Volatility and evaporating liquidity during the bund tantrum

(Extract from pages 10-11 of BIS Quarterly Review, September 2015)

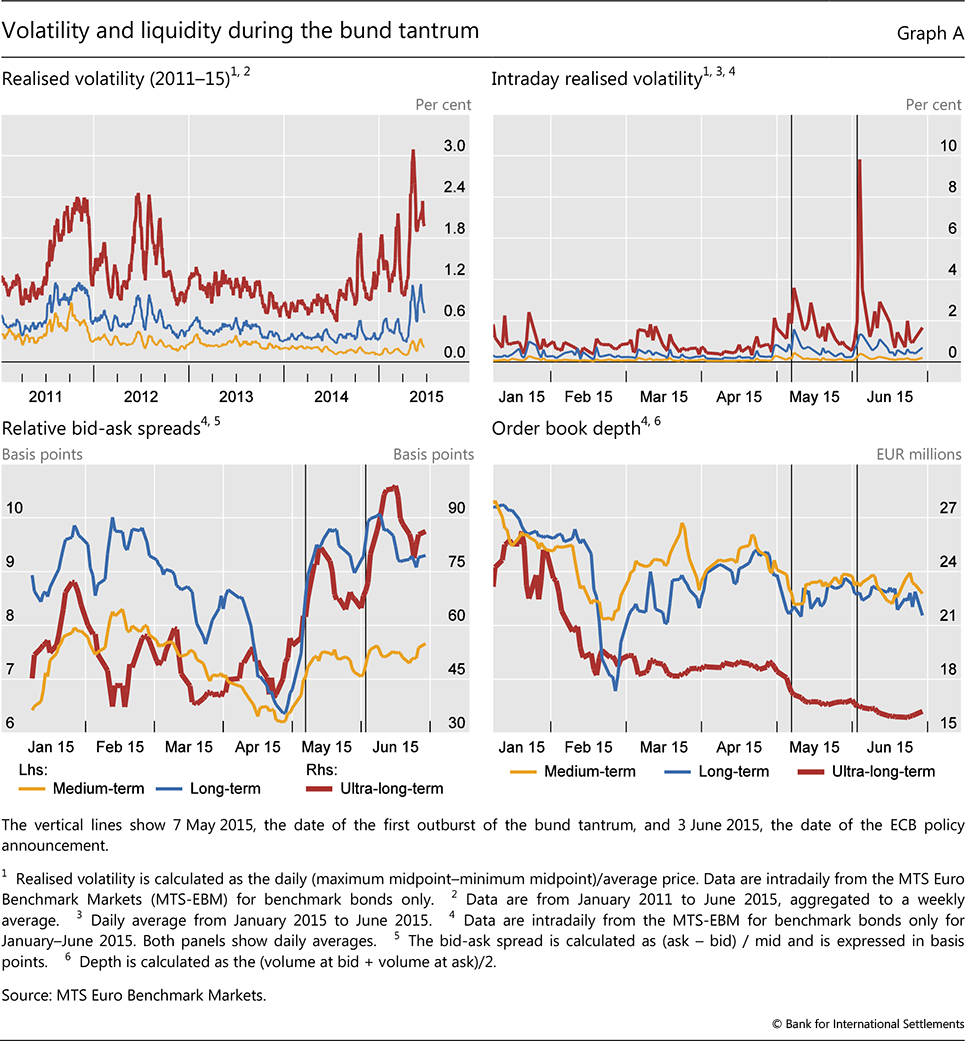

Volatility in German bond markets spiked during May-June 2015 (Graph A, top left-hand panel). Historical volatility, computed from daily maximum and minimum prices, was higher in June 2015 than during any other period over the past four years. Intraday volatility measures indicate even higher stress levels (Graph A, top right-hand panel). Bonds with very long maturities showed the highest intraday volatility, while bonds of shorter maturities were also affected, but to a lesser extent.

Bonds with very long maturities showed the highest intraday volatility, while bonds of shorter maturities were also affected, but to a lesser extent. Intraday data are taken from the Euro-MTS inter-dealer platform, the main wholesale electronic trading venue for German government bonds.

Intraday data are taken from the Euro-MTS inter-dealer platform, the main wholesale electronic trading venue for German government bonds.

The "bund tantrum", as some have termed the spike in German bond volatility on 7 May 2015, is especially puzzling. Yields on long-term bonds surged 21 basis points intraday, peaking at 80 basis points, but ended the day where they had been at the previous day's close, at 59 basis points. While the dynamics differed, such large intraday moves bore some resemblance to the US Treasury "flash rally" on 15 October 2014, during which yields suddenly fell by nearly 30 basis points before recovering by the close of trading. Unlike the 3 June spike in bund yields, which followed the release of an ECB statement on the euro area economic outlook and led to a repricing of inflation expectations, the market break on 7 May does not appear to have been related to the release of any particular information. One trigger factor might have been an unwinding of positions by leveraged directional investors in fixed income derivatives markets. In anticipation of the ECB's asset purchase programme, trades speculating on a continued decline in rates had become relatively crowded, according to some reports. In such circumstances, even minor news might have sufficed to turn the market's direction.

A common explanation for why prices in fixed income markets have become so volatile is that market liquidity has deteriorated. Indeed, measures of market liquidity computed using firm prices that are immediately executable support the conjecture that strained market liquidity conditions are at least partly to blame for the increased volatility.

Indeed, measures of market liquidity computed using firm prices that are immediately executable support the conjecture that strained market liquidity conditions are at least partly to blame for the increased volatility. The cost of immediately executable transactions in the bund market increased in the period around the bund tantrum. The increase in the bid-ask spread (Graph A, bottom left-hand panel), defined as the difference between the best available buy price (bid) and the best available sale price (offer) and expressed in basis points relative to the mid-quote, shows the increase in round-trip execution costs for small trades. Ultra-long-term bonds (those with more than 12½ years' remaining maturity) exhibited the worst deterioration in bid-ask spreads, with a near doubling in the relative bid-ask spread from 40 to roughly 80 basis points. A second spike coincided with the ECB's monetary policy press release on 3 June 2015. Some widening in bid-ask spreads around the release of pricing-relevant information is expected, as intermediaries widen quoted prices to reflect the increased risk that the market will move against them.

The cost of immediately executable transactions in the bund market increased in the period around the bund tantrum. The increase in the bid-ask spread (Graph A, bottom left-hand panel), defined as the difference between the best available buy price (bid) and the best available sale price (offer) and expressed in basis points relative to the mid-quote, shows the increase in round-trip execution costs for small trades. Ultra-long-term bonds (those with more than 12½ years' remaining maturity) exhibited the worst deterioration in bid-ask spreads, with a near doubling in the relative bid-ask spread from 40 to roughly 80 basis points. A second spike coincided with the ECB's monetary policy press release on 3 June 2015. Some widening in bid-ask spreads around the release of pricing-relevant information is expected, as intermediaries widen quoted prices to reflect the increased risk that the market will move against them.

A more informative liquidity measure in this market is order book depth (Graph A, bottom right-hand panel), which also showed signs of deterioration over the period. Order book depth is defined as the total volume available for immediate transaction at the best available bid and offer prices. Lower order book depth means that even small increases in trading volume can lead to large price swings. Over the first half of 2015, depth in the order book of German bunds was low and fragile, which can potentially amplify price movements. The most striking decline was in the depth available in ultra-long-term bonds. Immediately executable depth fell by more than a third over the six-month period, from €25 million to roughly €16 million. Less depth makes it difficult to execute larger trades without moving prices; large trades may then lead to volatility spikes similar to those of May-June 2015.

A variety of factors may stand behind the overall decrease in market liquidity for German bonds. As part of a longer-term trend, liquidity has declined as intermediaries scale down their inventory holdings of fixed income assets (see eg Committee on the Global Financial System, "Market-making and proprietary trading: industry trends, drivers and policy implications", CGFS Papers, no 52, November 2014). Some observers have also suggested that the ECB's Public Sector Purchase Programme (PSPP) in early 2015 may have further reduced the supply of tradable German bonds, which had already been fairly strained due to low issuance volumes in primary markets. As of 30 June, the ECB had purchased €46.3 billion of German bonds, representing roughly 6% of total German PSPP-eligible securities. This, in turn, reduced the availability of bonds for trading by intermediaries.

As of 30 June, the ECB had purchased €46.3 billion of German bonds, representing roughly 6% of total German PSPP-eligible securities. This, in turn, reduced the availability of bonds for trading by intermediaries. In particular, the depth available in German bond markets appears to have fallen around the time of the announcement, and it continued to fall at and after the start of the PSPP. However, the effects were most pronounced, and appear to be permanent, in bonds of very long-term maturity. As the ECB's PSPP did not buy large amounts of these securities, other factors such as the limited risk-bearing capacity of intermediaries may also have contributed to the decline.

In particular, the depth available in German bond markets appears to have fallen around the time of the announcement, and it continued to fall at and after the start of the PSPP. However, the effects were most pronounced, and appear to be permanent, in bonds of very long-term maturity. As the ECB's PSPP did not buy large amounts of these securities, other factors such as the limited risk-bearing capacity of intermediaries may also have contributed to the decline.

Indicators are constructed from submitted limit orders for benchmark bonds during normal trading hours (8:00-17:30). Bonds with a remaining maturity from 2.5 to 7.5 years are classified as medium-term, those >7.5 to <= 12.5 years as long-term, and those >12.5 years as ultra-long-term bonds. Market liquidity generally refers to the ease with which a security can be bought or sold without affecting the asset's price. This differs from funding liquidity, which refers to the ease with which investors can obtain funding for a position in a risky asset (see M Brunnermeier and L Pedersen, "Market liquidity and funding liquidity", Review of Financial Studies, no 22(6), 2009, pp 2201-38). The two measures of liquidity discussed here, the bid-ask spread and order book depth at the best bid and ask, are directly measurable in our data and are continuously available throughout the trading day. They are representative of realisable liquidity in the overall market. On 22 January 2015, the ECB unveiled its programme for public sector asset purchases (PSPP), amounting to purchases worth roughly €60 billion per month between 9 March and end-June 2016. The weighted average remaining maturity of German bonds held by the ECB in the PSPP is roughly 6.78 years; see www.ecb.europa.eu/mopo/implement/omt/html/index.en.html.