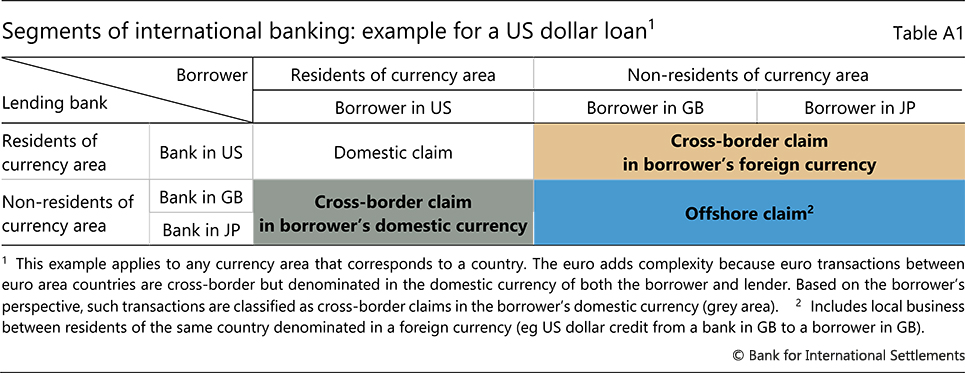

What constitutes international banking

International banking comprises cross-border business in any currency and local business in foreign currencies. It consists of three market segments, which are distinguished principally by whether a transaction is denominated in a currency that is foreign to the borrower, the lender or both of them (Table A1, coloured areas).

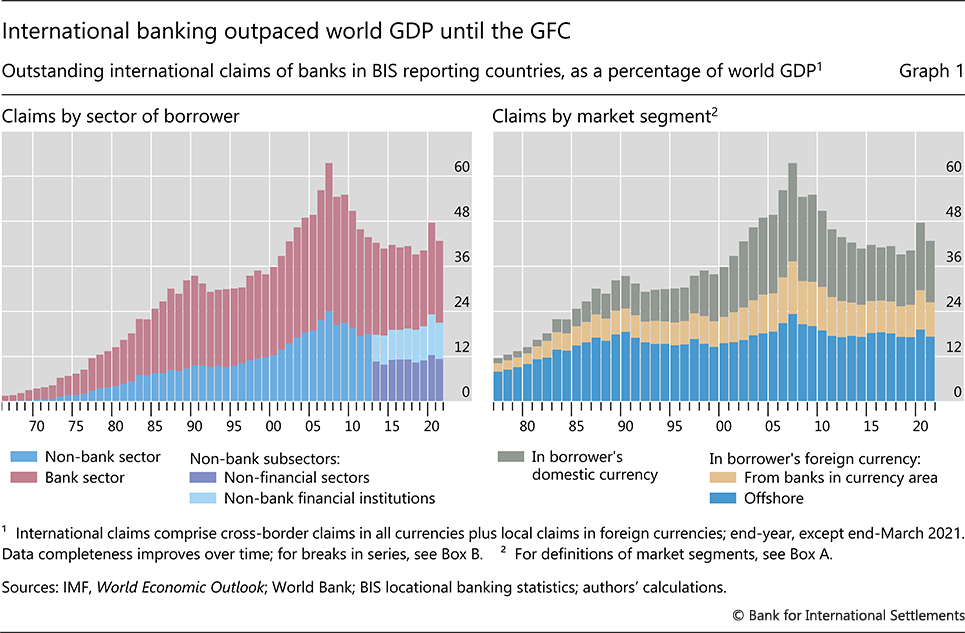

The first two segments constitute traditional international banking, where the currency is foreign to either the lender or the borrower but not both. One segment is cross-border lending by residents of a given jurisdiction in their domestic currency (Graph 1, right-hand panel, brown area). For example, a bank in New York might lend US dollars to a borrower in London or Tokyo (Table A1, brown area). The other segment is also cross-border but involves residents borrowing in their domestic currency from a bank abroad (Graph 1, right-hand panel, grey area). For example, a company in New York might borrow US dollars from a bank in London or Tokyo (Table A1, grey area). Both of these examples involve a counterparty that is a non-US resident and thus transacts in a foreign currency. For ease of interpretation, in this feature we define the currency from the borrower's perspective and thus refer to the first transaction as foreign currency (because the borrower is a non-US resident) and the second as domestic currency (because the borrower is a US resident).

The third segment is the offshore market, which was historically known as the "eurocurrency" market because it developed first in Europe (Graph 1, right-hand panel, blue area). The defining characteristic of this market is that business is denominated in a currency that is foreign to both parties. For example, a bank in Tokyo might lend US dollars to a bank in London, which might then onlend the dollars to another borrower in London (Table A1, blue area). While the first is a cross-border transaction and the second a local one, both are denominated in a currency that is foreign to the parties involved because all are non-US residents. Likewise, euro-denominated transactions between parties outside the euro area, and yen ones between parties outside Japan, are offshore.

The three segments are closely linked. Banks inside a currency area with surplus funding can channel it to the offshore market, and vice versa. Each segment is represented on major banks' balance sheets. For instance, reserves held by banks at the central bank (a domestic claim) can be used to settle domestic, international or offshore claims in the relevant currency (Aliber (1980)).

The views expressed in this article are those of the authors and do not necessarily reflect those of the Bank for International Settlements. This contrasts with the usual perspective in the BIS international banking statistics, where the currency is defined as domestic or foreign depending on the residence of the reporting bank.

{kind=link}