A tale of three journeys

Introduction

The global economy has reached a critical and perilous juncture. Policymakers are facing a unique constellation of challenges. Each of them, taken in isolation, is not new; but their combination on a global scale is. On the one hand, central banks have been tightening to bring inflation back under control: prices are rising far too fast. On the other hand, financial vulnerabilities are widespread: debt levels – private and public – are historically high; asset prices, especially those of real estate, are elevated; and risk-taking in financial markets was rife during the phase in which interest rates stayed historically low for unusually long. Indeed, financial stress has already emerged. Each of the two challenges, by itself, would be difficult to tackle; their combination is daunting.

This year's Annual Economic Report explores the global economy's journey and the policy challenges involved. It is, in fact, an exploration of not one but three interwoven journeys: the journey that has taken the global economy to the current juncture; the journey that may lie ahead; and, in the background, the journey that the financial system could make as digitalisation opens up new vistas. Much is at stake. Policymakers will need to work in concert, drawing the right lessons from the past to chart a new path for the future. Along the way, the perennial but elusive search for consistency between fiscal and monetary policy will again take centre stage. Prudential policy will continue to play an essential supporting role. And structural policies will be critical.

What follows considers, in turn, each of the three journeys.

The macroeconomic journey: looking back

How did the global economy fare in the year under review? Even more importantly, what forces shaped its journey?

The year under review

High inflation, surprising resilience in economic activity and the first signs of serious stress in the financial system – this is, in a nutshell, what the year under review had in store.

Inflation continued to hover well above central bank targets across much of the world. Fortunately, there were clear indications that headline inflation was peaking or had started to decline. But core inflation proved more stubborn. The reversal of commodity prices and a marked slowdown in manufacturing prices provided welcome relief even as stickier services prices gathered steam. Several forces were playing out, including easing global supply chain bottlenecks, the post-pandemic rotation of global demand back from manufacturing to services, and the effects of repeated generous fiscal support packages. Labour markets remained very tight, with unemployment rates generally at historical lows.

Global growth did slow, but proved remarkably resilient. The widely feared recession in Europe did not materialise, thanks partly to a mild winter, and China rebounded strongly once Covid restrictions were suddenly lifted. Consumption held up surprisingly well globally, as households continued to draw on savings accumulated during the pandemic and employment remained buoyant. As the year progressed, professional forecasters revised their growth projections upwards, although they still saw slower global growth in the year ahead.

Even as growth held up, signs of serious strains emerged in the financial system. Some milder ones appeared among non-bank financial intermediaries (NBFIs). In October, following the announcement of fiscal measures that undermined policy credibility, the UK government bond market saw a sharp increase in yields and a sudden evaporation of liquidity: leveraged investment vehicles through which pension funds were matching the duration of their liabilities were forced to sell to meet margin calls. Other signs of strain, perhaps more serious and surprising, appeared in the banking sector. A number of regional banks in the United States failed as a result of a combination of losses accumulated on long-maturity, mostly government, securities and lightning runs. And in an environment of fragile confidence, Credit Suisse – a global systemically important bank – went under, as it abruptly lost market access following long-standing concerns about its business model and risk management.

Once again, the strains prompted large-scale official intervention on both sides of the Atlantic to prevent contagion – worryingly, an increasingly familiar picture. Central banks activated or extended liquidity facilities or asset purchases. Where necessary, governments supplied solvency backing, implicitly or explicitly, in the form of guarantees and ultimate support for enlarged deposit insurance schemes. The response restored market calm.

In the meantime, the highly synchronous and forceful monetary policy tightening continued. Central banks across the globe hiked policy rates further. What's more, those that had engaged in large-scale asset purchases began to unwind them: albeit gradually, quantitative easing turned into quantitative tightening. At the same time, policy rates often remained below inflation rates, ie negative in real terms.

In response to the tightening and the economic outlook, financial conditions reacted unevenly. In general, banks tightened credit standards. But financial markets were less responsive. To be sure, on balance, conditions there did tighten compared with those prevailing at the time of the first hike. But in the second half of the year, they loosened somewhat, as bond yields declined and risky asset prices rose. Central banks contended with a disconnect between their communication, which pointed to a more persistent tightening, and financial market participants' views, which saw an easier stance ahead.

The longer-term backdrop

The rather unique combination of high inflation and widespread financial vulnerabilities is not simply a bolt from the blue. To be sure, the pandemic and, to a lesser extent, the war in Ukraine have played an important role in the recent inflation flare-up. But the root causes of the current problems run much deeper. After all, debt and financial fragilities do not appear overnight; they grow slowly over time.

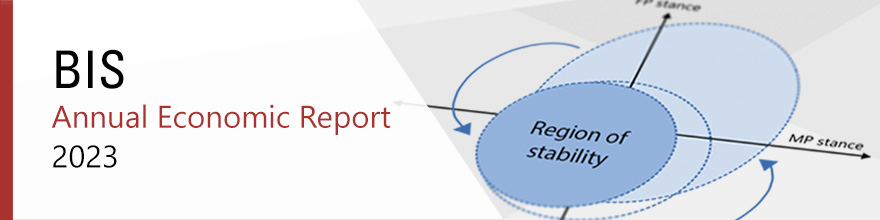

As explored in detail in Chapter II, the combination of high inflation and financial vulnerabilities is probably best seen as reflecting the confluence of two interdependent factors. First, the changing shape of the business cycle. Second, monetary and fiscal policies testing, once again, the boundaries of what might be termed the "region of stability" – the region that maps the constellations of the two policies that foster sustainable macroeconomic and financial stability, keeping the inevitable tensions between the policies manageable. The changing shape of the business cycle determines what kind of symptom signals that the boundaries are being tested – inflation, financial instability or both. The conduct of policy, interacting with structural forces, determines the shape of the business cycle itself.

The mid-1980s represented a watershed in the evolution of the business cycle, at least in advanced economies. Until then, recessions tended to follow a tightening of monetary policy designed to bring inflation under control, while financial stress was absent or largely contained. Thereafter, all the way to the sui generis Covid crisis, recessions were ushered in by financial booms that turned into busts, sometimes triggering widespread financial instability, while inflation remained generally low and stable. Emerging market economies, in turn, were buffeted by the global waves unleashed in advanced economies, most notably in the form of capital flows. Accordingly, regional and country differences aside, exchange rate tensions typically played a bigger role there than in advanced economies.

Two fundamental structural changes contributed to the shift from inflation-induced to financial cycle-induced recessions. Broad-ranging financial liberalisation, both domestically and internationally, provided scope for much larger financial expansions and contractions, no longer suppressed by the tight web of regulations that had greatly constrained the financial system. And the globalisation of the real economy helped central banks hardwire low inflation, by eroding the pricing power of labour and firms. In the process, inflation stopped acting as a reliable barometer of the sustainability of economic expansions: the build-up of financial imbalances took over that role.

Hence an acute policy dilemma. A painful lesson policymakers had drawn from the high-inflation era was that policies which turned out to be overambitious could generate price instability. In the low-inflation era, however, the constraints on economic expansions had seemingly disappeared. The boundaries of the region of stability had become fuzzier, hardly visible in fact. And the fragility of the financial system, not buttressed by a sufficiently incisive effort to strengthen prudential regulation, clouded the picture further. The economy appeared stable until, suddenly, it no longer was. The post-Great Financial Crisis (GFC) experience blurred the boundaries of the region even further. Inflation hovered stubbornly below inflation targets: having helped central banks' efforts, globalisation was now hindering them. And fiscal policy was asked to step up to the plate to ensure that central banks would no longer be the "only game in town", which it did.

By the time the Covid crisis struck, monetary and fiscal policy were testing the boundaries of the region of stability once again. Interest rates had never been so low and in some cases were now negative even in nominal terms. Central bank balance sheets had never been so large except during wars. Government debt in relation to GDP, joining private sector debt, was flirting with previous historical peaks reached around World War II. And yet, because of the exceptionally low interest rates, the debt burden had never felt so light. Low rates as far as the eye could see encouraged further debt expansion, public and private. The forceful and concerted monetary and fiscal response to the Covid crisis took policies one step further towards the boundary.

The remarkable post-pandemic surge in global demand against the backdrop of the supply disruptions did the rest. Against all expectations, inflation had come back with a vengeance. Monetary policy had to tighten, straining public finances and private sector balance sheets. The financial system came under stress. While understandable as the Covid crisis broke out, with the benefit of hindsight, it is now clear that the fiscal and monetary policy support was too large, too broad-based and too long-lasting.

The macroeconomic journey: looking ahead

Given where we are, what does the journey ahead look like? In the near term, it is indeed possible that the global economy will smoothly overcome the obstacles it is facing. This seems to be what financial market participants and professional forecasters are anticipating. Moreover, peering further into the future, the journey could continue without major incidents. That said, both near- and long-term hazards are lurking along the way. And policies will be the deciding factor.

Near- and longer-term hazards

In the near term, two challenges stand out: restoring price stability and managing any financial risks that may materialise.

Inflation could well turn out to be more stubborn than currently anticipated. True, it has been declining, and most forecasters see it moving within target ranges over the next couple of years. Moreover, inflation expectations, albeit hard to measure reliably, have not rung alarm bells. Even so, the last mile could prove harder to travel. The surprising inflation surge has substantially eroded the purchasing power of wages. It would be unreasonable to expect that wage earners would not try to catch up, not least since labour markets remain very tight. In a number of countries, wage demands have been rising, indexation clauses have been gaining ground and signs of more forceful bargaining, including strikes, have emerged. If wages do catch up, the key question will be whether firms absorb the higher costs or pass them on. With firms having rediscovered pricing power, this second possibility should not be underestimated. Our illustrative simulations indicate that, in this scenario, inflation could remain uncomfortably high. As last year's Annual Economic Report documented, transitions from low- to high-inflation regimes tend to be self-reinforcing. And once an inflation psychology sets in, it is hard to dislodge.

At a macroeconomic level, historically high private indebtedness and elevated asset valuations cloud the outlook. They can greatly heighten the sensitivity of private expenditures to higher interest rates, although the lengthening of maturities during the period of low inflation has muted, or at least delayed, the pass-through to debt service burdens, and the savings cushions built during the pandemic have softened the blow. Stylised simulations suggest that the impact could be substantial. In a higher-for-longer scenario, with policy rates reaching a peak 200 basis points above the market-implied one and staying there through 2027, debt service burdens would rise substantially, asset prices would drop markedly and output in a representative sample of economies could be some 2% lower at the end of a simulation horizon. Moreover, one should not rule out outsize responses should debt service burdens reach critical thresholds.

Higher interest rates, a turn in the financial cycle and an economic slowdown would eventually raise credit losses. These, in turn, could generate further strains in the financial system. It is quite common for banking stress to emerge following a monetary policy tightening – in as many as a fifth of cases within three years after the first hike. The incidence rises considerably when initial debt levels are high, real estate prices are elevated or the increase in inflation is stronger. The current episode ticks all the boxes. The stress we have seen so far has reflected exclusively interest rate risk, revealing the fragility of strategies predicated on the view that interest rates would remain low far into the future. The credit leg is still to come. The lag between the two legs can be quite long.

Once the credit leg materialises, the resilience of the financial system will be tested again. Simple simulations indicate that, in the market-implied interest rate scenario, in a representative sample of advanced economies credit losses would be in line with historical averages. But they would be of a similar order of magnitude as during the GFC in the higher-for-longer scenario.

The impact of those losses will depend, critically, on the loss-absorbing capacity of the banking system. Since the GFC, thanks in no small measure to the financial reforms, banks have bolstered their capital. That said, pockets of vulnerability remain. Recent events have shown how the failure of even comparatively small institutions can shake confidence in the overall system. Moreover, the price-to-book ratios of many banks, including large ones, have been languishing far below one. This reflects market scepticism about the underlying valuations and long-term profitability of those institutions. Admittedly, this is not new. But, in an environment of more fragile confidence, it could turn out to be a significant vulnerability.

Before stress emerged among banks, all the attention was focused on the NBFI sector. And with reason. The sector has grown in leaps and bounds since the GFC, and now accounts for over half of all financial assets globally. While, on balance, less leveraged than its banking counterpart, the sector is rife with hidden leverage and liquidity mismatches, especially in the asset management industry. It has been a source of large losses for banks, such as in the Archegos case – which, incidentally, hit Credit Suisse especially hard. And it was at the heart of the March 2020 turmoil, which prompted large-scale central bank interventions. The latest tremors in the UK gilt market are a reminder that attention is still justified.

While it is hard to tell where strains might emerge next, several vulnerabilities stand out. In the corporate sector, private credit markets remain very opaque against the backdrop of a long-term deterioration in credit ratings. In the leveraged loan market, securitised products have grown rapidly. Exposures to commercial real estate are bound to see losses, as the sector is buffeted by powerful cyclical and structural headwinds – losses that could also be a source of stress for banks, as they have been throughout history. In addition, structural weaknesses linger in some government bond markets.

Looking further out, a key source of concern is the sustainability of public debt – an issue analysed in depth in Chapter II. A vulnerable sovereign means a vulnerable financial system. This is because the sovereign can generate financial instability or fail to act as an effective backstop of the financial sector. Central banks can provide liquidity, but only the sovereign can back up solvency. Moreover, the sovereign's creditworthiness depends on the health of the financial sector. Indeed, banking crises have typically caused surges in public debt, in teens of GDP – directly, because of the government support, and indirectly, because of the damage to economic activity. Long-term projections of public debt trajectories are worrisome, even under favourable interest rate and growth configurations (see below).

Near- and longer-term policy challenges

The sheer size of the challenges ahead calls for a holistic policy response, involving monetary, fiscal, prudential and, last but not least, structural policies. Consider, in turn, the near-term and longer-term challenges, although the dividing line between the two is quite fuzzy.

The near term

The priority for monetary policy is to bring inflation back to target. The insidious damage that a high-inflation regime does to the economic and social fabric is well known. The longer inflation is allowed to persist, the greater the likelihood that it becomes entrenched and the bigger the costs of quenching it.

In bringing inflation back to target, central banks face at least three challenges. First, historical statistical relationships provide limited guidance when a transition to a high-inflation regime threatens. Both judgment and more formal models are tested hard. Second, the transmission mechanism of monetary policy is clouded by the exceptional post-pandemic conditions, which add to the well known lags. Hence the pause many central banks have taken to better assess the impact of the tightening so far. Finally, further financial system stress could well emerge. In that case, if the stress is acute enough, addressing it without compromising the fight against inflation will require the active support of other policies, not least prudential and fiscal, to complement central banks' deployment of the range of tools at their disposal. This would contain the damage while allowing monetary policy to keep a restrictive stance for as long as necessary.

The priority for fiscal policy is to consolidate. To be sure, deficits have narrowed somewhat, especially in cyclically adjusted terms. But some of the improvement reflects the temporary impact of the inflation burst, and cyclical adjustments have proved quite misleading in the past, especially before slowdowns. Moreover, from a long-term perspective, deficits remain too high. Consolidation would provide critical support in the inflation fight. It would also reduce the need for monetary policy to keep interest rates higher for longer, thereby reducing the risk of financial instability.

By bolstering the financial system's resilience, prudential policy can also support the inflation fight, as it would increase monetary policy headroom. Macroprudential measures need to be kept tight for as long as possible, or even tightened further where appropriate. Similarly, (microprudential) supervision needs to be stiffened to remedy some of the deficiencies that came to light in recent bank failures. While changes in regulatory standards take longer, a reflection on the recent experience should start without delay; and indeed it has. Examples of issues to be examined are the treatment of interest rate risk, the appropriateness of historical cost accounting, not least for assets used for liquidity management purposes (eg government securities) and assumptions about the stickiness of various deposit categories. But beyond banking, we should not lose sight of the urgent need to strengthen the regulation of NBFIs from a systemic perspective.

The longer term

In the longer term, the challenge is to put in place policies and frameworks that foster a stable financial and macroeconomic environment while strengthening the potential for robust and sustainable growth. As argued in detail in Chapter II, a key element of this multi-pronged strategy is to ensure that monetary and fiscal policies operate firmly within the region of stability. This means not being a source of instability and keeping sufficient safety margins or buffers to deal with the inevitable future recessions as well as with unexpected damaging shocks.

For monetary policy, two aspects stand out. As regards operational frameworks, it is essential to combine price stability objectives with the appropriate degree of flexibility. As explored in depth in last year's Annual Economic Report, low-inflation regimes, in contrast to high-inflation ones, have self-stabilising properties. No doubt this reflects, in part, the fact that, when inflation is mild, it ceases to be a significant factor influencing people's behaviour. This suggests that, under those conditions, there is room for greater tolerance for moderate, even if persistent, shortfalls of inflation from narrowly defined targets. The approach would also reduce the side effects of keeping interest rates very low for extended periods, such as the build-up of financial vulnerabilities and possible misallocation of resources. As regards institutional frameworks, to buttress the credibility of policy, safeguards for central bank independence, underpinned by appropriate mandates, remain essential. They should become especially valuable in the future, should fiscal positions continue to follow their deteriorating trend.

For fiscal policy, the priority is to ensure fiscal sustainability. Fiscal sustainability is the cornerstone of economic stability and is critical for monetary policy to do its job. Unfortunately, the long-term outlook is grim. Even under favourable assumptions, without sustained and firm consolidation efforts, debt-to-GDP ratios are set to rise relentlessly, threatening safety margins. The looming additional burdens linked to ageing populations, the green transition and geopolitical tensions complicate the picture further. And so does the apparent change in public attitudes following the generous support granted in the wake of the GFC and Covid crises, which has raised expectations regarding government transfers. From an operational perspective, the prominence of financial factors in economic fluctuations merits greater attention when assessing cyclical fiscal positions and fiscal space more generally. From an institutional perspective, there is a need to give more bite to properly designed fiscal rules and fiscal councils, including possibly through constitutional safeguards.

For prudential policy, there is a need for continuous adjustments. The dialectic between financial markets and regulation makes it impossible to stand still. The recent episodes of stress have provided just the latest example. As regards the financial stability risks raised more specifically by fiscal policy, an area that merits particular attention is the favourable treatment of sovereign debt. Adjustments to account effectively for market and credit risk in government securities would also need to give due consideration to the special role that government debt plays in the functioning of the financial system and in central bank operations. Institutionally, just as for monetary policy, it is important to secure the independence of supervisory authorities and to endow them with sufficient resources, both financial and human.

In addition, there is a need to further reflect on crisis management and the financial system's safety net more generally. Policy actions have, de facto, been extending the safety net with each crisis. And now there are proposals to reduce the scope for runs by extending deposit guarantee schemes further. Once confidence is lost, however, deterring runs and preventing institutions from losing market access would require nothing short of insuring 100% of demandable and short-term claims. This would weaken market discipline far too much and, ultimately, increase solvency risks to unacceptable levels. Moreover, while resolution schemes have been improved and should be improved further, when confidence crumbles, the pressure to extend support becomes insurmountable.

This suggests that expectations should be realistic and that a premium should be put on crisis prevention. It indicates that, refinements aside, there is no substitute for a holistic macroeconomic policy framework that promotes financial and macroeconomic stability, bolstered by a regulatory and supervisory apparatus that boosts the financial system's loss-absorption capacity. As described in previous Annual Economic Reports, such a comprehensive macro-financial stability framework, in which all policies play their part, is the way to go. Crises cannot be avoided altogether, but their likelihood and destructive force can be contained.

Accordingly, the ambition needed to build such a framework should be combined with realism about what it can deliver and humility in the way it is run. The challenges the global economy is now facing reflect, in no small measure, a certain "growth illusion", born out of an unrealistic view of what macroeconomic stabilisation policies can achieve. We should avoid falling into the same trap again. Its unintended result has been reliance on a de facto debt-fuelled growth model that has made the economic system more fragile and unable to generate robust and sustainable growth. Overcoming this reliance requires growth-oriented structural reforms (Chapters I and II). Unfortunately, such reforms have been flagging for too long. They should be revived with urgency.

Digitalisation and the financial system: the journey ahead

This takes us to the third and final journey. An important aspect of growth-oriented structural reform is digital innovation in the monetary and financial system. Historically, key innovations in monetary arrangements have enabled new types of economic activity that have led to major advances in the economy. For example, money as ledger entries overseen by trusted intermediaries paved the way for new financial instruments such as bills of exchange that boosted trade by bridging the geographical distance and the timing gap between incurring costs and receiving payment. The gains became even bigger once electronic record-keeping replaced paper ledgers.

Central banks have a duty to lead advances in the monetary system in their role as guardians. The central bank issues the economy's unit of account and ensures the finality of payments through settlement on its balance sheet. Building on the trust in central bank money, the private sector uses its creativity and ingenuity to serve customers. When viewed through this lens, the fight against inflation is just another aspect of the central bank's broader duty to defend the value of money. In the same vein, the central bank's role in innovation serves to defend the value of money by providing it in a form that keeps pace with technology and the needs of society.

Chapter III charts the course for the future of the monetary and financial system. It argues that the system could be on the cusp of a major technological leap. Following the dematerialisation of money from coins to book entries and the digital representation of those ledger entries, the next key development could be tokenisation – the digital representation of money and assets on a programmable platform. Unlike conventional ledgers, which rely on account managers to update records, tokens can incorporate the rules and logic governing transfers. Money and asset claims become executable objects that the user can transfer directly. Tokenisation could enhance the capabilities of the monetary and financial system, not just by improving current processes but also by enabling entirely new economic arrangements that are impossible in today's system. In short, tokenisation could improve the old, and enable the new.

Tokenisation overcomes a key limitation of today's arrangements. Currently, the digital representation of money and other claims resides in siloed proprietary databases, located at the edges of communication networks. These databases must be connected through third-party messaging systems that exchange messages back and forth. As a result, transactions need to be reconciled separately before eventually being settled with finality. Meanwhile, participants have an incomplete picture of actions and circumstances. This incomplete information, and the associated misaligned incentives, preclude some transactions that have a clear economic rationale. While workarounds, such as collateral or escrow, exist, they do have limitations and create their own inefficiencies. Tokenisation addresses the problems more fundamentally. Resolving FX settlement risk and unlocking supply chain finance are two examples discussed in the chapter. Both are thorny problems in the conventional financial system that are amenable to solution in a tokenised environment.

New demands are also emerging from end users themselves, as advances in digital services in everyday life raise their expectations. Users now demand that the monetary and financial system operate just as seamlessly as the apps on their smartphones. These demands are beginning to outgrow the siloed domains that are holding innovation back.

Chapter III presents a blueprint for a future monetary system. The blueprint envisages a new type of financial market infrastructure (FMI) – a "unified ledger". The key elements of the blueprint are central bank digital currencies (CBDCs), private tokenised money in the form of tokenised deposits and tokenised versions of other financial or real assets, depending on the particular use case. The success of this endeavour rests on the foundation of trust provided by central bank money and its capacity to knit together key elements of the financial system. To be sure, in crypto, stablecoins that reside on the same platform as other crypto assets also perform a means of payment role. However, for reasons explored at length in last year's Annual Economic Report, crypto is a flawed system, with only a tenuous connection to the real world. Central bank money is a much firmer foundation. The full potential of tokenisation is best harnessed by having central bank money reside in the same venue as other tokenised claims.

As a new type of FMI, a unified ledger will come with attendant setup costs. While some of the envisaged benefits could also be reaped through more incremental changes to existing systems, history shows that such fixes have their limits, especially as they accumulate on top of legacy systems. Each new layer is constrained by the need to ensure compatibility with the legacy components. These constraints become more binding as more layers are added, holding back innovative developments.

In the near term, a unified ledger could unlock arrangements that have clear economic rationale but which have not been feasible to date due to the limitations of the current system. Over the longer term, the eventual transformation of the financial system will be far more significant. The benefits will be limited only by the imagination and ingenuity of developers, much as the ecosystem of smartphone apps has defied the initial imagination of the platform-builders themselves.

Conclusion

The journey ahead for the global economy and its financial system is hazardous. However, it also offers great opportunities. Steering in the right direction will be far from easy. It calls for a rare mix of judgment, ambition, realism and the political will and capacity to implement the necessary policies. Those policies tend to involve short-term costs as the price to pay for bigger long-term benefits. Fortunately, the journey ahead is not predetermined.