Definition of capital in Basel III - Executive Summary

The 2007-09 Great Financial Crisis (GFC) revealed several weaknesses in the capital bases of internationally active banks: definitions of capital varied widely between jurisdictions, regulatory adjustments were generally not applied to the appropriate level of capital and disclosures were either deficient or non-comparable. These factors contributed to the lack of public confidence in capital ratios during the GFC. To address these weaknesses, the Basel Committee on Banking Supervision (BCBS) published the Basel III reforms in December 2010 with the aim of strengthening the quality of banks' capital bases and increasing the required level of regulatory capital. In addition, the BCBS instituted more stringent disclosure requirements.

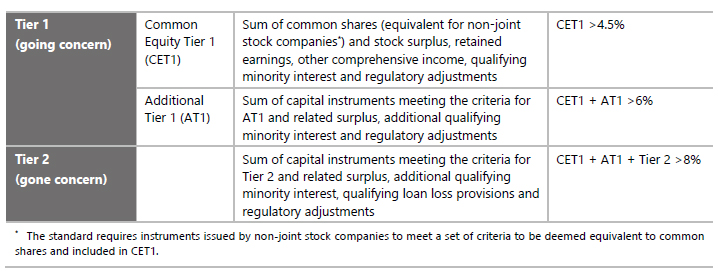

Regulatory capital under Basel III focuses on high-quality capital, predominantly in the form of shares and retained earnings that can absorb losses. The new features include specific classification criteria for the components of regulatory capital. Basel III also introduced an explicit going- and gone-concern framework by clarifying the roles of Tier 1 capital (going concern) and Tier 2 capital (gone concern), as well as an explicit requirement that all capital instruments must be able to fully absorb losses at the so-called point of non-viability (PoNV) before taxpayers are exposed to loss. In addition, regulatory deductions from capital and prudential filters have been harmonised internationally and are mostly applied at the level of common equity. Combined with enhanced disclosure requirements, aimed at improving the transparency of banks' capital bases and in this way improving market discipline, the revised definition aimed to reduce inconsistencies in its implementation across jurisdictions.

Components of regulatory capital

Common Equity Tier 1 capital (CET1) is the highest quality of regulatory capital, as it absorbs losses immediately when they occur. Additional Tier 1 capital (AT1) also provides loss absorption on a going-concern basis, although AT1 instruments do not meet all the criteria for CET1. For example, some debt instruments, such as perpetual contingent convertible capital instruments, may be included in AT1 but not in CET1. In contrast, Tier 2 capital is gone-concern capital. That is, when a bank fails, Tier 2 instruments must absorb losses before depositors and general creditors do. The criteria for Tier 2 inclusion are less strict than for AT1, allowing instruments with a maturity date to be eligible for Tier 2, while only perpetual instruments are eligible for AT1.

Total available regulatory capital is the sum of these two elements - Tier 1 capital, comprising CET1 and AT1, and Tier 2 capital. Each of the categories has a specific set of criteria that capital instruments are required to meet before their inclusion in the respective category. Banks are required to maintain specified minimum levels of CET1, Tier 1 and total capital, with each level set as a percentage of risk-weighted assets.

The PoNV condition requires all AT1 and Tier 2 instruments to be capable of being converted into common equity or written off. The trigger for the conversion/write-off is the earlier of (i) a decision of the relevant authority that the conversion/write-off is necessary, given that the bank is assessed to be non-viable; and (ii) a decision to inject public funds to prevent the bank's failure. This may happen based on either the authority's statutory powers or the contractual features of the capital instruments.

Minority (or non-controlling) interest

Minority interest, or non-controlling interest, arises from capital instruments issued to third parties by a fully consolidated subsidiary of a bank and can be located in any of the three components of regulatory capital: CET1, AT1 and Tier 2. Minority interest may receive recognition in the consolidated bank when it has the same loss-absorbing capacity as regulatory capital, that is, the instruments would, if issued by the parent bank, meet all of the criteria for classification as regulatory capital. In addition, the minority interest must not be funded, either directly or indirectly, by the parent bank and must be issued by a subsidiary that is itself a bank.

A bank subsidiary must maintain its minimum regulatory capital requirement at all times, and that capital must be available to support the consolidated group. As surplus capital in the subsidiary, that is, more than the statutory minimum requirement, could be repaid to the holders of the non-controlling interest, Basel III limits the recognition of minority interest to the amounts being used to cover statutory minimum capital requirements and excludes surplus capital of the subsidiary that is attributable to a non-controlling interest.

Regulatory adjustments

Basel III provides for a comprehensive list of regulatory adjustments and deductions from regulatory capital. These deductions typically address the high degree of uncertainty that these items have a positive realisable value in periods of stress and are mostly applied to CET1. Important deductions are goodwill and other intangible assets, deferred tax assets and investments in other financial entities.

For calculating regulatory capital for banks with investments in other financial institutions (banks, insurance and other financial entities) there should be no double-counting of capital. Hence, the underlying principle for the regulatory definition is "consolidation or deduction". The deduction should be applied by the investing bank to the same component of capital as the component in which the issuing bank receives recognition. This is referred to as the corresponding deduction approach.

New thresholds are applied to certain of the deductions under Basel III. Banks receive limited recognition for their significant investments in the common shares of unconsolidated financial institutions, mortgage servicing rights and deferred tax assets that arise from temporary differences. Each item is individually capped at 10% of the bank's common equity after the application of certain regulatory adjustments, and the aggregate is limited to 15% of the bank's CET1. Non-significant investments in unconsolidated financial institutions (that is, where the bank owns less than 10% of the common shares) are only deducted to the extent that all such exposures in aggregate exceed 10% of the bank's common equity.

* This Executive Summary and related tutorials are also available in FSI Connect, the online learning tool of the Bank for International Settlements.