Christopher Kent: After the boom

Speech by Mr Christopher Kent, Assistant Governor (Economic) of the Reserve Bank of Australia, at the Bloomberg Breakfast, Sydney, 13 September 2016.

Introduction

Today I want to talk about some important developments shaping the Australian economy, focusing on the sharp fall in commodity prices over the past few years.

In 2012, just after taking on my current role, some colleagues and I were looking at how the Australian economy had been adjusting to the unprecedented boom in commodity prices.1 By the time I presented that work, prices of Australia's key commodities had begun to turn down and mining investment had just peaked at a record level.2

Since then, commodity prices have fallen much further and so Australia's terms of trade (the price of our exports relative to imports) have fallen significantly. The fall was more than we, and most others, had expected. More recently, though, commodity prices have risen. And more than three-quarters of the anticipated decline in mining investment is now behind us.

The adjustment of the economy to the decline in the terms of trade and the large fall in mining investment has been a drawn out process, adversely affecting a range of industries and regions. But growth in the economy overall has been close to trend, and while the unemployment rate rose, it reached only a little above 6 per cent in 2015.3 More recently, inflation has declined.

Before talking about the period after the boom, I want to set the scene. First, I'll briefly review the boom years. Second, I'll describe what we anticipated four years ago would be likely to happen after the boom.

The Boom Years

The rapid industrialisation and urbanisation of the Chinese economy underpinned the strong rise in commodity prices from around the mid 2000s. As global demand for commodities began to outstrip supply, the prices of Australia's key commodity exports rose dramatically.

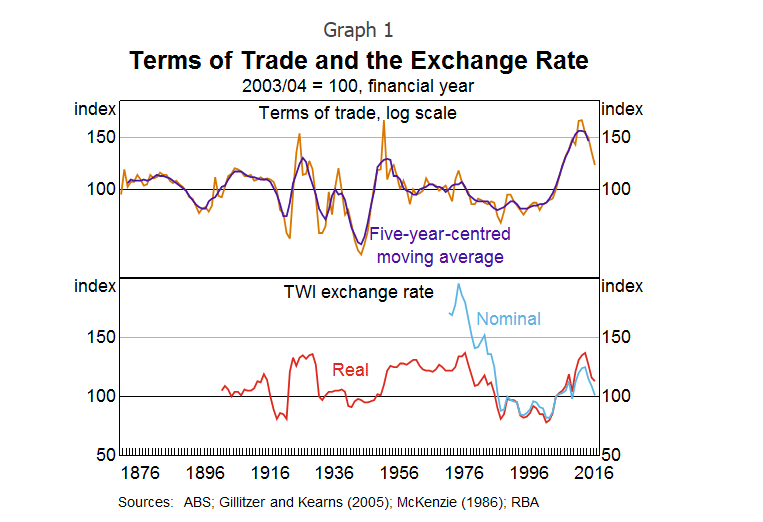

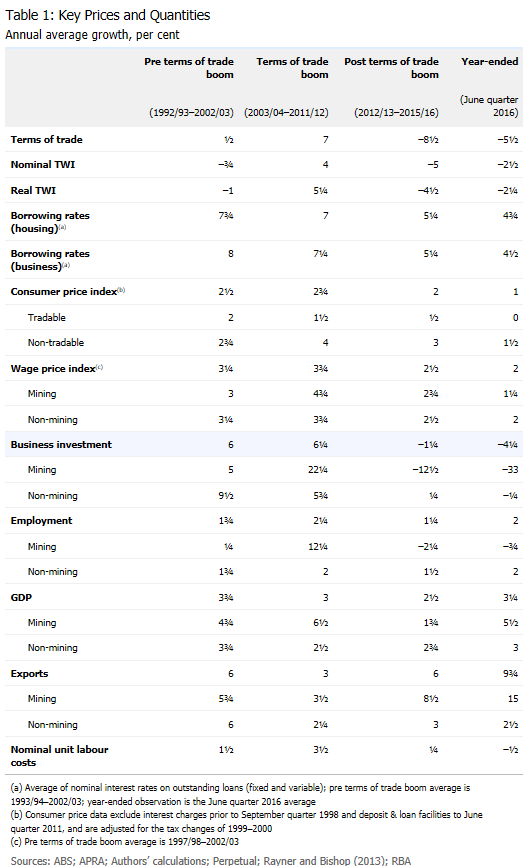

Australia's terms of trade rose by 85 per cent from the average of the early 2000s to the peak in late 2011 (Graph 1). That implied a significant boost to the real purchasing power of domestic production. Some of those gains were retained by foreign owners of mining assets, but a share of the gains stayed at home in the form of higher wages, tax revenues and profits for Australian owners of mines and of firms supporting mining activity.

The rise in Australia's terms of trade was associated with a large appreciation of the nominal exchange rate (see Table 1 in the Appendix). While this lowered the returns to Australian commodity exporters (and Australian exporters more broadly), it allowed real income gains to flow to the rest of the economy via the associated decline in the prices of imports.

The resource sector here and abroad responded to the commodity price boom by expanding productive capacity. This occurred gradually, reflecting both the unforeseen magnitude of the boom, its unexpected persistence, and the time required to plan for, approve and then complete large resource projects. In mid 2012, investment in the Australian resource sector had peaked at just under 8 per cent of GDP, compared with its average of around 2 per cent prior to the boom.

In the lead-up to that investment peak, growth in output, employment and wages in the resource sector (broadly defined to include those industries servicing it) was relatively strong. The boom in those industries led to strong economic conditions in the resource-rich states of Western Australia and Queensland.

The significant appreciation of the exchange rate provided a signal for labour and capital to be redistributed from the 'other tradable' sector towards the resource sector. As a result, the growth in investment, output, employment and wages was weak in the 'other tradable' sector.

The large nominal exchange rate appreciation also helped to contain inflationary pressures in an environment of strong growth in domestic demand and a decline in the unemployment rate to relatively low levels. Notwithstanding that assistance, overall inflation picked up to be a little above its inflation-targeting average.4 Non-tradable inflation was elevated during the boom years and growth in nominal unit labour costs was relatively strong for most of this period. In response to these inflationary pressures, the Reserve Bank raised the cash rate to be above its (inflation-targeting) average.

After the Boom – What We Had Thought Might Happen

In our previous analysis, we noted that during the commodity price boom the economy had behaved, in many respects, as theory suggested. We also discussed how the economy might adjust as the terms of trade declined.

It was clear that mining investment would fall, but at the same time, resource exports would increase as additional productive capacity came on line. However, overall demand for labour in the mining sector (and in mining-related activity) would decline because the investment phase in that sector is relatively more labour intensive than the production phase.5

With the global supply of commodities catching up to global demand, we thought that commodity prices and, therefore, Australia's terms of trade would decline (but remain higher than their pre-boom levels). That would normally be associated with a depreciation of the Australian dollar.

We anticipated that demand in the non-mining sectors would pick up and that labour and capital would be drawn back to that part of the economy. Any depreciation of the nominal exchange rate would facilitate that transition by improving the competitiveness of the 'other tradable' sector. The movement of labour would also be facilitated by some decline in wage growth, as the labour shed by companies that had undertaken the mining investment looked to move back into the non-mining sectors. In other words, we thought that the requisite real exchange rate depreciation would occur largely via the nominal exchange rate, but might also be assisted by a decline in domestic cost pressures.

These developments were expected, at least in part, to reverse some of the effects on consumer price inflation seen during the investment phase of the boom. In particular, a gradual depreciation of the exchange rate would put upward pressure on tradable inflation for a time, while a reduction in wage growth and domestic costs more generally would put downward pressure on non-tradable inflation. These opposing effects could potentially result in little net change to overall inflation, but given that inflation had been above average during the boom, it would not be surprising to see inflation below average after the boom.

But having made some predictions about the direction of some key variables, we also noted the considerable degree of uncertainty, including that related to the global economic outlook.

After the Boom – What Actually Happened?

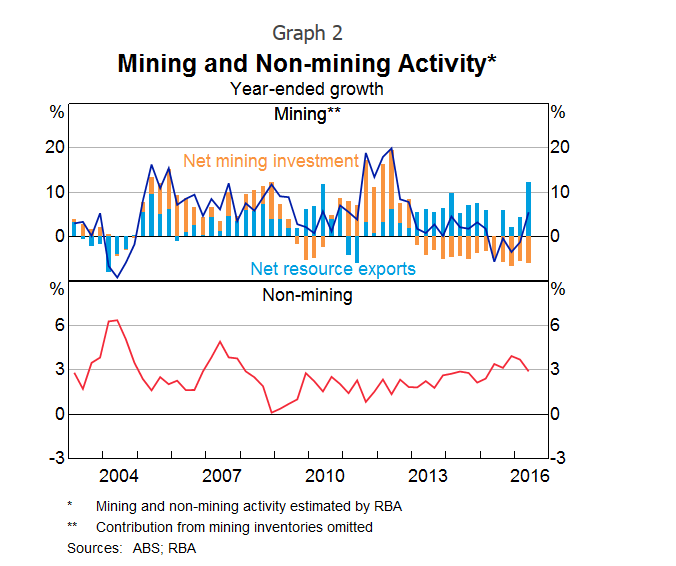

Many of our predictions have been borne out. Mining investment declined significantly and resource exports grew strongly. Mining investment has further to fall, although the largest drag on GDP growth from that source is likely to have come and gone over the financial year just passed. The decline in mining investment from 2012 led to lower growth in overall mining activity (mining investment plus resource exports; Graph 2). More recently, growth of mining activity has picked up. Mining activity is set to continue to grow for a time as the drag from mining investment wanes and production of liquefied natural gas continues to ramp up.

As had been anticipated, mining-related employment has contracted and wage growth in those industries has declined to be noticeably below that of other sectors.6

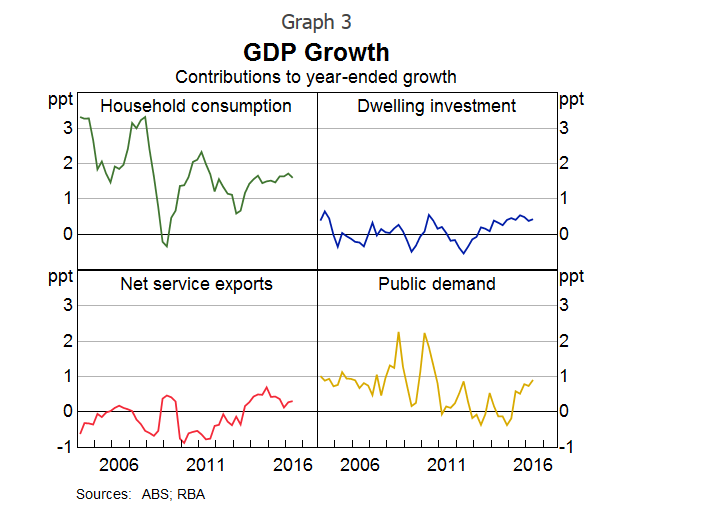

In the non-mining sector, growth in activity and employment (more recently) have picked up. The reduction in interest rates over the past few years has been assisting in rebalancing activity towards the non-mining economy, which is currently growing at around its long-run average rate (Graph 3). The depreciation of the nominal exchange rate since early 2013 has also supported activity in the 'other tradable' sector. Net service exports have made a noticeable contribution to GDP growth over the past few years, with tourism, education and business service exports all expanding.

Overall, inflation has declined, driven by lower inflation of non-tradable items and consistent with a significant decline in the growth of labour costs. At the same time, inflation of tradable items has increased following the exchange rate depreciation.

In short, the patterns of behaviour of these key macroeconomic variables have been quite consistent with what we had initially thought might happen. However, the magnitudes and speed of some of the adjustments have surprised us. In part, this reflects external developments, most notably:

- the larger-than-expected decline in commodity prices and the terms of trade; and

- the extent and persistence of low growth and low inflation in much of the world and the associated easy monetary policies of the major central banks.

Despite these challenges, the Australian economy has displayed a degree of flexibility that has helped the process of adjustment.

Commodity Prices and the Terms of Trade

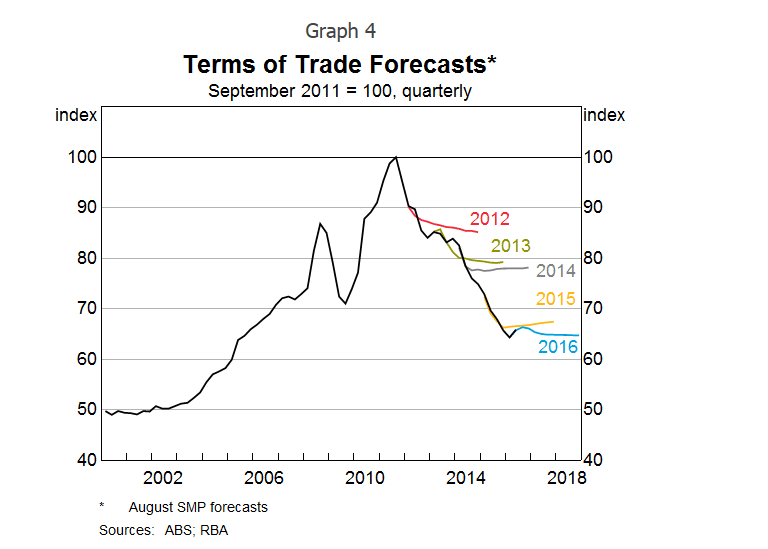

Australia's terms of trade declined by more than had been expected a few years ago (Graph 4). Around the time of our previous analysis, we were forecasting a further decline in the terms of trade over the coming years. But then from 2012 to 2015, we repeatedly revised down our forecasts.

The larger-than-expected decline in Australia's terms of trade reflected both demand- and supply-side factors. Growth in the demand for commodities from Asia, and China in particular, declined noticeably. In large part, this was in response to excess capacity in manufacturing as well as a decline in real estate investment in China. Among other things, this has seen the growth in global steel production stall, and hence lower growth in the demand for iron ore and coking coal.

On the supply side, commodity producers have been able to reduce their costs by more than initially thought possible, and some higher-cost suppliers sustained their production levels for longer than anticipated.7

The larger-than-expected decline in the terms of trade has weighed on growth in economic activity, employment, profits, wages and fiscal revenues, as well as on inflation. The effect has been largest in the mining sector and the key mining states, but it has been evident across the economy more broadly.

The Exchange Rate

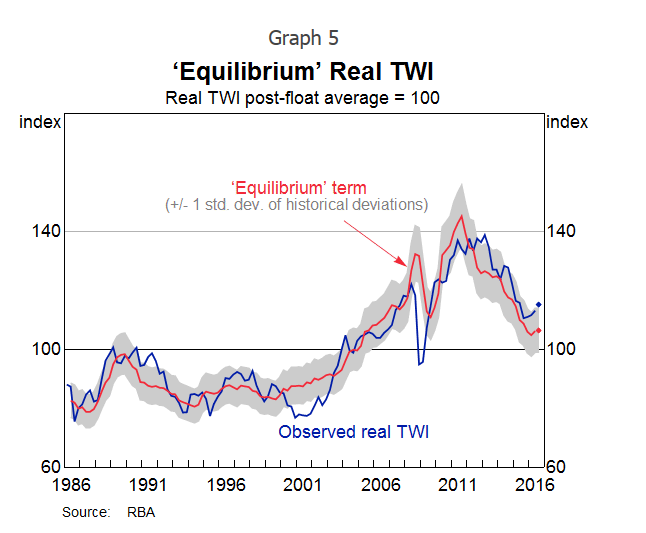

The depreciation of the Australian dollar over recent years has improved Australia's competiveness and thereby supported production in the tradable sector. However, the depreciation didn't start in earnest until 18 months after the terms of trade had peaked. And while it is hard to be precise, our modelling suggests that the exchange rate (the real trade weighted index, or real TWI) has not depreciated by quite as much as might have been expected in response to the actual decline in the terms of trade (and the reductions in domestic interest rates) (Graph 5). At least in part, this reflects lower-than-expected global growth and inflation, which has led to a prolonged period of very low interest rates and unconventional monetary policies in the major economies.8

Real GDP

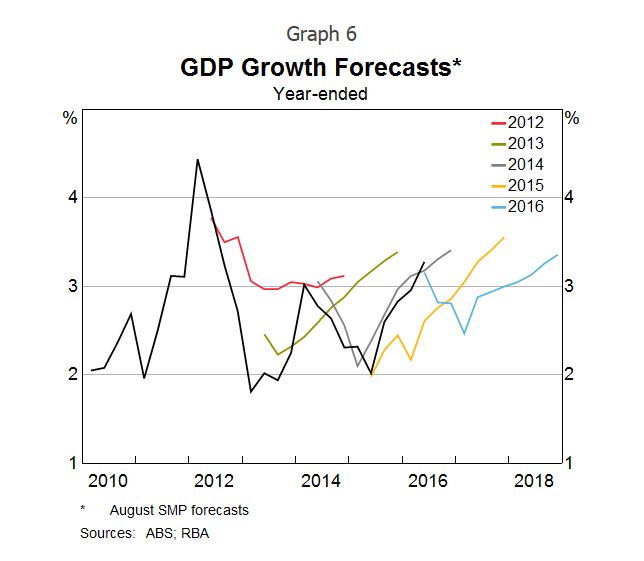

Australia's real GDP did not increase by quite as much as we had expected back in late 2012. The GDP forecast in the August 2012 Statement on Monetary Policy was a bit over 1 percentage point stronger than what came to pass over the year to March 2013 (Graph 6). We subsequently revised down our forecasts. In the intervening years growth was sometimes a little above our forecasts, sometimes below. GDP growth more recently has been a bit stronger than we'd expected a year ago.

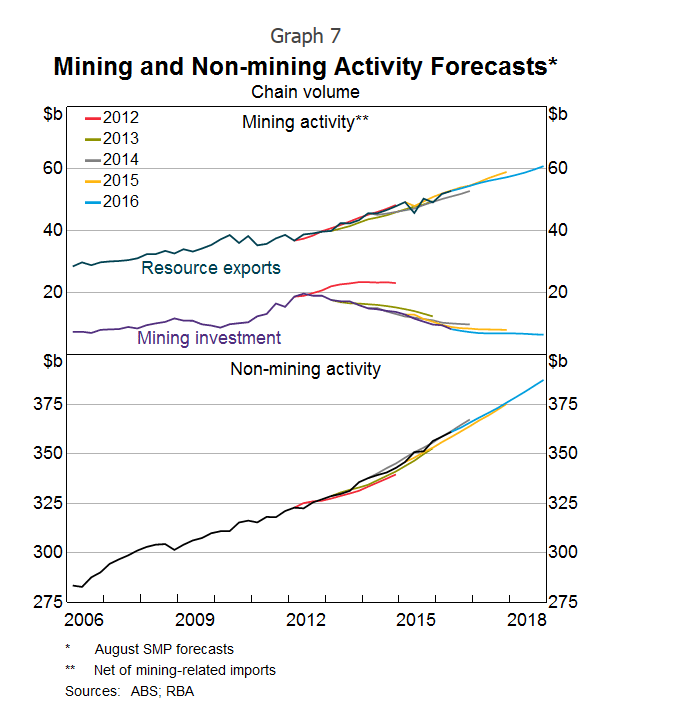

Much of the early forecast miss for GDP growth owed to mining investment. In late 2012, we had forecast that mining investment would be likely to rise a little further and stay elevated for a time (Graph 7). It soon became apparent, however, that mining companies had revised their earlier plans in response to lower-than-expected commodity prices. We revised down our forecasts accordingly. Since 2013, our liaison efforts have been instrumental in generating quite accurate forecasts for mining investment. The forecasts for resource exports have also been reasonably accurate over recent years.

Since 2012, growth in real non-mining activity has picked up gradually and has generally been a little stronger than was expected, supported by lower interest rates and the depreciation of the exchange rate.9

Nominal GDP

The weaker than earlier expected outcome for real GDP growth was not particularly large in comparison with the usual range of forecast uncertainty, and as I noted, real GDP growth over the past year has actually been a bit stronger than earlier anticipated. In contrast, the larger-than-expected decline in the terms of trade over the past few years has meant that nominal outcomes have been significantly weaker than earlier forecast. From 2013 to 2015, nominal GDP increased by around 8 per cent, which was half the initial forecast of 17 per cent. That has had important implications for growth in wages, costs and prices.

Labour and Labour Costs

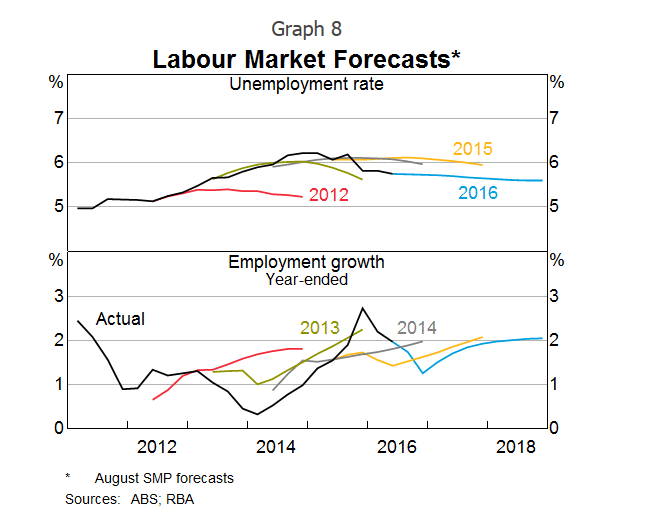

Given that real GDP growth was initially a bit weaker than expected, it's not surprising that employment growth was less than forecast and the unemployment rate higher than expected (Graph 8). More recently, however, the unemployment rate has declined by a bit more than had been anticipated.10

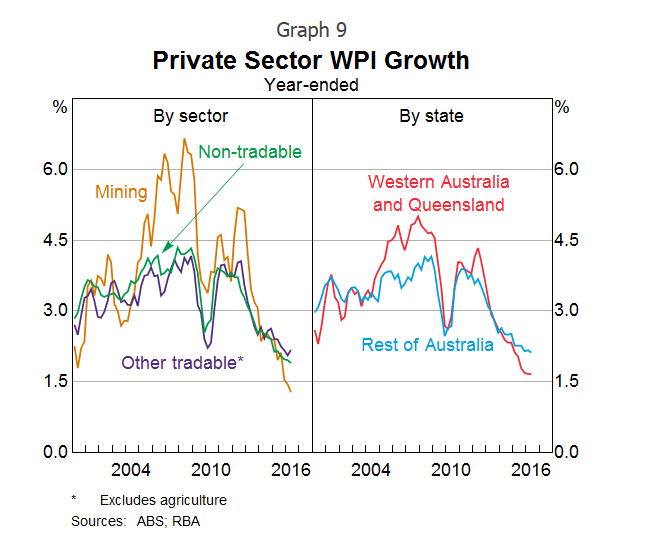

Shortly after the fall in the terms of trade, wage growth declined significantly across every industry and all states. It is currently lowest in Western Australia and Queensland, and in industries exposed to the end of the mining investment boom (Graph 9). Some decline in wage growth in response to the decline in mining investment and the terms of trade was to be expected, but the decline in wage growth has been greater than implied by historical relationships with the unemployment rate. That could reflect several factors:11

- Workers who had been engaged in mining-related activities moved to lower paid jobs outside the resource sector. This compositional effect contributed to lower growth in average earnings per hour than in the wage price index (at least until very recently).12

- Compared with earlier periods of high unemployment rates (e.g. in the 1980s and 1990s), increased labour market flexibility may have provided firms with greater scope to adjust wages in response to declines in the growth of their nominal revenues (which, in turn, followed from the fall in the terms of trade).

- Workers may be less certain of their employment prospects, possibly because of rising competitive pressures in a more globalised world, leading them to be more willing to accept lower wage outcomes in exchange for more job security.

- The decline in inflation and inflation expectations over recent years may also have influenced wage negotiations.

It is important to note that low growth in labour costs has, in many respects, helped the economy adjust to the lower terms of trade. In addition to the nominal exchange rate depreciation, low growth in labour costs is helping to improve Australia's international competitiveness and has encouraged more employment growth than would otherwise have occurred. More recently, wage growth has shown signs of stabilisation, with growth in the private sector wage price index unchanged for the past six quarters, while a broader measure of wage pressures, the growth in average earnings per hour, has picked up of late.

Other Costs and Margins

Spare capacity in a range of product markets also led to downward pressure on other costs and margins along the supply chain. This sort of pressure is particularly evident in low inflation of final retail prices for items sold in supermarkets and for many consumer durable goods.13

Inflation

Lower growth in labour and other costs, as well as lower margins, have contributed to lower-than-expected outcomes for inflation of both non-tradable and tradable items. Compared with earlier forecasts for 2013–2015, inflation in underlying terms has only been a little below expectations (7.1 per cent versus 7.8 per cent cumulated over that period). However, inflation has also been lower than expected more recently; our forecasts for 2016 have been revised down from a bit above 2 per cent to about 1½ per cent between February and August of this year.

Interest Rates

The initial misses on GDP and unemployment, and more recently on wage growth and inflation, owed significantly to the effects of the larger-than-expected decline in the terms of trade on the mining sector and the economy more broadly.

In response to the evolving outlook, the Reserve Bank Board has reduced the cash rate to low levels to improve the prospects for sustainable growth in the economy, with inflation rising to be consistent with the medium-term target.

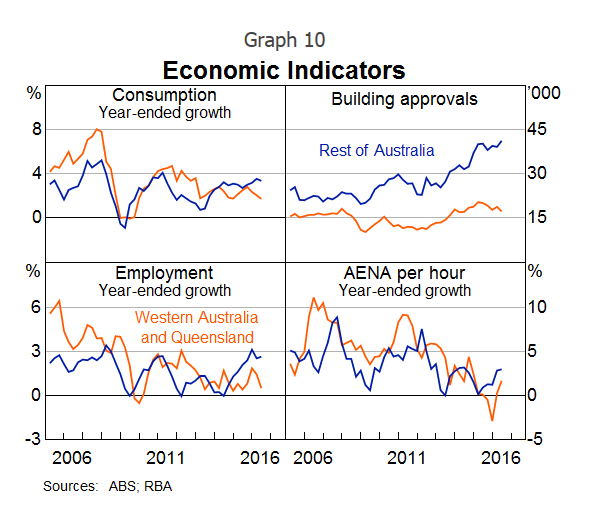

The low level of interest rates and the depreciation of the exchange rate have underpinned a rise in the growth of non-mining activity, which is currently running around its long-run average. Western Australia and Queensland have been most directly affected by the fall in commodity prices and mining investment, and so economic conditions there are still relatively weak (Graph 10). However, New South Wales and Victoria have been less affected by those pressures and so low interest rates and the lower exchange rate have led to an improvement in economic conditions in those states.

Conclusion

The pattern of adjustment of the Australian economy to the decline in the terms of trade and mining investment is generally consistent with what we had anticipated. However, the decline in the terms of trade was larger than expected. In response, there has been significant adjustment in a range of market 'prices' – including wages and the nominal exchange rate, although the exchange rate has depreciated a little less than otherwise given global developments. Monetary policy has also responded, with interest rates reduced to low levels. So while mining investment and nominal GDP growth have both been weaker than the forecasts of a few years ago and, more recently, inflation has been a bit weaker than expected, growth in the non-mining economy has picked up and been a bit better than earlier anticipated. Indeed, of late, real GDP growth has been a bit stronger and the unemployment rate a little lower than earlier forecast.

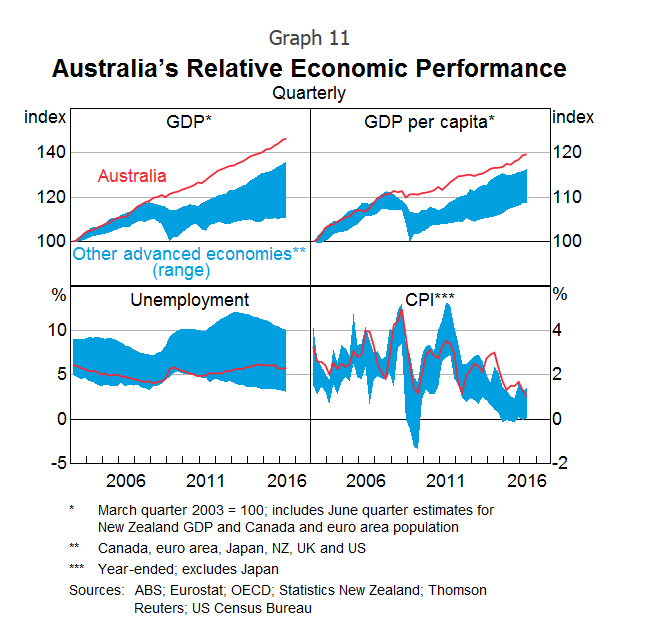

In many respects, the adjustment to the decline in mining investment and the terms of trade has proceeded relatively smoothly. The Australian economy has performed well compared to other advanced economies (Graph 11). Moreover, the drag on growth from declining mining investment is now waning and the terms of trade are forecast to remain around their current levels.

Of course our forecasts are subject to the usual range of uncertainty. But, given that commodity prices have increased substantially over the course of this year, some stability in the terms of trade from here on seems more plausible than it has for some time. Developments in China are likely to continue to have an important influence on commodity prices, given China's role as both a major producer and consumer of many commodities. For this reason the outlook for the Chinese economy is a key source of uncertainty for the Australian economy.

If commodity prices were to stabilise around current levels, that would be a marked change from recent years. Also, the end of the fall in mining investment is coming into view. The abatement of those two substantial headwinds suggests that there is a reasonable prospect of sustaining growth in economic activity, which would support a further gradual decline in the unemployment rate. There is also a good prospect that the growth in wages and the rate of inflation will gradually lift over the period ahead. That's what's implied by our central forecasts.

Thank you. I'd be happy to take a few questions.

Appendix

1 This was published in early 2013. See Plumb M, C Kent and J Bishop (2013), 'Implications for the Australian Economy of Strong Growth in Asia', RBA Research Discussion Paper No 2013–03.

2 Speech delivered to the joint IMF/Treasury/RBA conference on 'Structural Change and the Rise of Asia', Canberra, 2012. For other work done on this topic by RBA staff, see: Jääskelä J and P Smith (2013), 'Terms of Trade Shocks: What Are They and What Do They Do?', Economic Record 89, pp 145–159; Downes P, K Hanslow and P Tulip (2014), 'The Effect of the Mining Boom on the Australian Economy', RBA Research Discussion Paper No 2014–08; Kulish M and D Rees (2015), 'Unprecedented Changes in the Terms of Trade', RBA Research Discussion Paper No 2015–11; and Manalo, J, D Perera and D Rees (2015), 'Exchange Rate Movements and the Australian Economy', Economic Modelling (47), pp 53–62.

3 The economic adjustment this time around stands in contrast to previous terms of trade booms in Australia, which – despite being smaller than the recent boom – tended to end in sharp contractions in economic activity and large increases in unemployment. See: Battellino R (2010), 'Mining Booms and the Australian Economy', RBA Bulletin, March, pp 63–69; and Atkin T, M Caputo, T Robinson and H Wang (2014), 'Macroeconomic Consequences of Terms of Trade Episodes, Past and Present', RBA Research Discussion Paper No 2014–01.

4 Inflation peaked at 5 per cent in late 2008, but declined as economic conditions moderated during the global financial crisis. Growth in nominal unit labour costs also eased during the financial crisis, but rebounded to a peak of around 7 per cent in year-ended terms in early 2011.

5 Even so, labour demand in the resource sector would still remain somewhat higher than it was prior to the terms of trade boom, given the operational needs associated with producing more output.

6 Nevertheless, as anticipated, employment in the resource sector remains higher than pre-boom levels as production of resource commodities has increased.

7 For a discussion of the costs of producing iron ore, see: <http://www.rba.gov.au/publications/smp/boxes/2015/feb/a.pdf>. The decline in Australian producers' costs would have supported their profitability, but the decline in the costs of offshore producers would have allowed them to keep producing more than otherwise, and this extra supply would have weighed on commodity prices and, hence, the profits of Australian resource producers.

8 See Hambur J, L Cockerell, C Potter, P Smith and M Wright (2015), 'Modelling the Australian Dollar', RBA Research Discussion Paper 2015–12.

9 The improved growth in non-mining activity has occurred despite non-mining business investment remaining subdued. Weakness in non-mining business investment has been most evident in Western Australia and, to a lesser extent, Queensland, where the decline in mining investment and commodity prices have contributed to weak conditions in those states more broadly. More recently, non-mining investment appears to have increased in New South Wales and Victoria, where economic conditions have been improving.

10 There has also been some decline in population growth, most notably in Western Australia.

11 See Jacobs D and A Rush (2015), 'Why Is Wage Growth So Low?', RBA Bulletin, June, pp 9–18.

12 For a discussion of the differences between these measures, see: <http://www.rba.gov.au/publications/smp/2016/aug/price-and-wage-developments.html>.

13 See Ballantyne A and S Langcake (2016), 'Why Has Retail Inflation Been So Low?', RBA Bulletin, June, pp 9–17.