Basel III capital ratios for largest global banks increased above pre-pandemic levels in the second half of 2022, latest Basel III monitoring exercise shows

- Initial Basel III capital ratios increased above pre-pandemic levels in the second half of 2022 and liquidity coverage ratios declined but remained above pre-pandemic levels.

- The average impact of the final Basel III framework on Tier 1 minimum required capital of the largest global banks (+3.0%) increased by 20 basis points since the first half of 2022 (+2.8%).

- New dashboards provide an interactive visualisation of the results for the definition of capital and total loss-absorbing capacity (TLAC).

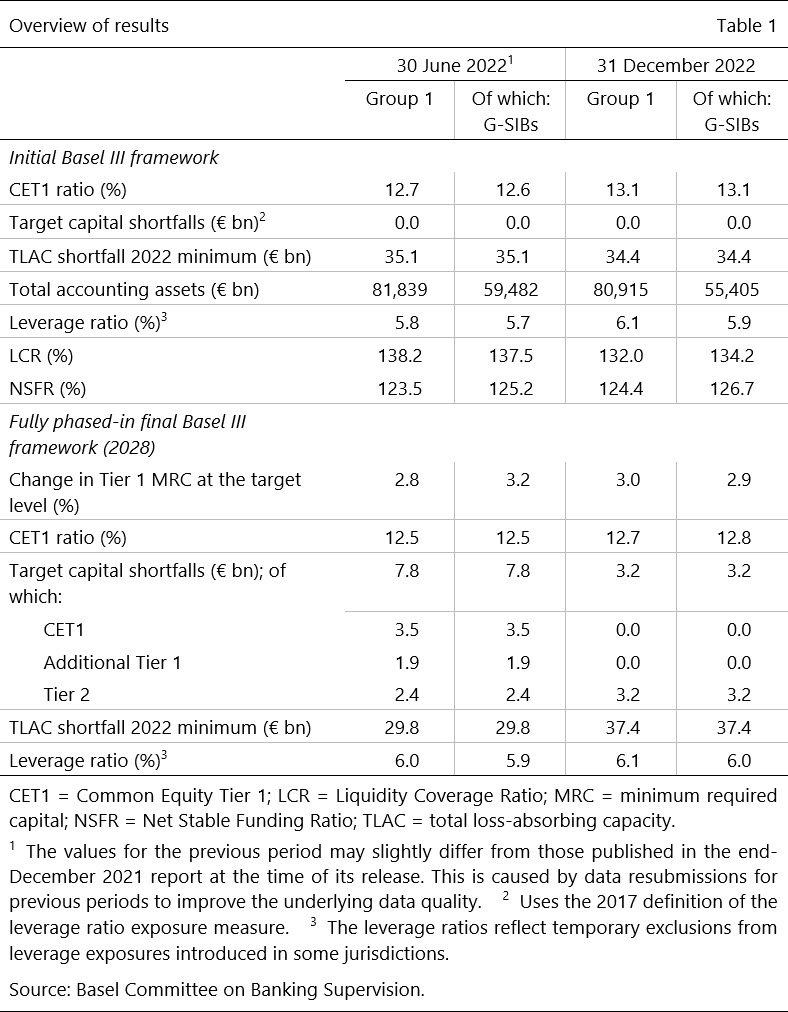

After a downturn in the first half of 2022, initial Basel III capital ratios for a sample of the largest global banks increased above pre-pandemic levels in the second half of 2022, according to the latest Basel III monitoring exercise, based on 31 December 2022 data, published today. The leverage ratio further increased on average, driven by Europe and the Americas, after showing an overall decrease during the pandemic period.

The dividend payout ratio continued its upward trend as banks no longer faced restrictions on dividends that member jurisdictions introduced at the onset of the pandemic.

The report sets out the impact of the Basel III framework, including the December 2017 finalisation of the Basel III reforms and the January 2019 finalisation of the market risk framework. It covers both Group 1 and Group 2 banks (see note to editors for definitions).

The implementation of the final Basel III minimum requirements began on 1 January 2023. For this reporting period, the average impact of the fully phased-in final Basel III framework on the Tier 1 minimum required capital (MRC) of Group 1 banks was +3.0%, compared with +2.8% at end-June 2022. Group 1 banks reported total regulatory capital shortfalls amounting to €3.2 billion, compared with a shortfall of €7.8 billion at end-June 2022.

The monitoring exercises also collect bank data on Basel III liquidity requirements. The weighted average Liquidity Coverage Ratio (LCR) decreased from the prior reporting period to 132.0% for Group 1 banks but remained close to pre-pandemic levels. For this reporting period, three Group 1 banks reported an LCR below the minimum requirement of 100%.

The weighted average Net Stable Funding Ratio (NSFR) increased to 124.4% for Group 1 banks. For this reporting period, all banks reported an NSFR above the minimum requirement of 100%.

The report is accompanied by interactive Tableau dashboards that allow users to explore the results with greater ease and flexibility. In addition to dashboards published previously, there is now an additional dashboard on the definition of capital. A section on TLAC was also added to the dashboard on the impact of the final Basel III framework. This finalises the Basel Committee's collection of dashboards related to Basel III monitoring.

Note to editors

Through a rigorous reporting process, the Basel Committee regularly reviews the implications of the Basel III standards for banks and has been publishing the results of such exercises since 2012.

The results of the monitoring exercise assume that the positions as of 31 December 2022 were subject to the fully phased-in initial or final Basel III standards. That is, they do not take account of the transitional arrangements set out in the Basel III framework. No assumptions were made about bank profitability or behavioural responses, such as changes in bank capital or balance sheet composition. For that reason, the results of the study may not be comparable with industry estimates.

Data are provided for 178 banks, including 111 large internationally active banks. These "Group 1" banks are defined as internationally active banks that have Tier 1 capital of more than €3 billion and include 29 institutions that have been designated as global systemically important banks (G-SIBs). The Basel Committee's sample also includes 67 "Group 2" banks (ie banks that have Tier 1 capital of less than €3 billion or are not internationally active).