The G-SIB framework - Executive Summary

During the Great Financial Crisis, the failure or impairment of a number of large, globally active financial institutions created enormous stress in the financial system and harmed the real economy. The public sector interventions to restore financial stability at the time demonstrated the need to put in place measures to reduce the likelihood and severity of the failure of a global systemically important financial institution (G-SIFI). To that effect, the official community developed new requirements for G-SIFIs, starting with global systemically important banks (G-SIBs). To reduce the probability of failure of G-SIBs, the Basel Committee on Banking Supervision (BCBS) increased the going-concern loss absorbency of G-SIBs through an assessment methodology and related higher loss absorbency (HLA) requirement.1

The G-SIB methodology and associated buckets

The BCBS published a G-SIB methodology in 2011, updating it in 2013 and then again in 2018. The fundamental features of the methodology have remained unchanged over time:

- The methodology relies on an indicator-based quantitative approach that aims to capture the systemic importance of a G-SIB.

- The selected indicators reflect the size of the banks, their interconnectedness, the lack of readily available substitutes or financial institution infrastructure for the services they provide, their global (cross-jurisdictional) activity and their complexity. These five categories of systemic importance receive equal weight in the computation of the numerical score that each bank in the sample receives in terms of its relative systemic importance.2

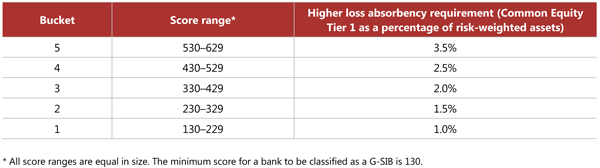

- Banks whose score is above a minimum cutoff level set by the BCBS are classified as G-SIBs. The G-SIB score can fall into one of five buckets (see table). Attached to each bucket is an incremental HLA requirement, as explained below. As the G-SIB assessment is conducted annually, a bank's score may move between buckets because of absolute or relative changes in its degree of systemic importance in relation to the other banks in the sample.

- The methodology permits supervisory judgment to justify divergence from the indicator-based measurement approach when classifying a bank as a G-SIB or allocating it to a specific bucket in the methodology. However, the applicability of supervisory judgment is strictly controlled in the methodology, in terms of both its impact and the process for incorporating it.

The methodology, as updated in 2018, clarifies the disclosure requirements that national authorities would set for their G-SIBs, and especially for the 75 largest banks in the world.

The methodology, including the indicator-based measurement approach itself and the cutoff/threshold scores, is reviewed every three years. In the next review, due in 2021, the BCBS plans to pay particular attention to alternative methodologies for the substitutability category.

HLA implications and capital instruments

G-SIBs are required to hold additional capital, the amount of which depends on their score. The additional capital requirements start at 1.0% of risk-weighted assets for the lowest bucket, up to a capital requirement of 3.5% of risk-weighted assets for the top (fifth) bucket.

The top (fifth) bucket is empty. However, it may become populated between reviews. Should this happen, a sixth bucket would be added to provide incentives for banks not to further increase their systemic importance.

The HLA requirement for each bucket has remained unchanged since the G-SIB methodology was first introduced. These requirements were set on the basis of various analytical studies, attempting to balance the benefits of reducing the probability of a systemic financial crisis against the negative impact on credit flows of building up higher buffers.

The HLA requirement is to be met with Common Equity Tier 1 capital as defined by the Basel III framework, and it applies to the consolidated group, in line with the data collected for the G-SIB methodology. At the same time, the HLA requirement, as set in the G-SIB methodology, is the minimum level, giving national jurisdictions the option to impose higher requirements on their banks.

As clarified in 2018, if a G-SIB breaches the HLA requirement, it is required to agree to a capital remediation plan to return to compliance over a time frame to be established by its supervisor. Until it has completed that plan and returned to compliance, it is subject to the limitations on dividend payout defined by the conservation buffer bands and to other arrangements as required by the supervisor. If a G-SIB progresses to a higher bucket, it is required to meet the additional requirement within 12 months. Conversely, if the G-SIB score falls, resulting in a lower HLA requirement, the bank would be immediately released from its previous HLA requirement.

Timeline

The revised assessment methodology will take effect in 2021 (based on end-2020 data), and the resulting HLA requirement would be applied in January 2023.

This Executive Summary and related tutorials are also available in FSI Connect, the online learning tool of the Bank for International Settlements.

1 To reduce the extent or impact of failure of G-SIBs, it improved recovery and resolution frameworks. This dimension is not part of the G-SIB methodology and is therefore not covered in this Executive Summary.

2 The revised methodology published in 2018 introduces: (i) revisions to some of the individual indicators used for each of the five categories; (ii) the inclusion of insurance activities in some of the individual indicators; and (iii) a change to the definition of cross-jurisdictional indicators to be consistent with the definition of BIS consolidated statistics.