EME government debt: cause for concern?

In emerging market economies (EMEs), the Covid-19 pandemic increased governments' funding needs at the very moment that investor appetite waned. In March, local currency bond yields rose rapidly and international investors withdrew on a massive scale. While government debt markets have since started to stabilise, the economic crisis triggered by the pandemic has brought into sharp focus two international dimensions of EME governments' funding risk: their vulnerability to currency depreciations and their dependence on non-resident portfolio investors.

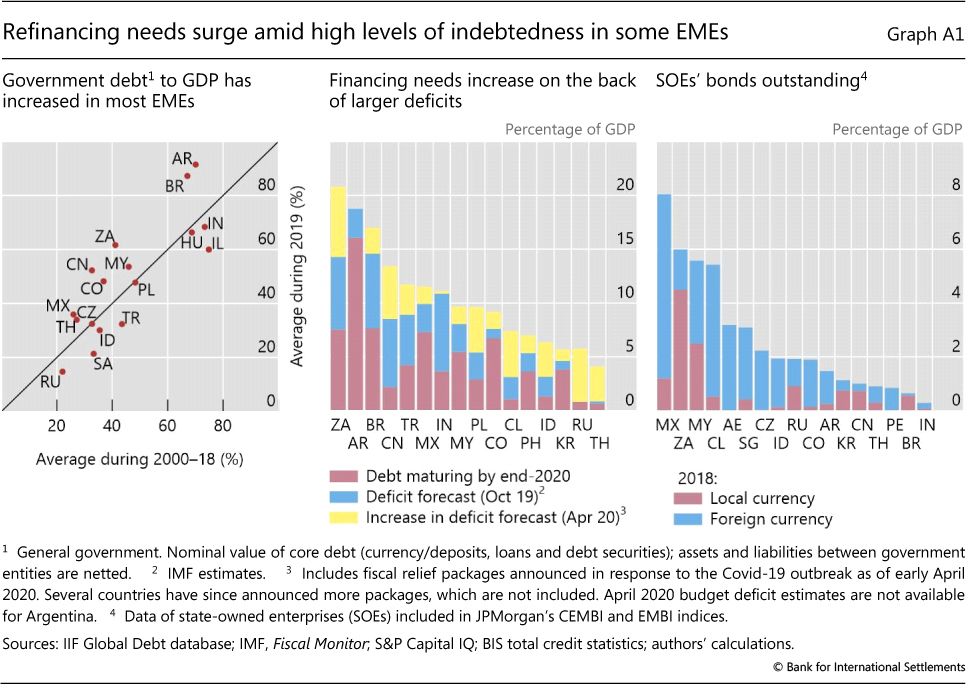

Even before the crisis, government debt relative to GDP had risen in many EMEs over the previous two decades (Graph A1, left-hand panel). Some EMEs now have a stock of government debt to GDP as high as 70%. However, as interest rates fell over the same period, the debt service burden of those economies rose by less.

Owing to the crisis, financing needs have increased for most EMEs. Several governments already had large annual refinancing needs in 2020 (Graph A1, centre panel). Fiscal expenditure is set to increase in all EMEs because of relief packages aimed at alleviating the economic fallout of virus containment measures. At the same time, revenues are expected to fall as economic activity declines. Commodity-producing EMEs are additionally hit by the decline in oil and other commodity prices in 2020. Across EMEs, the overall refinancing need in 2020 is expected to be around 10% of GDP on average, and up to 20% for some especially hard-hit countries (centre panel).

Across EMEs, the overall refinancing need in 2020 is expected to be around 10% of GDP on average, and up to 20% for some especially hard-hit countries (centre panel).

The crisis may also crystallise some contingent liabilities for governments, particularly in relation to state-owned enterprises (SOEs). In some EMEs, SOEs outside the general government sector have high debt levels (Graph A1, right-hand panel), including liabilities incurred by their affiliates abroad. The weak profitability of some of these SOEs makes their liabilities more likely to fall on government balance sheets. Indeed, already prior to the crisis, direct transfers to SOEs were weighing on budgets in some countries (eg Mexico and South Africa).

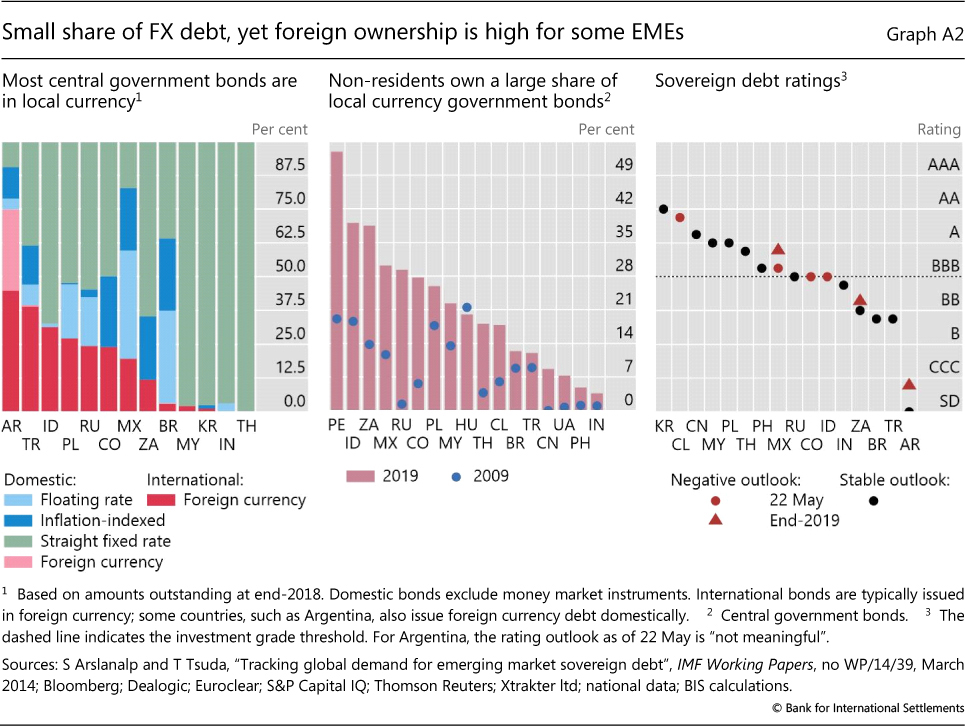

Against this backdrop, two aspects of the external funding structure of government debt are of potential concern. The first concern is the currency composition of EME debt. Most EME governments have reduced their exposure to currency devaluations by developing their local currency government bond (LCGB) markets. At end-2019, around 80% of central government bonds were denominated in local currency, mostly at fixed rates (Graph A2, left-hand panel). However, a few EMEs still have a substantial share of their bonds denominated in foreign currencies and thus remain vulnerable to valuation changes linked to exchange rate depreciation. In addition, SOEs' liabilities can be sensitive to currency devaluations when they have substantial amounts of foreign currency-denominated debt and face a decline in their foreign currency incomes. For example, about 90% of the debt of the oil-producing SOEs of Brazil, Colombia and Mexico is denominated in US dollars. The collapse in commodity prices is now weighing on the financial position of SOEs that have relied on income from commodity sales as a "natural hedge" to service their foreign currency debt.

At end-2019, around 80% of central government bonds were denominated in local currency, mostly at fixed rates (Graph A2, left-hand panel). However, a few EMEs still have a substantial share of their bonds denominated in foreign currencies and thus remain vulnerable to valuation changes linked to exchange rate depreciation. In addition, SOEs' liabilities can be sensitive to currency devaluations when they have substantial amounts of foreign currency-denominated debt and face a decline in their foreign currency incomes. For example, about 90% of the debt of the oil-producing SOEs of Brazil, Colombia and Mexico is denominated in US dollars. The collapse in commodity prices is now weighing on the financial position of SOEs that have relied on income from commodity sales as a "natural hedge" to service their foreign currency debt.

The second potential concern is the challenges posed by the participation of foreign investors in LCGB markets. As of mid-2019, non-residents held about 20% of the LCGBs (Graph A2, centre panel), up from 10% a decade ago. Increased foreign participation has many advantages when the domestic institutional investor base is less developed. It provides funding and adds to the liquidity of domestic government bond markets. It has also helped EMEs to reduce short-term foreign currency borrowing, a key driver of past crises. Yet foreign portfolio investment does not fully insulate EMEs from funding strains. A large increase in domestic currency bond yields often coincides with currency depreciation. The two can combine to raise EME governments' funding costs. In addition, large market moves can trigger unhedged foreign investors' risk limits, leading to asset sales or more hedging. These adverse dynamics have played out in recent months.

A large increase in domestic currency bond yields often coincides with currency depreciation. The two can combine to raise EME governments' funding costs. In addition, large market moves can trigger unhedged foreign investors' risk limits, leading to asset sales or more hedging. These adverse dynamics have played out in recent months.

A potential rating downgrade is another structural vulnerability for several EMEs (Graph A2, right-hand panel). As of late May 2020, several large EMEs were borderline investment grade. A downgrade below investment grade could reduce the pool of potential investors, forcing some to sell their security holdings if they, for instance, have investment grade mandates or match investment grade indices. This cliff effect risks a severe market disruption.

The views expressed are those of the authors and do not necessarily reflect the views of the Bank for International Settlements. The Mexican government has a hedging programme in place to protect public finances from oil price fluctuations. See K Micic, "Recent trends in EME government debt volume and composition", BIS Quarterly Review, September 2017, pp 22-4. See A Aguilar, V Alfonso, R Barbone and C Cantú, "Oil dependence in Latin America", BIS Bulletin, forthcoming. "Original sin redux" is the term coined to describe the risks associated with non-resident ownership of LCGBs; see A Carstens and H S Shin, "Emerging markets aren't out of the woods yet", Foreign Affairs, 15 March 2019. See B Hofmann, I Shim and H S Shin, "Emerging market economy exchange rates and local currency bond markets amid the Covid-19 pandemic", BIS Bulletin, no 5, April 2020; and P Hördahl and I Shim, "EME bond portfolio flows and long-term interest rates during the Covid-19 pandemic", BIS Bulletin, no 18, May 2020.