Supervisory implications of IFRS 17 insurance contracts - Executive Summary

Significance of IFRS 17

After almost 20 years in the making, the final International Financial Reporting Standard (IFRS) 17 Insurance Contracts was released in May 2017, marking one of the most significant developments in the insurance industry in recent years. IFRS 17 sets out how companies should value issued insurance (including reinsurance) contracts, typically an insurer's largest balance sheet items. Therefore, the standard is hugely significant in the determination of an insurer's financial position. IFRS 17 is expected to improve the usefulness, transparency and cross-jurisdictional comparability of insurers' financial reports. As the international standard for the accounting of insurance contracts, IFRS 17 will be used by the majority of global insurers for general purpose financial reporting and, in some cases, for prudential reporting as well.1

Main elements of IFRS 17

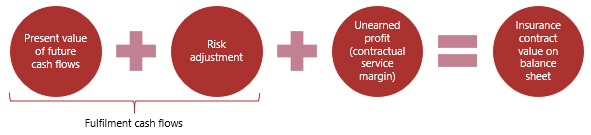

At a very high level, the value of an insurance contract based on the IFRS 17 core requirements is as follows:

IFRS 17 will require many affected insurers to significantly change the way they currently value and report their insurance contracts. The following are some of the major changes expected:

- for life insurers, the requirement to value insurance contracts using fully updated information to better reflect insurers' true underlying financial positions

- for non-life insurers, the requirement to discount future cash flows and to set up explicit risk adjustment for incurred insurance claims

IFRS 17 will become effective on 1 January 2021, with early adoption allowable in certain circumstances. To give effect to IFRS 17, the standard needs to be transposed into local accounting rules. The national accounting bodies may decide to adopt IFRS 17 with or without adjustments, and jurisdictional requirements will determine if IFRS 17 will be applicable only to listed companies or to all.

Interlinkages with prudential requirements

In the banking sector, the regulatory treatment of accounting provisions relies primarily on accounting standards. In contrast, there is a spectrum of regulatory approaches in the insurance sector covering the extent to which accounting standards are relied upon in the valuation of insurance contracts. At one end of the spectrum, an insurance supervisor could adopt IFRS 17 with few, if any, adjustments for prudential purposes. At the other extreme, an insurance supervisor could prescribe a completely different valuation standard for insurance contracts for prudential purposes, independent of IFRS 17 or any other local accounting standards.

Note that, in the past, the international supervisory community, as represented by the International Association of Insurance Supervisors, stated publicly that it is most desirable for general purpose financial reporting to be as consistent as possible with prudential reporting.

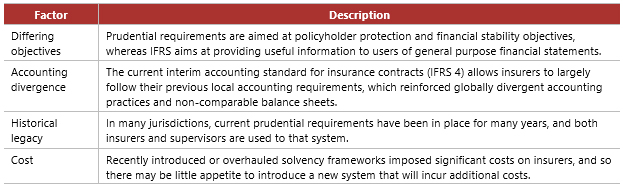

There are many reasons why local insurance supervisors have adopted different approaches, including:

Supervisory issues

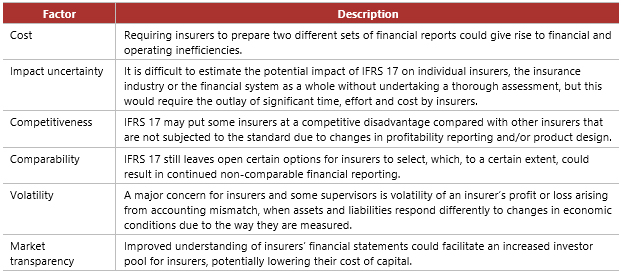

The implications of IFRS 17 for supervisory frameworks depend on the different regulatory approaches. In jurisdictions where IFRS 17 will also be used for prudential purposes, supervisors will need to introduce the necessary legislative or regulatory changes in order to implement the standard. In other jurisdictions, supervisors will need to decide if they will continue to prescribe diverging prudential requirements or to adopt IFRS 17. Factors that may affect this decision include:

IFRS 17 could also have financial stability implications. The International Accounting Standards Board expects IFRS 17 to contribute to long-term financial stability by revealing useful information about insurers that will enable actions to be taken in a timely way. From a supervisory perspective, this could be achieved, for example, if IFRS 17 is used as a valuation basis incorporated in a jurisdiction's regulatory solvency control framework and this results in an earlier trigger for appropriate supervisory intervention.

Excerpts from the IFRS and interpretations in this document are reproduced with the kind permission of the International Accounting Standards Committee Foundation. Please see the related Copyright and Disclaimer Notice.

This Executive Summary and related tutorials are also available in FSI Connect, the online learning tool of the Bank for International Settlements.

1 IFRS 17 considerations are relevant in jurisdictions adopting IFRS financial reporting. Some jurisdictions with large insurance industries, such as Japan and the United States, have not adopted IFRS and require insurers to report using local accounting standards.