the developed world will persist for longer. In this context, the changes in expectations regarding the Fed's monetary policy conduct have been particularly important because of both its weight in financial markets and the uncertainties surrounding it (figure 6). The markets assume a more gradual normalization of monetary policy than that announced by the Fed. In any case, there are differing appreciations about how it will resolve the tensions between the dynamics of the real sector, inflation and exchange rate conditions in the US economy. In Japan, the UK and Europe, the markets expect policies to remain as expansionary, or be even more so, considering their weak economic growth rates and projected inflation exceeding their central banks' targets.

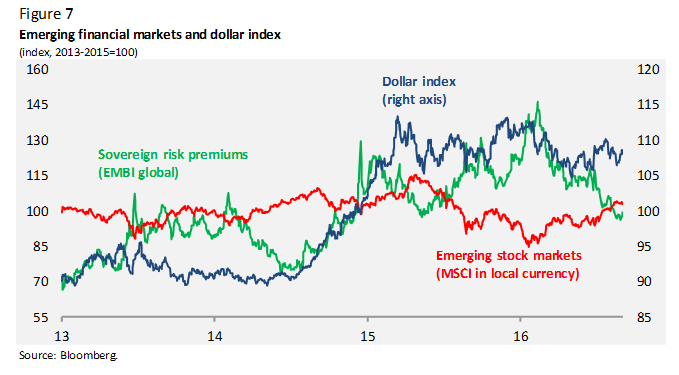

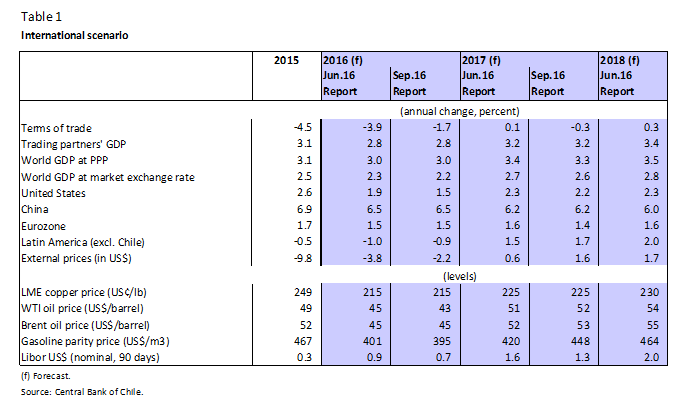

In this context, the fraction of fixed-income assets-including long term-with negative rates has increased considerably around the world. I draw your attention to this fact, because it was unimaginable some years back. Thus, higher risk appetite and the search for yield have pushed the prices of risky assets up, squeezing sovereign spreads and appreciating currencies vis-a-vis the dollar (figure 7). In any case, the intensity with which this change in financial conditions will impact activity or commodity prices is not so clear. In the baseline scenario, global activity projections do not change significantly. For the 2016-2017 biennium average growth in the world economy is expected to stand at 3.2%, while Chile's trading partners should grow by 3.0%, also fairly unchanged from June. The terms of trade will deteriorate less over the projection horizon, although the trajectories foreseen for the prices of copper and oil are similar to those of June, expecting prices in 2018 of US$2.3 per pound of copper and around US$55 per barrel of oil (table 1).

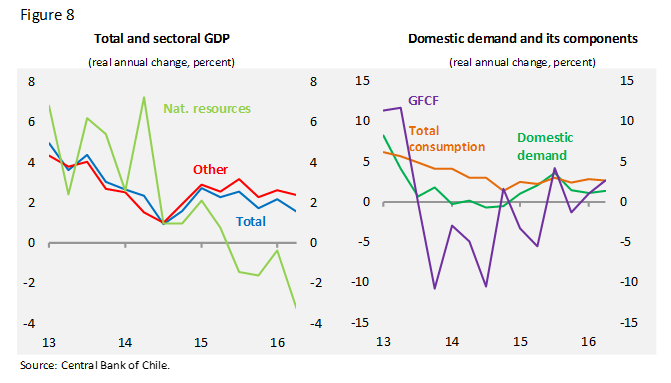

Locally, second-quarter data for domestic activity and demand confirmed bounded economic growth. GDP posted lower annual growth than in the first quarter, but with a configuration where natural-resource-related sectors -particularly mining- showed less favorable performance while other GDP changed little, if anything. The total consumption component of demand continued to grow at around 2.5% in annual terms, while investment posted positive growth, boosted by specific factors associated with imports of machinery and equipment. On the other hand, during the second quarter investment in construction and other works showed a sharper than expected fall, with a still weak real estate sector (figure 8).

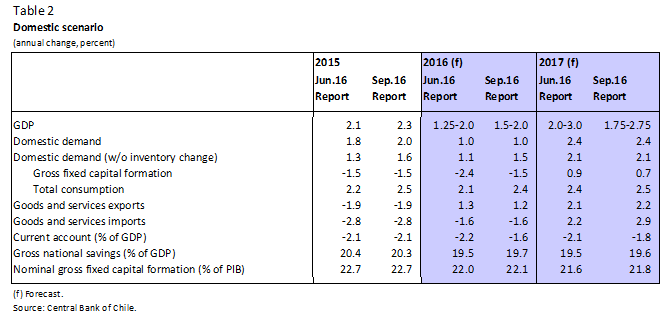

In this context, this Report's baseline scenario assumes that GDP will rise between 1.5% and 2.0% this year, considering that the information reviewed for the first half of the year brings no surprise with respect to our June projections. For 2017, a range is projected for GDP between 1.75% and 2.75%, down from expectations in June. Our forecast for 2017 GDP puts in in the 1.75% to 2.75% range, less than we expected in June. Domestic demand minus inventories should post a modest recovery in 2017: 2.1% annually, after growing 1.5% in 2016. In any case, we have upgraded our growth projection for this year from June, because we now estimate a smaller decrease of gross fixed capital formation, in particular because of the performance of the machinery and equipment item in the second quarter. However, this is partly offset by the expected annual fall in construction and other works, where a debilitated real estate sector stands out.

In 2017, we foresee that gross fixed capital formation (GFCF) will continue to grow around 1% annually, still affected by the drop in mining investment, but counterbalanced by growth in investment in other sectors. As a fraction of GDP, both real and nominal GFCF will still fall short of its 2015 figures. Real GFCF will average 22.7% of GDP in 2016-2017, while its nominal version will average 21.9% in the same biennium. As for consumption, the changes are smaller, as it is still expected to grow near 2.5% annually in 2016 and 2017, quite unchanged from 2015 (table 2).

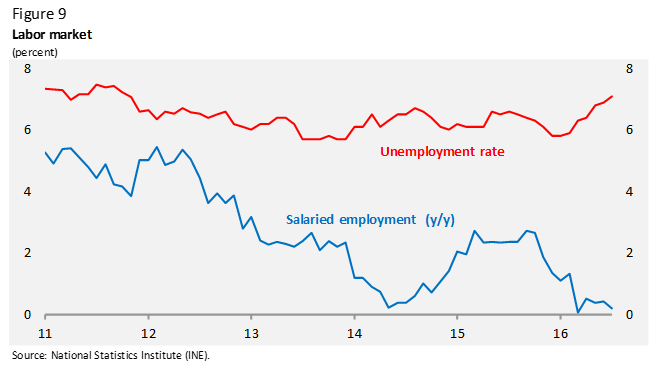

As a working assumption, we estimate that the trajectory of public spending will be consistent with the fiscal rule and the Administration's announcements that it will follow a path of budgetary consolidation. Another input is that the determinants of domestic spending have seen no major changes in the past few months. Imports of goods, leaving out some specific factors, show bounded growth, while business and consumer confidence remains low by historic standards. The labor market is adjusting gradually and is expected to adjust further in the baseline scenario (figure 9).

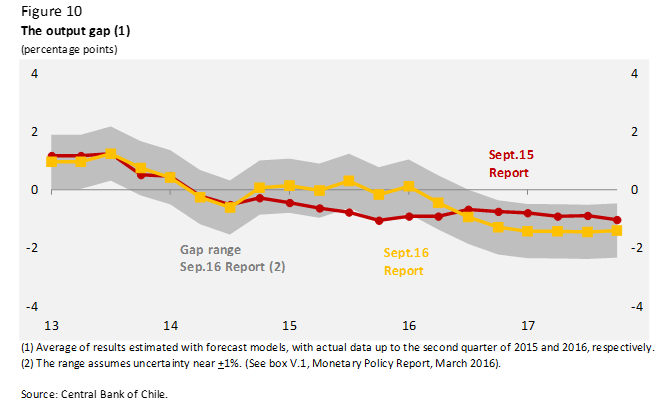

I should stress that these projections assume that the low figures for actual and expected investment have driven down both trend and potential GDP growth. May I remind you that by trend growth we mean the growth rate that is possible to achieve in the medium term. Potential growth differs from trend growth in that it can be affected by temporary shocks to productivity and constraints to factor use that may alter our productive capacity over the short term, but not in the long. That is why our trend GDP growth estimates are a little higher than our potential growth estimates.

Our latest evaluations place trend growth at 3.2%, three tenths of a point less than year ago estimates. Meanwhile, we forecast potential growth for 2016 and 2017 between 2.5% and 3%, compared with the 3% to 3.5% range estimated last year for the same period. Moreover, incoming figures suggest that potential growth will take longer to converge with trend growth. Anyway, our assessment of the current output gap is not very different from what we foresaw a year ago. This, because although since then we have revised downward our 2016 GDP growth figure by something more than one percentage point, at the same time we lowered our estimate for potential growth and 2015 GDP growth was revised up (figure 10).

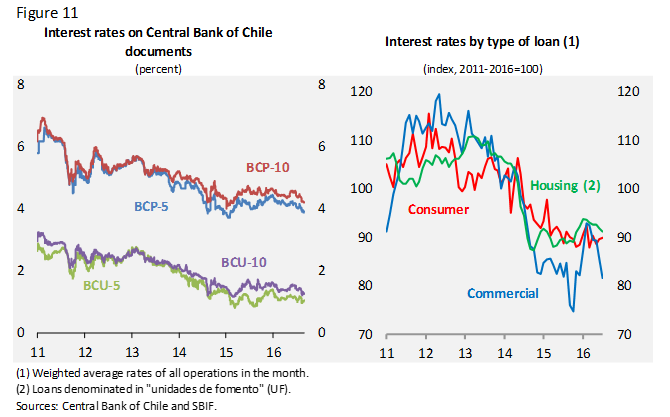

In recent months, financial conditions from the standpoint of borrowing costs have remained favorable. The fees charged in commercial, consumer and mortgage loans are near record lows. At the same time, growth in the stock of consumer and commercial loans has recovered from a year ago. The opposite is true of mortgage loans, which have decelerated from earlier this year. This low credit cost coincides with also low long-term interest rates. The latter responds to both the expansionary monetary policies in Chile and around the world and more structural conditions (figure 11). In any case, qualitative information, such as the Bank Lending Survey for the second quarter and our August Business Perception Report, shows that a weaker demand for credit is perceived. According to the respondents, this is due to a shortage of investment projects and job security fears.

Turning to our monetary policy, if the macroeconomic scenario that has been taking shape over the past few months consolidates, with external financial conditions that, while volatile, are better than we projected in June, where gaps are bounded and inflation is returning to the target a little earlier, we see no need to make any new increases in the policy rate over the policy horizon. Accordingly, we use as a working assumption that the monetary policy rate will be kept unchanged during the projection horizon. As always, any monetary policy measure or adjustment to the rate will be conditional on the expected effects of incoming information on the projected inflation dynamics.

Some thoughts I wish to share on monetary policy conduct. For two and a half years, inflation has been above the Central Bank's defined tolerance range. The main reason being, as we have said time and again, the increase in the exchange rate, which was necessary in the new conditions facing the Chilean economy. Because it was a one-time shock and therefore with transitory effects on inflation, tightening the policy was less than optimal.

Most recently, the exchange rate broke the upward trend it followed for several quarters. Actually, it has dropped compared with its levels early in the year. Symmetric to our previous actions, if for this reason inflation were to fall temporarily below our target, we would not apply a more expansionary monetary policy, unless after some time we saw second-round effects jeopardizing the return of inflation to 3% over a two-year horizon.

Importantly, any changes in the policy stance in either direction can be warranted only if our medium-term inflation forecast suggests that it will deviate away from the 3% target. Of course this would be determined by changes in its fundamentals.

What are the risks we identified in our baseline scenario?

On the external front, one of the main risks is a reversal of the improved international financial conditions. As I said, the path that the Fed will ultimately take to adjust the policy rate is critical. An increase in the fed funds rate is very likely within this year, and the markets' expectations point at very gradual subsequent adjustments. A more aggressive action by the Fed could increase global volatility significantly, affecting asset prices, capital flows and currencies. The Brexit vote materialized one of the risks outlined in June but, to this date, its effects seem bounded. However, its true consequences are still in the making, so further repercussions on medium-term growth in the UK and Europe cannot be ruled out. Add to this the concerns about the soundness of part of European banks, particularly in Italy and Portugal. And let's not forget several open electoral processes around the world, whose results could cause a shift towards more protectionist policies.

In the emerging world, the overall risk outlook has tended to moderate in the past few months. Accordingly, concerns about China have eased, while the Chinese impulse policies have stabilized the pace of growth. Significant risks remain, however, namely the doubts surrounding the sustainability of these measures over time, as well as about the Chinese financial system and real estate sector, among other factors. Moreover, a scenario in which the Fed's monetary policy becomes more aggressive may have important negative implications on China. In Latin America, beyond very recent improvements, adjustments to both public and private spending are still needed.

Domestically, short-term inflationary risks remain tied to the evolution of the exchange rate and, therefore, to the risks coming from abroad. In any case, inflation expectations two years out have remained near 3%. On the output side, the improved external financial conditions could affect growth more than previously estimated. Meanwhile, business and consumer expectations are still in pessimistic territory, which could hold back the recovery of consumption and investment, triggering a sharper deterioration of the labor market.

Having assessed these risks, we estimate that the risk balance is unbiased for both inflation and activity.

In a nutshell, inflation has declined as expected, and our forecasts point at a faster convergence to 3% than we thought in June. Our output and demand outlook is fairly unchanged. There are still risks in our external scenario, even if its recent evolution surprised us for the better.

Allow me some final reflections.

Final reflections

I will end with some thoughts on the capacity of monetary and fiscal policy to address the economic cycle. I think we must because, after years of slow growth and within a context of increasing social demands, pressures on both have become stronger and the way we decide to confront them will be crucial in the future of our economy and our country.

I see three main challenges:

First, it is obvious that neither monetary nor fiscal policy can flatten out the business cycle, much less affect the economy's trend growth. But they certainly can smooth the cycle and help the economy make sound adjustments when suffering a domestic or external shock.

Anyway, the capacity to smooth the cycle is proportional to the medium-term sustainability of these policies. Why? It is very simple: economic decisions -think of investment, for example- depend not only on such policies' immediate effects, but also on how the various economic agents expect them to continue to affect the economy in the future.

Thus, even if we believe that the effects of some policy action can be very powerful, if the agents consider that implementing that policy will be inconsistent with the macroeconomic equilibria, its effects will be diminished and may even be counterproductive.

In the case of fiscal policy, this problem has been properly addressed in our country by way of a fiscal rule that establishes that fiscal spending must be consistent with the economy's capacity to generate earnings in the medium term. This rule has been carefully monitored, and has even been replicated in other countries. Ending it could not only result in many problems in the future, but also lessen the macroeconomic effects of fiscal spending today.

Make no mistake: I am not for total inflexibility, nor am I for mechanically subscribing to a rule, as I am convinced that flexibility is necessary on certain occasions. This has been the case, actually.

My concern is rather whether we have exhausted these degrees of flexibility. Let me remind you that just over one year ago the initial structural balance (or zero deficit) objective was modified. In addition, to accommodate revisions to the long-term price of copper and trend GDP-both potentially curbing the spending capacity-the Ministry of Finance decided to recalculate the rule every year using the new parameters, and from there reduce the structural deficit by 0.25 percentage points of GDP.

No doubt this is one way to adjust gradually to the new boundaries that the rule establishes for fiscal spending, but it obviously implies that in a cycle where the key parameters are revised downward, we will be spending above our medium-term revenues for a longer period of time. The low net debt of the Treasury, courtesy of a responsible fiscal policy, has allowed for this gradual adjustment without major surprises. However, there are limits and the debt has been increasing. In this context, I am particularly concerned that the accumulation of commitments could end up straining our public finances.

In the case of monetary policy, the limit comes from credibility. There is an explicit objective-the inflation target-and a market that monitors on a daily basis to see whether our monetary policy conduct is consistent with achieving that objective.

For as long as the market remains confident in the Bank's capacity and, above all, on its commitment to take inflation to 3% in the two-year horizon, an expansionary monetary policy will be successful. The minute we lose that confidence, we will fail.

That is why we are adamant about our concern with inflation expectations, insisting that we will do whatever it takes for it to stand at 3% over the forecast horizon. The good news is that we have succeeded: despite inflation's high volatility, due mainly to the sharp variations in the exchange rate, expectations two years out have remained at 3%. This encourages us to keep our guard up and not to neglect what has been achieved or try to extract from monetary policy more than it can deliver.

The second challenge is that experience suggests that our first line of action to deal with the cycle is monetary policy. This is the main reason for the expansionary nature of our policy making in recent years, even with inflation being persistently above the target range. Keep in mind that the fiscal rule determines a generally acyclical public expenditure, meaning that it runs independent from the business cycle. Why? Because fiscal policy is typically slow to react and any change in spending decisions are much more difficult to undo.

Thus, monetary policy is essential to deal with the economy's cyclical fluctuations. That explains our actions. Since late 2013 we have implemented a clearly expansionary monetary policy, indeed one of the most expansionary among emerging market economies. Real short-term interest rates have been negative or barely above zero for all this time, helping medium- and long-term rates to be nearly as low as they have ever been.

This policy has not only helped the economy to adjust smoothly by providing support to aggregate demand; by letting the exchange rate move freely it has also contributed to the adjustment of relative prices-a key element to address in these conjunctures. The contrast with other episodes is evident. Suffice it to recall the costs associated with the defense of the exchange rate in the early 1980s and, to a lesser extent, during the Asian crisis and its aftershocks in the late 1990s.

Even if this episode has driven inflation above the tolerance range, the main issue from the standpoint of monetary policy is that inflation expectations have always been anchored to the target. And if at some point it seemed that they could deviate, we acted promptly to prevent it. There is no doubt in my mind that the main reason were the actions of the Central Bank of Chile, which attest to its commitment with its constitutional mandate to keep inflation low and stable. This record has played an essential part in our solid reputation.

The third-and especially important-challenge is that we must never lose sight of the fact that the benefits of boosting medium- and long-term growth greatly outdo those of smoothing the cycle.

Hence, it is critical that as a country we put special emphasis on medium-term growth. We should think particularly carefully how it is affected by the various policies adopted, and strengthen those that favor it. Without growth, there are simply no resources to deepen social policies.

As I mentioned when I presented our June Monetary Policy Report, we are one of the few countries in the region that have approached the borders of development. In the past, other countries fell short of the opportunity. Grabbing it depends on us only. Commodity cycles and international windfalls come and go. In the long run, countries are the masters of their own destinies, and behind those that developed and provided a better standard of living to their people are the good public policies they implemented.

Ladies and gentlemen: in a few months I will be concluding the five-year term established by the Constitutional Law for the governors of the Central Bank of Chile. I believe that, although the past few years have been quite complex, the joint efforts of the Bank's staff and Board members have helped us succeed in our mission. I take this opportunity to thank you for all your support during this period.

Thank you.