Bank resolution framework - Executive summary

Taxpayer-funded bailouts of banks considered too big to fail were a defining characteristic of the Great Financial Crisis. In the intervening years, international standard setters and national authorities have taken steps to reduce both the probability and impact of the failure of such systemically important firms. Key among those steps was the development of an international framework for more effective resolution, which directly targets the impact of the failure of systemically important financial institutions. This Executive Summary provides an overview of the main elements of that framework as it applies to banks.

Identifying systemically important banks (SIBs)

A bank can be systemically important globally (G-SIB), domestically (D-SIB) or both. The Basel Committee on Banking Supervision (BCBS) has developed an indicator-based methodology for identifying G-SIBs according to the relative impact a bank's failure would have on the global financial system. The framework is also used to determine a G-SIB's additional loss absorbency requirements. The BCBS's framework for dealing with D-SIBs is principles-based, but likewise covers both the identification of D-SIBs (based on the relative impact of a bank's failure on the domestic financial system) and the assessment of additional loss absorbency requirements by national authorities.

The objective of the G-SIB and D-SIB frameworks is to enhance the going-concern loss absorbency of SIBs and reduce the probability of their failure.

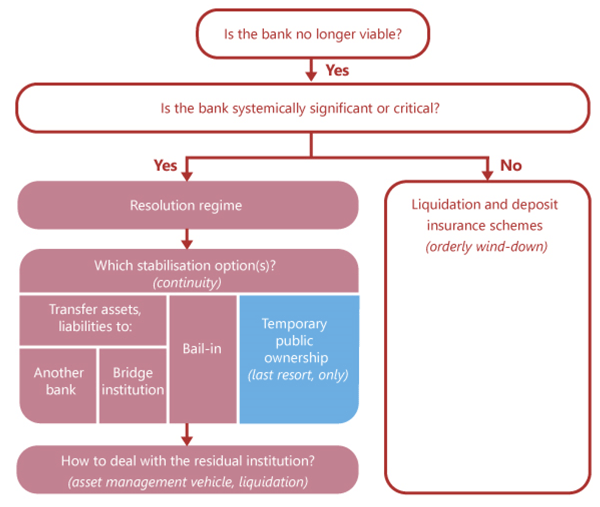

Implementing effective resolution regimes

An effective resolution regime should make possible the resolution of any bank in an orderly manner without severe systemic disruption or exposing taxpayers to the risk of loss. This is achieved by protecting the functions of the firm that are critical to the financial market or the real economy and ensuring that losses are borne by shareholders and creditors of the failing firm, as they would be in insolvency.

The international standard for resolution regimes for banks and other financial institutions, Key Attributes of Effective Resolution Regimes for Financial Institutions (Key Attributes), was developed by the Financial Stability Board (FSB). The Key Attributes are directed at systemically important financial institutions (SIFIs), including both D-SIBs and G-SIBs. They set out 12 essential features that should be part of the resolution regimes of all jurisdictions. These features fall into three broad categories:

- Comprehensive resolution regimes and tools - features that enable authorities to resolve firms without public funds and in a manner that preserves critical financial and economic functions. These include a resolution regime consistent with the Key Attributes that captures any financial institution that could be systemically significant or critical if it fails and an operationally independent resolution authority with a broad range of resolution powers.

- Effective cross-border cooperation and coordination - features that ensure resolution regimes and tools work effectively in a cross-border context. These include a legal framework that enables the resolution authority to cooperate with relevant foreign authorities, institution-specific cross-border cooperation agreements between the home and relevant host authorities and, in the case of G-SIBs, crisis management groups (CMGs) comprising the relevant authorities in jurisdictions that are home or host to entities that are material to the firm's resolution.

- Sustained recovery and resolution planning - features that ensure firms and authorities are prepared to handle severe distress or failure effectively. These include an ongoing process for recovery and resolution planning and recovery and resolution plans comprising elements prescribed in the Key Attributes.

The FSB has developed extensive guidance on the implementation of the Key Attributes that takes into account the need to accommodate different national legal systems and market environments.

The resolution process outlined in the Key Attributes can be represented (as it applies to banks) as follows:

Ensuring sufficient total loss-absorbing capacity (TLAC)

For home and host authorities - and markets - to be confident that G-SIBs are resolvable and no longer too big to fail, these firms must have sufficient loss-absorbing and recapitalisation capacity to allow for an orderly resolution that mitigates the impact on financial stability, ensures the continuity of critical functions and avoids exposing public funds to loss.

With that in mind, the FSB developed, in consultation with the BCBS, an international standard that sets a minimum TLAC requirement for G-SIBs. The TLAC standard defines the minimum amount of qualifying financial instruments that must be available for bail-in within resolution at G-SIBs.

G-SIBs in developed economies must meet an interim minimum TLAC requirement from 1 January 2019 and the final minimum requirement from 1 January 2022. For G-SIBs in emerging market economies, the corresponding implementation deadlines are 1 January 2025 and 1 January 2028, respectively.

This Executive Summary and related tutorials are also available in FSI Connect, the online learning tool of the Bank for International Settlements.