Emerging market benchmarks

(Extract from pages 28-29 of BIS Quarterly Review, September 2014)

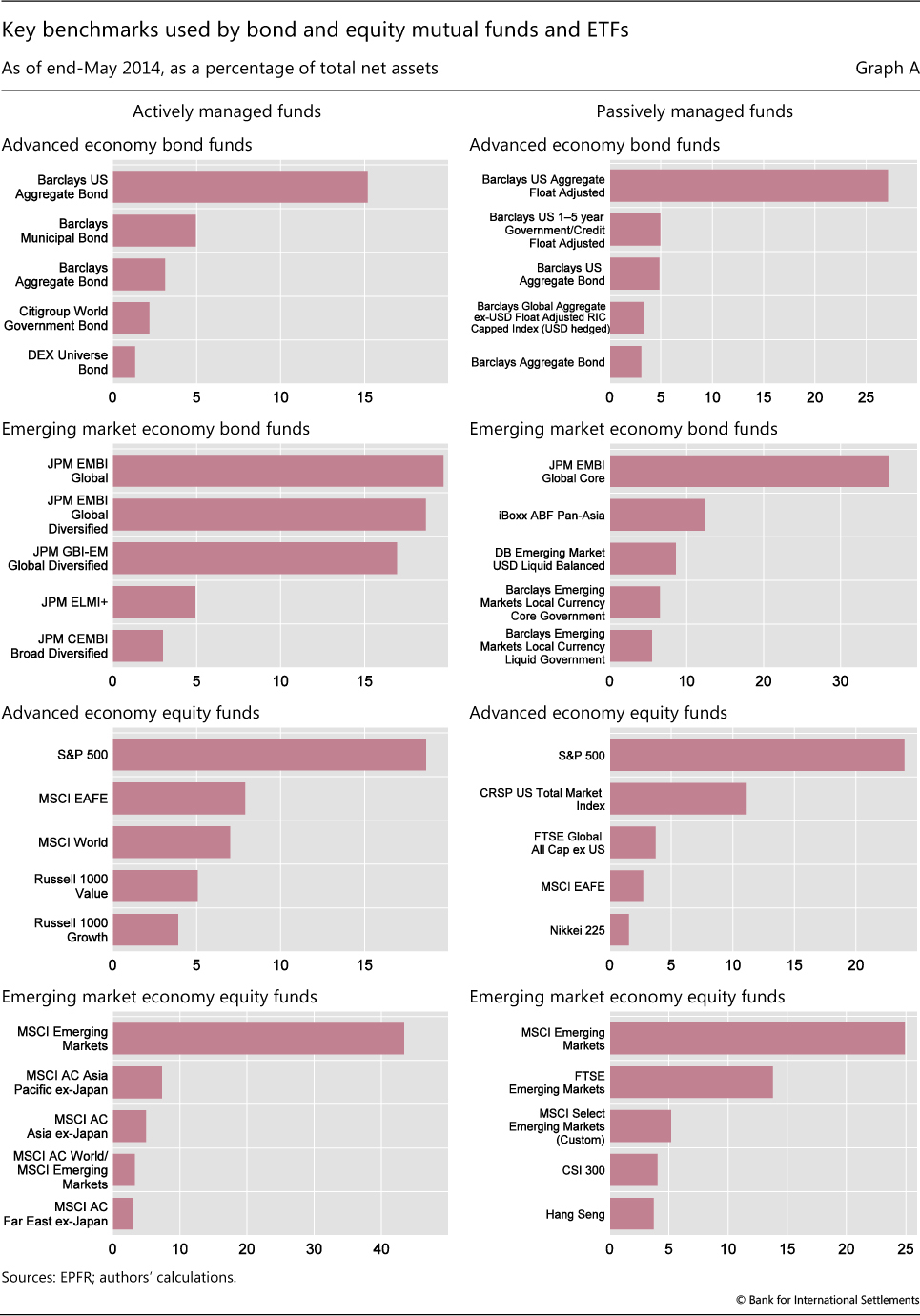

To measure concentration in the use of benchmarks of EME asset funds, we identify a benchmark index adopted by each fund and then aggregate the AUM of all funds using the index. Graph A shows that EME equity and bond funds are more concentrated than their AE counterparts in their use of benchmarks. For example, two JPMorgan EMBI Global indices are used for 38% of the total AUM of actively managed EME bond funds in the EPFR database, while two Barclays Capital bond indices are used for 20% of the total AUM of actively managed AE bond funds.

Given the wide use of a small number of benchmark indices, their construction and composition are crucial. Major indices have been created by broker-dealers. Indices such as Morgan Stanley's MSCI equity indices, JPMorgan Chase's EMBI and GBI bond indices and Barclays Capital's bond indices are typically constructed on the basis of tradability, liquidity, credit rating and valuation criteria. Under these criteria, an issuer with a larger amount of marketable securities receives a larger index weight. Other weighting schemes are also used. For example, Barclays Capital offers bond indices that weight countries by GDP or fiscal strength.

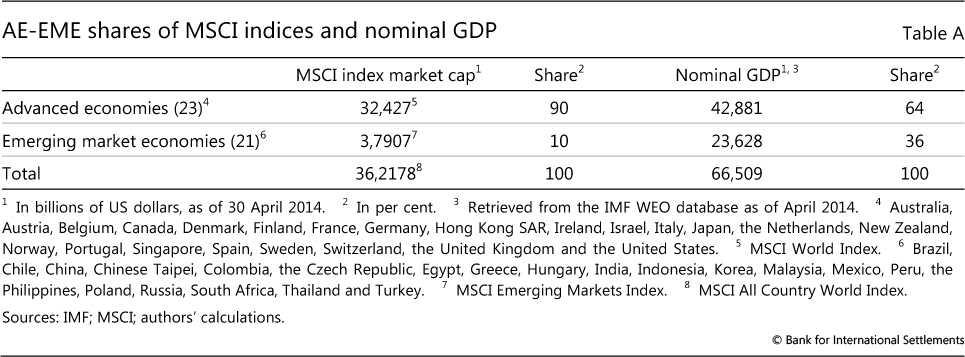

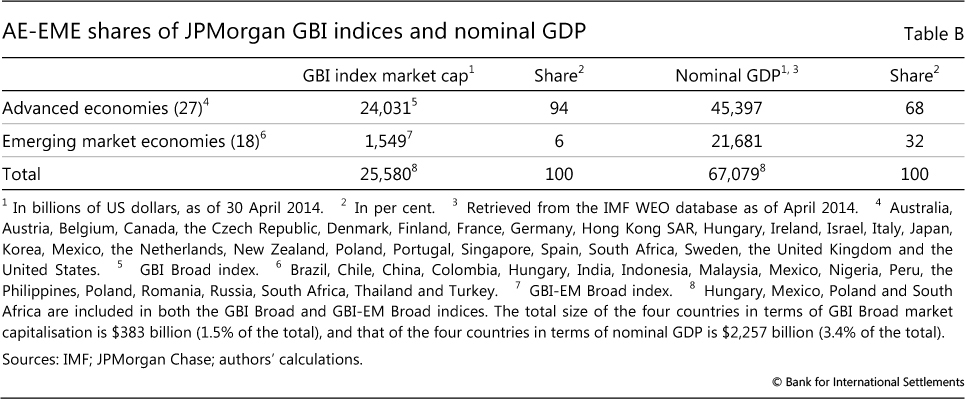

As an illustration, the EME share in the global equity and bond indices is much smaller than their GDP share. In particular, in the MSCI All Country World Index (ACWI), which includes 23 major AEs and 21 major EMEs, the EME share is 10%. This contrasts with the GDP share of 36% of the same 21 EMEs out of the total GDP of the 44 economies (Table A). The same is true for the JPMorgan GBI Broad index for 27 AEs and the JPMorgan GBI-EM Broad index for 18 EMEs. When we combine these two indices, the EME share is 6%, while their GDP share is 32% (Table B).

Recently, index providers have become progressively more independent. As an example, for the Markit iBoxx ABF indices, Markit collects prices from multiple sources, controls for quality and then computes an average of the price on a daily basis. Moreover, in October 2012, the market weights of the Markit iBoxx ABF indices were adjusted to consider the following three factors: local bond market size (20%), sovereign local debt rating (20%) and the GEMLOC Investability Indicator (60%). In July 2010, Pacific Investment Management Company (PIMCO) also launched two GDP-weighted sovereign bond indices (PIMCO Global Advantage Government Bond Index and European Advantage Government Bond Index) using the individual Markit country components.

In July 2010, Pacific Investment Management Company (PIMCO) also launched two GDP-weighted sovereign bond indices (PIMCO Global Advantage Government Bond Index and European Advantage Government Bond Index) using the individual Markit country components.

The GEMLOC Investability Indicator is a measure of accessibility to foreign investors based on a methodology developed by the World Bank. The indicator scores a market on a set of 14 subfactors that are aggregated to the overall score.