Who is issuing international bonds denominated in emerging market currencies?

(Extract from pages 22-23 of BIS Quarterly Review, December 2013)

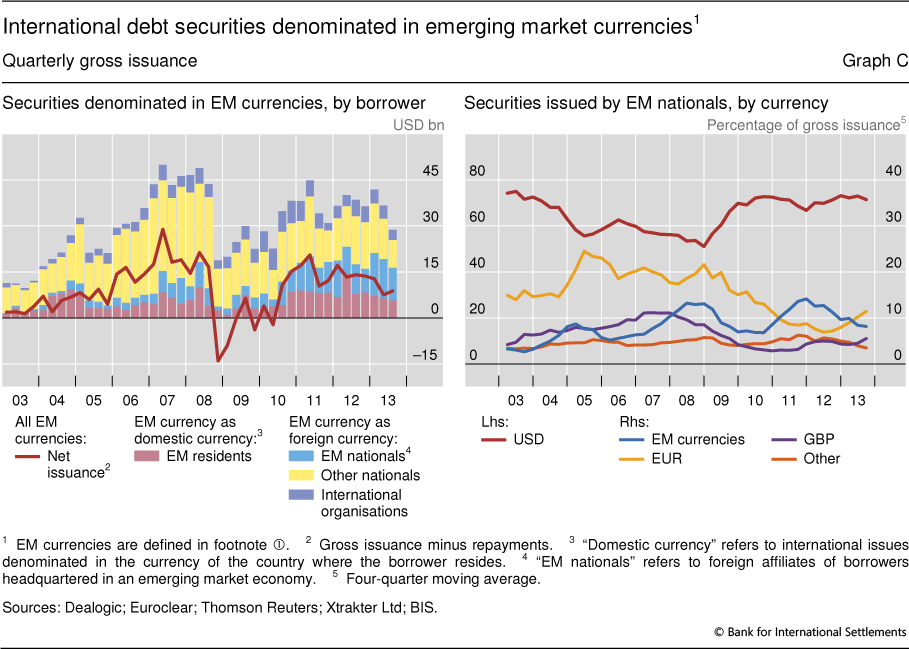

In recent quarters investor demand for higher-yielding assets has supported robust issuance of international debt securities denominated in emerging market (EM) currencies. In January-September 2013, gross issuance of such securities totalled $107 billion, down slightly from $115 billion during the same period in 2012. On a net basis, ie after adjusting for repayments, issuance in January-September 2013 was concentrated in the Brazilian real, Chinese renminbi and Mexican peso. While increased volatility in global financial markets in mid-2013 contributed to a slowdown in the issuance of EM currency-denominated international debt securities in the third quarter, new placements remained well above the lows seen in 2008-10 (Graph C, left-hand panel).

In January-September 2013, gross issuance of such securities totalled $107 billion, down slightly from $115 billion during the same period in 2012. On a net basis, ie after adjusting for repayments, issuance in January-September 2013 was concentrated in the Brazilian real, Chinese renminbi and Mexican peso. While increased volatility in global financial markets in mid-2013 contributed to a slowdown in the issuance of EM currency-denominated international debt securities in the third quarter, new placements remained well above the lows seen in 2008-10 (Graph C, left-hand panel).

Recent international issuance in EM currencies was boosted by EM companies, especially their affiliates based abroad. The BIS international debt securities statistics capture issuance outside the market where the borrower resides - offshore issuance - regardless of the currency. Borrowers resident in an emerging market who issue offshore in their domestic currency have accounted for only a small share of EM currency-denominated issuance in international markets: 18% in 2013, equal to the average for the 2003-12 period (Graph C, left-hand panel). But if the nationality of issuers is considered, then there has been a marked change in the importance of EM borrowers. Companies headquartered in an emerging market but residing outside that market - shown in the left-hand panel of Graph C as EM nationals issuing in an EM currency as a foreign currency - accounted for 35% of gross international issuance of EM currencies in 2013. This compares to 25% in 2011-12 and only 11% prior to 2011.

Borrowers resident in an emerging market who issue offshore in their domestic currency have accounted for only a small share of EM currency-denominated issuance in international markets: 18% in 2013, equal to the average for the 2003-12 period (Graph C, left-hand panel). But if the nationality of issuers is considered, then there has been a marked change in the importance of EM borrowers. Companies headquartered in an emerging market but residing outside that market - shown in the left-hand panel of Graph C as EM nationals issuing in an EM currency as a foreign currency - accounted for 35% of gross international issuance of EM currencies in 2013. This compares to 25% in 2011-12 and only 11% prior to 2011.

In recent years, Asian firms were the most active EM issuers of international debt securities denominated in EM currencies, followed by Latin American firms. Whereas Brazilian and Mexican firms issuing real- or peso-denominated bonds internationally tend to issue through their head offices, Chinese, Korean and Russian firms often issue through affiliates abroad, including ones based in offshore financial centres. To the extent that the parent company stands ready to offer financial support to its affiliates abroad, analysing borrowing through the lens of nationality rather than residence can provide additional insights about a country's vulnerability to volatility in global financial markets.

To the extent that the parent company stands ready to offer financial support to its affiliates abroad, analysing borrowing through the lens of nationality rather than residence can provide additional insights about a country's vulnerability to volatility in global financial markets.

The increased presence of EM borrowers suggests that the international market for emerging market debt is opening to a wider diversity of borrowers. Historically, international issuance of bonds denominated in EM currencies was dominated by borrowers of high credit quality; international investors tended to prefer to separate the currency risk associated with EM-denominated issues from the credit risk associated with EM borrowers. While borrowers headquartered in advanced economies - "Other nationals" in the left-hand panel of Graph C - remain the most active issuers of international securities denominated in EM currencies, in recent years their share has fallen well below the 55% level of the 2000s, to 38% in 2012 and 36% in 2013. International organisations typically accounted for a further 12%.

The perceived improvement in the credit standing of many EM economies in recent years helps to support investor demand for EM currency-denominated bonds issued by EM companies. Such issuance in turn helps EM companies to reduce currency mismatches in their assets and liabilities.

That said, the US dollar continues to account for the bulk of their international issuance by a large margin. The US dollar's share of new placements by EM nationals has averaged 71% since 2010, well above the 61% share seen in 2003-09 (Graph C, right-hand panel). By comparison, EM currencies have accounted for between 6% and 17% of international issuance by EM-headquartered borrowers since 2010. The euro accounted for about 19% of gross issuance by EM nationals prior to 2009, but its share has since fallen to less than 10%. The euro's share of issuance by borrowers headquartered in central and eastern Europe is higher than that of issuance by borrowers from other regions. Yet even in Europe the US dollar is the currency of choice; since 2009 the US dollar's share of their international issuance has averaged 65%.

For the purpose of this box, EM currencies are defined as any currency other than the following 11: Australian dollar, Canadian dollar, Danish krone, euro (including legacy currencies), Japanese yen, Norwegian krone, New Zealand dollar, Swedish krona, Swiss franc, pound sterling and US dollar. As of end-September 2013, this definition produced a total of 76 currencies denominating one or more issues in the BIS international debt securities statistics. The BIS classifies a debt security as international if any one of the following characteristics is different from the country of residence of the issuer: country where the security is registered, law governing the issue, or market where the issue is listed. See "Enhancements to the BIS debt securities statistics", BIS Quarterly Review, December 2012, pp 63-76. For an explanation of why some borrowers issue through offshore affiliates, see "Emerging market debt securities issuance in offshore centres", BIS Quarterly Review, September 2013, pp 22-3.