Step-in risk - Executive Summary

The 2007–09 Great Financial Crisis (GFC) provided evidence that banks sometimes have incentives beyond contractual obligation or equity ties to "step in" to support unconsolidated entities to which they are connected. This happened in the form of credit or liquidity support that banks provided to, among others, securitisation conduits, structured investment vehicles and money market funds.

In response, in October 2017 the Basel Committee on Banking Supervision (BCBS) issued guidelines on the identification and management of step-in risk, which refers to the risk that a bank will provide financial support to an entity beyond, or in the absence of, its contractual obligations should the entity experience financial stress. The guidelines aim to alleviate potential spillover effects from the shadow banking system1 to banks from this risk. This involves bank assessments of potential step-in risk and the supervisory evaluation of such assessments through regular reporting. The guidelines were developed as part of an initiative by the G20 to strengthen the oversight and regulation of the shadow banking system, and were expected to be implemented by 2020.

Since the GFC, a number of policy developments, including those initiated by the BCBS, have helped to identify and reduce the likelihood of a bank stepping in. The guidelines are intended to supplement these reforms and provide a structured, forward-looking approach focusing on residual step-in risk (ie after consideration of risk mitigants). These guidelines aim for consistency across jurisdictions but, at the same time, acknowledge the idiosyncratic nature of this risk.

Identifying and managing step-in risk

Step-in risk arises when a bank considers that it is likely to suffer a negative impact from the weakness or failure of an unconsolidated entity and concludes that this impact is best mitigated by stepping in to provide financial support (eg to avoid the reputational risk the bank would suffer otherwise).

To help banks and supervisors deal with step-in risk, the BCBS guidelines provide a method for identifying it. They also describe potential risk measurement and management approaches that banks and supervisors can use that leverage existing prudential tools by informing or supplementing them. The guidelines do not prescribe any automatic Pillar 1 capital or liquidity charges but rely on the application of existing prudential measures in the Basel Framework.

Under the guidelines, banks should establish their own policies and procedures to identify and assess step-in risk as part of their risk management processes, regularly conduct self-assessment and report the results to their supervisors. Where significant step-in risk is identified, banks are required to choose the most appropriate response, while supervisors should review and challenge bank assessments and responses.

Banks' self-assessment

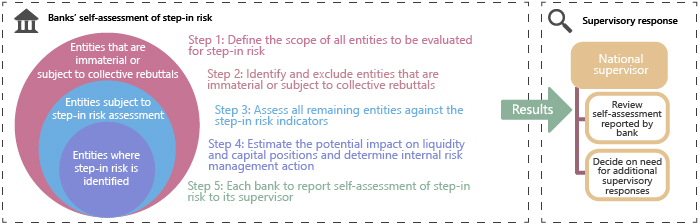

The first step for a bank is to define the scope of all entities to be evaluated for potential step-in risk, taking into account their relationship with the bank. Because step-in risk could involve a variety of entities, the guidelines do not prescribe a definitive list of entity types.2 Instead, they follow a principles-based approach under which a bank should consider all unconsolidated entities3 with which it has one or more of the following relationships: (i) the bank is acting as sponsor; (ii) the bank invests in the entity's debt or equity instruments; or (iii) the bank has another (non-)contractual involvement that exposes it to risks.

In terms of specific types of entity, a bank may exclude from the assessment, in general, non-financial entities (except providers of critical operational services) and insurance and banking entities (these are already subject to prudential treatment). Securitisation entities, asset management companies and the associated assets under management that are not consolidated for regulatory purposes should be included in the assessment.

In the second step, a bank may exclude entities from the assessment that are immaterial (ie if the bank were to provide support, its liquidity and/or capital positions would not significantly deteriorate4) or subject to collective rebuttals (ie the bank is prohibited by national laws or regulations from supporting them).

The third step is to assess all remaining entities against a (non-exhaustive) list of step-in risk indicators focused on the purpose and design of the entity. These should be considered in combination to reach a conclusion. They include the nature and degree of sponsorship, banks' degree of influence, potential provision of implicit support, exposure to structured entities/variable interest entities and highly leveraged entities, liquidity stress/first-mover incentive, risk transparency for investors, the existence of accounting disclosure requirements, investor risk alignment, potential reputational risk from branding and cross-selling, historical dependence or provision of step-in support, and regulatory restrictions and mitigants to a bank's propensity to step in (see Section 3 of the guidelines).

In the fourth step, for entities where step-in risk is identified, a bank should use the appropriate method to estimate the potential impact on liquidity and capital positions – measurement of the risk – and determine the appropriate internal risk management action. A bank's approach to step-in risk management and measurement should be sensitive to residual risk by considering the degree and effectiveness of any step-in risk mitigants. Depending on the nature and extent of the anticipated step-in support, a bank may address significant step-in risk to an entity by using any of the following approaches, either in isolation or in combination: inclusion of the entity in the regulatory scope of consolidation, use of a conversion factor to estimate the risk (conversion approach), application of Basel III liquidity requirements to account for step-in risk, stress testing, provisioning, application of a large exposure-like internal limit and step-in risk disclosure.

In the fifth step, a bank should report the results of its self-assessment to its supervisor, either as part of an existing supervisory process or as a standalone step-in risk report. This needs to be done on a regular basis. The expectation is that this reporting becomes mandatory and should be done annually. The guidelines provide two illustrative templates that may be used for supervisory reporting.

Supervisory response

The guidelines assign national supervisors the responsibility for reviewing bank policies and procedures, their self-assessments and any remedial actions taken. If the supervisory assessment reveals that significant residual step-in risks have not been appropriately estimated or mitigated, a supervisor should decide whether there is a need for an additional supervisory response. Measures that supervisors may consider include those available to banks (see step four above) and the application of ex post punitive capital charges if a bank actually steps in to support an entity beyond its contractual obligations.

1 The Financial Stability Board describes the shadow banking system as "credit intermediation involving entities and activities (fully or partially) outside the regular banking system". Shadow banking is now often referred to as "non-bank financial intermediation".

2 For illustrative purposes, Annex 2 of the guidelines provides a list of entities that could be considered in the assessment.

3 Unconsolidated entities are defined as entities that are outside the scope of regulatory consolidation, which includes all banking and relevant financial entities meeting regulatory criteria or the threshold for triggering consolidation. The scope of regulatory consolidation might differ from that for accounting.

4 A bank should establish its own internal policy for determining materiality, subject to supervisory review.

This Executive Summary and related tutorials are also available in FSI Connect, the online learning tool of the Bank for International Settlements.