Currency trading gets more financial

(Extract from page 25 of BIS Quarterly Review, December 2013)

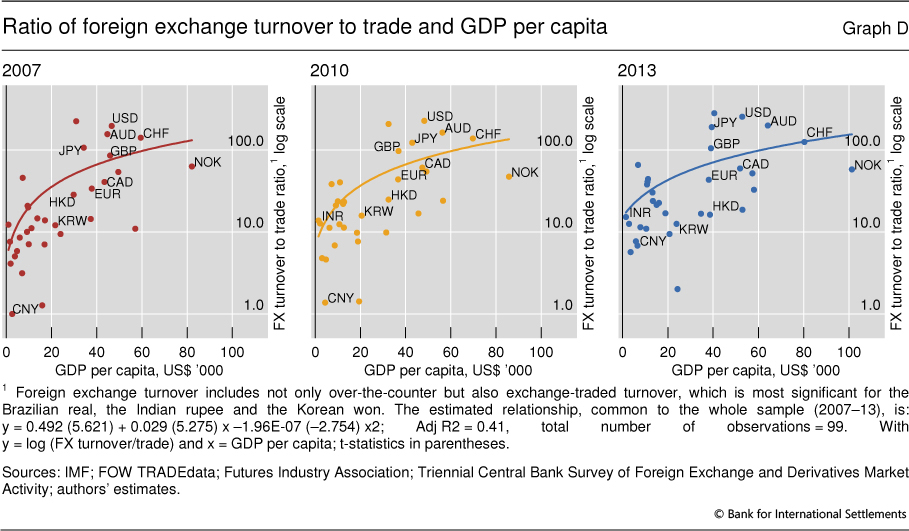

The Triennial Central Bank Survey in both 2007 and 2010 suggested that foreign exchange turnover in relation to a country's underlying trade grows with national income. In particular, as income per capita rises, currency turnover as a ratio of current account transactions of the home country rises from one to 10 times to a hundred or more (Graph D, left-hand and centre panels). In effect, with higher income, currencies become less connected to the real economy and more related to the financial economy. Estimated separately on the 2007 and 2010 data, the curvilinear regression lines ("Kuznets curves") were remarkably similar. As economies develop and GDP per capita rises, this ratio rises and the balance shifts from trade-related to financial transactions in a very predictable fashion.

In particular, as income per capita rises, currency turnover as a ratio of current account transactions of the home country rises from one to 10 times to a hundred or more (Graph D, left-hand and centre panels). In effect, with higher income, currencies become less connected to the real economy and more related to the financial economy. Estimated separately on the 2007 and 2010 data, the curvilinear regression lines ("Kuznets curves") were remarkably similar. As economies develop and GDP per capita rises, this ratio rises and the balance shifts from trade-related to financial transactions in a very predictable fashion.

The 2013 data again show the same relationship between national income and the balance between trade-related and financial transactions (Graph D, right-hand panel). Statistical tests do not support the hypothesis that the relationship has changed over time.

In terms of goodness of fit, the relationship is quite tight. In 2013, burgeoning renminbi trading strengthened an already strong relationship, while the blip in yen turnover temporarily weakened it (see "The anatomy of the global FX market through the lens of the 2013 Triennial Survey" in this issue). Taking the three years' observations together, the simple curvilinear model accounts for two fifths of the variance.

Robert N McCauley and Michela Scatigna, "Foreign exchange trading in emerging currencies: more financial, more offshore", BIS Quarterly Review, March 2011, pp 67-75.