The new era of expected credit loss provisioning

Following the Great Financial Crisis, accounting standard setters have required banks and other companies to provision against loans based on expected credit losses. While the rules adopted by the two main standard-setting bodies differ, banks must in both cases provision for expected credit losses from the time a loan is originated, rather than awaiting "trigger events" signalling imminent losses. In the short term, provisions may rise but the impact on regulatory capital is expected to be limited. However, the new rules are likely to alter the behaviour of banks in credit downturns, potentially dampening procyclicality. Banks, supervisors and market participants must prepare for their respective roles in implementing the new approach and assessing its impact.1

JEL classification: G21, G28, M40, M48.

The Great Financial Crisis (GFC) of 2007-09 highlighted the systemic costs of delayed recognition of credit losses on the part of banks and other lenders. Pre-crisis, application of the prevailing standards was seen as having prevented banks from provisioning appropriately for credit losses likely to arise from emerging risks. These delays resulted in the recognition of credit losses that were widely regarded as "too little, too late". Furthermore, questions were raised about whether provisioning models, including the effect of provisioning on regulatory capital levels, contributed to procyclicality by spurring excessive lending during the boom and forcing a sharp reduction in the subsequent bust.

Following the crisis, the G20 Leaders, investors, regulatory bodies and prudential authorities called for action by accounting standard setters to improve loan loss provisioning standards and practices. In response, the International Accounting Standards Board (IASB) in 2014 published IFRS 9 Financial Instruments, which includes a new standard for loan loss provisioning based on "expected credit losses" (ECL).2 For its part, the US Financial Accounting Standards Board (FASB) published its final provisioning standard based on "current expected credit losses" (CECL) in 2016.3 The new standards will come into effect between 2018 and 2021.4

Under both IASB standards5 and FASB standards, the current accounting model for recognising credit losses is commonly referred to as an "incurred loss model" because it requires the recording of credit losses that have been incurred as of the balance sheet date, rather than of probable future losses. Loss identification is based on the occurrence of "triggering" events supported by observable evidence (eg borrower loss of employment, decrease in collateral values, past-due status) combined with expert judgment. The new "expected credit loss" standards replace this with a more forward-looking approach that emphasises shifts to the probability of future credit losses, even if no such triggering events have yet occurred.

Section 1 looks more closely at the motivation for expected credit loss standards. Section 2 outlines the key features of the new standards, highlighting the main differences between the IASB and FASB approaches. Section 3 considers the transition, drawing on recent surveys by accounting firms and supervisors. Section 4 considers how the new standards might affect patterns of bank lending and procyclicality once they are in place. A concluding section examines the role of central banks, supervisors and other stakeholders in implementing the new regime.

Why provision for expected credit losses?

Borio and Lowe (2001) observe that, conceptually, if lending rates accurately reflected credit risks, banks would have no reason to set aside additional provisions at the initiation of a loan to cover expected losses. The higher interest margin on a risky loan would reflect the increased risk of non-payment, while a higher discount rate (reflecting greater risk) on the loan's cash flows would offset the higher interest margin in guiding the bank's lending decision. Of course, capital would still be needed to cover unexpected losses. Provisions would then be appropriate if the riskiness of the loan increases after initiation, to recognise the higher discount rate and reduced likelihood of repayment - or, equivalently, the value of the loan would be marked down as part of a fair value accounting approach. By the same token, a bank might even take "negative provisions" (an increase in asset values) if riskiness were to recede.

Why, then, should provisions be based on expected losses from the moment a loan is initiated? One answer is that loan pricing may not reflect the risks because of transitory market conditions. If past experience and sound modelling suggest that credit risks are not fully reflected in loan pricing decisions, prudent risk management would suggest supplementing market signals with additional evidence. A second set of explanations relate to capital. Peek and Rosengren (1995) and Dugan (2009) note that the need to maintain adequate capital (or rebuild deficient capital) is less likely to bind banks' decisions in good times than in bad, creating a bias to lend freely during upswings. Forward-looking provisioning essentially brings the capital cost of a lending decision forward in time, restoring (to some extent) the incentive value of capital for marginal lending decisions, even in times when the capital buffer itself is not a binding constraint.

Against this, some point to the danger that allowing too much judgment in setting provisions could enable banks to use provisioning to smooth earnings, reducing the transparency of financial accounts and hence their usefulness to investors and counterparties. To avoid this impression, provisioning standards need to set clear rules for when and how provisions are established and adjusted over time, along with transparency as to methodologies and assumptions.

Numerous studies have established that delayed or backward-looking provisioning practices contribute to the procyclicality of bank lending, while forward-looking provisioning reduces procyclicality. For example, Laeven and Majnoni (2003), looking at 1,419 banks in 45 countries in the 1988-99 period, find a positive relationship between provisions and pre-provision earnings, suggesting that banks use provisions to smooth income, and that a negative relationship holds between provisions and growth in lending and GDP, implying that provisions are procyclical. Beatty and Liao (2011), looking at quarterly data on 1,370 US banks in the 1993-2009 period, find that a longer delay in banks' loan-loss recognition increases the negative impact of recessions on bank lending. They find this result for several measures of delayed loss recognition at the bank level: a flow measure (the responsiveness of provisions to past non-performing loans (NPLs)), a stock measure (the ratio of loan loss allowances to contemporaneous NPLs) and a market measure (the link between a bank's current reported income and future equity returns). Bushman and Williams (2012) apply a similar approach to banks in 27 countries, measuring the relationship between banks' loan-loss provisions and their past and future NPLs. They find that banks' risk-taking discipline (the tendency to reduce leverage when asset volatility rises) is greater for banks that take provisions well ahead of actual loan losses.

Regulatory interventions can alter some of these effects. Jiménez et al (2013), study the "statistical provisioning" regime introduced by Spanish supervisory authorities in 2000, which was intended to introduce a more forward-looking element to Spanish banks' general provisions. They find that the initial strengthening of provisioning requirements dampened bank lending, and that subsequent policy adjustments that loosened the requirements spurred lending - but that these effects were stronger for banks where capital and provision levels were already high.6

In its April 2009 report on addressing procyclicality in the financial system,7 the Financial Stability Forum (FSF) noted that "Earlier recognition of loan losses could have dampened cyclical moves in the current crisis," and argued that "earlier identification of credit losses is consistent both with financial statement users' needs for transparency regarding changes in credit trends and with prudential objectives of safety and soundness." The FSF report recommended: "The FASB and IASB should reconsider the incurred loss model by analysing alternative approaches for recognising and measuring loan losses that incorporate a broader range of available credit information." These recommendations were endorsed by the G20 Leaders8 and taken up by the IASB and FASB, with the input and encouragement of the newly formed Financial Stability Board (FSB), the Basel Committee on Banking Supervision (BCBS), key banking, insurance and securities regulators, and the IASB-FASB Financial Crisis Advisory Group, as well as investors and other stakeholders.9

Overview of the new standards

The IASB and FASB standards share a number of features. Both are designed to provide financial statement users with more useful information about a company's ECL on financial instruments that are not accounted for at fair value through profit or loss (eg trading portfolios). The impairment approach requires banks and other companies to recognise ECL and to update the amount of ECL recognised at each reporting date to reflect changes in the credit risk of financial assets. Both approaches are forward-looking and eliminate the threshold for the recognition of ECL, so that it is no longer necessary for a "trigger event" to have occurred before credit losses are reported. And both standards require companies to base their measurements of ECL on reasonable and supportable information that includes historical, current and - for the first time - forecast information. Thus, the effects of possible future credit loss events on ECL must be considered.10

Where the two standards differ is mainly in terms of the degree to which losses are recognised over an asset's lifetime. The FASB calls for a consideration of ECL over the life of a loan from the time of its origination whereas the IASB favours a staged approach.

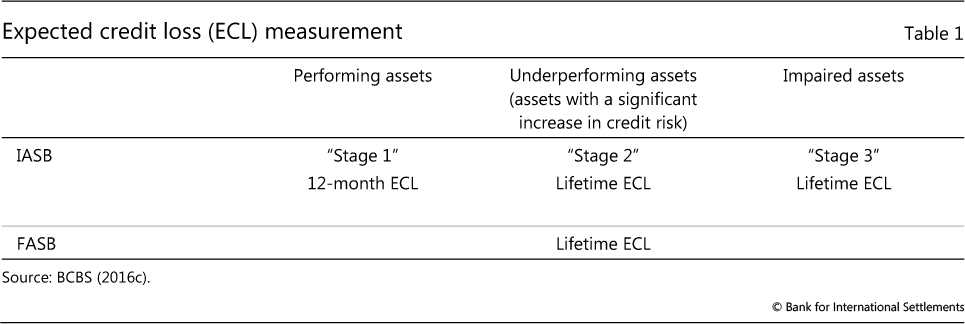

More specifically, as summarised below and in Table 1, IFRS 9 requires banks and other companies to report ECL in three stages as the deterioration in credit quality takes place.11 For Stage 1, they would report "12-month expected credit losses" and for Stages 2 and 3, full "lifetime expected credit losses".

In Stage 1 under the IASB approach, which would begin as soon as a financial instrument is originated or purchased, 12-month ECL are recognised as an expense and a loss allowance is established. This serves as a proxy for the initial expectations of credit losses. For financial assets, interest revenue is calculated on the gross carrying amount (ie without adjustment for the loss allowance). Unless its credit quality changes, the same treatment will then apply every subsequent year until its maturity.

A bank or other lender would calculate 12-month ECL as the portion of lifetime ECL that may result from default events on a financial instrument within the 12 months after the reporting date. This is understood as the likely credit loss on an asset over its lifetime times the probability that the default will occur in the next 12 months.

If at inception a bank can identify assets or a portfolio of such assets that are expected to have a substantial default risk over the coming year, such assets would be more appropriately considered under Stages 2 or 3.

When credit quality is deemed to deteriorate significantly and is no longer considered to be "low credit risk", the asset would move into Stage 2. At this point, the full lifetime ECL would be reported. The resulting increase in the provisions is typically expected to be significant. As in Stage 1, interest income is calculated based on the gross carrying amount (ie without adjustment for ECL).

Under IFRS 9, lifetime ECL is the expected present value of losses that arise if borrowers default on their obligations at some time during the life of the financial asset. For a portfolio, ECL is the weighted average credit losses (loss-given-default) with the probability of default as the weight.12 The relationship between lifetime and 12-month ECL will depend on many factors, including the loan's maturity as well as how default risks and recovery values are expected to evolve over the life of a loan.

Significant increases in credit risk may be assessed on a collective basis, for example on a group or subgroup of financial instruments. This should ensure that lifetime ECL are recognised when there is a significant increase in credit risk, even if evidence of that increase is not yet available on an individual asset level. IFRS 9 presumes that a loan has significant credit risk when it becomes 30 days past due and, thus, must be shown in Stage 2 or 3, where provisions are based on lifetime ECL.13

Stage 3 occurs when the credit quality of a financial asset deteriorates to the point that credit losses are incurred or the asset is credit-impaired. Lifetime ECL would continue to be reported for loans in this stage of credit deterioration but interest revenue is calculated based on the lower net amortised cost carrying amount (ie the gross carrying amount adjusted for the loss allowance).

The FASB approach, by contrast, does not distinguish provisioning according to stages. Instead, the full lifetime ECL are recognised in provisions from the time of origination (Table 1).

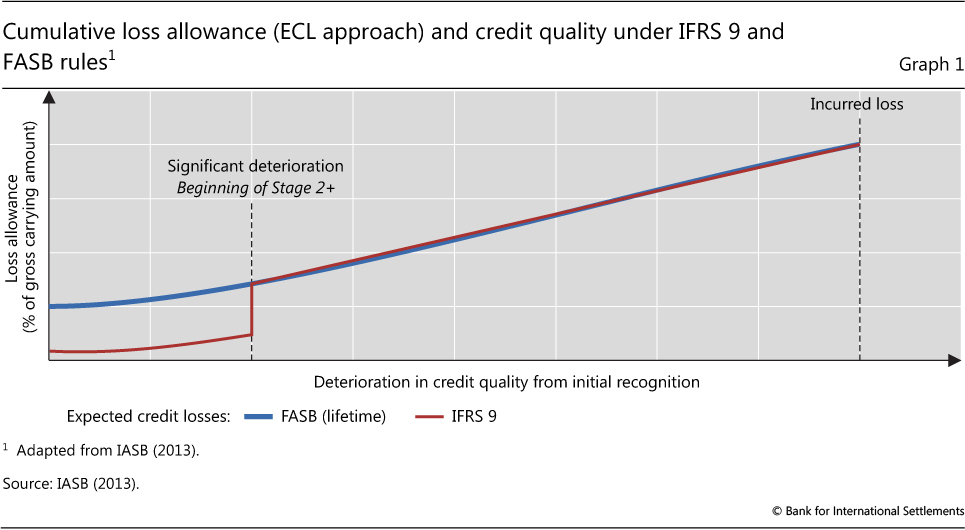

Since lifetime ECL are recorded for all exposures, the recognition of credit losses is expected to be earlier and more significant under the FASB approach, compared with the IASB approach, where only the 12-month ECL are recognised in Stage 1 (Graph 1).

This would result in lower provisions under the IASB standard for loans that have not yet suffered significant deterioration in credit quality (Stage 1). The two approaches converge in utilising lifetime credit losses only once significant credit deterioration occurs.

A second key IASB-FASB difference involves income recognition on problem loans. IFRS 9 continues to allow banks to book the accrual of interest income on non-performing loans even if the bank is not receiving some or all of the cash income due on the loan. By contrast, the FASB standard allows a bank or other creditor to use existing accounting methods for recording payments received on non-accrual assets, including a cash basis method, a cost recovery method or some combination of both. Since the accrued interest could be overstated and unreliable, the cash basis method and the cost recovery method are widely recognised as being more conservative approaches to interest income recognition for non-performing loans.14, 15 Some observers have expressed concern that allowing banks to continue to recognise income on non-performing loans, coupled with inadequate loan loss provisioning and delayed loan write-off practices, has provided disincentives for banks in countries following IFRS to reduce their excessive levels of non-performing loans.16 In September 2016, these concerns prompted the European Central Bank (ECB) to propose including information on both accrued interest income on non-performing loans and the "cash interest income received" (similar to non-accrual treatment) for non- performing loans for supervisory reporting purposes as well as public disclosure.17

Box A

Key aspects of the BCBS supervisory guidance, 2015

The BCBS supervisory guidance contains eight principles for banks on robust governance, methodologies, credit risk rating processes, experienced credit judgment and allowance adequacy, ECL model validation, common data and risk disclosures. The BCBS also has three principles calling for supervisors to adequately evaluate credit risk management, ECL measurement and capital adequacy.

In discussing the principles in the supervisory guidance, the BCBS highlights that banks must maintain sound corporate governance over their credit risk management and ECL estimation processes. Sound bank methodologies for assessing credit risk and estimating ECL should cover all lending exposures, including for restructured and credit impaired loans, should be subject to independent reviews, and must go beyond historical and current data to consider relevant forward-looking information. Clear roles and responsibilities for model validation are needed along with adequate independence and competence, sound documentation and independent process review.

The BCBS further stresses that supervisors should assess credit risk management, ECL measurement and factor these into their assessment of banks' capital adequacy. In doing so they may make use of the work performed by banks' internal and external auditors in reviewing banks' credit risk assessment and ECL measurement functions.

In December 2015, the BCBS published its final supervisory guidance to address how ECL accounting approaches should interact with a bank's overall credit risk management practices. It expresses the Committee's support for the use of ECL approaches and encourages their application in a manner that will provide incentives for banks to follow sound credit risk management and robust provisioning practices.18 The guidance is intended to complement, not replace, the relevant accounting standards and it encourages robust implementation by banks and thorough supervisory review (see Box A).

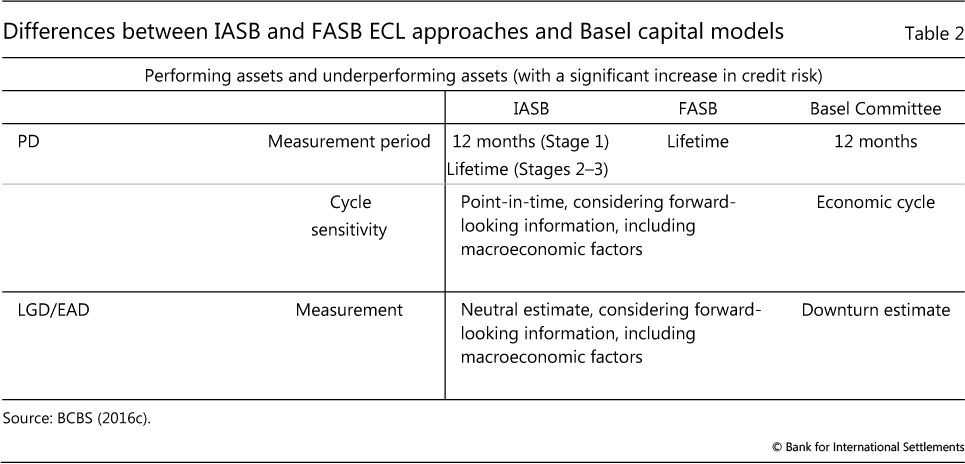

The BCBS notes that banks may have well established regulatory capital models for the measurement of expected losses. However, while these models may be used as important starting points for estimating ECL for accounting purposes, regulatory capital models may not be directly usable without adjustment in the measurement of accounting ECL, given their different objectives and inputs (Table 2). For example, the Basel capital framework's expected loss calculation for regulatory capital differs from accounting ECL in that the Basel capital framework's probability of default (PD) may be "through the cycle" and is based on a 12-month time horizon. Another difference is that loss-given-default (LGD) in the Basel capital framework reflects downturn economic conditions, while in the accounting framework it is intended to be neutral to the business cycle.19

The transition: banks' progress in implementation

The IASB standard is mandatorily effective for annual periods beginning on or after 1 January 2018, although earlier adoption is permitted. The FASB rules become effective from 2020 for listed companies and 2021 for all other firms.

In 2016, global surveys by major accounting firms and other organisations noted that, despite progress by banks in implementing the IFRS 9 standard, considerable work remains. For example, Deloitte's Global Banking IFRS Survey captured the views of 91 banks - 15 from the Asia-Pacific region, seven from Canada, and 69 from Europe, the Middle East and Africa - including 16 global systemically important financial institutions (G-SIFIs).20 Similar surveys were performed by PricewaterhouseCoopers UK (PwC), which surveyed 43 institutions in 10 countries,21 and Ernst and Young. In November 2016, the European Banking Authority (EBA) published its report on the IFRS 9 implementation progress of over 50 financial institutions across the European Economic Area.22 Barclays (2017) estimated the impact of IFRS 9 on capital and provisions in Europe from a careful examination of disclosures by 28 large European banks.

One key finding was that many banks are still assessing the impact. In the Deloitte survey, 60% of banks either did not disclose or could not quantify the transition impact. In the PwC survey, 30% did not yet have an indication of the impact.

Of the banks who did estimate impacts, the majority in the Deloitte survey estimated that total loan loss provisions would increase by up to 25% across asset classes. In the PwC survey, 19% of respondents expect an increase of 0-10%, while 32% expect an increase between 10-30%. These were in line with the findings of the EBA, which estimated an increase of 18% on average and up to 30% for 86% of respondents. Barclays estimates an increase of about one third for the typical bank in its sample, mostly from the recognition of lifetime ECL for loans in Stage 2.

The estimated corresponding decrease in capital is relatively moderate. In the Deloitte survey, 70% of respondents anticipate a reduction of up to 50 bp in core Tier 1 capital ratios. However, most banks do not yet know how their regulators will incorporate the allowance estimates into regulatory capital definitions. The EBA reported that, while quantitative estimates provided by survey respondents were preliminary, CET1 and total capital ratios would fall, on average, by 59 bp and 45 bp respectively. CET1 and total capital ratios are estimated to fall by up to 75 bp for 79% of respondents. Barclays translates its increase in provisions to an average fall in capital of about 50 bp. Supervisors are exploring ways to ease the burden of adjustment as banks boost their capital ratios (Box B).

Box B

Capital adequacy in the transition

While supporting ECL provisioning standards, the BCBS is considering the implications for regulatory capital. One concern is that the impact of ECL provisioning could be significantly more material than currently expected and result in an unexpected decline in capital ratios. The two-year difference between the IASB and FASB implementation dates could also raise level-playing-field issues.

One concern is that the impact of ECL provisioning could be significantly more material than currently expected and result in an unexpected decline in capital ratios. The two-year difference between the IASB and FASB implementation dates could also raise level-playing-field issues.

With these concerns in mind, in October 2016, the BCBS released a consultative document that proposed to retain for an interim period the current regulatory expected loss (EL) treatment of provisions under the standardised and the internal ratings-based (IRB) capital approaches for credit risk. In addition, the BCBS requested comments on three possible transition approaches to allow banks time to adjust to the new ECL accounting standards.

- Approach 1: Day 1 impact on Common Equity Tier 1 (CET1) capital spread over a specified number of years;

- Approach 2: CET1 capital adjustment linked to Day 1 proportionate increase in provisions; or

- Approach 3: Phased prudential recognition of IFRS 9 Stage 1 and 2 provisions.

The BCBS mentioned that its current preference is for Approach 1 because it directly addresses a possible "capital shock" in a straightforward manner. Nevertheless, comments on Approaches 2 and 3 were encouraged because they consider the ongoing evolution of ECL provisions during the transition period and not just the impact at the date of adoption of ECL accounting on banks' provisions and CET1 capital. Once finalised, any transition approach would be accompanied by related Pillar 3 disclosure requirements.

BCBS (2016c, 2016d). As previously mentioned, IFRS 9 will be effective in 2018 and the FASB's CECL standard will be effective starting in 2020 for listed companies and 2021 for all other firms.

Box C

Enhanced risk disclosure needed during the transition period to IFRS 9

The importance to market confidence of useful disclosure by financial institutions of their risk exposures and risk management practices has been underscored during the GFC and its aftermath. At the FSB's request, the Enhanced Disclosure Task Force (EDTF) recommended disclosures to help market participants understand the upcoming changes to ECL approaches and to promote consistency and comparability. The EDTF's report, published in December 2015, found that investors and other financial report users want to understand the specific reasons for any changes at transition in ECL loan loss provisions compared with the existing approach and the ongoing drivers of variability in credit losses.

The EDTF recommended that a gradual and phased approach during the transition period would be most useful to users by giving them clearer insights, as implementation progresses, into the likely impacts of the new ECL standards and to allow users to make useful comparisons between banks. The initial focus should be on qualitative disclosures but quantitative disclosures - including the impact on earnings and capital of ECL approaches - should be added as soon as they can be practicably determined and are reliable but, at the latest, in 2017 annual reports for banks following IFRS. For example, the EDTF recommends banks following IFRS should provide:

- qualitative disclosures about general ECL concepts, differences from the current approach, and implementation strategy, starting with 2015 and 2016 annual reports;

- qualitative disclosures about detailed principles, governance organisation and capital planning impact starting with 2016 annual reports; and

- disclosure of quantitative assessments of the impact of adoption of the ECL approach starting when practicable and reliable but, at the latest, in 2017 annual reports.

In addition, the EDTF recommended that the granularity of disclosures should improve each year during this transition period. When IFRS 9 becomes effective, banks would provide the required ECL disclosures.

The FSB convened the EDTF in May 2012 to develop principles for improved bank disclosures and identify leading practice risk disclosures. The EDTF comprised senior officials and experts representing financial institutions, investors and analysts, credit rating agencies and external auditors. In October 2012, it reported recommendations to the FSB (EDTF (2012)), which were welcomed by the G20 Leaders, the FSB and the chairs of the IASB and FASB. EDTF (2015). A similar approach, adjusted for the applicable transition period years, would be used for banks subject to US GAAP, including the FASB's CECL standard.

The surveys pointed to a need for further work on modelling, data and implementation. Overall data quality and the availability of the origination lifetime PD were the biggest data concerns for most banks. Total estimated programme budgets continued to increase. However, Deloitte found that more than three quarters of these budgets had yet to be spent, less than two years before the IFRS 9 effective date, and that almost half of surveyed banks did not have enough technical resources to complete the project. The EBA found that the involvement of some key stakeholders, which in general included senior credit risk experts, audit committees and the board of directors, seemed limited.

Deloitte asked its respondents how IFRS 9 would affect their pricing strategies for mortgages, corporate loans and other products. Most self-described "price makers" expect that it will have an impact on product pricing, while self-described "price takers" still think that this is unlikely. The divergent views suggest some scope for uncertainty and experimentation.

On disclosure, Ernst and Young, which surveyed 36 top-tier financial institutions worldwide in 2016, found that "most banks expect to disclose a first quantitative impact assessment to the markets during 2017." Of the 36 surveyed banks, 28 have already implemented the EDTF's 2012 recommendations but only 23 plan to implement the EDTF's recommended ECL disclosures. Despite IAS 8 requirements and the 2015 EDTF recommendations for improved ECL transition disclosures, over 40% of banks do not plan to disclose quantitative information before 2018.23 See Box C for a further discussion.

The steady state: impact on the financial system

As discussed above, a number of academic studies have found that more prompt loss recognition, measured over a variety of data sets and indicators, reduces the procyclicality of bank lending. Would the new FASB and IASB approaches achieve this goal?

Some observers are sceptical. Barclays (2017), for example, suggests that a "typical" recession may reduce European bank CET1 ratios by an average 300 bp, which would probably lead to a cut-back in lending. The Barclays analysts focus on the "cliff effect" in the IFRS framework, where the shift from a one-year expected loss in Stage 1 to a lifetime loss in Stage 2 would force a sharp increase in provisions in the early stages of a downturn. By contrast, the incurred-loss approach, while delaying recognition to the later stages of a typical recession, would allow banks to accumulate an additional buffer stock of capital through retained earnings before the needed provisions are taken.

Against this, a number of points can be made. First, there is no guarantee that banks accumulate the needed provisions even as expected losses grow. Indeed, many banks continued to pay dividends throughout the GFC despite apparent capital shortfalls. Early loss recognition would accelerate the process of balance sheet clean-up so that banks are in a better position to support a recovery. Second, post-crisis regulatory efforts have focused on building capital buffers to the point that, even once they are reduced in a downturn, the bank would remain a going concern. According to BCBS (2016b), large ("Group 1") banks maintained fully phased-in Basel III CET1 ratios of 11.8% at end-December 2015, well above the target level (including the capital conservation buffer) of 7%. These buffers ought to be large enough to absorb shocks related to forward-looking provisioning; if they are not, this would call for capital buffers to be strengthened, not for provisioning to be delayed. And third, the provisioning rules (in combination with the strengthened regulatory and supervisory framework) are designed to reduce the build-up of loans in the upturn phase of the cycle. This should reduce the capital cost of an increase in provisions when the cycle starts to turn.

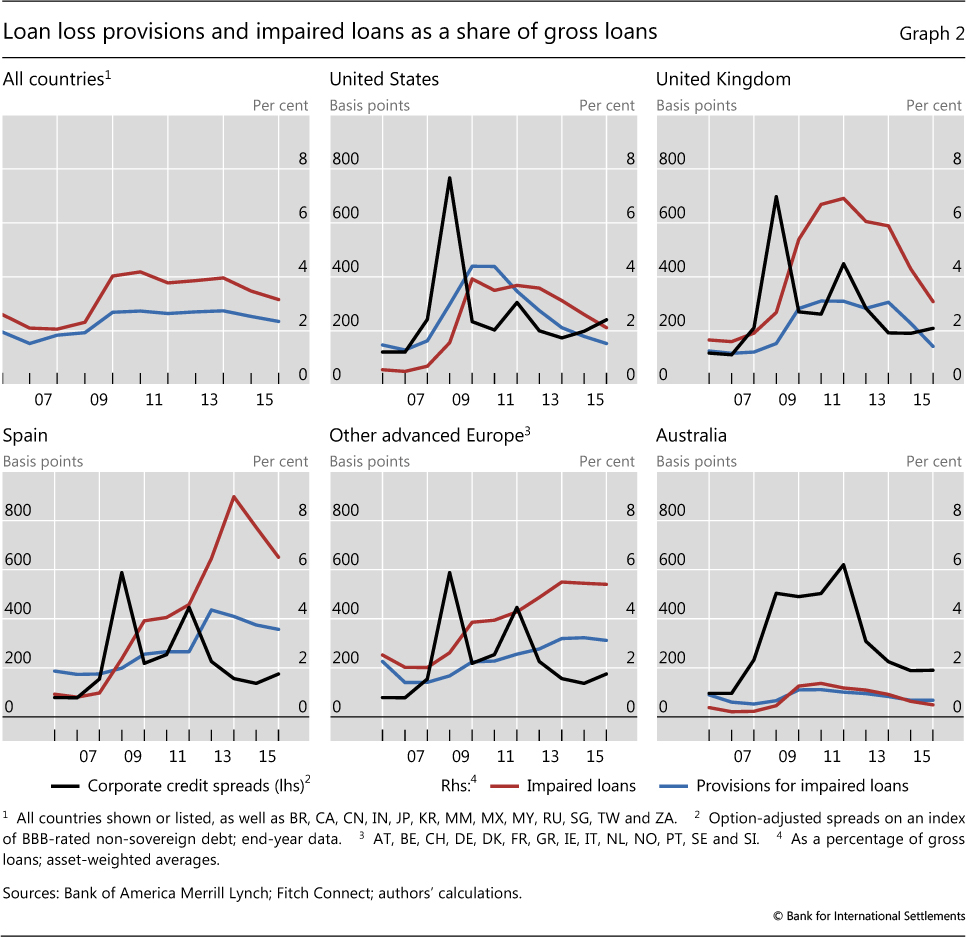

The experience of bank provisioning and impairments in the GFC and subsequent European sovereign debt crises offers some insight into these patterns (Graph 2). Across most countries and regions, both loan loss provisions (blue lines) and the stock of impaired loans (red lines) peaked a year or two after market signals of heightened credit risk (for example, the black lines that represent corporate credit spreads).24 Provisions and impaired loans need not coincide - provisions are set against credit losses, which typically fall short of the full carrying value of the loan. For example, a bank might judge some portion of the impaired loans will be recovered, depending on the quality of the underlying assets and/or collateral. It is notable, however, that the relationship between loan loss provisions and impaired loans varies sharply across countries and regions. In Spain, for example, the statistical provisioning policy boosted provisions above impaired loans ahead of the two crises, but the subsequent rise in impaired loans was nevertheless well ahead of what had been set aside earlier.

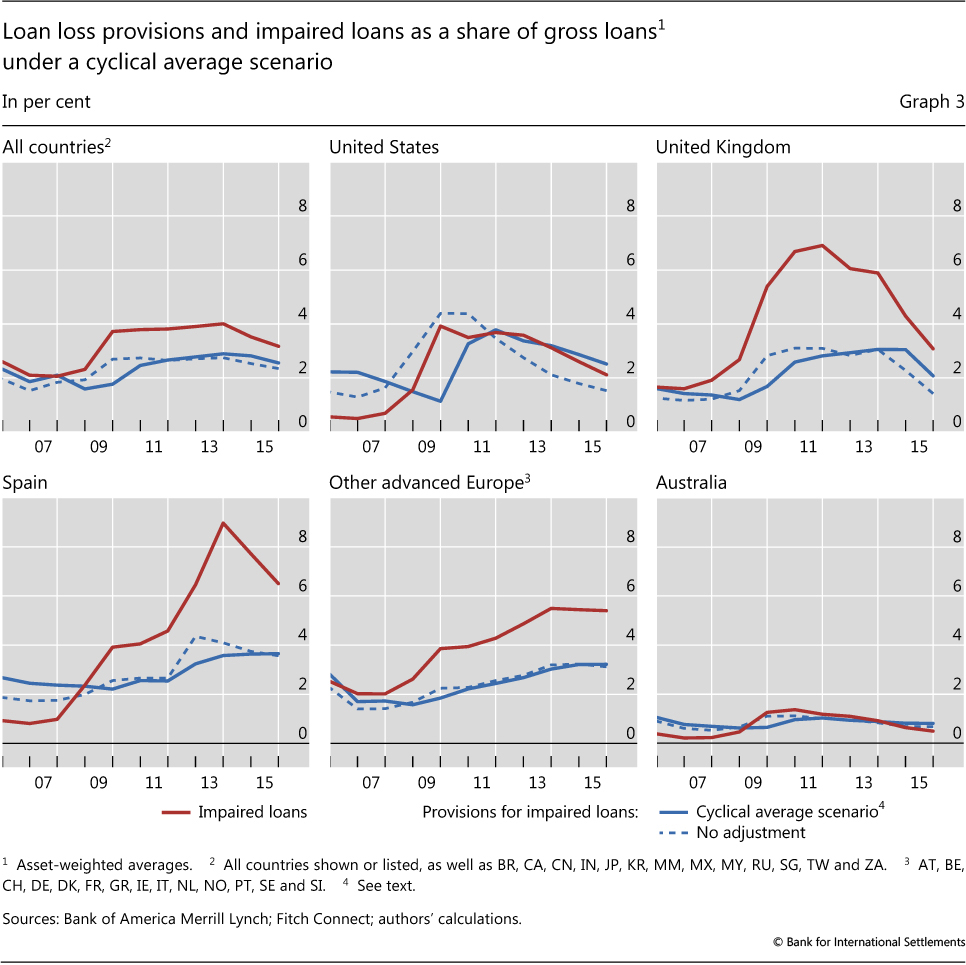

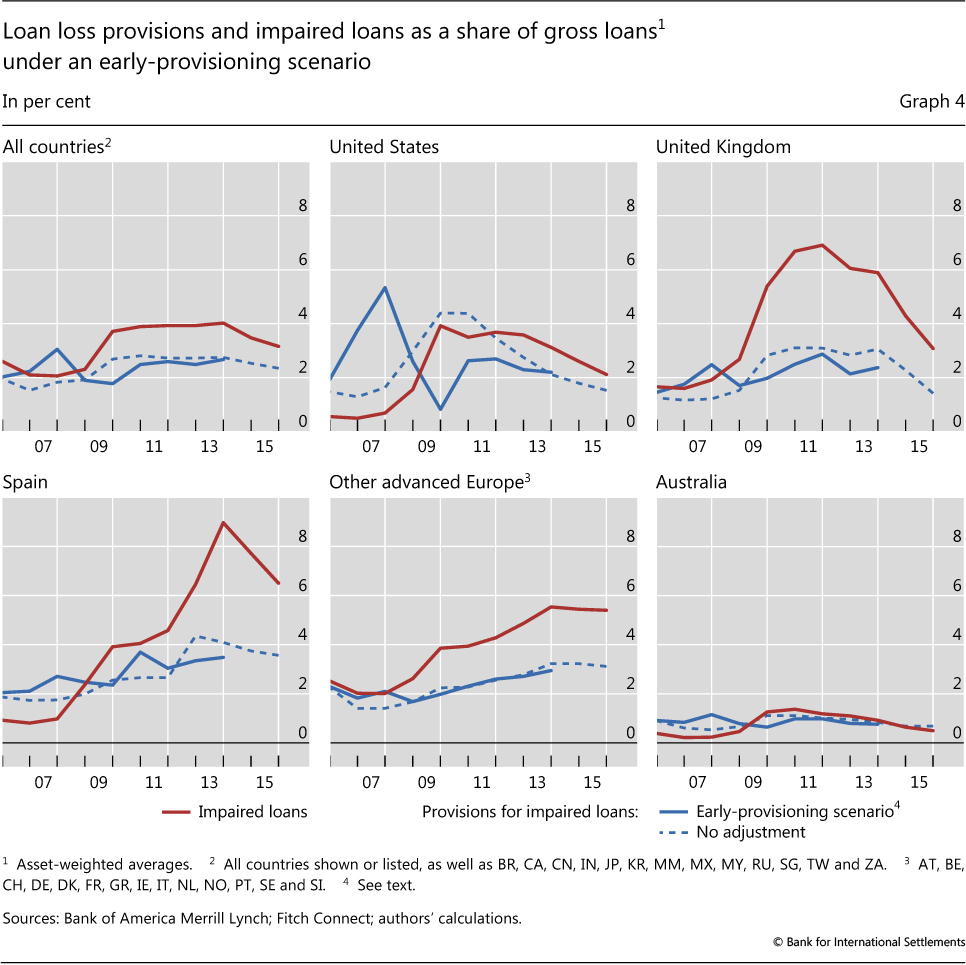

How would the picture have differed if more forward-looking provisioning rules had been in place? Graphs 3 and 4 illustrate the outcomes of two exercises that attempt, imperfectly, to answer this question.

In Graph 3, we develop a "cyclical average" scenario. For each bank in our sample, we have calculated the average amount of provisions taken each year, as a share of loan growth, and we have then augmented (or reduced) each year's level of provisions by the difference between this average and those made in a given year. Thus, the annual impairment charge is reduced in years when provisions were high (namely those in the immediate aftermath of the crisis) and increased in years when provisions were low (namely the years preceding and well after the crisis). This is intended to produce a provisioning series resembling one that would have occurred had provisions been based on modelled ECL, where the behaviour of credit losses throughout the business cycle is accounted for in the relevant model.

The outcome is a revised series of provisions (blue lines in Graph 3). Loan loss provisions would have increased substantially ahead of the crisis for key countries under this scenario: for the US banks, for example, they would have risen from 1.3% of gross loans in 2006 to 2.2% - not a large increase, but a material one. Provisions under this scenario would have fallen from 4.4% of gross loans in 2009 to 1.1% of gross loans, possibly reducing the post-crisis "credit crunch". For the European banks, provisions would have risen from 1.4% to 1.7% before the crisis, and would have fallen by a relatively small amount during the crisis years of 2008-09 and 2011-12.

A second scenario is illustrated in Graph 4. Here we have simply assumed that banks took provisions (as a share of gross loans) two years earlier than they did. The outcome is similar to the first exercise. For US banks, provisions rise even more sharply than in our "cyclical average" experiment, rising to 3.8% in 2006, corresponding to the sharp rise in provisions that instead took place immediately after the crisis. For other countries and regions, the impact is more muted.

The increased provisions likely would have resulted in lower lending ahead of the crisis. A number of studies (Bernanke and Lown (1991), Gambacorta and Shin (2016), Kishan and Opiela (2000, 2006), Cohen and Scatigna (2016)) have established that bank capitalisation has a significant impact on lending behaviour, suggesting that, to the extent that the provisions were taken out of capital, this would have dampened subsequent lending. The size of the estimated effect varies; a 1 percentage point increase in the common equity-to-assets ratio has been associated with subsequent increases in lending growth of 0.6% (Gambacorta and Shin (2016)) to 0.9% (Cohen and Scatigna (2016)).25 Beatty and Liao (2011) find an impact of 0.4% during economic expansions, rising to 1.1% during recessions, with the effects varying by bank size. A more rigorous analysis would be needed to understand how our scenarios for changed provisioning behaviour would have translated into changes in credit.

Both of these scenarios, of course, assume an unusually strong capacity for foresight among banks, almost all of which were caught unaware by the size of loan losses during the crisis. But the exercises illustrate how relatively small shifts in the timing of provisions can have a significant impact on the capacity of banks to absorb losses in crisis episodes, and can affect patterns of loan growth both before and after financial crises.

Conclusions

The new ECL provisioning standards are intended to induce a major change in how banks approach and manage credit risk. While provisions may increase significantly for some banks, the regulatory capital impacts in the transition to the new regime appear likely to be relatively limited (and may be further dampened by supervisors). In future, banks will be asked to examine the nature, likelihood and timing of the risks embedded in their lending decisions, and to reflect this assessment in their financial statements as soon as a loan is made. If this assessment is performed appropriately and with the full range of future risks in mind, this should reduce the procyclicality of the financial system.

The effectiveness of the new standards will depend not only on how banks implement them, but also on the contributions of central banks, supervisors and other stakeholders.26 Based on their experience during financial crises, central banks and banking supervisors have a strong interest in promoting the use of sound credit risk and provisioning practices by banks. Supervisors also expect banks to provide useful public disclosures about credit risk exposures, credit risk management, provisioning and related matters to bring about a higher degree of transparency that facilitates market discipline and promotes market confidence.27 Central banks and other prudential authorities can also play a very important role in promoting sound bank implementation practices through their banking supervisory activities in a manner that complements the efforts of accounting standard setters.28

At the same time, it will be necessary to consider how to achieve important transparency goals and prudential objectives while also reducing the regulatory burden associated with ECL provisioning. At a time when the BCBS has been exploring ways to reduce undue dependence on models in the capital adequacy framework, ECL standards may require more use of models for accounting purposes.29 The IASB, supervisors, banks and auditors should explore how to achieve the transparency principles underlying IFRS 9 and the robust credit risk management and provisioning practices desired by the BCBS, while at the same time reducing any unnecessary burden on banks, including smaller institutions.

The role of auditors will also be critical. Authorities can encourage auditors to achieve a greater understanding of IFRS 9 as well as related implementation efforts and supervisory guidance. Supervisors should gain a better understanding of auditor roles, meeting with them when appropriate. This could be helpful in encouraging an improvement in the quality of bank auditor practices.30

For these important stakeholders to perform their roles, the new provisioning frameworks will need to be fully assimilated and understood. Models will need to be validated and regularly reviewed. Complex data will need to be compiled and maintained. Disclosure practices will need to reinforce prudent risk measurement and management through market discipline. Survey results indicate a need for central banks and other prudential authorities to become more active in encouraging banks to devote more resources to implement ECL provisioning requirements in a more robust, consistent and transparent manner. New, forward-looking thinking will be needed for a new era.

References

Agénor, P-R and L Pereira da Silva (2016): "Reserve requirements and loan loss provisions as countercyclical macroprudential instruments: A perspective from Latin America", Inter-American Development Bank Policy Brief, no IDB-PB-250, February.

Barclays (2017): "European banks: IFRS9 - bigger than Basel IV", 9 January.

Basel Committee on Banking Supervision (2012): "The internal audit function in banks", June.

--- (2014): "External audits of banks", March.

--- (2015): "Guidance on credit risk and accounting for expected credit losses", December.

--- (2016a): "Reducing variation in credit risk-weighted assets - constraints on the use of internal model approaches", March.

--- (2016b): "Basel III monitoring report", September.

--- (2016c): "Regulatory treatment of accounting provisions", October.

--- (2016d): "Regulatory treatment of accounting provisions - interim approach and transitional arrangements", October.

Beatty, A and S Liao (2011): "Do delays in expected loss recognition affect banks' willingness to lend?", Journal of Accounting and Economics, vol 52, pp 1-20.

Bernanke, B and C Lown (1991): "The credit crunch", Brookings Papers on Economic Activity, no 2, pp 205-39.

Borio, C and P Lowe (2001): "To provision or not to provision", BIS Quarterly Review, September, pp 36-48.

Bushman, R and C Williams (2012): "Accounting discretion, loan loss provisioning, and discipline of banks' risk-taking", Journal of Accounting and Economics, vol 54, pp 1-18.

Cohen, B and M Scatigna (2016): "Banks and capital requirements: channels of adjustment", Journal of Banking and Finance, vol 69, supp 1, pp S56-S69.

Deloitte (2016): "Sixth global IFRS banking survey: no time like the present", May.

Dugan, J (2009): "Loan loss provisioning and pro-cyclicality", remarks by John C Dugan, Comptroller of the Currency, before the Institute of International Bankers, 2 March, Washington DC.

Edwards, G (2014): "The upcoming new era of expected loss provisioning", SEACEN Financial Stability Journal, vol 2, May.

--- (2016): "Supervisors' key roles as banks implement expected credit loss provisioning", SEACEN Financial Stability Journal, vol 7, December.

Enhanced Disclosure Task Force (2012): "Enhancing the risk disclosures of banks".

--- (2015): "Impact of expected credit loss approaches on bank risk disclosures", November.

Ernst & Young (2016): "EY IFRS 9 impairment banking survey".

European Banking Authority (2016): "Report on results from the EBA impact assessment of IFRS 9", November.

European Central Bank (2016): "Draft guidance to banks on non-performing loans", September, Annex 7.

Financial Accounting Standards Board (2016): "Accounting Standards Update No. 2016-13, Financial Instruments-Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments", June.

Financial Stability Forum (2009): "Report of the Financial Stability Forum on addressing procyclicality in the financial system", April.

G20 (2009): "London Summit - Leaders' Statement", 2 April.

Gambacorta, L and H S Shin (2016): "Why bank capital matters for monetary policy", BIS Working Papers, no 558, April.

International Accounting Standards Board (2013): "Snapshot: financial instruments: expected credit losses", March.

--- (2014a): "IFRS 9 Financial Instruments", July.

--- (2014b): "Project Summary: IFRS 9 Financial Instruments", July.

International Auditing and Assurance Standards Board (2016): "Project to Revise ISA 540: An Update on the Project and Initial Thinking on the Auditing Challenges Arising from the Adoption of Expected Credit Loss Models", March.

International Forum of Independent Audit Regulators (2016): "Report on 2015 Survey of Inspections Findings", 2016.

International Monetary Fund (2015): "A strategy for resolving Europe's problem loans", Staff Discussion Note, SDN/15/19, September.

Jiménez, G, S Ongena, J-L Peydro and J Saurina (2013): "Macro prudential policy, countercyclical bank capital buffers and credit supply: evidence from the Spanish dynamic provisioning experiments", European Banking Centre Discussion Paper, no 2012-011.

Kishan, R and T Opiela (2000): "Bank size, bank capital, and the bank lending channel", Journal of Money, Credit and Banking, vol 32, pp 121- 41.

--- (2006): "Bank capital and loan asymmetry in the transmission of monetary policy", Journal of Banking and Finance, vol 30, pp 249-85.

Laeven, L and G Majnoni (2003). "Loan loss provisioning and economic slowdowns: too much, too late?", Journal of Financial Intermediation, vol 12, pp 178-97.

Peek, J and E Rosengren (1995): "The capital crunch: neither a borrower nor a lender be", Journal of Money, Credit and Banking, vol 27, pp 625-38.

PricewaterhouseCoopers UK (2016): "IFRS 9: Impairment - global banking industry benchmark", May.

Saurina, J and C Trucharte (2017): The countercyclical provisions of the Banco de España, forthcoming.

1 Benjamin H Cohen is Head of Financial Markets, BIS. Gerald A Edwards Jr is Chairman and CEO, JaeBre Dynamics. Formerly, he held the positions of Senior Advisor, FSB and BCBS Accounting Task Force, and Associate Director and Chief Accountant, US Federal Reserve Board. The views expressed in this article are those of the authors and do not necessarily reflect those of the BIS. We are grateful to Claudio Borio, Pablo Pérez and Hyun Song Shin for comments and to Alan Villegas for excellent research assistance.

2 IASB (2014a): IFRS 9 also includes new rules for classification and measurement of financial instruments and hedge accounting.

3 FASB (2016): the FASB standard refers to its new provisioning approach as being based on "current expected credit losses" or "CECL".

4 See Edwards (2014), who addressed key efforts of the G20, Financial Stability Board (FSB and its predecessor, the Financial Stability Forum, or FSF) and the BCBS to encourage the development of these new standards, summarised the IASB and FASB approaches (and why convergence was not achieved) and explored their potential impacts and implementation challenges before IFRS 9 was published.

5 IASB standards are known as the International Financial Reporting Standards (IFRS).

6 See Saurina and Trucharte (2017) for a review of the Spanish experience with statistical provisioning. In some other jurisdictions using IFRS standards, supervisors expected banks to use statistical provisioning approaches (Agénor and Pereira da Silva (2016)).

7 Financial Stability Forum (2009).

8 G20 Leaders (2009).

9 To be clear, the IASB and FASB published their standards because they believe their ECL approaches would provide better information for investors about credit losses; they did not seek to address procylicality issues. But, as the FSF noted, the earlier recognition of ECL should nonetheless help to mitigate procyclicality.

10 IFRS 9 applies the same impairment approach to all financial assets that are subject to impairment accounting, thus removing a source of current complexity. All banks and other companies that hold financial assets or commitments to extend credit that are not accounted for at fair value through profit or loss (eg trading portfolios) would be affected by IFRS 9's impairment rules. This includes trade receivables and lease receivables, loan commitments and financial guarantee contracts, and loans and other financial assets measured at amortised cost or that are reported at "fair value through other comprehensive income" (such as available-for-sale assets).

11 IASB (2014b).

12 Since lifetime ECL consider the amount and timing of payments, a credit loss (ie a cash shortfall) arises even if the bank expects to be paid in full but later than due.

13 IFRS 9 has a presumption that the credit risk on a financial asset has increased significantly since initial recognition when contractual payments are 30 days or more past due. While this 30-day threshold is not necessarily an absolute indicator for increased credit risk, it is presumed to be the latest point at which lifetime ECL should be recognised through a shift to Stage 2 or Stage 3.

14 Under the cash basis method, a bank would not accrue interest income for a non-performing loan but would instead record income only for interest payments received in cash from the borrower. Under the cost recovery method, typically all payments received by the bank would be applied to reduce the principal on the loan and, only after that has been fully repaid, would any further payments be reflected as interest income.

15 IFRS 9 also includes more extensive guidance on write-offs than IAS 39 by requiring write-offs when the bank has no reasonable expectation of recovering a financial asset in its entirety or a portion thereof (and related disclosures), although it does not specify the number of days past due or other information often considered by banks as a basis for loan write-offs. Generally, the FASB CECL standard allows bank write-offs to continue to be made under banking practices for writing off uncollectible loans - practices that have been shaped in large part by US supervisory guidance and practice.

16 For example, IMF (2015).

17 European Central Bank (2016).

18 BCBS (2015).

19 Under both IASB and FASB ECL standards, the use of a PD/LGD method to measure ECL is not required and other methods can be used (eg a loss rate method).

20 Deloitte (2016).

21 PricewaterhouseCoopers UK (2016).

22 European Banking Authority (2016).

23 Ernst & Young (2016).

24 The graph shows ratios for a sample of roughly 100 large global banks from both advanced and emerging market economies, weighted by total assets. The sample was confined to institutions with more than $150 billion in total assets and where loans were at least 20% of assets.

25 More precisely, Cohen and Scatigna (2016) find that a 1 percentage point higher capital ratio for banks in their sample at end-2009 was associated with 2.83 percentage points faster asset growth over the subsequent three years.

26 For a more extensive discussion of how central banks and other prudential authorities can encourage robust implementation practices, see Edwards (2016).

27 BCBS (2015).

28 These supervisory activities focus on encouraging sound implementation practices and not on developing accounting standards or interpretations. As such, they do not infringe on the roles and independence of accounting standard setters. In our experience, such carefully developed, sound activities focusing on enhanced practices are appreciated by accounting standard setters and securities regulators.

29 For example, a recent consultative document sets out the BCBS's proposed changes to the advanced internal ratings-based approach and the foundation internal ratings-based approach. The proposed changes envisage complementary measures, including the elimination of certain model-based approaches, that aim to (i) reduce the complexity of the regulatory framework and improve comparability; and (ii) address excessive variability in the capital requirements for credit risk (BCBS (2016a)).

30 It is very important that auditors understand the accounting requirements and supervisory guidance, and that supervisors fully understand the role auditors play when determining whether they should "rely" on their work, in whole or in part. Key publications of the international audit standard setter (IAASB (2016)), the Basel Committee (BCBS (2012, 2014)) and the International Forum of Independent Audit Regulators (IFIAR (2016)) could help supervisors and auditors address these issues and promote improved auditor practices in this area.