Simon M Potter: Concluding remarks at the Monetary Policy Implementation in the Long Run Conference

Concluding remarks by Mr Simon M Potter, Executive Vice President of the Markets Group of the Federal Reserve Bank of New York, at the Monetary Policy Implementation in the Long Run Conference, Federal Reserve Bank of Minneapolis, Minneapolis, Minnesota, 19 October 2016.

Thank you for participating in the conference "Monetary Policy Implementation in the Long Run" here at the Federal Reserve Bank of Minneapolis. Over the past two days we have engaged in productive and thought-provoking discussions of the evolution of monetary policy implementation across global central banks. These discussions will help shape the way the Federal Reserve thinks about monetary policy implementation in the future.

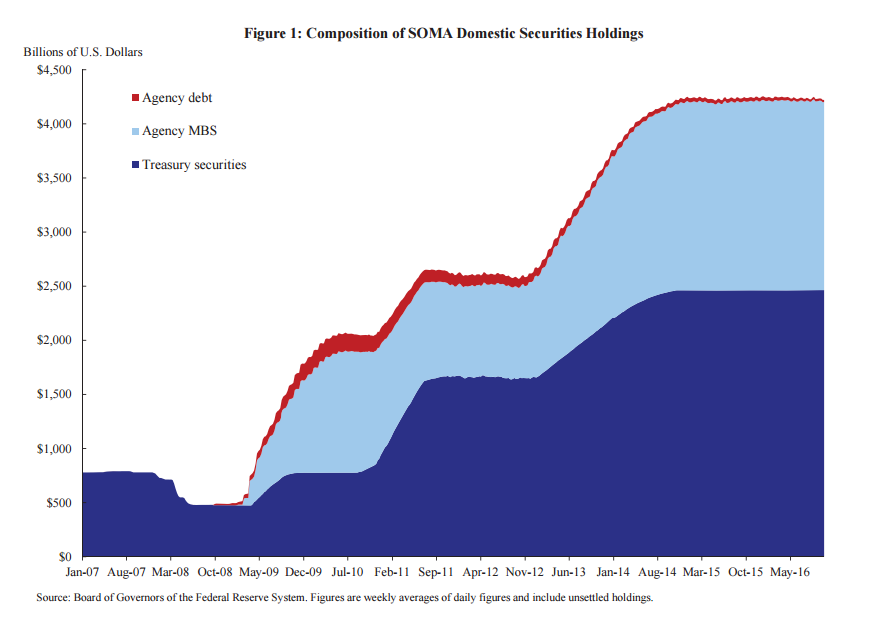

The Federal Reserve's implementation of policy has evolved in important ways in recent years, including using the balance sheet as an active policy tool at the zero lower bound (ZLB). Through a series of large-scale asset purchase programs (LSAPs), the Federal Reserve's balance sheet expanded to include more longer-term Treasury securities and two additional asset classes, agency debt and agency mortgage-backed securities (MBS).1 Agency MBS currently represent more than 40 percent of the System Open Market Account (SOMA) domestic portfolio.2

Furthermore, in order to maintain the size of the SOMA's agency holdings, the New York Fed's Open Market Trading Desk (the Desk) continues to reinvest principal paydowns on agency MBS and agency debt into agency MBS each month.3 In my remarks today, I will share some reflections on LSAPs at the ZLB and the flexibility that access to the agency MBS market gives the Federal Reserve to execute such programs. Before I begin, however, let me remind you that the views I express are my own and do not necessarily reflect those of the Federal Reserve Bank of New York or the Federal Reserve System.

Large-Scale Asset Purchase Programs

Currently, all the major advanced-economy central banks are either at or close to the zero lower bound. Their approach to adding policy accommodation with a near-zero overnight policy rate has been to use outright purchases of assets, term lending schemes, and forward guidance on these policy tools.4 The policy of outright purchases of assets is often called quantitative easing (QE) because of the Bank of Japan's earlier policy focused solely on increasing the size of the central bank's liabilities.5 While QE is a useful catch-all term for this set of policies, it masks the fact that central banks make different choices in the assets they buy to expand their balance sheets.6 Central bank laws specifying which assets can be purchased and held outright vary, although nearly all central banks can buy and hold the debt issued by their sovereign.7 Indeed, most of the empirical work on the effectiveness of LSAPs is based on the analysis of sovereign debt purchases. More recently, a number of central banks have extended their purchases into the corporate debt and asset-backed securities markets. The Federal Reserve Act does not permit the purchase of privately issued debt such as corporate debt or privately issued ABS. While this might appear to be a constraint for the Federal Reserve, purchases of non-sovereign debt by other central banks have been small-both in size and as a percentage of GDP-compared with the Federal Reserve's purchases of agency MBS, which are guaranteed by federal agencies and can affect private borrowing rates.8

In expanding their balance sheets through asset purchases, central banks must consider how their choice of assets-for example, sovereign debt, corporate bonds, or federal agency debt-will affect the policy transmission mechanism. Central banks must also take into account any implementation challenges related to executing in a given market. There are many broad transmission channels through which an LSAP program can provide additional monetary accommodation:

- Increasing the monetary base and central bank liabilities-the QE channel

- Reinforcing that interest rates will remain low-the signaling channel9

- Changing the quantity and mix of financial assets held by the private sector-the portfolio balance channel

- Taking interest rate risk out of the private sector-the duration channel

- Taking credit risk out of the private sector-the credit channel

- Taking prepayment risk out of the private sector-the prepayment channel

- Improving market function-the market function channel

The purchases of different assets will have different degrees of impact across these channels. For example, sovereign assets will generally work primarily through the first four channels, while corporate bonds would also work through the credit channel and MBS would also work through the prepayment channel. For these first six channels, one can argue that it is the expected stock of security holdings to be purchased by a central bank that chiefly determines the amount of accommodation-that is, the impact the central bank's purchases are expected to have on the size and duration of assets available to the public. Alternatively, for the market function channel, the "flow" effects are most important, in that the transactions associated with a central bank's asset purchases can also affect an asset price by altering market liquidity and functioning, although such effects may dissipate quickly. This channel could achieve monetary accommodation through the purchase of any security type in which market functioning has become stressed. One example is the European Central Bank's Securities Markets Programme, which was designed "to address the malfunctioning of securities markets".10

The purchase of non-sovereign assets can be helpful by providing additional channels for monetary accommodation to be realized. Further, having additional markets to operate in can help central banks overcome functional limitations that could exist if they were restricted to LSAPs in only one market. For example, the stock of assets held by the private sector in a given market might be too small to meet the monetary policy goal. Or, the purchase of a large amount of the existing stock of a given market might result in impaired market functioning, which, in the extreme, could impair the effectiveness of the LSAP and other monetary policy tools. Lastly, when participating in non-sovereign markets for the first time, a central bank might need to learn more about the asset class and build or refine the internal systems needed to operate in that market.11 In all these cases, a central bank might choose to diversify across different asset classes to achieve its policy objective.

With these considerations in mind, I now want to turn to a discussion of the large-scale asset purchase programs pursued by the Federal Reserve. My focus will be on the Fed's agency MBS purchases-which provide the central bank with an additional policy transmission tool and significant additional capacity to provide policy accommodation. Although the purchase of U.S. Treasuries is not central to my remarks, it is important to note that the Federal Reserve is fortunate in having a sovereign debt market that is the deepest and most liquid in the world and is sufficiently large that there are no close capacity limits. The experience with the three LSAP programs and the Maturity Extension Program showed that the Federal Reserve was able to purchase Treasuries at a fast pace without affecting market functioning.

Before continuing to the main part of my discussion, I would also note that my intention is to consider the practical and operational issues surrounding the implementation of LSAPs, rather than to debate the merits of LSAPs relative to other potential monetary policy tools. There are a number of important issues linked to the potential costs of LSAPs but unrelated to these implementation issues. Policymakers' judgments on these costs, such as financial stability impacts, political economy ramifications, and the effect on the consolidated fiscal situation, will be critical in assessing the overall costs and benefits of LSAPs.12 These caveats are particularly important to bear in mind in looking at the agency MBS market, since many might argue that the main issuers in the agency market gained private benefits at the expense of the taxpayers in the period prior to the financial crisis.13

Overview of the U.S. Agency Mortgage Market

In depth and liquidity, the agency MBS market is second only to the U.S. Treasury market domestically; it is also deeper than most foreign sovereign debt markets. The fixed-rate agency MBS market currently has roughly $5.7 trillion outstanding, with an estimated average daily trading volume of approximately $200 billion in 2016 year-to-date.14 In contrast, the slightly larger U.S. corporate market has an average daily trading volume of only $30 billion per day.15

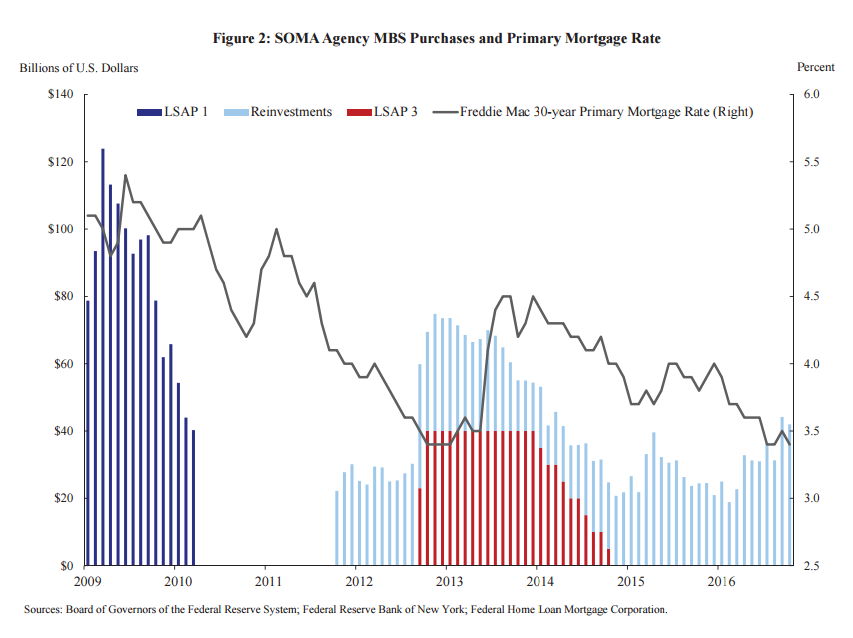

The substantial trading volume and liquidity of the agency MBS market are due, in large part, to the existence of the to-be-announced (TBA) MBS trading convention. This structure provides investors with the ability to trade a wide range of MBS with similar characteristics without requiring them to analyze the underlying details of each individual mortgage security, since any security with the same agency issuer, original maturity term, and coupon can be delivered into a single TBA contract.16 This transforms a market of hundreds of thousands of individual mortgage securities into a limited number of homogenous TBA contracts. For example, in July 2016, the Desk purchased approximately $34.5 billion in agency MBS across only 10 different TBA contracts; upon settlement of those transactions the following month, SOMA received almost 2,000 different individual MBS securities. In addition, the TBA market trading convention allows for the use of dollar rolls (which extend the settlement date by one month) and coupon swaps (which allow the specific TBA contract being purchased to be switched). These trading tools have been used to facilitate efficient settlement and can alleviate market stress.17

The liquidity and market depth provided by the TBA trading convention facilitate the Desk's ability to conduct large-scale asset purchases in a non-sovereign market and to do so at a relatively fast pace without hindering market functioning. For example, the Desk purchased more than $1 trillion agency MBS in 2009 and almost $800 billion of agency MBS in 2013. These purchases allowed the SOMA portfolio, which owned no agency MBS at the end of 2008, to expand its agency MBS holdings to approximately $1.76 trillion by October 2014.18

SOMA agency MBS holdings have been maintained near this level since the end of the latest purchase program on October 29, 2014. These holdings constitute approximately 10 percent of GDP and account for almost one-third of the universe of fixed-rate agency MBS. The SOMA portfolio of agency MBS is considerably larger than the portfolios of non-sovereign debt that other global central banks have purchased, which represent about 5 percent of GDP and less than 10 percent of each individual market.19 Similarly, purchases can be conducted at a pace that provides a meaningful level of accommodation without any adverse effects on market functioning.20 Over the past month, the Desk reinvested approximately $44 billion of principal payments from its holdings of agency MBS and agency debt in the TBA market.21

By comparison, purchases of non-sovereign debt at the ECB, BoE, and BoJ have all been at a pace of less than $15 billion per month.22

The payment structure of agency MBS is unique since the principal and interest of agency MBS are guaranteed by one of three federal agencies: Fannie Mae, Freddie Mac, and Ginnie Mae. However, the cash flows behind these securities are based upon the mortgage payments of millions of homeowners whose home mortgages have been securitized in an agency MBS. This structure allows the Federal Reserve to support private borrowing, and the housing market, while purchasing federal agency securities. This feature is important for policymakers to consider when deciding whether to operate in the agency MBS market or the Treasury market.

Agency MBS, like the underlying mortgages, have monthly payments of principal and interest. Homeowners also have the option to make additional principal payments each month, or to pay off the loan in full. Prepayment is especially attractive when interest rates fall and homeowners are able to refinance their loans into new loans at a lower interest rate. Investors demand an extra return to bear the risk of prepayment, which is incorporated into the yield of agency MBS. By purchasing agency MBS, the Federal Reserve can bear a considerable amount of this risk, removing it from the portfolios of private investors and thereby lowering mortgage rates. This outcome, in turn, stimulates additional demand for housing, and promotes increased refinancing activity. In the current environment, the Federal Open Market Committee (FOMC) has directed that principal payments from SOMA's agency debt and agency MBS portfolio be reinvested into agency MBS. Therefore, SOMA reinvests the monthly paydown of principal on an ongoing basis. As a result, the Federal Reserve maintains a regular presence in the agency MBS market with near daily purchase operations.

Review of the Federal Reserve's Two Agency MBS Purchase Programs

Since 2008, two LSAP programs have included the purchase of agency MBS. The primary goals of the two programs differed, reflecting the distinct market conditions and economic environment that existed at the time each was initiated. In LSAP 1, announced in November 2008, agency MBS purchases were chiefly designed to provide support to mortgage and housing markets and to foster improved conditions in financial markets more generally. In LSAP 3, launched in September 2012, the agency MBS purchases were primarily focused on providing overall policy accommodation.

In November 2008, there were significant dislocations in many financial markets, especially in the markets for the U.S. federal housing agencies' securities.23 In addition, the housing market was a focal point of the financial crisis. To help support the housing market and improve conditions in financial markets, the FOMC announced an LSAP program on November 25, 2008, that consisted of purchases of agency debt and agency MBS.24 The stated purpose of this program was to "reduce the cost and increase the availability of credit for the purchase of houses, which in turn should support housing markets and foster improved conditions in financial markets more generally."25 Research suggests that this program reduced "abnormal pricing" in agency MBS-the component of the spread considered to be due to market dysfunction-by about 70 basis points over its first six months.26 In that same time period, the spread of agency MBS repurchase agreements (repos) to Treasury repos fell from more than 200 basis points to near zero. In the framework noted above, this LSAP worked primarily through the market functioning channel. However, research also suggests that borrowing costs were lowered more broadly through a portfolio balance effect.27 Overall, the Desk's purchases, aided by the lowering of fed funds to the ZLB in December 2008, resulted in lower mortgages rates, which in turn reduced the cost of home purchases and allowed existing borrowers to refinance at more attractive terms.

Following the initial LSAP, the liquidity and market functioning of the housing agency securities largely normalized; however, the pace of economic growth remained modest. Therefore, in September 2012, the FOMC started an outcome-based program to purchase $40 billion of agency MBS per month.28 Agency MBS purchases were added to the ongoing Treasury-related programs as a means of putting additional downward pressure on longer-term interest rates to make broader financial conditions more accommodative and to provide further support to mortgage markets. Consistent with this objective, research suggests that the impact of MBS purchases in LSAP 3 worked primarily through the reduction of general interest rates, with both agency MBS and Treasury security purchases having a similar effect on agency MBS yields.29 While MBS purchases also lower MBS yields through the prepayment channel, a further benefit of agency MBS purchases during LSAP3 may have been in facilitating a faster pace of total long-term debt purchases which increases the impact of the duration and portfolio balance channels by increasing the expected stock of the central bank's total longer-term debt holdings. In contrast to LSAP1, LSAP3 was not found to operate through the market function channel.

Summary and the Potential Role of Agency MBS in the Future

Overall, the size and structure of the agency MBS market make it a desirable choice for conducting operations of the magnitude necessary to have a meaningful impact on financial and macroeconomic conditions in the United States. Our experience with agency MBS purchases suggests that they have been successful across both dimensions. In contrast, the Federal Reserve's experience conducting sales of agency MBS is limited to a few small value exercises.30 Central banks that are currently buying non-sovereign assets in LSAPs have a similar lack of experience with sales. There may be separate lessons to be learned from selling agency MBS.31

Current FOMC guidance states that the sale of agency MBS is not anticipated, other than potentially to eliminate residual holdings well in the future, and that in the longer run, SOMA will consist primarily of Treasury securities.32 From a practical standpoint, sales may be complicated in that they would likely be conducted through the sale of individual securities, not through the use of the TBA market, because the securities in the SOMA portfolio might be more valuable than TBA cheapest-to-deliver.33 This complication could eliminate the liquidity advantage provided by transacting in TBA.34 However, it is prudent for the Desk to be prepared for a wide variety of scenarios, including sales or the need to purchase additional agency MBS. This flexibility is particularly important given the complex nature of agency MBS and the specialized knowledge and systems required to hold and transact in the agency MBS market.

From an implementation perspective, the Federal Reserve is fortunate to have the option of implementing monetary policy in a large and liquid non-sovereign market with direct implications for existing and prospective homeowners. We have spent the past two days discussing monetary policy implementation in the long run. Given the Federal Reserve's experience in the agency MBS market over the past eight years, it is important to consider what role-if any-agency MBS transactions may have in the policy implementation toolkit of the future.

1 SOMA purchased agency debt from 1971 to 1981, so participating in one of the agency markets was not entirely new in 2008. In addition, in 2011-12 a maturity extension program extended the maturity of Treasury securities in the SOMA portfolio, although it did not expand the size of the SOMA portfolio.

2 The share is calculated as of October 12, 2016, see System Open Market Account Holdings.

3 Since the start of the year, these purchases have averaged approximately $30 billion per month. In addition to conducting these transactions, the Desk reinvests maturing proceeds from Treasury securities, though the Treasury reinvestment transactions take place at auction rather than in the primary market.

4 The accommodative monetary policy stance of the European Central Bank (ECB) rests upon three nonstandard instruments: a series of targeted long-term refinancing operations, a negative deposit facility rate, and an asset purchase program that includes private and public sector securities. The Bank of England (BoE) currently sets the Bank Rate at 25 basis points and is currently purchasing £60 billion in gilts over a 6-month period; the Asset Purchase Facility will have £435 billion in gilts when the purchase round ends in February 2017. In addition, the BoE launched an 18-month, £10 billion corporate bond purchase program in September 2016. The monetary policy framework of the Bank of Japan (BoJ) now targets both the levels of interest rates across the yield curve as well as the pace of expansion of Japan's monetary base. Its current interest rate targets include a negative deposit facility rate at -10 basis points for the short-end and a 0 percent yield target for the 10-year yield. Of note, the BoJ's three-tier deposit system exempts the majority of its system reserves from the negative rate. As for the quantity target, the BoJ pledges to maintain an expansion of "around" ¥80 trillion per year until realized inflation exceeds a 2 percent target in a sustainable manner by purchasing primarily Japanese government securities.

5 During the Bank of Japan's Quantitative Easing Program, which lasted from 2001-06, the BoJ targeted the liability side of its balance sheet by explicitly targeting the level of bank reserves. This was accomplished via repurchase agreements and purchases of Japanese government bonds with a remaining maturity of less than 5 years.

6 In a speech on January 13, 2009, then-Federal Reserve Chairman Ben Bernanke discussed the differences between "Quantitative Easing" and "Credit Easing".

7 A prominent exception is the central bank of Chile. See Section 27 of theBasic Constitutional Act of the Central Bank of Chile.

8 The Federal Reserve permits purchases of debt issued or guaranteed by the U.S. government or government agencies (such as agency debt and agency MBS).

9 This channel usually relates to signaling about short-term rates. A variant is to target longer-term interest rates by a commitment to use balance sheet expansion if necessary. The ECB's OMT program, created to purchase government bonds of euro-area countries that were granted financial assistance under certain conditions, was perceived as meaningfully reducing yields through commitment alone; no actual purchases were needed. In late September 2016, the Bank of Japan unveiled a new monetary framework called "quantitative and qualitative monetary easing with yield curve control" (QQEY). The new regime consists of two major components: (1) "yield curve control," in which the BoJ will target both short-end interest rates (with the deposit rate at -0.1 percent) and long-dated yields (around 0 percent for 10-year Japanese government bond yield), and (2) an "inflation-overshooting commitment," which amounts to maintaining monetary expansion until the 2 percent inflation target is exceeded in a stable manner.

10 See the May 10, 2010 press release for the ECB's Securities Markets Programme.

11 For example, the Federal Reserve chose to transact in the agency MBS market via external investment managers at the start of LSAP I "as a means of implementing the MBS program quickly and efficiently while at the same time minimizing operational and financial risks. - Beginning on March 2, 2010, the New York Fed began to use internal staff to execute MBS purchases." See FAQs: MBS Purchase Program.

12 In a speech at Jackson Hole on August 31, 2012, Ben Bernanke discussed a cost-benefit framework for evaluating non-traditional monetary policy tools. He noted the tools' potential impacts on market functioning, financial stability, and the Fed's ability to exit policies when needed, as well as the risk of financial losses.

13 In the Federal Open Market Committee's Rules and Authorizations, the "Guidelines for the Conduct of System Open Market Operations in Federal-Agency Issues" note that "open market operations in federal-agency issues are not designed to support individual sectors of the market or to channel funds into issues of particular agencies." These guidelines were temporarily suspended in January 2009.

14 For trading volumes, visithttp://www.sifma.org/research/statistics.aspx. For outstanding MBS, visit http://www.embs.com/secure/cgi-bin/asp/AnalyticsMenu.asp.

15 There are no other non-sovereign debt markets that are of comparable depth and liquidity.

16 For more information on the TBA market, see Vickery and Wright (2013).

17 Dollar rolls can be used to address a shortage of a specific security that is expected to be transitory. This tool is used somewhat regularly for a small portion of SOMA agency MBS purchases. Coupon swaps can address shortages of a specific security that are not expected to be resolved quickly. This tool was last used in June 2010 to facilitate the settlement of Fannie Mae 5.5 percent coupons, which stopped being originated shortly after purchase because of a sharp drop in primary mortgage rates.

18 This number includes settled and unsettled agency MBS positions. SeeH.4.1 report on October 2, 2014.

19 For example, the Bank of England's latest corporate bond purchase program targets purchases of up to £10 billion of outstanding bonds, which is less than 10 percent of the estimated outstanding eligible corporate bond market of roughly £150 billion.

20 At its highest pace, the Desk purchased more than $100 billion of agency MBS in a given month. The last time the Desk's purchases exceeded $100 billion per month was in June 2009. Since 2009, the Desk has improved its ability to execute agency MBS transactions. Beginning on March 2, 2010, the New York Fed began to use internal staff to execute MBS purchases. Beginning on April 9, 2014, the New York Fed began to increasingly conduct agency MBS purchases over FedTrade, its proprietary trading platform. Combined, these changes allow the Desk to conduct large-scale agency MBS operations with all of its counterparties.

21 This represents purchases between September 14, and October 13, 2016. On October 13, the Desk announced plans to purchase $42 billion in its reinvestment purchase operations between October 14 and November 10, 2016.

22 In addition to making asset purchases, these central banks also developed programs targeting bank lending channels, given that their capital markets are smaller relative to the banking system compared to the United States.

23 For example, 5-year Fannie Mae debt securities, which had traded, on average, 42 basis points above similar-maturity Treasury securities in 2007, traded as high as 159 basis points above Treasury securities in November 2008. Similarly, current coupon agency MBS spreads averaged 137 basis points above similar-maturity Treasury securities in 2007; that spread was as high as 288 basis points in November 2008. Both of these spread levels in November 2008 were at or near the highest spread levels in many decades of available data.

24 On November 25, 2008, the FOMC announced purchases of $100 billion in agency debt and $500 billion in agency MBS. On March 18, 2009, this program was modified to include a total of $200 billion in agency debt and $1,250 billion in agency MBS, as well as $300 billion in longer-term Treasury securities.

25 Federal Reserve Board of Governors press release, November 25, 2008.

26 See Hancock and Passmore (2011)

27 See Gagnon, Raskin, Remache and Sack (2010).

28 Note that at that time the Federal Reserve was already in the middle of the maturity extension program (MEP) which was selling shorter-maturity Treasury securities and purchasing longer-maturity Treasury securities. When the MEP expired in December, purchases of $45 billion per month in Treasury securities were added to the LSAP.

29 Hancock and Passmore (2015) estimate the impact of the purchase of a 1 percent market share of the agency MBS and U.S. Treasury markets to be 2.0 basis points and 2.5 basis points, respectively. At current market sizes, these estimates suggest that $28 billion of agency MBS purchases or $42 billion in U.S. Treasury purchases would lower agency MBS yields by 1 basis point.

30 The Desk conducts small-value exercises from time to time as a matter of prudent advance planning. They do not represent a change in the stance of monetary policy, and no inference should be drawn about the timing of any change in the stance of monetary policy in the future. These exercises include outright sales of agency MBS and coupon swaps of unsettled agency MBS holdings. The most recent coupon swap small-value exercise occurred in October 2016, and the most recent agency MBS sales small-value exercise occurred in late May-early June 2016.

31 One example of an agency MBS sales program is the U.S. Treasury's decision to liquidate its $142 billion agency MBS portfolio in 2011 through a combination of about $10 billion per month in sales and ongoing principal paydowns. The Treasury announced on March 21, 2011, that it would wind down this portfolio and sales took place between March 22, 2011, and March 13, 2012.

32 See the "Policy Normalization Principles and Plans" section of the FOMC's Rules and Authorizations, January 2016.

33 Because of improved prepayment characteristics, agency MBS that have been outstanding for a number of years are often more valuable than newly issued securities that are otherwise similar. Therefore, these securities tend to trade at a higher market price than TBA, making them unsuitable for trading through the TBA market.

34 Selling SOMA's agency MBS holdings as specified pools may have a liquidity disadvantage compared to TBA. However, this may be mitigated by the fact that a substantial portion of the SOMA portfolio is in very large securities. Owing to the use of CUSIP aggregation, a process which allows multiple securities to be combined into a single larger security, more than 25 percent of the SOMA agency MBS portfolio is in 20 individual securities.