Proportionality in Banking Supervision - Executive Summary

The Basel Framework is the full set of standards for the oversight of internationally active banks (IABs) in member jurisdictions of the Basel Committee on Banking Supervision (BCBS). This framework includes the Core Principles for Effective Banking Supervision (BCPs) and regulatory (Pillar 1), supervisory (Pillar 2) and disclosure (Pillar 3) standards. Although the BCPs are universally applicable, the remaining elements of the Basel Framework (the three pillars) are the standard for IABs.

To accommodate the diversity of banks and banking systems, the BCPs embed the concept of proportionality. Proportionality allows assessments of compliance with the BCPs that are commensurate with the risk profile and systemic importance of a broad spectrum of banks. Similarly, the Basel Framework allows for some proportionality by providing supervisory authorities with options for adopting simpler standardised approaches. In some jurisdictions, even the simpler approaches under the Basel Framework might require further adaptation. To support those authorities seeking to implement proportionality, the BCBS published its high-level considerations on proportionality. The considerations are voluntary and do not alter existing BCBS standards, guidelines or sound practices.

Overarching considerations in applying proportionality

Banks vary based on size, their international activities, level of sophistication and ownership structure. The institutional characteristics of supervisory authorities can also differ in legal powers, organisational structure, resource availability and independence. These differences can influence the proportionality approaches taken. Regardless of these variations, all proportionality approaches should remain consistent with the BCPs, foster financial system soundness, safeguard financial stability and limit regulatory arbitrage across and within jurisdictions.

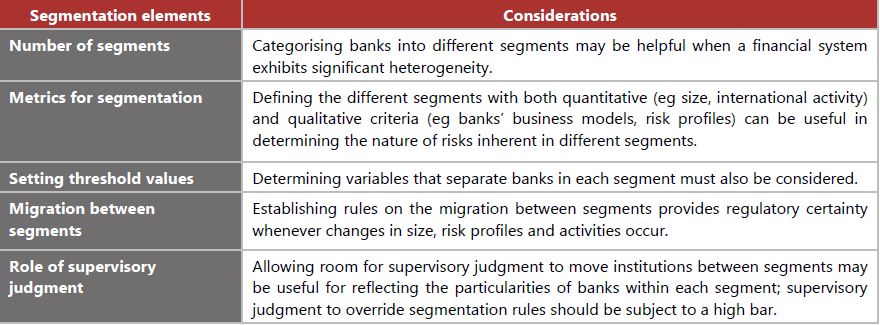

In designing proportionality approaches, one of the most fundamental issues involves segmentation: that is, how to differentiate among banks for purposes of applying tailored requirements. The table below sets out issues to consider in establishing a segmentation structure.

Core Principles for Effective Deposit Insurance Systems

Applying proportionality to risk-based capital (RBC) requirements

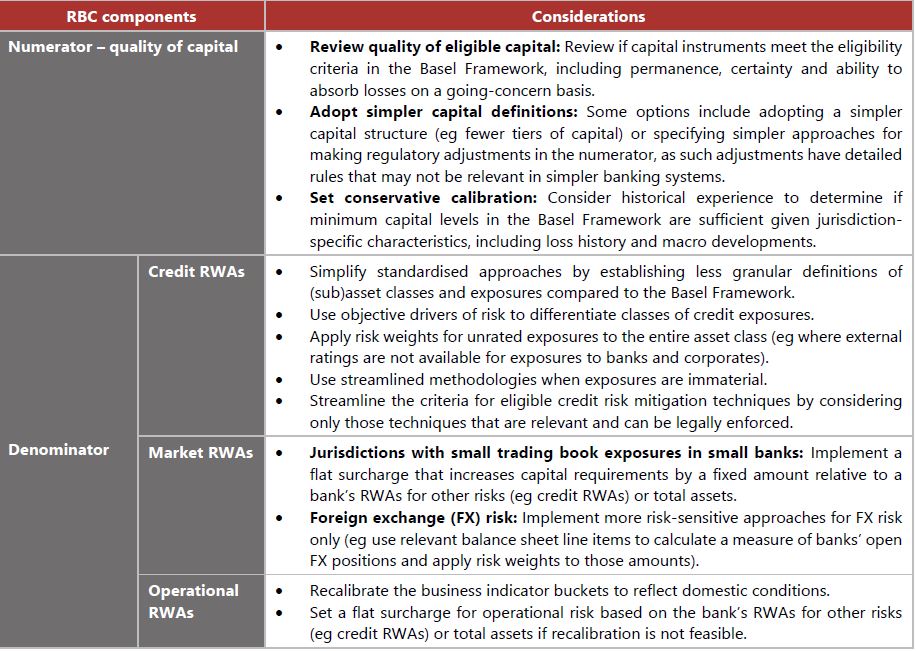

Some considerations in determining proportionality approaches to the RBC ratio are outlined below. This includes both the definition of capital (numerator) and the calculation of risk-weighted assets (RWAs) for credit, market and operational risks (denominator).

Applying proportionality to other Pillar 1 regulatory requirements

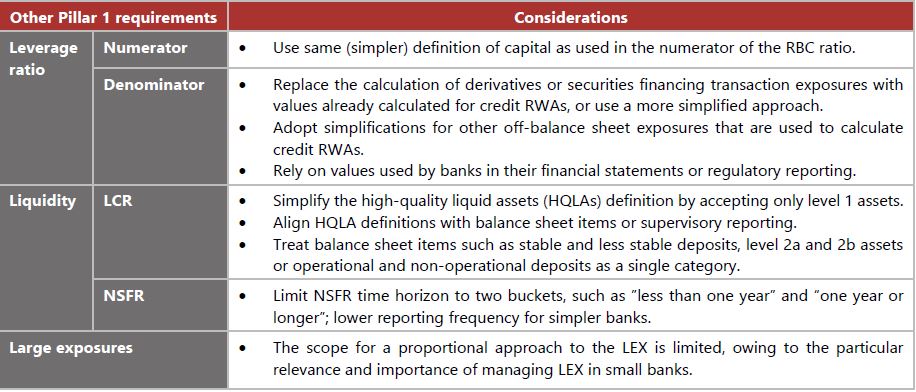

The table below highlights some considerations in determining proportionality approaches for other Pillar 1 requirements. These include:

- the leverage ratio (LR): the LR complements RBC requirements by providing a backstop against excessive leverage and model risk. The LR is calculated as a measure of Tier 1 capital (numerator) over a bank's total exposures (denominator)

- two liquidity standards: the Liquidity Coverage Ratio (LCR), a measure that promotes short-term resilience, and the Net Stable Funding Ratio (NSFR), which requires banks to maintain a stable funding profile in relation to their asset composition and off-balance sheet activities; and

- the large exposures (LEX) standard: the LEX limits the maximum loss that a bank could face in the event of a sudden counterparty failure, by limiting the size of a bank's LEX to a single counterparty or to a group of related counterparties to 25% of the bank's Tier 1 capital

Applying proportionality under Pillars 2 and 3

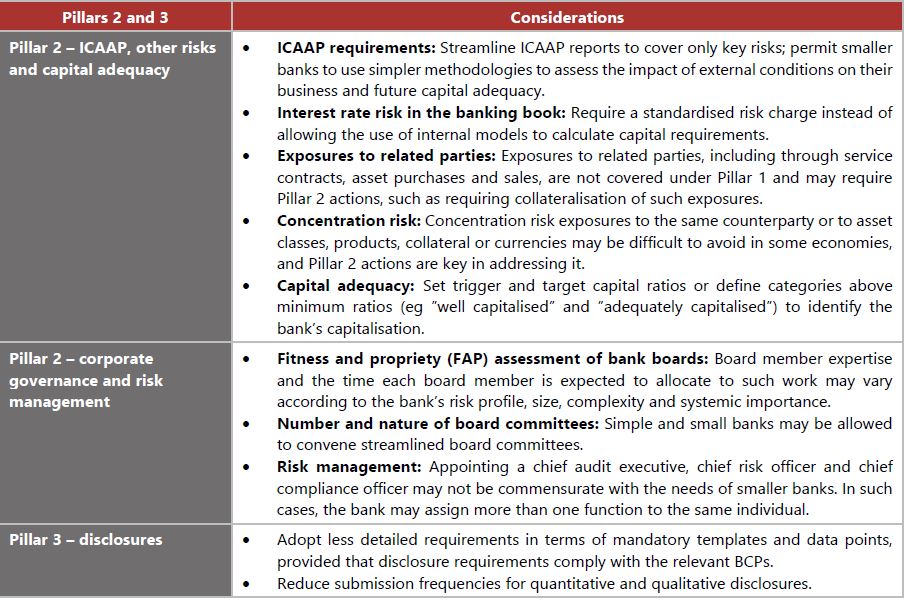

The Pillar 2 supervisory review process includes an assessment of banks' internal capital adequacy assessment processes (ICAAPs), risks not covered under Pillar 1, capital adequacy, and governance and risk management. The Basel Framework also requires compliance with Pillar 3 disclosure requirements. Below are some considerations in applying proportionality to Pillars 2 and 3 of the Basel Framework.

This Executive Summary and related tutorials are also available in FSI Connect, the online learning tool of the Bank for International Settlements.