Financing the AI infrastructure boom: on- and off-balance sheet borrowing

Box extracted from Overview chapter "Markets recalibrate amid shifting currents"

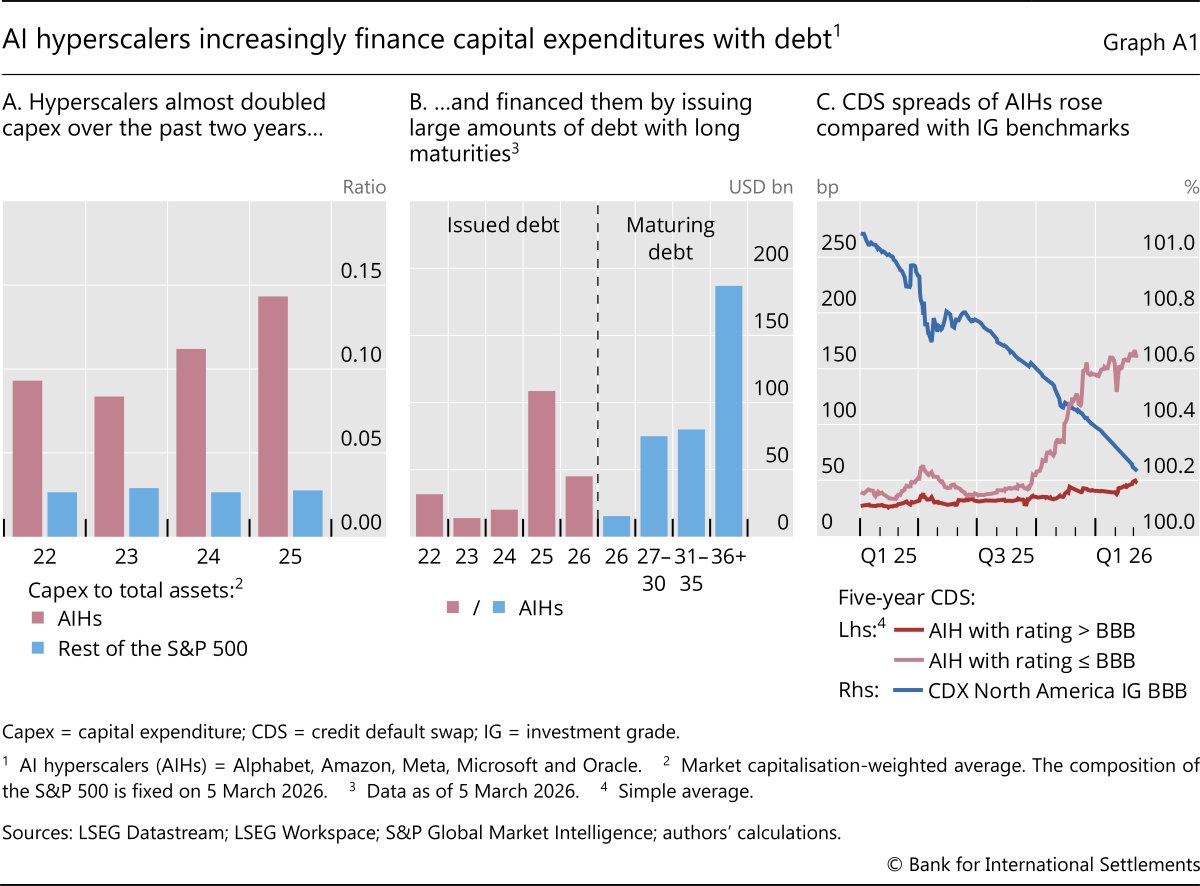

Investment in artificial intelligence (AI) infrastructure, particularly data centres, has risen rapidly and now accounts for a substantial share of investment in advanced economies. Against this backdrop, big US tech firms – "hyperscalers" – have accelerated their capital expenditures (capex) (Graph A1.A). But, as these expenditures have grown significantly beyond their usual investments, a rising share of spending is funded through borrowing.

– have accelerated their capital expenditures (capex) (Graph A1.A). But, as these expenditures have grown significantly beyond their usual investments, a rising share of spending is funded through borrowing.

Corporate bond markets have been hyperscalers' primary source of financing. Their gross issuance increased markedly, topping $100 billion in 2025 (Graph A1.B). Most issuance was longterm, with maturities over five years, locking in funding for multi-year build-outs. However, credit default swap (CDS) spreads rose (Graph A1.C), especially for hyperscalers with lower credit ratings, reflecting both the volume of supply and uncertainties around the projects' payoffs.

Alongside traditional bonds, hyperscalers have turned to off-balance sheet arrangements to finance infrastructure expansions, often in partnership with private credit firms. A common structure involves a dedicated vehicle – often a joint venture or special purpose entity – that acquires or develops data centre assets. The vehicle is capitalised with equity from a consortium of sponsors and raises debt through private placements. The hyperscaler typically holds a minority stake, commits to long-term operating leases or capacity offtake agreements (longterm commitments to purchase or reserve power and compute capacity), and may provide various guarantees. Economically, this substitutes upfront capex with multi-year operating expenses while keeping most of the associated debt off the hyperscaler's balance sheet. The debt is serviced by lease cash flows and is held by private credit funds and other institutional investors, sometimes with investment grade features supported by asset backing and contractual guarantees from hyperscalers with investment grade credit ratings.

These arrangements amount to "shadow borrowing": obligations that are economically akin to debt but largely reside outside corporate balance sheets. By channelling sizeable private credit into AI infrastructure, these structures strengthen links between hyperscalers and non-bank investors such as private credit vehicles and insurers. Banks support the vehicles with funding lines, potentially creating new shock transmission channels – eg via refinancing pressures at the vehicle level, procyclical shifts in private credit appetite or the activation of guarantees.

The views expressed here are those of the authors and not necessarily those of the BIS or its member central banks. These include firms such as Amazon, Alphabet, Microsoft, Meta and Oracle. See also I Aldasoro, S Doerr and D Rees, "Financing the AI boom: from cash flows to debt", BIS Bulletin, no 120, 2026.