The 2008 crisis: transpacific or transatlantic?

This study analyses two hypotheses that ascribe the 2008 US financial crisis to capital inflows. The Asian savings glut hypothesis posits that net inflows into high-grade US public bonds from countries running current account surpluses led to the housing boom and bust. An excess of savings over investment abroad led to an excess of US investment over savings. The European banking glut hypothesis holds that gross inflows into private bonds led to the boom. Leveraging-up by European banks enabled the leveraging-up of US households. Gross flows from Europe better matched US mortgage market trends towards private credit risk, floating interest rates and narrow spreads. What is more, European banks produced, not just invested in, US mortgage-backed securities. Their US securities affiliates held huge exposures to such securities that deserve recognition. Furthermore, European banks' leveraging-up also provided credit that enabled housing booms in Ireland and Spain. These findings favour the European banking glut hypothesis.1

JEL classification: E44, F34, G01, G21.

The Great Financial Crisis (GFC) divided the world into three different groups. Some countries experienced housing booms in the years before the crisis, and found themselves at its epicentre: the United States, the United Kingdom, Spain and Ireland. Banks in some other countries had exposed themselves to these booms and suffered banking crises: Germany, Belgium, the Netherlands and Switzerland. Finally, the rest of the world played the role of spectators hit by the seizing-up of the US dollar-based international banking system and the subsequent downward spiral of world trade.

Before the crisis, Bernanke (2005) and others had implicated a set of countries running current account surpluses in the US boom.2 They argued that a savings glut in Asia (better a dearth of investment in countries hit by the Asian financial crisis in 1997-98) and among some commodity exporters had led to a strong bid for safe US bonds. This one-way investment put downward pressure on US bond yields and stimulated US investment, especially in homes. As a result, US spending rose relative to US output, widening the US current account deficit. An excess of Asian saving over investment thus led to an excess of US investment over saving. On this view, these "transpacific" imbalances ultimately caused the GFC (Ferguson (2008), Wolf (2014)).

Key takeaways

- Substantial capital flowed into safe US government bonds and risky US mortgage bonds in the years to 2008.

- US bond market developments in 2000-07 show more of the imprint of the flows into mortgage bonds.

- European banks not only bought risky US mortgage bonds but also manned the production line through their US securities subsidiaries, which were active in packaging and selling such bonds.

- European bank credit also enabled the real estate booms in Ireland and Spain.

Others have pointed instead to two-way transatlantic flows. In the 2000s, European banks leveraged up their equity with dollars borrowed from US and other investors and ploughed them into US private debt. More than anything else, they bought private label mortgage-backed securities (MBS), or complex bonds based on them. Their eager buying of such securities enabled their issuance to surpass that of government agency MBS in 2005. Leveraging-up by European banks begat unsustainable leveraging by US households: the transatlantic crisis (Bayoumi (2017)). In support of this view, Borio and Disyatat (2011) found that gross capital flows from Europe to the United States dominated the net capital flows from surplus countries; they denied the link between global imbalances and the GFC. Acharya and Schnabl (2010) showed that banks from both surplus and deficit countries, mostly in Europe, set up conduits that held risky US MBS funded by short-term commercial paper. Shin (2012) dubbed the alternative hypothesis the banking glut.

This special feature argues that, as an account of key features of the GFC, the savings glut story comes up short and the banking glut story gives more satisfaction. While the flows into US bonds from surplus countries may well have exceeded those from European banks, the latter better match developments in the US mortgage market. European banks' US subsidiaries manned the production line of the private label MBS, issuing them as well as investing in them. Moreover, the more exaggerated property booms in Ireland and Spain drew on even larger portfolio and money inflows from European banks. In contrast to US developments, securitisation played little role in the Irish or Spanish booms, but in common with US developments a strong flow of credit from European banks played a big role.

The rest of this article analyses the Asian and European capital inflows, their imprint on the US mortgage market, the role of European banks' US securities affiliates and evidence that European investors were over-represented as buyers of US MBS. One box examines the relationship between external credit flows and domestic credit booms, and another sketches the larger but more traditional capital flows into Ireland and Spain. A final section concludes that European bank leverage enabled the US, Irish and Spanish booms.

Comparing and contrasting the two gluts

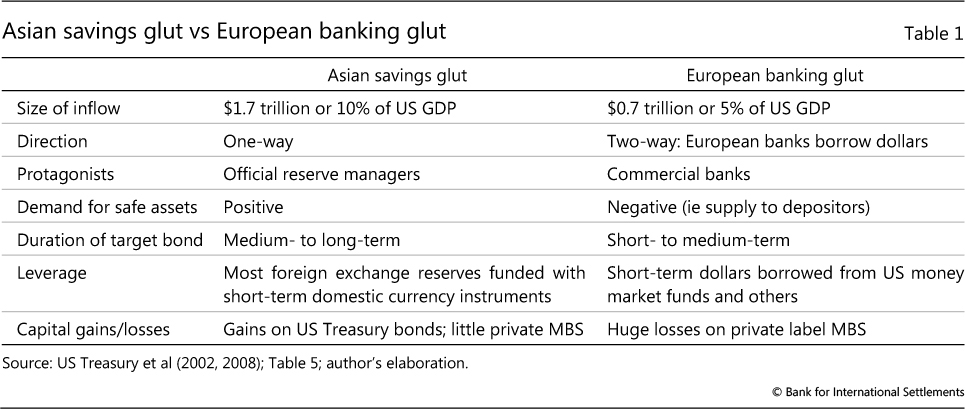

Let us first compare and contrast the capital flows associated with the savings and banking gluts and then pose two questions: Which flow better matches the big changes seen in the US mortgage market? And how did the role of European banks' US securities affiliates as MBS producers enlarge these banks' footprint in this market?

The differences between the two stories bear emphasis (Table 1). Twice as much money flowed into US bonds from March 2000 to mid-2007 from Asian official holders as flowed into US private asset-backed securities from European banks and others between end-2002 and mid-2007. In the first, official reserve managers purchased safe, longer-term US government obligations, generally funding themselves with domestic currency liabilities. In the second, banks purchased riskier, short-term bonds backed by US mortgages, commercial real estate and other assets, funded by short-term dollar debt. Asian reserve managers took duration risk. European banks took credit and maturity risk, buying risky so-called "spread product" to earn a margin over the cost of short-term funding.

The first story presents itself as a current account story, although some countries built foreign exchange reserves despite running current account deficits and some surplus countries did not build up foreign exchange reserves (Borio and Disyatat (2011)). The flow was one-way. The second story is a capital account story, with gross capital flow running in two directions.

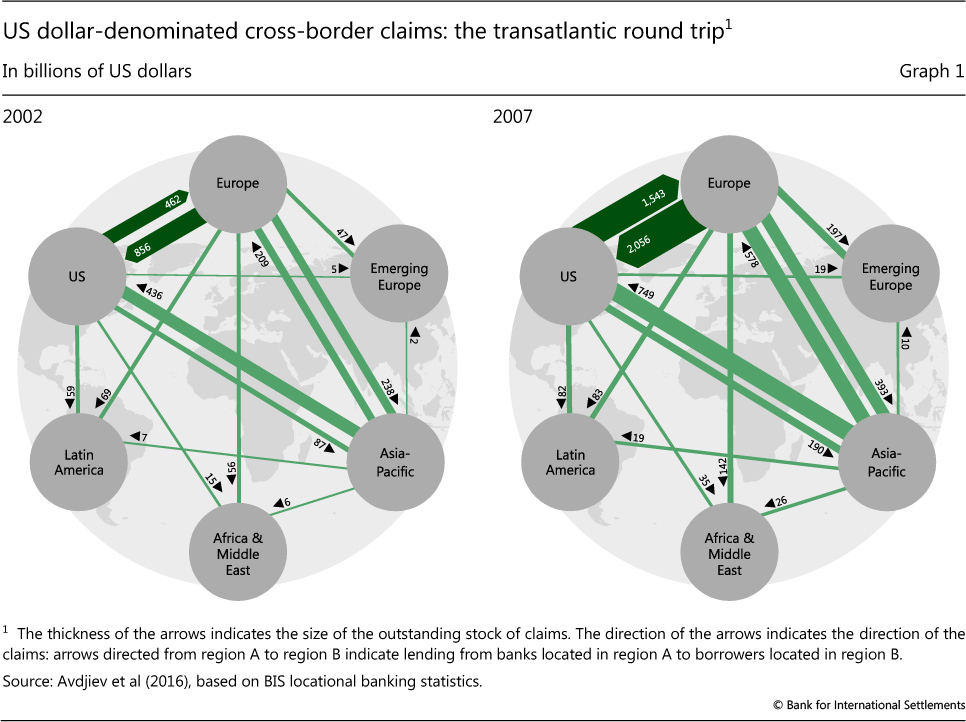

Current accounts drive long-term changes in countries' net international investment positions, albeit with important valuation effects (Gourinchas and Rey (2014)). The evolution of these positions in the United States before the crisis lent itself to an analysis of sustainability that led to dire predictions of dollar crisis as cited above. By contrast, the current account of the euro area, and of Europe as a whole, approximated balance, and few fretted about a sudden stop of European bank intermediation between US investors and highly leveraged US households. Large gross flows from Europe to the US were balanced by flows in the opposite direction: European banks funded portfolios of US assets by "round-tripping" dollar funds from the United States and back again (McGuire and von Peter (2009), Shin (2012) and Avdjiev et al (2016)). Dollars raised from US money market funds (Baba et al (2009)) flowed back Stateside through purchases of private MBS (Graph 1). As a result, someone who looked only at the current account balance overlooked the large risk exposures resulting from these accumulating flows.

The Asian and European flows also differed in their demand for safe assets. Focusing on the official inflow, Caballero et al (2008) saw it as chasing safe assets that Wall Street had a comparative advantage in producing. In fact, official reserve managers steered clear of risky private MBS, however rated (Ma and McCauley (2014)). Instead they hugged the shore of US Treasury bonds and US government-supported agency bonds. Those developing this thesis overlooked European banks' provision of safe assets to US money market funds. These banks invested the proceeds in pseudo-safe MBS, many rated AAA, in a so-called "credit arbitrage" strategy which proved far riskier than expected. Official reserve managers demanded dollar safe assets; European banks supplied them.

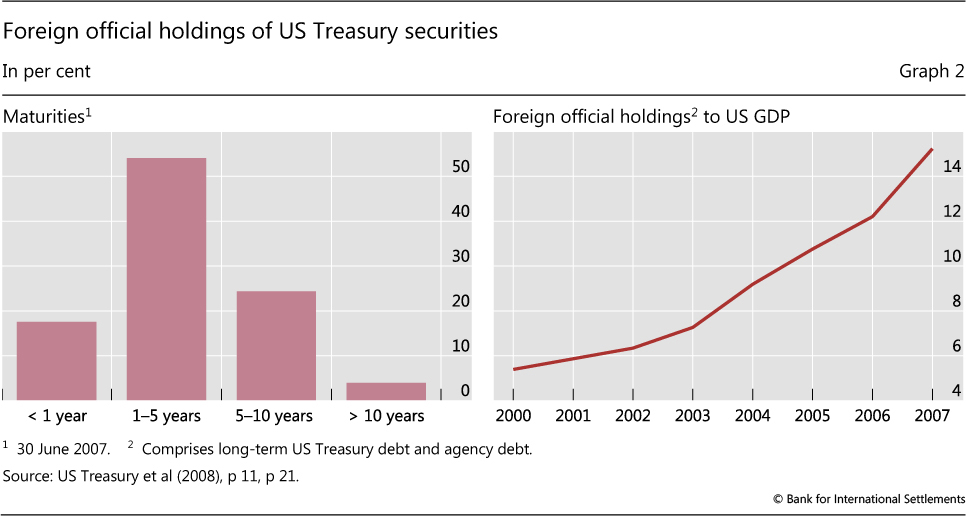

Official reserve managers had long since extended maturities from Treasury bills to Treasury and agency notes. Their sweet spot on the yield curve was at medium-term maturities (Graph 2), which provided extra yield to cover the cost of domestic liabilities or dollar depreciation. By contrast, European banks preferred to match their mostly short-term dollar funding with floating rate MBS. Below we discuss how the US mortgage market reshaped itself around their demand, shifting from Treasury bills to Libor as the benchmark reference rate for adjustable rate mortgages (ARMs).

The portfolio values diverged in the crisis. Official reserve managers enjoyed capital gains as US Treasury bond yields fell and the dollar rose (Gourinchas et al (2012), Bénétrix et al (2015)). European banks, along with US securities firms and some large US banks, suffered massive losses and responded by reducing exposures in Europe (Cecchetti et al (2012)) and elsewhere (McCauley et al (2019)).

Which capital flow matches US mortgage market trends?

Considerable evidence links inflows of bank credit or of debt capital more generally to credit growth within an economy (Box A). In the lead-up to the GFC, however, two very different capital inflows accompanied the boom in private credit in the United States, especially in the mortgage market, in the 2000s. One way of assessing their relative contributions is to compare the expected impact of each flow to the stylised facts of the evolution of the US bond market in those years.

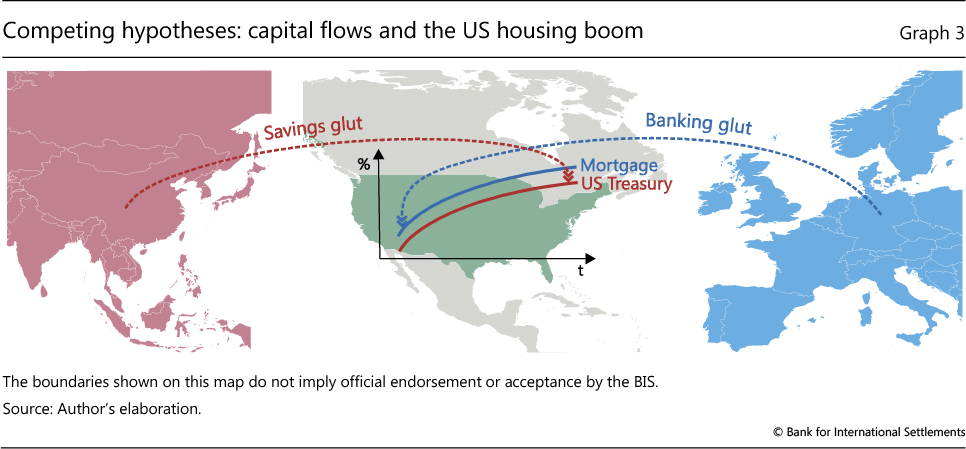

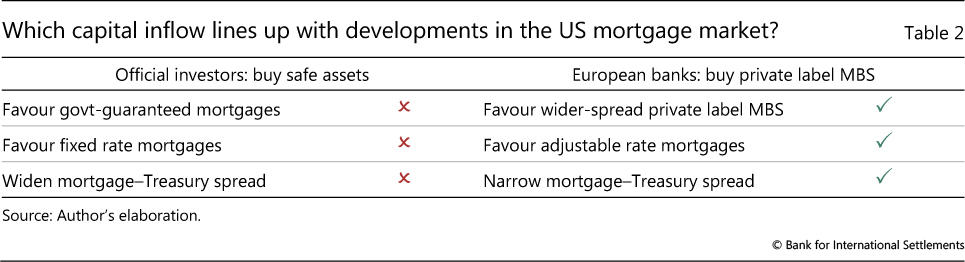

The Asian savings glut story predicted flows into Treasuries and agencies, lower Treasury yields, higher mortgage spreads and more fixed rate mortgages (Graph 3, red arrow). Risk-averse foreign exchange reserve managers typically prefer safe assets, including US Treasury and agency securities (McCauley and Rigaudy (2011)).

Box A

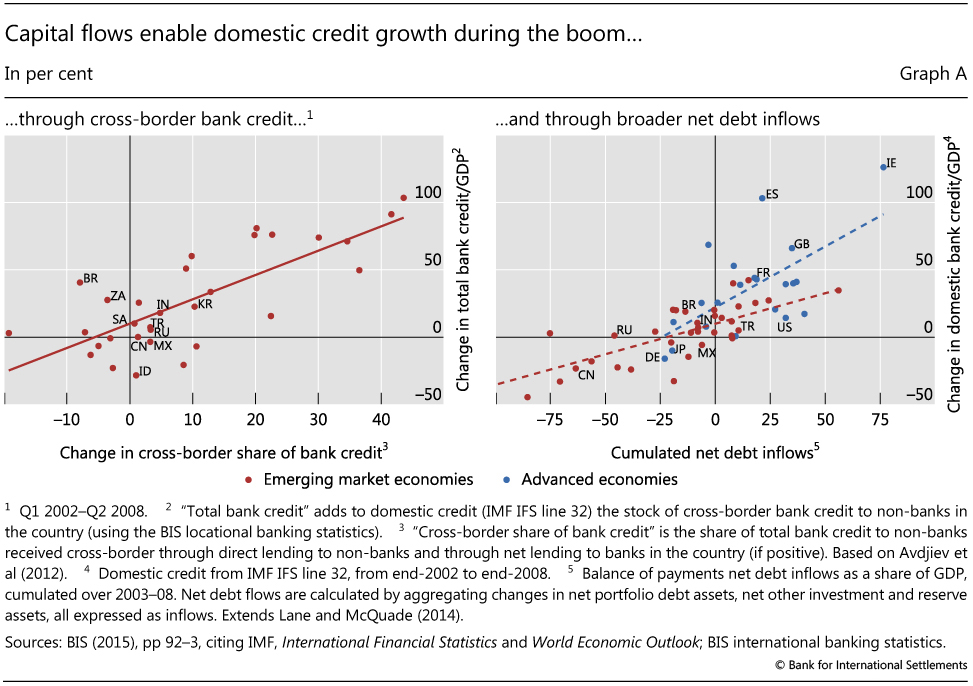

Capital inflows enable domestic credit growth in a boom

Credit booms and capital inflows tend to reinforce one another (Aliber and Kindleberger (2015)). Inflows of foreign capital to banks free them from the constraint of the domestic funding base and thereby enable domestic credit booms. In a sample of 31 emerging market economies between early 2002 and 2008, Avdjiev et al (2012) found that a rise in the share of cross-border bank funding, extended either directly to domestic non-banks or indirectly through banks, helped boost the ratio of bank credit to GDP, a measure of credit booms (Graph A, left-hand panel). Banks found non-core liabilities abroad to fund credit at home (Hahm et al (2013)).

Lane and McQuade (2014), using a broader sample of 62 countries and a more inclusive measure of international capital flows, found a similar dynamic. Here, the larger the net debt inflows, including both portfolio and bank flows, the larger the increase in a given economy's ratio of bank credit to GDP (Graph A, right-hand panel). The inclusion of Ireland, Spain and the United Kingdom shows that a domestic credit boom's reliance on external financing is not a symptom of financial underdevelopment. In fact, in the subsample of 23 advanced economies the response to capital inflows is greater than among EMEs, as the steeper trend line suggests.

Given their preference for intermediate-term notes, this inflow should have depressed Treasury yields at such maturities. US Treasury rates should have fallen by more than MBS yields (even with the diversification of reserve managers into agency securities). And the decline in fixed rate mortgage yields should have biased mortgage lending towards those carrying fixed rates.

The banking glut story focuses on the effect of banks as buyers of risky private mortgage debts. Banks favoured the wider spread over US Treasury obligations that unguaranteed mortgages promised. This preference favoured a shift in mortgage finance from publicly guaranteed to private label MBS. Since banks' readiest funding source is short-term, a banking glut favoured floating rate debt. It would tend to narrow the gap between private yields (especially short- to medium-term) and US Treasury yields, and mortgage spreads in particular (Graph 3, blue arrow).

The first two predicted effects of the Asian savings glut - inflows into US Treasuries and lower Treasury yields - did indeed hold. As noted, $1.7 trillion in official inflows flowed into US Treasury and agency bonds in 2000-07 (Graph 2, right-hand panel). This amounted to about 10% of GDP. Warnock and Warnock (2009) found 10-year yields were 80 basis points lower in 2005 as a result.

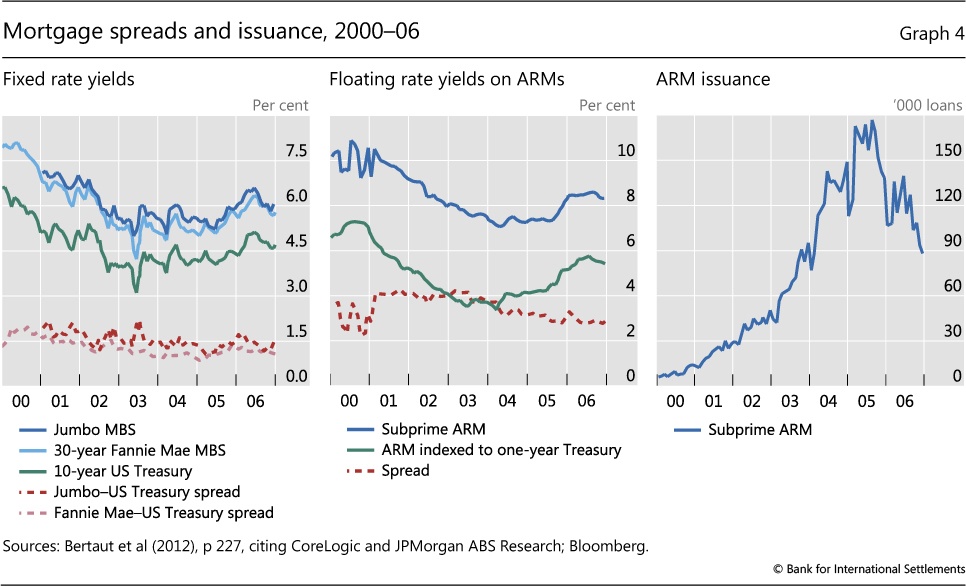

But predictions regarding mortgage flows and yields did not pan out. The left-hand panel of Graph 4 shows that, to the contrary, spreads on fixed rate agency and private jumbo MBS actually narrowed in the 2000s. Furthermore, rather than this being the heyday of fixed rate mortgages as long promoted by the US agencies, ARMs bulked large among the new mortgages securitised without agency guarantees. As a result, fixed rate mortgages declined from an estimated 78% of MBS issues in 2001 to just 60% in mid-2007 (Goodman et al (2008), Exhibits 1.2 and 1.5). Thus, the fixed rate bonds that reserve managers favoured lost share in the boom. In sum, key bond market developments in the 2000s did not match what might have been expected from a big official flow into Treasury notes (Table 2, first column).

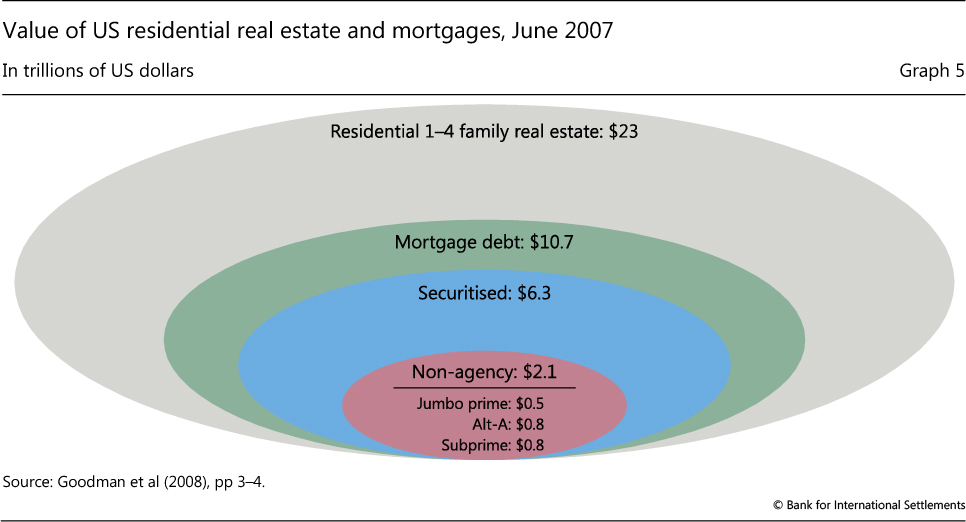

The predictions of the banking glut story perform better (Table 2, second column). First, European banks' demand drove US mortgage finance away from government guarantees to private credit risk. Non-agency mortgages reached 55% of all gross issuance in 2005 and 2006 (Goodman et al (2008), p 6; see also Frankel (2006)). In stock terms, non-agency securitisations reached one third of the total (Graph 5). Second, ARMs predominated in private label MBS, at 62% of private issues (Goodman et al (2008), p 6, p 10), conveniently allowing banks to match their short-term funding. In 2006 ARMs were up to 40% of all MBS issued. In terms of rates, long-term spreads actually narrowed (Graph 4, left-hand panel). Spreads also narrowed for non-agency ARMs relative to agency issues. The centre panel of Graph 4 shows that the spread between subprime ARMs and "conforming", agency ARMs declined by 100 basis points between 2002 and 2006, even as issuance exploded (right-hand panel). One can infer very strong demand.

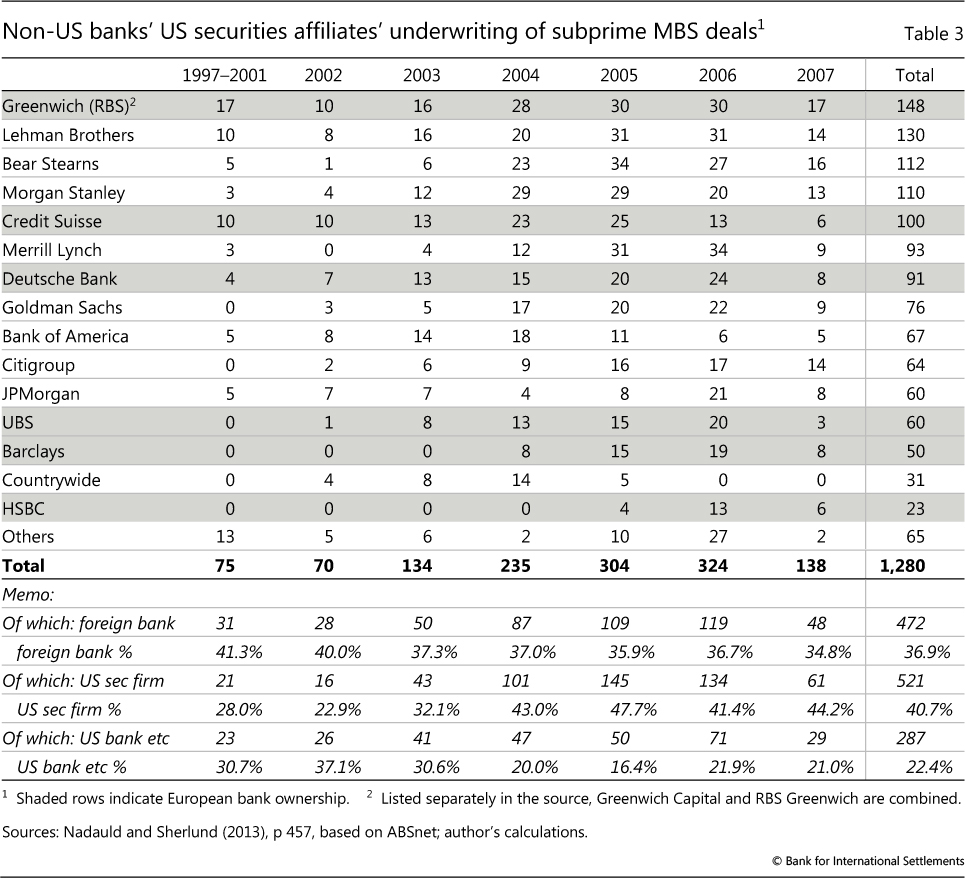

That demand gained strength from European investors in general, and European banks in particular. To appreciate this requires that we recognise that the geography of European banks' balance sheets did not coincide with the borders of Europe (Avdjiev et al (2016)). A full accounting of the role of European banks requires taking the measure of their securities subsidiaries within the United States, mostly funded in the United States. Like the US-owned securities firms with which they competed, their securitisation production lines drove mortgage originators to deliver the raw material (Nadauld and Sherlund (2013)).

European banks as producers of MBS

The usual image of European banks as hapless investors in US MBS in the mid-2000s needs thorough revision. In Zuckerman (2009), Lewis (2010), Dunbar (2011) and US court cases, banks from Dusseldorf or Kiel play the role of sophisticated investors in name only, serving as, in market parlance, "stuffees". However, certain European banks played quite a different role (Bank of England (2007), p 37).

Six European banks produced private label MBS out of their US securities affiliates. They ranked among the top 15 underwriters of subprime MBS (Table 3). RBS's Greenwich ranked first, with a 12% share, above that of Lehman Brothers, Bear Stearns and Morgan Stanley. Collectively, Greenwich, Credit Suisse (ranked fifth). Deutsche Bank (ranked seventh), UBS, Barclays and HSBC claimed a 35-40% share. Crucially, they retained that share as the US securities firms grabbed market share from the big US banks and others in 2004-05 (Table 3, memorandum items).

By 2007, banks' business model of underwriting private MBS had evolved to include holding a substantial fraction of the product on their balance sheets. What Dunbar (2011) and Goldstein and Fligstein (2017) liken to a Henry Ford-type production line started with a "warehouse" of mortgages that underwriters would assemble into MBS. They then sliced and diced these into collateralised debt obligations (CDOs) and booked them as trading assets. By 2007, underwriters could sell lower-rated, wider-spread securities, but mostly ended up holding the "super-senior" tranches in their trading books.3,4

Contemporary observation and subsequent research confirmed the nexus between underwriting and MBS holdings. The Swiss Federal Banking Commission commented (2008, p 7): "At least towards the end of the mortgage boom, the CDO securitization business functioned only to the extent that market players such as UBS, Merrill Lynch and Citigroup were willing and able to retain 'unattractive' low-yield Super Senior CDO tranches of individual securitizations on the own (trading) books" (see also Zuckerman (2009), p 176). In a study of the holdings of highly rated securitisation tranches across US-owned bank holding companies, MBS underwriting strongly predicted holdings (Erel et al (2014)). For UBS, the Commission (p 5) reported that "the CDO Desk had not only securitized CDOs and sold such CDOs to investors, but had retained the Super Senior CDOs- on its own (trading) books".

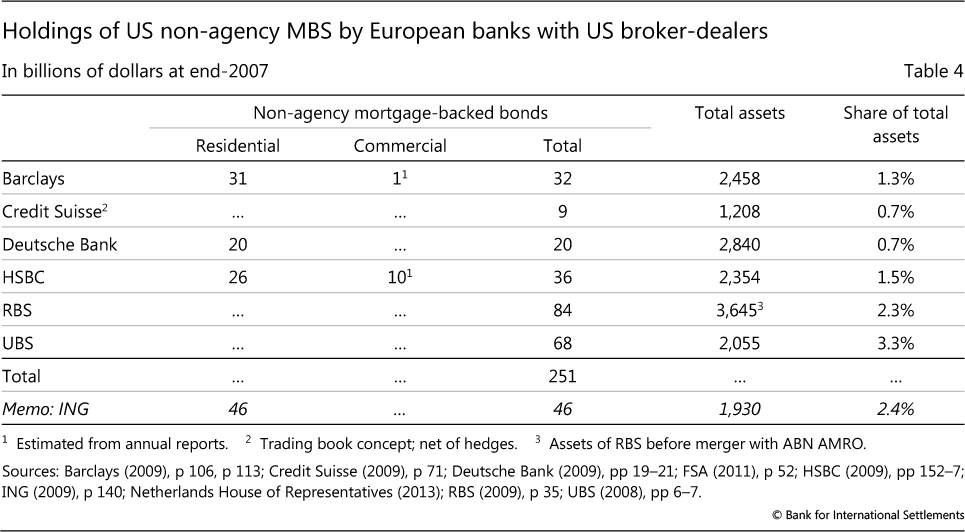

The six European banks had $251 billion of private MBS at end-2007 (Table 4). A seventh, ING, held a further $46 billion in its US internet banking thrift. No doubt, the data from 2008 annual reports and official or officially mandated reports are not consistent across banks, with Credit Suisse in particular reporting on a net trading positions basis.5 Moreover, some of the exposures of the other five banks were hedged, though it is not possible to say how much.6

There are good reasons to suppose that these six European banks held this quarter of a trillion dollars' worth of US MBS in mid-2007 on the balance sheets of their US securities affiliates. As described above, their business models involved holding such securities on the US book, and contemporary observation placed them there. In addition, the ex post aggregate profitability of foreign-owned securities firms in 2008 suggest they did.

In particular, European-owned broker-dealers racked up large losses in 2008 from writedowns of assets, consistent with their having retained ultimately toxic bonds on their US books. The US Bureau of Economic Analysis (BEA) reports that European-owned non-banking finance and insurance firms took capital losses from "widespread write-downs of financial assets" (Ibarra and Koncz (2009), p 29) of no less than $110.8 billion in that crisis year (Lowe (2011), p 98).7

Did European banks hog private US MBS?

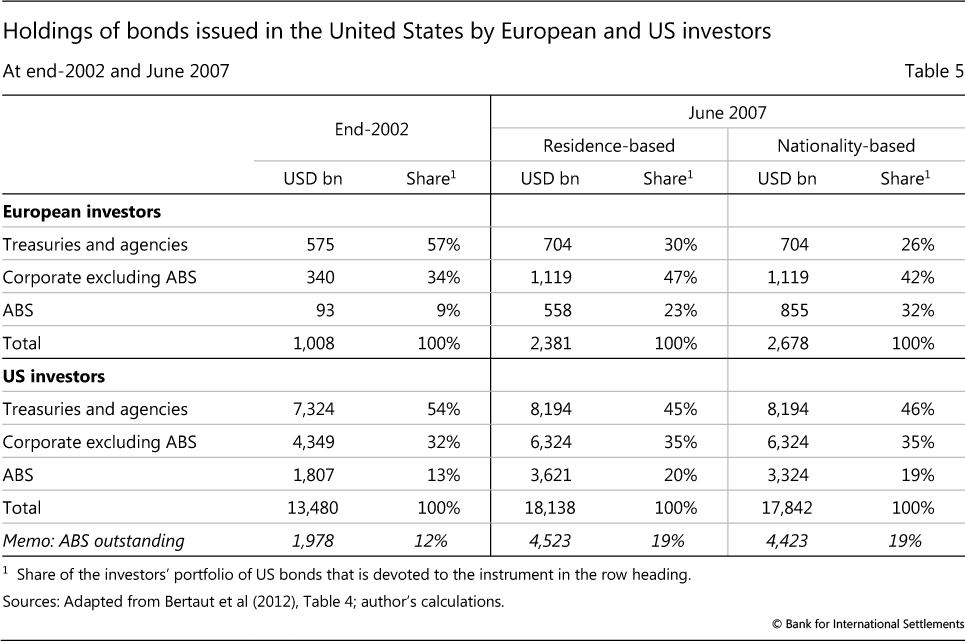

A key element of the banking glut view is the drive by European banks to load up on risky US mortgages. However, Bertaut et al (2012) report that private label asset-backed securities (ABS) represented 23% of US bond holdings of European investors in mid-2007, similar to US investors at 20% (Table 5, fourth column). ABS include residential and commercial MBS, and bonds backed by car loans and airline leases.

These data represent holdings by residence. The more telling observation, however, requires data compiled on a nationality basis. As noted, European banks did not confine their balance sheets within European national borders.

If the exposures discussed in the previous section were held in the US books, then European banks did indeed take on more than their share of the risk arising from leveraged US mortgages. From a nationality perspective, such holdings add to European investors' holdings and subtract from US investors' holdings. This is shown in the last two columns of Table 5, which add to the figures reported by Bertaut et al (2012) on a residency basis the exposures booked on US affiliates from Table 4.

On this showing, European investors, including banks, loaded up on risky US MBS in the years before the GFC. At end-2002, their US bond portfolio resembled that of US investors. Their portfolio consisted of mostly safe Treasury and agency securities, with about a third of it in plain vanilla US corporate bonds. By mid-2007, the profile of European investors' US bonds had veered away from that of US investors towards riskier bonds. Even on a residence basis (Table 5, centre columns), European investors had shifted out of safe Treasury and agency securities into corporate bonds, while US resident portfolios kept Treasury and agency securities in first place. On a nationality basis (two right-hand columns), including holdings at US affiliates, European investors had promoted ABS to second place, above safe assets in third place.8

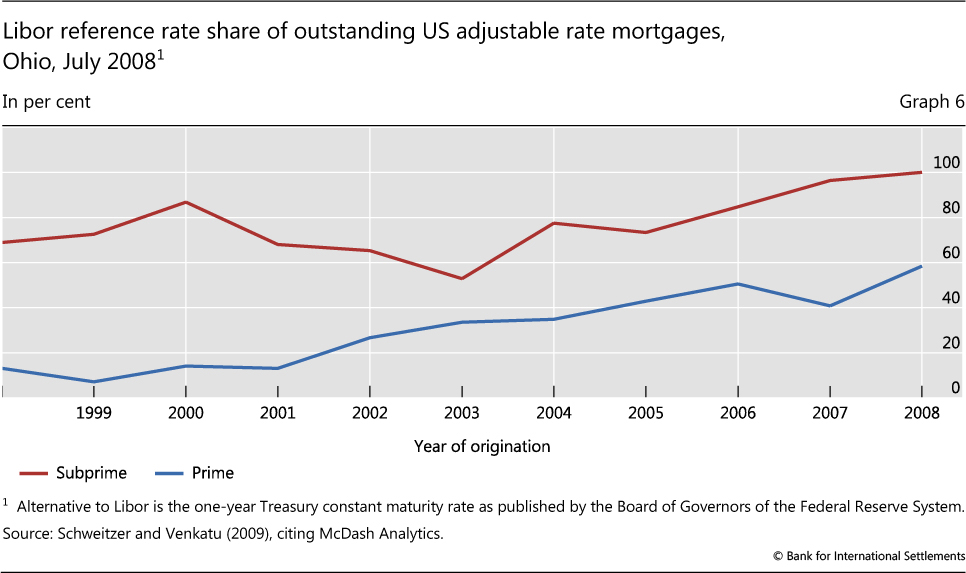

The US mortgage market reshaped its pricing around the needs of foreign banks in the 2000s, highlighting their importance as investors. Historically, ARMs were priced off of national reference rates, mostly one-year Treasury bills. As securitisation picked up with non-US banks as big investors, US mortgage bankers shifted to using offshore Libor as the reference rate. For example, within the stock of Ohio mortgages in July 2008, later vintages of ARMs referred more and more to Libor (Graph 6). The Libor-linked share of subprime reached practically 100%, while that of prime mortgages rose even faster from less than 20% in the turn-of-the-century vintages to 60% by 2008.9 The benchmark was not "Changed by Wall Street, for Wall Street" as Morgenson (2012) headlined, but rather for Lombard Street (London) and for Taunusanlage (Frankfurt).

In sum, European banks claimed a market share of a third or more in the production of highly leveraged MBS. Like the US securities firms analysed by Nadauld and Sherlund (2013), as these underwriters ramped up production, they sent a signal to mortgage bankers to extend more credit. Moreover, European investors, especially European banks, bulked large as ultimate holders of such paper as well. The influence of European banks in the market helped to propel Libor to displace US Treasury bills as the preferred reference rate in floating rate US mortgages.

Why did European banks take on so much exposure to private MBS? Dunbar (2011) and Nadauld and Sherlund (2013) highlight the role of leverage regulation, and Bayoumi (2017) easy access to repo finance. However, while regulation and the repo market permitted risky strategies, they do not explain why bank managers chose them. Part of the answer could be that bank managers took aim at market share (UBS (2008), pp 10-11, Zaki (2008), p 11 and p 15, Martin (2013), p 194 and Chapter 13, Augar (2018), p 153) and size, possibly as a defence against takeover. One perceived advantage of size was that it could boost the credit rating since rating agencies considered size when reckoning the odds of government support in extremis (Hau et al (2013), King et al (2016)).

Certainly, European banks did not confine their expansion to US assets or securitised assets. This is evident from their leading role in funding the Spanish and Irish real estate and credit booms. In these cases, they did not rely on securitisation of the US variety, but still contributed to large capital inflows as well as outsize domestic credit and property price booms (Box B).

Box B

The Spanish and Irish cases: larger inflows from European banks, bigger booms

The Irish and Spanish cases resembled the US case in several salient respects. Both featured a large increase in private credit, big run-ups in house prices and, one way or another, a huge inflow of bank capital. The securitisation of mortgages in the United States should not obscure the role of banks as buyers of the bonds (Connor et al (2012)). And rather than just a heavy reliance on floating rate mortgages at the margin, these European economies relied entirely on floating rate mortgages.

The Spanish and Irish booms differed from the US boom in several important respects, however. For one thing, since both Spain and Ireland were part of the euro area, short-term interest rate setting looked to a broader economic domain than these two booming countries in the periphery (Regling and Watson (2010), p 24, Bank of Spain (2017), p 30).

Second, the investment of official reserves from Asia probably exerted less downward pressure on long-term yields in the euro area than such investment put on US Treasury yields. The dollar attracted about two thirds of reserves in the 2000s and the euro only 20-25%. Add the thoroughgoing reliance on floating rate mortgages in these European countries, rather than the long-term fixed rate debt favoured by official reserve managers, and it is hard to pin much of their booms on the Asian savings glut.

Third, the role of securitisation, the focus of many analyses of the US case, was much reduced in Spain and basically absent in Ireland. In Spain, the regional cajas depended heavily on so-called covered bonds to fund their mortgages, and 75% of these were held by foreign investors (Berges et al (2012)), notably German banks. These do not remove the risk of the mortgages from the originator, so they are better viewed as long-term secured funding rather than as securitisation proper. Other forms of securitisation did not qualify for removal of the assets from the balance sheet owing to limited risk transfer (Almazan et al (2015)).

With little risk transfer of real estate credit, the Irish and Spanish banks only shared their boom exposures to the extent that foreign banks participated in the credit booms directly. In Ireland's case, an RBS subsidiary, Ulster Bank, did manage to run up significant losses, for which the UK rather than the Irish taxpayers ended up paying. In Spain, however, the foreign bank role was limited. On the contrary, the international diversification of the two largest Spanish banks stood them in good stead as earnings abroad stabilised their profitability.

A further aspect that distinguishes the Irish and Spanish cases from the US one is the exposure of banks to property companies. They brought exposure not only to commercial real estate, but also to the construction of houses. On close inspection, the profitability of these in a boom frequently turns on speculation in raw land. This reinforced the banks' exposures to the feedback loop among capital inflows, credit growth and real estate prices.

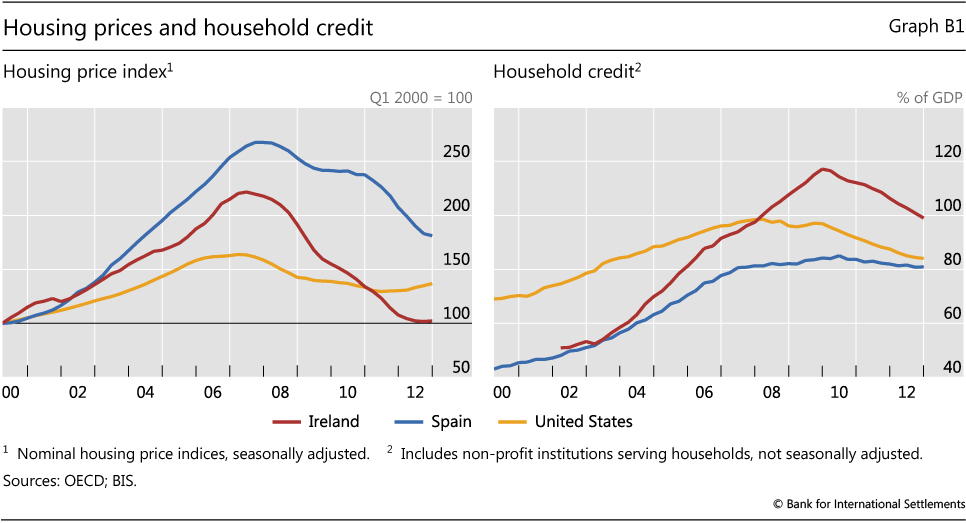

Fifth, house prices and household indebtedness traced more extreme trajectories in Ireland and Spain than in the United States. By the lights of the OECD, at least, house prices boomed more in Spain and Ireland than in the United States (Graph B1, left-hand panel). However, the US index conceals significant regional variation: the Case-Schiller 20-city index for the United States more than doubled between 2000 and the peak in mid-2006.

Ireland takes the prize for the largest run-up in household debt of the three as a share of GDP (Graph B1, right-hand panel). It rose by 50% of GDP through 2008, even before the ratio surged as the denominator fell. But Spain was not far behind. On this measure, the US experience was again relatively mild.

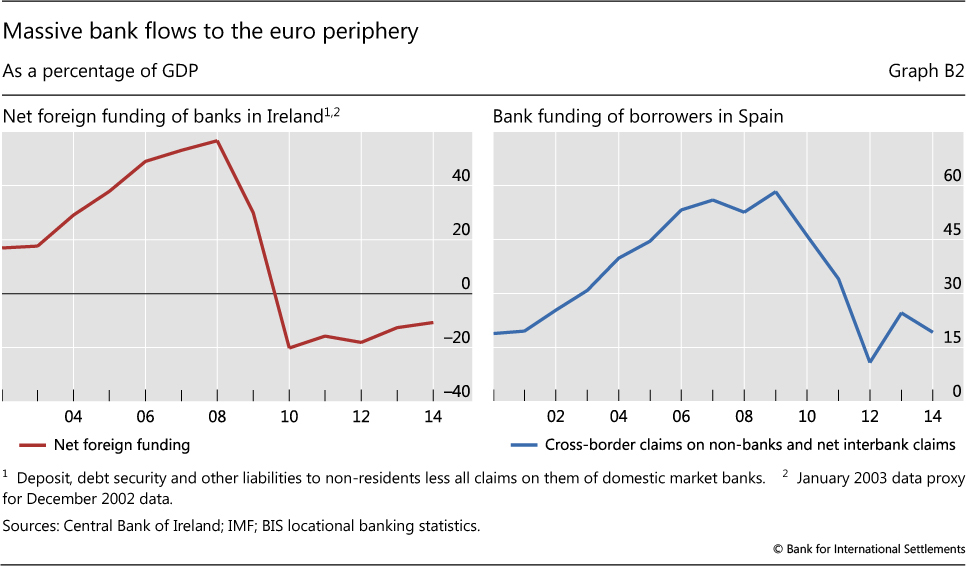

A final way in which the Irish and Spanish cases distinguish themselves from the US case is in the scale of the capital inflow. The left-hand panel of Graph B2 shows the net foreign liabilities of the banks in Ireland with local lending business. It shows a net inflow of over 50% of GDP (Everett (2017)). Recall that the inflow of official reserves into US Treasuries from end-2000 to mid-2007 amounted to 10% of 2007 GDP, and the change in European investors' holdings of US ABS in the same period amounted to about half that. In other words, even stripping out foreign banks' offshore activity in Ireland, and counting both the transpacific and transatlantic flows to the United States, the inflow of external funding into the Irish banking system was triple these capital flows into the United States.

It shows a net inflow of over 50% of GDP (Everett (2017)). Recall that the inflow of official reserves into US Treasuries from end-2000 to mid-2007 amounted to 10% of 2007 GDP, and the change in European investors' holdings of US ABS in the same period amounted to about half that. In other words, even stripping out foreign banks' offshore activity in Ireland, and counting both the transpacific and transatlantic flows to the United States, the inflow of external funding into the Irish banking system was triple these capital flows into the United States.

The inflow of bank credit to Spain also reached staggering proportions (Graph B2, right-hand panel). Since Spain does not have a large presence of offshore banking, we simply sum the stock of BIS reporting banks' cross-border claims on non-banks in Spain with their net cross-border claims on banks in Spain (see Avdjiev et al (2012) for further discussion). This aggregate rose from 15% of Spanish GDP to almost 60%.

Despite the differences, the key similarity stands out. European banks enabled credit booms in the United States, Ireland and Spain. The crises also cumulated: US losses crippled many European banks and sapped their defences against strains in Europe.

The US data include non-profits. Excluding offshore banks; see Honohan (2006), Central Bank of Ireland (2010) and Lane (2015).

Conclusions

The GFC was, in Delong's (2009) phrase, the "wrong crisis" that struck the wrong part of the US bond market (Tooze (2018)). Official reserve managers could have staged a sudden stop or even reversal of their purchase of US Treasury bonds. This could have imposed a dollar depreciation and a costly adjustment on the US economy. Instead, in 2007-08, highly leveraged European banks scrambled to secure dollar funding as they experienced credit losses - and the dollar appreciated sharply (McCauley and McGuire (2009)). European banks' vulnerability arose from their role as producers of the ultimately toxic assets as well as from their role as investors. As a result, their affiliates' US balance sheets required massive writedowns in 2008.

The banking glut offers a better account than the savings glut for US mortgage market developments of the 2000s. Large official inflows into US Treasury and agency notes should have reinforced a US mortgage market dominated by fixed rate mortgages that enjoyed government agency guarantees. Instead, we observe a big shift to mortgages priced with floating ("adjustable") interest rates and to more risky, leveraged mortgages that agencies could not guarantee. The dominance of the savings glut with its demand for safe assets should have manifested itself in wider spreads, but the spread of the riskiest mortgages over normal ones actually narrowed.

The banking glut also better accounts for the parallel real estate booms and busts in Spain and Ireland. True, official reserve managers did invest in euro-denominated government bonds. But the Irish and Spanish mortgage markets work on floating rates closely tied to the policy rates set by the ECB. Again, expansion-minded European banks provide a more compelling account of these banking systems' remarkable ease of external financing. In fact, the Irish and Spanish banking systems experienced capital inflows that were huge in relation to the inflows into the United States in the same years.

It would be wrong to argue the banking glut to the exclusion of the savings glut. Along the line that Bertaut et al (2012) argue, the huge inflow into safe assets compressed the term premium on safe assets (lowering the return to taking duration risk), and thereby induced a search for yield in credit. But it would also be wrong to claim that US and European investors responded to this incentive in the same manner. European investors shifted their US bond portfolio in the direction of credit risk markedly more than US investors did.

The Irish and Spanish credit and real estate booms did not require features much emphasised in the US case (eg FCIC (2011)): securitisation with (or without) risk transfer (Connor et al (2012), Carbó-Valverde et al (2012), Almazan et al (2015) and Acharya et al (2013)), reliance on faulty, conflicted ratings (UBS (2008)), or a big government role in the housing market (Rajan (2010), Morgenson and Rosner (2011)). But banks in Ireland and Spain did depend on credit from European banks that were working their equity harder. Occam's razor cuts in favour of one account for such similar and simultaneous phenomena.

References

Acharya, V and P Schnabl (2010): "Do global banks spread global imbalances? Asset-backed commercial paper during the financial crisis of 2007-09", IMF Economic Review, vol 58, no 1, pp 37-73.

Acharya, V, P Schnabl and G Suarez (2013): "Securitization without risk transfer", Journal of Financial Economics, vol 107, issue 3, pp 515-36.

Aliber, R and C Kindleberger (2015): Manias, panics and crashes, 7th edition, Palgrave.

Almazan, A, A Martín-Oliver and J Saurina (2015): "Securitization and banks' capital structure", The Review of Corporate Finance Studies, vol 4, no 2, pp 206-38.

Augar, P (2018): The bank that lived a little: Barclays in the age of the very free market, Allen Lane.

Avdjiev, S, R McCauley and P McGuire (2012): "Rapid credit growth and international credit: challenges for Asia", BIS Working Papers, no 377, April.

Avdjiev, S, R McCauley and H S Shin (2016): "Breaking free of the triple coincidence in international finance", Economic Policy, vol 31, issue 87, July, pp 409-51.

Baba, N, R McCauley and S Ramaswamy (2009): "US dollar money market funds and non-US banks", BIS Quarterly Review, March, pp 65-81.

Bank for International Settlements (2015): 85th Annual Report, June.

Bank of England (2007): Financial stability report, issue no 22, October.

Bank of Spain (2017): Report on the financial and banking crisis in Spain, 2008-2014.

Barclays Bank PLC (2009): Annual report 2008.

Bayoumi, T (2017): Unfinished business: the unexplored causes of the financial crisis and the lessons yet to be learned, Yale University Press.

Beltran, D, L Pounder and C Thomas (2008): "Foreign exposure to asset-backed securities of US origin", Board of Governors of the Federal Reserve System, International Finance Discussion Papers, no 939, August.

Bénétrix, A, P Lane and J Shambaugh (2015): "International currency exposures, valuation effects and the Global Financial Crisis", Journal of International Economics, vol 100, issue 1, pp 518-40.

Berges, A, E Ontiveros and F Valero (2012): "The internationalization of the Spanish financial system", in J L Malo de Molina and P Martin-Acena (eds), The Spanish financial system, Palgrave, pp 347-81.

Bernanke, B (2005): "The global saving glut and the US current account", Sandridge Lecture, Virginia Association of Economists, Richmond, Virginia, 10 March.

--- (2018): "The real effects of the financial crisis", Brookings Papers on Economic Activity, fall.

Bernanke, B, C Bertaut, L Pounder DeMarco and S Kamin (2011): "International capital flows and the returns to safe assets in the United States, global imbalances and financial stability", Bank of France, Financial Stability Review, no 15, February.

Bertaut, C, L Pounder DeMarco, S Kamin and R Tryon (2012): "ABS inflows to the United States and the global financial crisis", Journal of International Economics, vol 88, no 2, pp 219-34.

Borio, C and P Disyatat (2011): "Global imbalances and the financial crisis: link or no link?" BIS Working Papers, no 346, May.

Caballero, R, E Farhi and P-O Gourinchas (2008): "An equilibrium model of 'global imbalances' and low interest rates", American Economic Review, vol 98, pp 358-93.

Carbó-Valverde, S, D Marques-Ibanez and F Rodríguez-Fernández (2012): "Securitization, risk-transferring and financial instability: the case of Spain", Journal of International Money and Finance, vol 31, pp 80-101.

Cecchetti, S, R McCauley and P McGuire (2012): "Interpreting TARGET2 balances", BIS Working Papers, no 393, December.

Central Bank of Ireland (2010): The Irish banking crisis: regulatory and financial stability policy, 2003-2008, A Report to the Minister for Finance by the Governor of the Central Bank, 31 May.

Connor, G, T Flavin and B O'Kelly (2012): "The US and Irish credit crises: their distinctive differences and common features", Journal of International Money and Finance, vol 31, pp 60-79.

Credit Suisse (2009): Annual report 2008.

Delong, B (2009): "The wrong financial crisis", VoxEU, 10 October.

Deutsche Bank (2009): Annual review 2008.

Dunbar, N (2011): The devil's derivatives, Harvard Business Review Press.

Edwards, S (2005): "Is the US current account deficit sustainable? If not, how costly is adjustment likely to be?", Brookings Papers on Economic Activity, no 1:2005, pp 211-71.

Erel, I, T Nadauld and R Stulz (2014): "Why did holdings of highly rated securitization tranches differ so much across banks?" Review of Financial Studies, vol 27, no 2, pp 404-53.

Everett, M (2017): "Blowing the bubble: the global funding of the Irish credit boom", The Economic and Social Review, vol 46, no 3, autumn, pp 339-65.

Ferguson, N (2008): The ascent of money, Penguin.

Financial Crisis Inquiry Commission (2011): The financial crisis inquiry report, January.

Financial Services Authority (2011): The failure of the Royal Bank of Scotland: Financial Services Authority Board Report, December.

Frankel, A (2006): "Prime or not so prime? An exploration of US housing finance in the new century", BIS Quarterly Review, March, pp 67-78.

Goldstein, A and N Fligstein (2017): "Financial markets as production markets", Socio-Economic Review, vol 15, no 3, pp 483-510.

Goodman, L, S Li, D Lucas, T Zimmerman and F Fabozzi (2008): Subprime mortgage credit derivatives, John Wiley.

Gorton, G and A Metrick (2012): "Securitized banking and the run on repo", Journal of Financial Economics, vol 104, issue 3, June, pp 425-51.

Gourinchas, P-O, H Rey and K Truempler (2012): "The financial crisis and the geography of wealth transfers", Journal of International Economics, vol 88, no 2, pp 266-85.

Gourinchas, P-O and H Rey (2014): "External adjustment, global imbalances, valuation effects", in G Gopinath, E Helpman and K Rogoff (eds), Handbook of international economics, vol 4, North Holland, pp 585-646.

Hahm, J-H, H S Shin and K Shin (2013): "Noncore bank liabilities and financial vulnerability", Journal of Money, Credit and Banking, vol 45, issue 1, April, pp 3-36.

Hau, H, S Langfield and D Marques-Ibanez (2013): "Bank ratings: what determines their quality?" Economic Policy, vol 28, issue 74, pp 289-333.

Honohan, P (2006): "To what extent has finance been a driver of Ireland's economic success?", ESRI Quarterly Economic Commentary, winter, pp 59-72.

HSBC Holdings PLC (2009): Annual report and accounts 2008.

Ibarra, M and J Koncz (2009): "Direct investment positions for 2008: country and industry detail", Survey of Current Business, July, pp 20-34.

ING (2009): 2008 Annual Report.

Kalse, E (2009): "ING Direct was source of success and problems for Dutch bank", NRC Handelsblad, 30 October.

King, M, S Ongena and N Tarashev (2016): "Bank standalone credit ratings", BIS Working Papers, no 542, February.

Krugman, P (2007): "Will there be a dollar crisis?", Economic Policy, vol 22, no 51, pp 436-67.

Lane, P (2015): "The funding of the Irish domestic banking system during the boom", paper presented to Statistical and Social Inquiry Society of Ireland, 15 January, revised February.

Lane, P and P McQuade (2014): "Domestic credit growth and international capital flows", Scandinavian Journal of Economics, vol 116, issue 1, January, pp 218-52.

Lewis, M (2010): The big short, Allen Lane.

Lowe, J (2011): "Direct investment for 2007-2010: detailed historical-cost positions and related financial and income flows", Survey of Current Business, November, pp 50-137.

Ma, G and R McCauley (2014): "Global imbalances: China and Germany", China & World Economy, vol 22, no 1, pp 1-29.

Martin, I (2013): Making it happen: Fred Goodwin, RBS and the men who blew up the British economy, Simon & Schuster.

McCauley, R, A Bénétrix, P McGuire and G von Peter (2019): "Deglobalisation in banking?", Journal of International Money and Finance, forthcoming.

McCauley, R and P McGuire (2009): "Dollar appreciation in 2008: safe haven, carry trades, dollar shortage and overhedging", BIS Quarterly Review, December, pp 85-93.

McCauley, R and J-F Rigaudy (2011): "Managing foreign exchange reserves in the crisis and after", "Portfolio and risk management for central banks and sovereign wealth funds", BIS Papers no 58, October, pp 19-47.

McGuire, P and G von Peter (2009): "The US dollar shortage in global banking", BIS Quarterly Review, March, pp 47-63.

Moody's Investors Service (2007): "ABCP market at a glance: ABCP credit arbitrage snapshot", Structure Finance Special Report, 31 August.

Morgenson, G (2012): "Changed by Wall Street, for Wall Street" New York Times, 28 July, p BU1.

Morgenson, G and J Rosner (2011): Reckless endangerment, Henry Holt and Company.

Nadauld, T and S Sherlund (2013): "The impact of securitization on the extension of subprime credit", Journal of Financial Economics, vol 107, no 2, October.

Netherlands House of Representatives, Committee of Parliamentary Inquiry into the Financial System (2013): Credit lost II - taking stock, 19 April 2012.

Obstfeld, M and K Rogoff (2005): "Global current account imbalances and exchange rate adjustments", Brookings Papers on Economic Activity, no 1:2005, pp 67-123.

Rajan, R (2010): Fault lines, Princeton University Press.

RBS (2009): Annual report and accounts, 2008.

Regling, K and M Watson (2010): A preliminary report on the sources of Ireland's banking crisis.

Schweitzer, M and G Venkatu (2009): "Adjustable-rate mortgages and the Libor surprise", Federal Reserve Bank of Cleveland, Economic Commentary, January.

Setser, B and N Roubini (2005): "Our money, our debt, our problem", Foreign Affairs, vol 84, no 4, Jul/Aug, pp 194-8.

Shin, H S (2012): "Global banking glut and loan risk premium", IMF Economic Review, vol 60, no 2, pp 155-92.

Summers, L (2004): "The US current account deficit and the global economy", Per Jacobsson Lecture, International Monetary Fund, October.

Swiss Federal Banking Commission (2008): UBS subprime report, 16 October.

Swiss National Bank (2010): 102nd Annual Report.

Tooze, A (2018): Crashed: how a decade of financial crises changed the world, Viking.

UBS (2008): Shareholder report on UBS's write-downs, April.

US Senate, Committee on Homeland Security and Governmental Affairs, Permanent Subcommittee on Investigations (2011): Wall Street and the financial crisis: anatomy of a financial collapse, 13 April.

US Treasury, Federal Reserve Bank of New York and Board of Governors of the Federal Reserve (2002): Report on foreign holdings of US long-term securities as of March 31, 2000, April.

--- (2008): Report on foreign portfolio holdings of US securities as of June 30, 2007, April.

Warnock, F and V Warnock (2009): "International capital flows and US interest rates", Journal of International Money and Finance, vol 28, pp 903-19.

Wolf, M (2014): The shifts and the shocks, Penguin.

Zaki, M (2008): UBS, les dessous d'un scandale, Favre Sa.

Zuckerman, G (2009): The greatest trade ever: how John Paulson bet against the markets and made $20 billion, Penguin Viking.

1 An earlier version of this paper was presented to the conference "The 2008 Global Financial Crisis in retrospect", University of Iceland, 30-31 August 2018. The author would like to thank Robert Aliber, Michael Bordo, Claudio Borio, Richard Cantor, Jaime Caruana, Guy Cecala, Stijn Claessens, Ben Cohen, Patrick Honohan, Philip Lane, Patrick McGuire, Fernando Restoy, Catherine Schenk, Hyun Song Shin, Marcel Zimmerman, Gyfli Zoega and Daniel Zuberbuehler for helpful discussion and Yifan Ma and Jeff Slee for able research assistance. The views expressed are those of the author and do not necessarily reflect those of the BIS.

2 Bernanke et al (2011) recognised that domestic vulnerabilities contributed to the crisis; Bernanke (2018) has emphasised the role of financial panic, recalling the "run on repo" of Gorton and Metrick (2012). Several prominent economists in the 2000s worried about current account imbalances and their accumulation into unsustainable net external debt. Summers (2004), Edwards (2005), Obstfeld and Rogoff (2005) and Setser and Roubini (2005) warned of an impending sudden stop of financing that would lead the dollar to plunge and the US economy to enter a recession. Krugman (2007) memorably pictured the dollar reaching a Wile E Coyote moment and then falling.

3 By contrast, Cayman Island entities owned MBS held in asset-backed commercial paper (ABCP) conduits, designed to keep the assets off the sponsor's balance sheet. US Treasury et al (2008) should have captured these holdings in mid-2007 as foreign. In 2007, European banks sponsored ABCP conduits holding at least $100 billion in US MBS (Moody's (2007), Acharya and Schnabl (2010), p 56, Acharya et al (2013), p 522). The last column of Table 3 thus understates European exposures.

4 Greg Lippmann at Deutsche Bank emailed about the buyers of MBS tranches in February 2007 (US Senate (2011), p 349): "[T]he other side is all cdos so it is the cdo investors who r on the other side who buys cdos: aaa-reinsurance, ws [Wall Street] conduits, European and Asian banks, aa-high grade cdos, European and Asian banks and insurers-. some US insurers, bbb other mezz [mezzanine] abs [asset-backed security] cdos (i.e. ponzi scheme), European banks and insurers, equity some US hedge funds, Asian insurance companies, Australian and Japanese retail investors through mutual funds".

5 A position could be short over a certain range of prices, but long thereafter. Lewis (2010, Chapter 9) describes how Morgan Stanley took a short position in BBB tranches "netted" against multiple long positions in AAA tranches (sold in part to UBS), with disastrous results.

6 Deutsche Bank's CDO desk famously put on a multi-billion dollar short (Zuckerman (2009), Lewis (2010), Dunbar (2011)), but US Senate (2011) found that overall the bank remained long and took losses.

7 The presumption is that UBS's US affiliate took losses on the $25 billion in US ABS transferred at appraised prices by UBS to the SNB-funded Stabilisation Fund in September 2008 (Swiss National Bank (2010), pp 83-5). In the BEA data, foreign-owned non-banking finance and insurance firms reported overall losses of $60 billion in 2008. This sum exceeded the net losses of $40 billion recorded by the rest of foreign-owned firms in the financial sector, including depository institutions. Foreign-owned depository institutions reported capital losses of $41 billion (Lowe (2011), p 98). Much of this loss was presumably accounted for by ING Direct USA, which had boosted returns at its US internet banking thrift, ING Direct, by switching its assets from agency paper to risky Alt-A MBS (Kalse (2009)). Asian- and Canadian-owned non-banking affiliates, absent from Table 4, reported capital losses of only $1.7 billion and $5.7 billion, respectively.

8 Within ABS, foreign investors had more than their share of ultimately risky mortgage bonds. Beltran et al (2008), Table 6, estimate that non-US investors held 29% of $2.2 trillion in securitised non-agency home mortgages. Including amounts in Table 4 on the assumption that they were held on balance sheets in the United States takes this share above 40%. This share is well above private foreign investors' 14% of US Treasury bonds outstanding or 9% of agency bonds outstanding.

9 "'It was all about securitization, especially subprime loans,' said Guy D. Cecala, publisher of Inside Mortgage Finance, an industry authority. 'You had Wall Street saying, "If we want to sell this overseas, we have to pick a more international-flavored index." Subprime lenders just started using it overnight, and then it started to spill out into any loan you wanted to securitize'" (Morgenson (2012)).