Pillar 2 framework - Executive Summary

The four principles of Pillar 2 are an integral component of the Basel Framework. They describe the supervisory review process to make sure a bank's capital and liquid asset holdings are adequate, given its risk profile.

Pillar 2 complements the minimum regulatory requirements of Pillar 1 and the disclosure requirements under Pillar 3. It is a principles-based standard premised on sound supervisory judgment to ensure that banks have sound internal processes in place and use appropriate risk management techniques to support their businesses.

Pillar 2 can be tailored to the risks, needs and circumstances of a particular jurisdiction and bank. The resulting jurisdictional differences are alleviated through supervisory cooperation in supervisory colleges and other forms of collaboration and coordination.

Some areas are particularly important for supervisory review under Pillar 2. One such area is an assessment of corporate governance, including misconduct risk and firm-wide risk management, as well as those risks that are considered under Pillar 1 but not fully captured by Pillar 1 capital requirements. Examples of these risks are interest rate risk in the banking book; non-financial risks such as strategic risk, business model risk and reputational risk; and aspects of credit concentration risk.

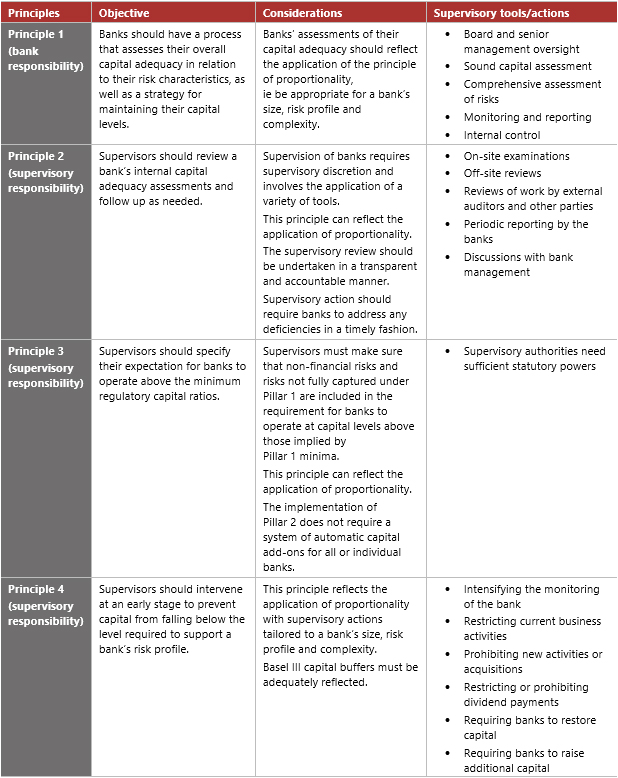

The four principles of Pillar 2

Of the four principles, principle 1 is aimed at banks while the remaining principles are intended for supervisors. The internal capital adequacy assessment process (ICAAP) of a bank under principle 1 must reflect an integrated approach to risk management and capital management, involving an assessment of the level of, and appetite for, risk and then ensuring that the level and quality of capital are appropriate to that risk profile. The ICAAP should be developed on a consolidated basis, but supervisors may require an ICAAP to be undertaken at the bank-only level within a group. The implementation of supervisory principles 2-4 - that is, reviewing and assessing banks' ICAAPs, requiring banks to operate above minimum capital requirements and taking early actions - typically involves various combinations of supervisory tools and activities, as noted in the table below.

Implementation

The collective implementation of the four principles necessitates a proportionate supervisory approach that typically varies with a bank's size, complexity and risk profile. It is designed to involve supervisory judgment, and supervisors use a range of approaches when implementing Pillar 2. For example, forward-looking stress testing that identifies possible events or changes in market conditions that could adversely impact a bank is an important tool in implementing principle 1. The supervisory implementation of principles 2-4 is driven by the implementation of risk-based supervision, a forward-looking supervisory framework applied by most supervisors.

* This Executive Summary and related tutorials are also available in FSI Connect, the online learning tool of the Bank for International Settlements.