Overview of the revised credit risk framework - Executive Summary

The Basel Committee on Banking Supervision (BCBS) has revised the credit risk framework as part of the Basel III reform package. The revisions seek to restore the credibility in the calculation of risk-weighted assets (RWAs) and improve the comparability of banks' capital ratios.

As under Basel II, the revised credit risk framework provides two main approaches for calculating credit RWAs:

Standardised approach (SA) - Under the SA, banks use a prescribed risk weight schedule for calculating RWAs. Similarly to Basel II, the risk weights depend on asset class and are generally linked to external ratings, but enhancements have been introduced.

Internal ratings-based (IRB) approach - Under the IRB approach, banks can use their internal rating systems for credit risk, subject to the explicit approval of their respective supervisors. Similarly to Basel II, banks can use either the advanced IRB approach (ie use their internal estimates of risk parameters such as probability of default (PD), loss-given-default (LGD) and exposure-at-default (EAD)) or the foundation IRB approach (ie use only their internal estimates of PD). However, enhancements to and constraints on the application of IRB approaches for certain asset classes have been introduced under Basel III.

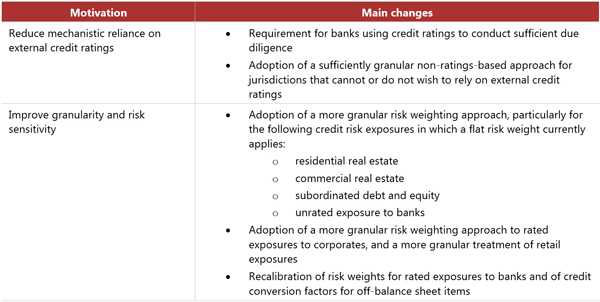

Standardised approach (SA)

The following are the main changes to the credit risk SA:

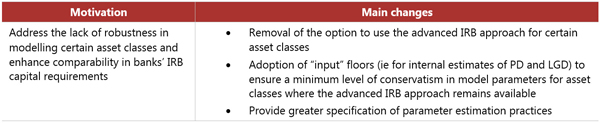

Internal ratings-based (IRB) approach

The following are the main changes to the credit risk IRB approach:

Implementation timeline

Both the revised SA and IRB approach will be implemented on 1 January 2022.

This Executive Summary and related tutorials are also available in FSI Connect, the online learning tool of the Bank for International Settlements.