Central bank digital currencies as superheroes?

Keynote speech by Tara Rice, Head of Secretariat, Committee on Payments and Market Infrastructures, at the fifth annual meeting of CEBRA's International Finance and Macroeconomics Program, 20 October 2021.

Introduction

Money has changed in form drastically over the course of human history – from ancient shells and stones to today's coins, banknotes, bank sight deposits and credit cards.* More recent payment innovations include mobile money, payment apps, stablecoins and even a new form of central bank-issued money, central bank digital currencies (or CBDCs).1

CBDCs can be seen as a digital form of the central bank money we have in use today: cash (ie banknotes) and central bank settlement accounts. Retail CBDCs would be a central bank liability, a form of "digital cash" accessible to all. Wholesale CBDCs, also a digital liability of the central bank, could become a new instrument for settlement between financial institutions.

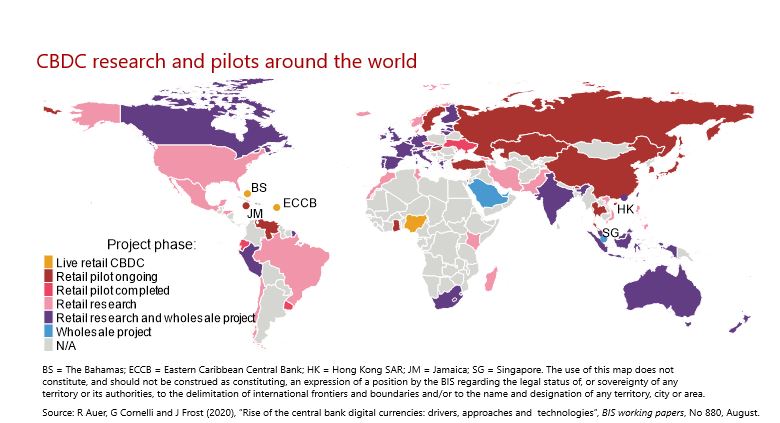

According to last year's CPMI CBDC survey, nearly 90% central banks were doing some sort of work on the topic.2 In fact, some are moving into more advanced stages, progressing from conceptual research to experimentation. Over the course of the last four years of conducting this survey, we have seen the work advance considerably.

Particularly in the area of wholesale CBDCs, many central banks are past the research stage and currently experimenting with concrete proofs-of-concept. Let me briefly mention a couple of examples led by the BIS Innovation Hub. Project mCBDC Bridge is testing interoperability between CBDC systems of four different jurisdictions3 on the same DLT platform while Project Dunbar is exploring the interoperability between multiple CBDCs on a shared platform.4

Also in the area of retail CBDCs, central banks are making large steps. Two retail CBDCs have been launched, namely the Sand Dollar of the Central Bank of the Bahamas and DCash of the Eastern Caribbean Central Bank.5

Most retail CBDC projects focus on domestic issues and use cases. Last year's CPMI CBDC survey showed that financial inclusion and enhancing domestic payments efficiency and safety are key motivations of central banks for issuing CBDC. These are followed by financial stability and monetary policy-related reasons. But CBDCs are seen by many central banks as an opportunity to enhance cross-border payments, as well. Cross-border payments can be defined as where the payer and payee each reside in a different jurisdiction, most often with a different currency. As you might have experienced yourself, cross-border payments have four primary challenges – they are generally costly, can be slow, suffer from low transparency and are not widely accessible. Many of today's frictions are rooted in differences among domestic payment systems (eg opening hours, technical standards, data requirements).6

In this context, CBDCs are seen by some as a superhero or superheroine solution; that is, as an opportunity to address all of the pain points in payments. Superheroes and heroines have fantastic abilities. They are full of possibilities. They come in many shapes and sizes: some are gifted with flight (like Captain Marvel), some with telekinesis (Wanda Maximoff), and others with super strength (Wonder Woman).

We could say that CBDCs also have many potential superpowers, or design features. They ought to have at least a "required" set of powers – perhaps strength and agility. Figuratively speaking, these ought to represent the prerequisites for a safe and secure CBDC.

CBDCs offer hope in improving payments generally, and in enhancing cross-border payments, more specifically. Like all superheroes, CBDCs do not need the full spectrum of superpowers. Having a few important design features could be sufficient for enhancing cross-border payments. Like Kamala Khan, whose powers include shapeshifting, elasticity, and size alteration – the ultimate power is perhaps interoperability.

On that note, I'd like to focus my remarks on three topics related to how CBDCs can help on the international dimension of payments: (i) a taxonomy to describe the different forms and elements of cross-border interoperability; (ii) the conceptual trade-off between cost and complexity on the one hand and benefits on the other (which in this case would be mainly in reducing the frictions of cross-border payments); and (iii) some thoughts on lessons learned and the way forward.

1. Interoperability

At a very high level, there are two fundamentally different ways in which cross-border payments with CBDCs can be envisioned:

The first is, like cash, a retail CBDC of a given jurisdiction is made available to anybody residing inside or outside that jurisdiction. This model would entirely depend on the jurisdiction's domestic CBDC design and would not require coordination between the issuing central banks because, by design, there will be just one central bank.

In practice, relatively few central banks are considering such fully open (and anonymous) systems. The Bahamian CBDC – the Sand Dollar – for example, is only available for domestic use. Non-residents can hold Sand Dollars when visiting the Bahamas, but only through a special Sand Dollar wallet, with a holding limit of 500 Sand Dollars and a transaction limit of 1,500 Sand dollars per month. (That is equal to 500 and 1,500 US dollars, respectively). While no central bank from an advanced economy has yet decided to proceed with a retail CBDC, many are exploring the topic due to its wide-ranging implications.

Alternatively, cross-border payments with CBDCs can be achieved through interoperability. This approach – the main focus of my talk – relies on design choices of the payments system infrastructures, and requires strong cooperation among central banks.

This is the approach that a number of central banks are following. A survey of 50 central banks conducted in early 2021 by my BIS colleagues7 shows that a quarter are considering incorporating interoperable features in designing their CBDC to reduce frictions in cross-border and cross-currency settlement. One key advantage of CBDCs compared with the efforts of improving the existing payments infrastructure is the opportunity to start with a "clean slate". If central banks take the international dimension into account when designing their domestic CBDCs and commit to interoperability, consistent standards and coordination of CBDC designs are built in from the start. And many problems inherent in today's legacy technologies and processes could be mitigated.

I'll note that my focus is on how cooperation can help achieve interoperability but also what challenges can arise. There are a number of critical issues with regard to the forces at work between competition and interoperability that I will not cover.

A conceptual framework for interoperability

Let's define interoperability. In a broad sense, interoperability is the technical or legal compatibility that enables a system or mechanism to be used efficiently in conjunction with other systems or mechanisms. There are a number of ways to classify interoperability; let me present three broad categories:

First, technical interoperability refers to making sure the systems use the same technical standards, such as message formats and communication protocols, as well as the hardware and software infrastructure needed for them to operate. Accounts and payees can be identified in different ways, eg using letters, numbers, institutional identifiers or even aliases such as a phone number or email address. Addressing a payment initiated in one system to a specific account in another system is a non-trivial challenge. For the non-CBDC systems we see today, technical interoperability is promoted through common ISO standards and APIs.

But agreeing on using the same standards is not enough to fully leverage the advantages of interoperability. This is where the second category, terminology (or semantic) interoperability comes in. Terminology interoperability is about everyone speaking and understanding the same language. It involves using the standards and arrangements in a uniform way, developing vocabularies and schemes to describe data exchanges, and ensuring that data elements are understood in the same way by all communicating parties Terminology interoperability is necessary for the effective delivery of services to a user across multiple systems. For example, even if messages can be exchanged between two systems, challenges arise when messages in one system are based on Latin alphabets, and another could be designed, say, for Chinese characters.

Finally, business interoperability refers to bilateral and multilateral agreements between infrastructures covering their mutual rights and obligations in processing transactions on behalf of their participants. For example, agreements on who can access the payments platform and when, execution and response times, how to clear and settle obligations among infrastructures and how to address risks of payment failures.

Let's compare this with how we interact in today's conference on Webex. We have invested in the technology; we have our computers or mobile devices connected to the internet, and we are all able to use Webex. We are clearly technically interoperable, even though we use different computers or other devices, different operating systems etc.

But there's more to it. The organisers have chosen English as the conference language and everyone connected via WebEx can be assumed to speak English (or to have a translate function working properly). So we have terminology (or language) interoperability.

We have also agreed multilaterally to some common business rules; we are muted when not speaking, and we raise our hands or the chat function to ask questions. We have agreed to hold this event at this specific time of the day so that those from other time zones can attend this event more easily. This is business interoperability.

2. Benefits, challenges and trade-offs of interoperability

Achieving meaningful progress in enhancing cross-border payments requires interoperability in all three categories, in varying forms depending on the initial starting point and the level of innovation or development desired. There are numerous trade-offs to consider, and I will come back to this in a moment.

Benefits

Generally speaking, the degree of overall interoperability increases as we adopt pure technical interoperability and then also include terminology and finally business interoperability. Various benefits are associated with increased interoperability between payment systems, and many of these also apply to CBDCs.

Interoperability between different CBDCs will allow for greater efficiency, which may eventually mean lower costs and reduced processing times, ie cheaper and faster cross-border payments. Compatible message standards, for example, will allow payments to flow without data loss or manual interventions.

Common agreements for CBDC wallet providers or common charging and foreign exchange conversion practices would enable users to calculate fees and rates prior to initiating a cross-border payment, resulting in higher transparency. And having common or compatible compliance regimes reduces uncertainty and costs, at the same time increasing user access.

All this leads to benefits for existing users and greater inclusion. And from a macro perspective, having full interoperability can encourage regional and international economic and financial integration.

Challenges

But achieving interoperability is not easy and requires some heroic power and determination. The challenges, like the benefits, increase as we move from technical to also include terminology and business operability.

With technical interoperability, moving to a new payment platform involves research, development and investment costs. It may be the case that its benefit can be felt only when there is a sufficient number of platforms or users that have adopted the new technology. This can mean inertia, especially when there are legacy systems in place. So it requires a significant level of commitment, as well as coordination between domestic and foreign entities and industry groups.

With terminology interoperability, once the investments in the underlying technology have been made, arrangements must be made to ensure uniform implementation. This might require additional investments, but potentially also changes in domestic laws to align standards, such as those involving anti-money laundering and counterterrorist policies. This requires again cooperation and coordination, across platform operators and regulators, which can be challenging and time-consuming, especially in a cross-border context.

As regards business interoperability, it is a mistake to think that when there's technical and terminology interoperability, we are almost there. Getting to bilateral and multilateral agreements might sometimes require a divergence from common practices. It might involve costs related to legal, operational, financial risk management, and possible foreign exchange settlement issues and agreements. This requires a dialogue with stakeholders, both domestically and internationally.

These steps require investment costs, the commitment of stakeholders and coordination among them, making interoperability complex to achieve. This holds for any type of payment system that jurisdictions wish to interlink. But here CBDCs could be seen as a solution. All jurisdictions start from scratch and are in the preliminary stages of their designs. And no one has a legacy CBDC system in place. This is the time to align approaches and agree on design features that allow interoperability.

Central banks already collaborate closely at an international level and have committed to the G20-endorsed roadmap to address the key challenges in cross-border payments. CBDCs are one solution that could be harnessed to overcome some of the obstacles I noted earlier with cross-border payments.

Trade-offs

Going forward, central banks will consider a variety of issues in designing CBDC systems. Interoperability is one important aspect. Many of the issues I've identified are jurisdiction-specific, which means that the ideal form of the CBDC and interoperability will vary across jurisdictions, there is no "one-size-fits-all" answer.

In pursuing interoperability between different CBDCs, a trade-off arises between costs and complexity to overcome on the one hand and the final efficiency (ie speed, safety, transparency etc) gains on the other.

The optimal choice is not a corner solution: that is, it's not black and white. Back to my analogy: superhero stories showcase the classic "good versus evil", but there are often deeper themes behind the stories. This is the same with CBDC and other innovations in digital payments.

Central banks have multiple options in how they could achieve interoperability, from harmonising messaging standards to also aligning business rules and regulatory frameworks. Thus the accrued benefits of achieving interoperability between CBDCs will differ across jurisdictions.

For CBDCs, technical interoperability will require use of common technical standards, such as message formats, cryptographic techniques, data requirements and user interfaces. Terminology interoperability will require CBDCs to move towards common languages, broadly speaking, for messaging and data, and to achieve uniform and consistent interpretation of data and information across systems and jurisdictions. Business interoperability will require the establishment of links and agreements between the central banks and/or payment system operators involved and allows participants – either retail or wholesale – in one CBDC system to make payments to those in another. But these forms of interoperability are often interdependent: central banks would, for example, need to agree on the clearing, settlement and FX conversion across CBDCs (business interoperability) alongside the commitment to share and interpret relevant data and information consistently (terminology interoperability).

For countries with many cross-border transactions, the benefits of cheaper and speedier cross-border payments might outweigh significant investment costs and the efforts required to modify public laws and regulations and private contractual arrangements. For others, having some basic level of compatibility through technical standardisation might be sufficient if not perfect.

If you've studied economics or business, you are likely familiar with the Pareto Principle, or the 80/20 rule. The idea is that 80% of the results come from 20% of the action. Let's apply this to the trade-off between cost and complexity versus improvements in the efficiency of cross-border payments and CBDCs. Central bank investments may be relatively low to achieve the first 80% of improvements, but then costly to achieve the final 20% of improvements. That said, while we may be happy with, say, 80% of maximum (payments) speed, should we accept 80% of maximum payment system safety and integrity? I would say that there are some areas where we cannot and should not compromise.

Also, the design of jurisdictions' current domestic payment systems will play a role. For central banks that aim to make their CBDC system interoperable with their current domestic RTGS, they might, for example, decide to use the same domestic technical interfaces and messaging standards, which might lead to national differences and complicate cross-border interoperability.

Let me say just a few words on CBDC alternatives to enhance cross-border payments. Development of stablecoins as a payment system continues apace, and the cryptoasset market continues to grow substantially. Are CBDCs the only solution? No, there are potential scenarios where a well designed stablecoin that meets all regulatory requirements could provide an affordable and inclusive payment option to households in some jurisdictions.

Let's link this back to the superheroine analogy. The Incredible Hulk, with potential for good but also for disruption, might be the appropriate stablecoin hero here. Certainly more work is needed – and it is already under way – on the potential regulation of stablecoin arrangements. Cryptoassets pose more acute challenges to the current regulatory and monetary system. Loki, the god of mischief, might be fitting here.

Clearly, more research is needed to further understand the trade-offs faced by different jurisdictions; on the impact of different interoperability choices on benefits and costs, and on the various business cases for cross-border interoperability.

3. Lessons learned

As I noted at the outset, the BIS Innovation Hub, central banks and financial institutions are experimenting with cross-border CBDC solutions. Let me raise three early lessons from these experimental projects.

First, not all projects will succeed. Failure lies on the path to innovation. Of course, failure is not the objective, but if we want to be at the cutting edge, we need to recognise that not all projects will succeed. As our General Manager said earlier this week, we need to "fail forward;" that is embrace failure as a stepping-stone to innovation.8 Not all successful projects will automatically lead to implementation. Still, the learnings of all projects – successful and unsuccessful ones alike – will provide important insights. The interesting thing about this concept is that is at odds with central banks culture. Central banks are by their nature quite conservative, and do not seek to fail.

Second, we must think ahead about possible scenarios and their outcomes, even if some of those scenarios seem at the moment unlikely. Why? Technological disruption is moving very quickly. We need to stay nimble and be prepared for outcomes that may not seem likely now, but which could have significant financial stability and macroeconomic implications. We should be thinking ahead about potential risks and what could be done to mitigate them. As noted, while central banks are moving steadily but cautiously with regard to CBDCs, comparatively, private stablecoin developers are moving at a very rapid pace. This requires that authorities must be thinking ahead about the potential regulation of stablecoins. An example is the recent consultation report on the application of the CPMI-IOSCO Principles for Financial Market Structures to stablecoin arrangements.9

Finally, international coordination and cooperation are essential. Failure to coordinate risks fragmentation of the financial system and lack of interoperability between countries in technical terms but also in policy terms. In addition to coordination and cooperation, we need public and private sector commitment over a sustained period of time. Without that commitment, I do not think we will be able to achieve the ambitious the objectives set out in the G20 roadmap, including the cross-border payment targets, aiming for meaningful progress by 2027.

4. Looking ahead

Today I have focused on how CBDCs could enhance cross-border payments, and in particular on the role of interoperability in achieving this goal. Let me end by highlighting some policy mistakes that should be avoided when further pursuing this work.10

First, while CBDCs have unique features, central banks should be aware that there are other policy tools to reach their public policy objectives, and that there's an interplay between them. In terms of improving cross-border payments, CBDCs are just one of the 19 elements, or building blocks, that comprise the G20 Roadmap. Other ways to improve cross-border payments include enhancing existing payment systems and arrangements and aligning regulatory, supervisory and oversight frameworks for cross-border payments. They impact each other, and their interdependencies should be carefully considered.

Importantly, CBDCs will not exist in isolation, and they are part of a broader payments ecosystem, next to other payment methods and systems. As is generally the case with any new technology or process, the eventual international adoption of CBDCs is likely to proceed at different speeds in different jurisdictions. This calls for interoperability with legacy payment arrangements, not only domestically but also abroad. Hence, the analysis of cross-border or domestic interoperability with non-CBDC payment arrangements calls for further work. Here pursuing backward compatibility between old and new may provide a solution, as we see in other areas of industry with strong network externality. Answering these open questions will be crucial for the appropriate design of CBDCs as a new form of money in the digital era.

Additionally, we clearly need to watch out for negative spillovers when exploring CBDCs in a cross-border dimension, especially, the macro-financial implications of cross-border CBDC use. International use of CBDCs could potentially increase cross-border flows or lead to currency substitution. However, some specific design choices for CBDCs could limit such use.

Let me close by saying that the superhero (heroine) motif makes for a great family movie night, but doesn't solve our real world problems. It reminds us of classical ideas of virtue and valour. But to be successful as a cross-border means of payment, CBDCs will require real-world solutions that only we can define and resolve. It will require material investment in infrastructures and resources, significant forward thinking, a little failing forward, and a heroic amount of international collaboration as well as sustained political support.

* This speech and the views expressed are those of the individual and do not necessarily reflect the views and/or position of the BIS or CPMI.

1 Many thanks to Anneke Kosse for her (super power) contributions to this speech.

2 C Boar and A Wehrli, "Ready, steady, go? – Results of the third BIS survey on central bank digital currency", BIS Papers, no 114, January 2021.

3 The Hong Kong Monetary Authority, the Bank of Thailand, the Digital Currency Institute of the People's Bank of China and the Central Bank of the United Arab Emirates.

4 Reserve Bank of Australia, Bank Negara Malaysia, Monetary Authority of Singapore, and South African Reserve Bank.

5 See "CBDC research and pilots around the world". Source: R Auer, G Cornelli and J Frost, "Rise of the central bank digital currencies: drivers, approaches and technologies', BIS Working Papers, no 880, August 2021.

6 See FSB, Enhancing cross-border payments stage 3 roadmap, 2020 and CPMI, Enhancing cross-border payments: building blocks of a global roadmap stage 2 report to the G20, 2020.

7 See R Auer, C Boar, G Cornelli, J Frost, H Holden and A Wehrli, "CBDCs beyond borders: results from a survey of central banks", BIS Papers, no 116, June 2021.

8 A Carstens, "Lessons on innovation", speech at the DC Fintech Week, 18 October 2021.

9 "Application of the Principles for Financial Market Infrastructures to stablecoin arrangements", CPMI Papers, no 198, 6 October 2021.

10 See D Elliott and L de Lima, "Central bank digital currencies: six policy mistakes to avoid", Oliver Wyman, May 2021.

{kind=link}