Boom and bust of the recent silver and gold rush: the role of leveraged retail investors

Box extracted from Overview chapter "Markets recalibrate amid shifting currents"

After a prolonged rally through 2025 and into early 2026, prices of precious metals such as gold and silver reversed abruptly in late January and February 2026. Retail-driven exuberance, increasingly channelled through exchange-traded funds (ETFs), set the stage for outsize moves, continuing the trend from 2025. The daily rebalancing of leveraged ETFs and margin-triggered liquidations amplified the swings, particularly in silver.

The daily rebalancing of leveraged ETFs and margin-triggered liquidations amplified the swings, particularly in silver.

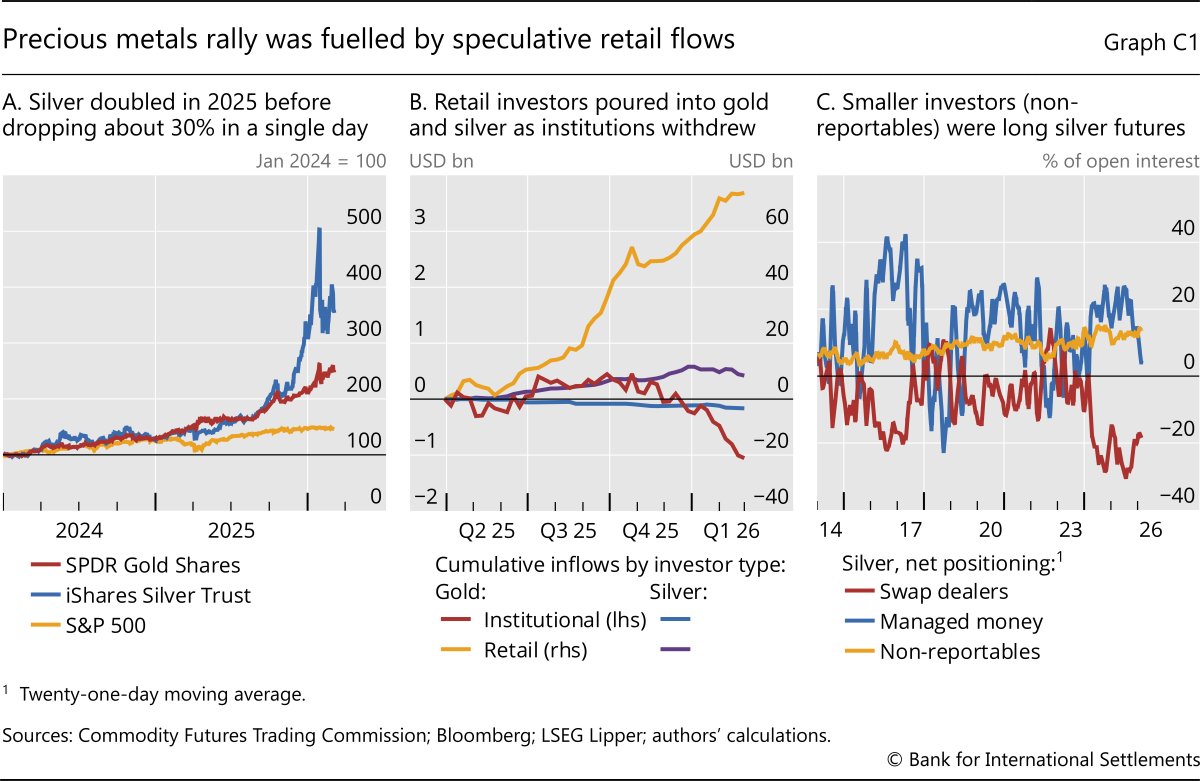

Following substantial gains in 2025 and a further surge in early January 2026, gold and particularly silver prices plunged in late January (Graph C1.A). After doubling over 2025 and rising by over 50% in January 2026, the silver price fell by about 30% in a single day in late January (blue line). Gold broadly followed a similar but less extreme pattern (red line). The precious metals crash seemingly coincided with shifts in expectations about the US dollar and the path of monetary policy, but was hard to square with broader changes in fundamentals. The abrupt price drop and the spike in precious metals' volatility point to the role of retail flows, and amplification of price moves due to forced sales by leveraged ETFs, trend-following investors such as commodity trading advisers (CTAs) and margin dynamics.

Fund flow data indicate that retail investors were the main source of inflows into silver and gold funds in the run-up to the episode. In contrast, institutional investors maintained stable positions or even trimmed exposure (Graph C1.B). Moreover, futures positioning reveals long leveraged exposure among smaller speculative participants. "Non-reportables" – typically smaller investors – were long silver futures heading into the correction. As prices fell sharply and exchanges raised margin requirements, these investors probably had to reduce positions quickly. "Managed money" – including CTAs and institutional investors – also cut long positions, while dealers stepped in to provide liquidity by cutting short positions (Graph C1.C).

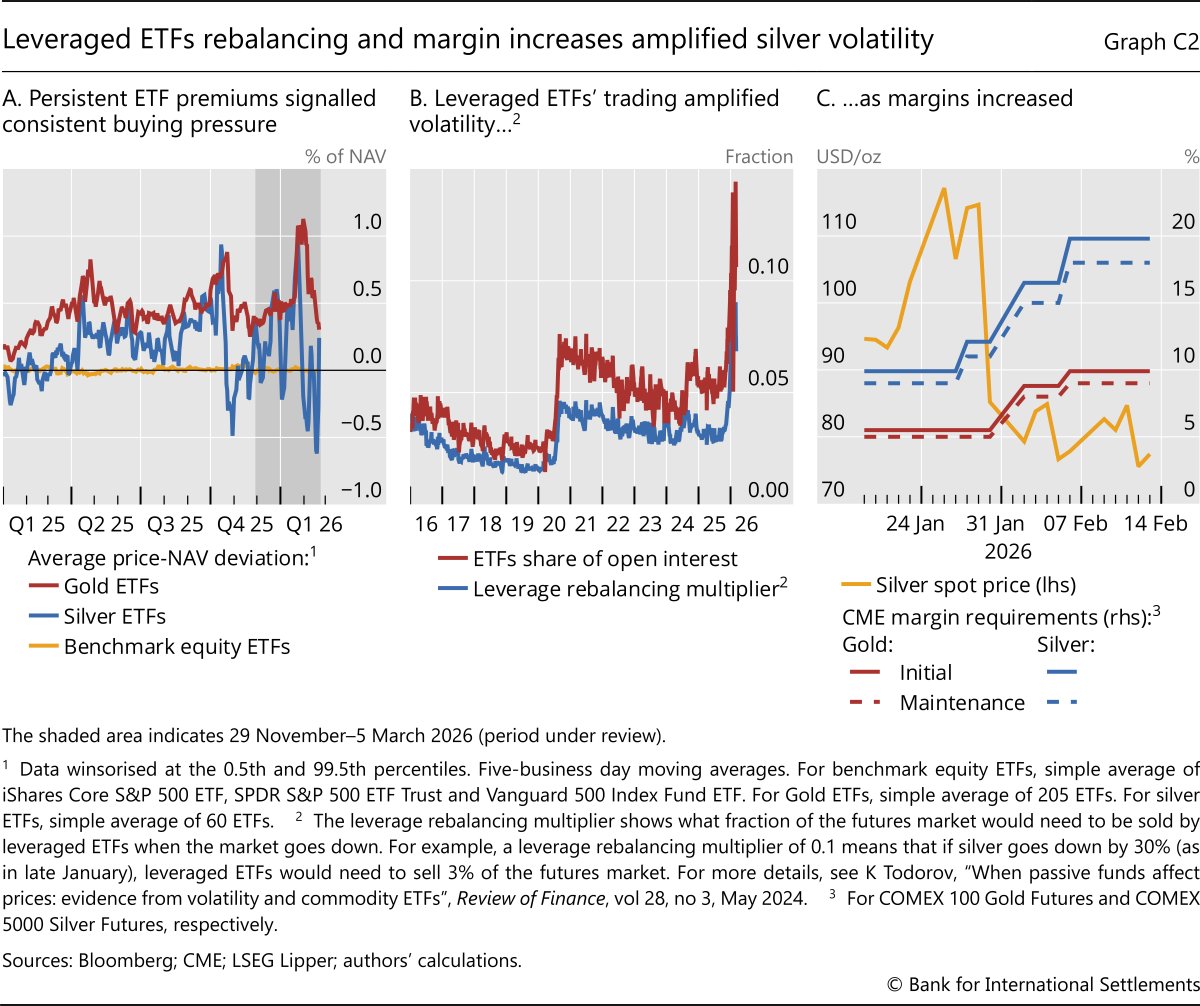

For some time, retail investors have found it attractive to use ETFs to obtain precious metal exposure. Sustained premia of gold and silver ETFs over their net asset value (NAV) signalled strong, one-sided buying pressure that outpaced primary market arbitrage (Graph C2.A). Such persistent premia arise when demand for ETF shares exceeds the capacity of authorised participants to create new shares and deliver physical metal to bring market prices down to NAV. As prices reversed in late January, these premia compressed rapidly, and for silver turned into pronounced discounts, consistent with one-sided selling pressure and a sharp turn in flows.

Leveraged silver ETFs contributed to the turmoil because of their amplification mechanics. To maintain fixed daily leverage, these funds rebalance each day. When prices rise, they buy the underlying asset (often via silver futures) to restore target leverage and when prices fall, they sell the underlying asset. This predictable, momentum-like trading creates feedback loops that reinforce prevailing trends and can distort prices.

The footprint of leveraged ETFs' destabilising trading appears to have grown amid the retail-driven exuberance in precious metal markets. The leverage rebalancing multiplier, a summary measure of the market impact of leveraged ETFs' daily rebalancing flows, doubled over the course of 2025 (Graph C2.B, blue line). The share of ETFs in the market followed similar dynamics (red line). This indicates that leveraged ETF activity became a larger part of the market and intensified price trends.

Margin-triggered liquidations further amplified the sell-off. Rapid price declines increased variation margins on futures positions, and several exchanges tightened initial margin requirements during the episode (Graph C2.C). The resulting funding pressures forced deleveraging among participants most exposed to the downdraft, akin to past stress episodes. The liquidations of investors' positions, alongside systematic selling from leveraged ETF rebalancing into the decline, probably added to downward pressure, creating a self-reinforcing loop of lower prices and further margin calls.

The liquidations of investors' positions, alongside systematic selling from leveraged ETF rebalancing into the decline, probably added to downward pressure, creating a self-reinforcing loop of lower prices and further margin calls.

The views expressed here are those of the authors and not necessarily those of the BIS or its member central banks. G Cornelli, M Lombardi, and A Schrimpf, "Bubble conditions in US equities and gold?", BIS Quarterly Review, December 2025. K Todorov, "When passive funds affect prices: evidence from volatility and commodity ETFs", Review of Finance, vol 28, no 3, May 2024. BIS, "Carry off, carry on", BIS Quarterly Review, September 2024.