Basel III liquidity indicators increase slightly while risk-based capital and leverage ratios are stable for large internationally active banks, latest Basel III monitoring exercise shows

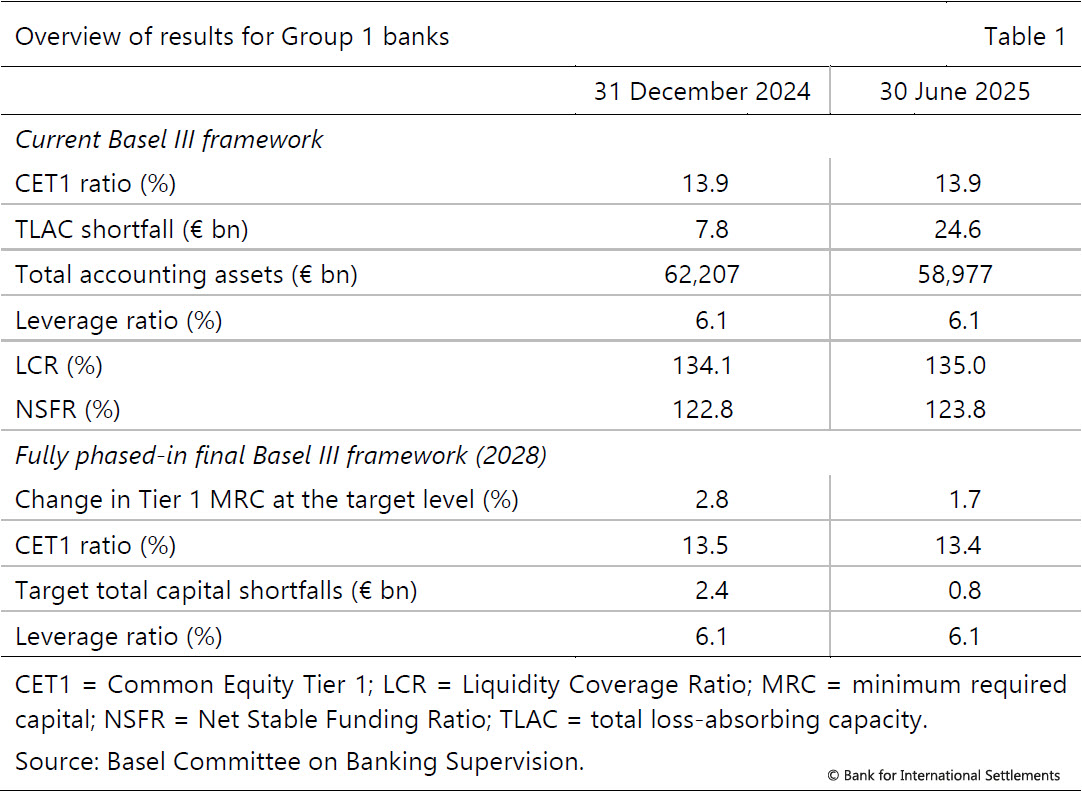

- Banks' liquidity ratios increased slightly while Basel III risk-based capital and leverage ratios are stable in the first half of 2025.

- The average impact of the Basel III framework on the Tier 1 minimum required capital (MRC) of Group 1 banks decreased, driven by implementation progress.

- The newly expanded cryptoasset exposures dashboard shows how banks are classifying their cryptoasset exposures.

Basel III Liquidity Coverage Ratios (LCRs) and Net Stable Funding Ratios (NSFRs) increased while capital and leverage ratios remained stable for large internationally active banks in the first half of 2025, according to the latest Basel III monitoring exercise, published today.

The report, based on data as of 30 June 2025, sets out trends in current bank capital and liquidity ratios and the impact of the fully phased-in Basel III framework, including the December 2017 finalisation of the Basel III reforms and the January 2019 finalisation of the market risk framework. It covers both large internationally active banks (Group 1) and other smaller banks (Group 2). See note to editors for definitions.

The implementation of the final elements of the Basel III minimum requirements began on 1 January 2023.

The report is accompanied by interactive Tableau dashboards, offering users an intuitive way to explore results. One dashboard focuses on banks' exposure to cryptoassets and shows how banks have reported whether they believe certain cryptoasset exposures meet the four classification conditions outlined in SCO60.

Note to editors

Through a rigorous reporting process, the Basel Committee regularly reviews the implications of the Basel III standards for banks and has been publishing the results of such exercises since 2012.

The results shown for "current Basel III framework" reflect the current jurisdictional standards that apply to the reporting banks as of 30 June 2025, which reflect different degrees of implementation of the Basel III reforms. The Basel III implementation dashboard provides an overview of Basel III implementation status across jurisdictions. The results shown for "fully phased-in final Basel III framework (2028)" assume that the positions as of 30 June 2025 were subject to the full application of the Basel III standards. That is, they do not account for transitional arrangements set out in the Basel III framework, which expire on 1 January 2028. No assumptions were made about bank profitability or behavioural responses, such as changes in bank capital or balance sheet composition. For that reason, the results of the study may not be comparable with industry estimates.

Data are provided for 150 banks, including 101 large internationally active banks. These "Group 1" banks are defined as internationally active banks that have Tier 1 capital of more than €3 billion and include 29 institutions that have been designated as global systemically important banks (G-SIBs). The Basel Committee's sample also includes 49 "Group 2" banks (ie banks that have Tier 1 capital of less than €3 billion or are not internationally active).

The values for the previous period may differ slightly from those published in the previous report. This is because, first, some banks have updated their earlier data to improve accuracy and expand the dataset over time. Second, additional national Pillar 1 requirements have been included to give a clearer picture of how Basel III affects banks' target capital requirements. For more information, you can refer to the Basel III monitoring methodology note.