New correspondent banking data - the decline continues at a slower pace*

- The number of active correspondent banks worldwide fell by about 3% in 2019 and about 22% between 2011 and 2019.

- The volume and value of cross-border payments continued to grow over the last eight years, suggesting a higher concentration in payment flows.

Cross-border payments are vital for economic growth, international trade, global development and financial inclusion. Yet they are generally slower, more expensive, less transparent and less accessible than domestic payments. These long-standing issues have been thrown into sharp relief by improvements in domestic payments and by developers of proposals for new payment arrangements. The G20 has made enhancing cross-border payments a priority during the 2020 Saudi Arabian Presidency and has asked the Financial Stability Board (FSB) to coordinate the development of a roadmap to tackle the system's multidimensional problems. To address these issues, in response to a remit from the G20, the Committee on Payments and Market Infrastructures (CPMI) has developed the building blocks of a global roadmap with the aim of making durable improvements in cross-border payments.

Correspondent banking is a crucial part of any solution that enhances cross-border payments. To settle cross-border payments, most payment service providers rely on the so-called correspondent banking network1 - a network that is shrinking and becoming more concentrated. Thus, monitoring these trends is of first-order importance for the international community.

To help do so, the CPMI will, for the next three years, publish an annual quantitative review based on payment message data that SWIFT has agreed to provide.2 The review includes (i) this commentary, highlighting key trends; (ii) a chartpack; and (iii) the underlying data. It builds on similar analyses by the CPMI and FSB.

2019 CPMI quantitative review of correspondent banking data

The 2019 data confirm that correspondent banking relationships continue to contract in number. Despite the worldwide decline, they continue to play a pivotal role for cross-border payments. The statistics cover monthly payment message data for more than 200 countries and jurisdictions from 2011 to 2019.3 The data set lays out a network of bilateral relationships (either bank-to-bank or country-to-country). From these payment messages, the following measures can be calculated: (i) a cross-border payment message from one country to another identifies a corridor; (ii) a cross-border payment message from one bank to another identifies a correspondent banking relationship; and (iii) the count of active correspondents measures, corridor by corridor, the number of banks abroad that have received messages sent by banks in a given country.4

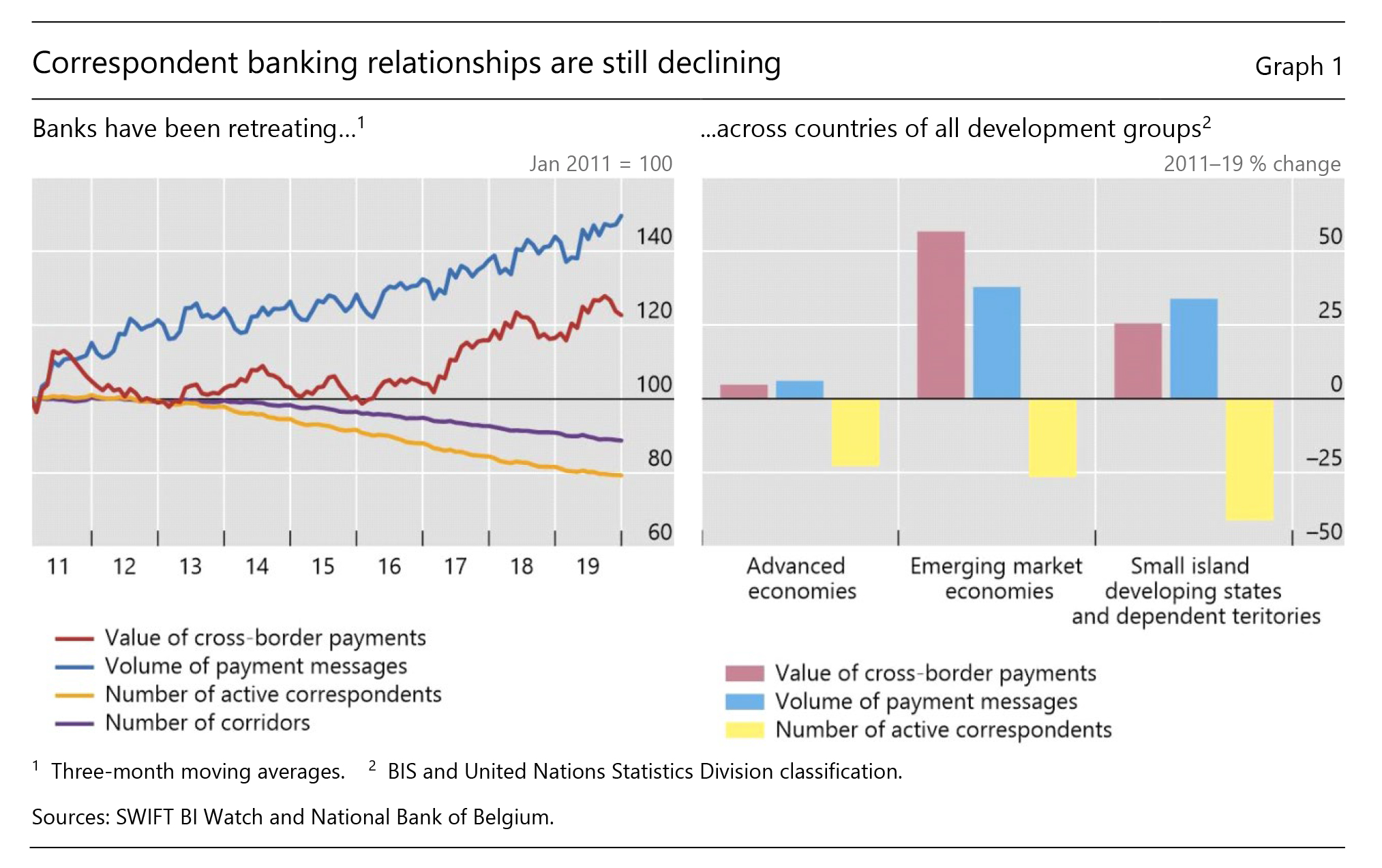

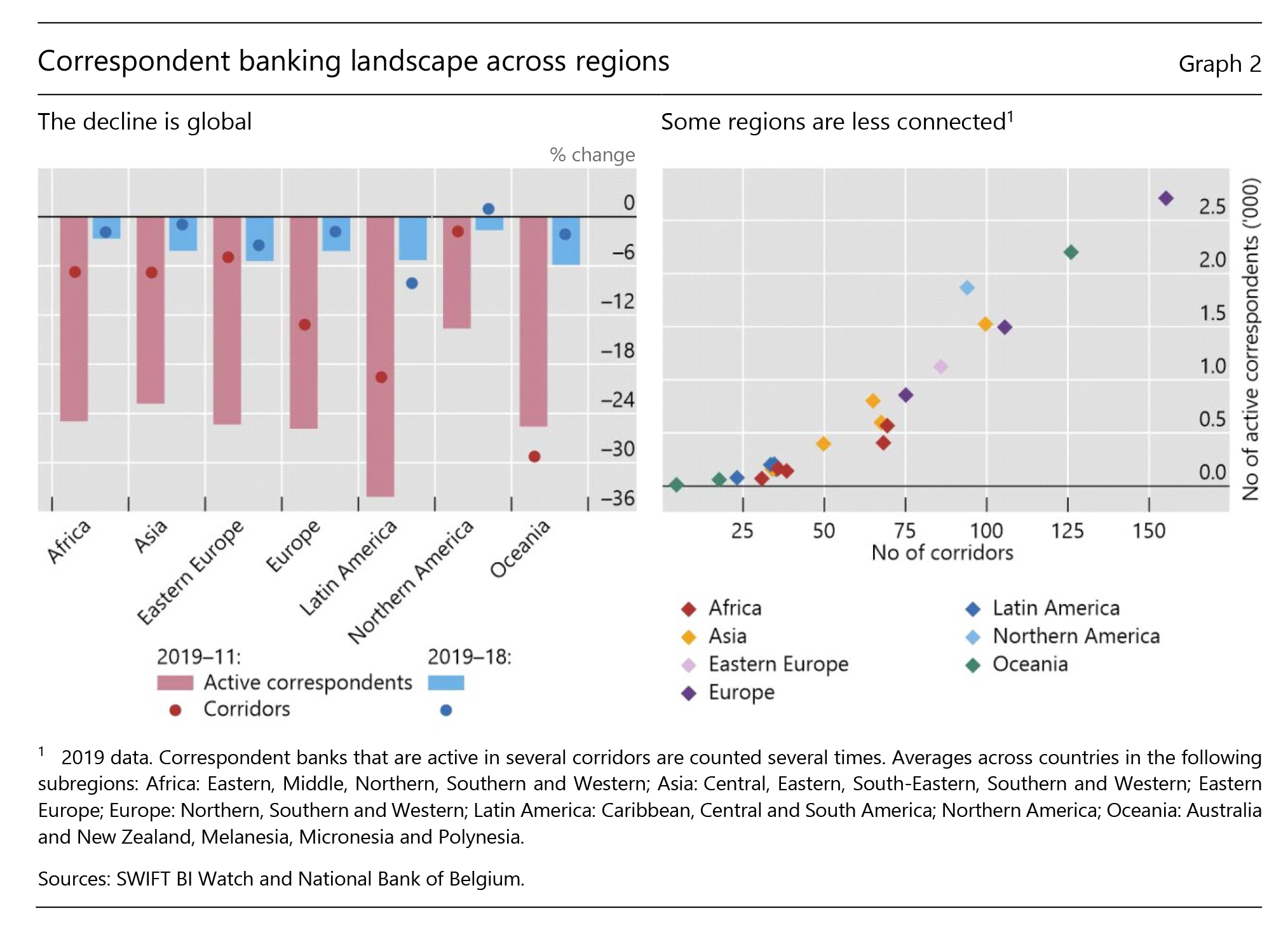

The number of active correspondents worldwide has declined by 22% since 2011 and by 3% since 2018 (Graph 1, left-hand panel). Over the last eight years, the rate of decline has varied across jurisdictions (interactive world map) and is more pronounced in emerging market economies and small island developing states and dependent territories (Graph 1, right-hand panel). The country-level declines range from 23% in advanced economies to 41% in small island developing states and dependent territories. Across regions, the 2011-19 rates of decline range from 13 to 34%, with Northern America at the low end and Latin America at the high end (Graph 2, left-hand panel). In 2019, the region of Oceania saw the largest yearly decline in the number of active correspondents of about 6%, followed by Eastern Europe and Latin America.

A similar but less dramatic decline is seen for the number of corridors. The SWIFT data show that the number has fallen by roughly 12% in eight years and about 2% in 2019-18. (Graph 1, left-hand panel). Here too, the decline is felt more acutely in some regions than others (Graph 2).

Despite the decline in the number of active correspondents and corridors, both the value and volume of cross-border payments processed via correspondent banking networks continued to grow in the last year, by roughly 5% and 4% respectively (Graph 1, left-hand panel). Over the same period (2011-19), emerging market economies saw an increase in the value of cross-border payments via correspondent banking about 10 times larger than that of advanced economies (Graph 1, right-hand panel).

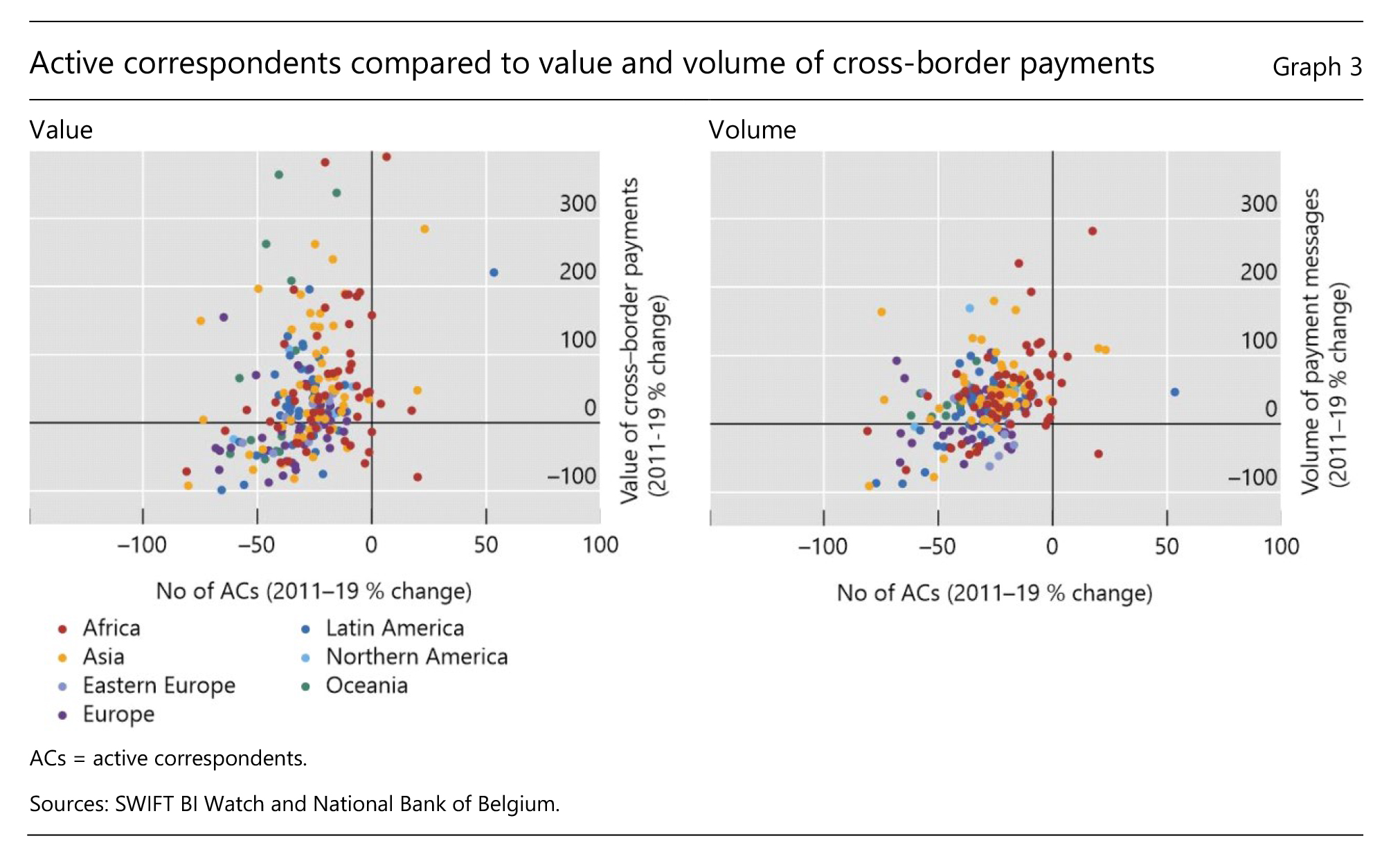

Not surprisingly, the divergence in these trends is widespread (Graph 3). A large share of countries have lost active correspondents even where the value and volume of cross-border payments have increased between 2011 and 2019 (Graph 3, top left-hand quadrants), possibly suggesting continued financial globalisation or the transfer of money via a third country.5 At the same time, some jurisdictions saw a decline in both active correspondents and in value and volume (Graph 3, bottom left-hand quadrants). These countries either sent or received fewer payments altogether, or used cross-border payment infrastructures and arrangements not based on correspondent banking through SWIFT. In 2019, 36 out of 50 territories with the largest decline in active correspondents have been newly added to the list, as compared with the previous year. The majority are small island developing states and dependent territories with very low Transparency International scores.

To investigate these trends, the international community has conducted several studies.6 A recent BIS study examines the drivers and consequences of the retreat of correspondent banks. The study suggests that this retreat might hurt financial inclusion, raise the cost of cross-border payments or drive them to less regulated or unregulated channels. The FSB has published updates on work to assess and address correspondent banking declines. An IMF paper underlines that addressing the correspondent banking decline will take time and would require strengthened, coordinated and collective action on the part of public and private stakeholders.

While the 2020 data will not be available for some time, early indications suggest that the Covid-19 crisis is likely to accelerate changes in correspondent banking landscape.7 Even though the pandemic has limited cross-border movement, the crisis has amplified calls to reinforce coordination and reduce fragmentation in cross-border payment systems.

* This analysis was prepared by Codruta Boar, Committee on Payments and Market Infrastructures.

1 Correspondent banking is an essential component of the global payment system, especially for cross-border transactions. Through correspondent banking relationships, banks can access financial services in different countries and jurisdictions and provide cross-border payment services to their customers. In addition, most payment solutions that do not necessarily involve a bank account at customer level (eg remittances) rely on correspondent banking for the actual transfer of funds (Committee on Payments and Market Infrastructures (2016): Correspondent banking).

2 SWIFT, as the most commonly used messaging platform for cross-border payments, captures a meaningful amount of correspondent banking activity and the data likely deliver an accurate picture of the trends in correspondent banking payment traffic between countries and jurisdictions. Data relating to SWIFT messaging flows is published with permission of S.W.I.F.T. SC. SWIFT © 2020. All rights reserved. Because financial institutions have multiple means to exchange information about their financial transactions, SWIFT statistics on financial flows do not represent complete market or industry statistics. SWIFT disclaims all liability for any decisions based, in full or in part, on SWIFT statistics, and for their consequences.

3 See the data inventory table in the CPMI correspondent banking chartpack.

4 See T Rice, G von Peter and C Boar, On the global retreat of correspondent banks, BIS Quarterly Review, March 2020, pp 37-52.

5 Money transferred via a third country, ie country C, would not be observed in flows between country A and country B.

6 See Financial Stability Board, FSB action plan to assess and address the decline in correspondent banking: Progress report, 2019; International Monetary Fund, Recent trends in correspondent banking relationships - further considerations, Policy Papers, 2017; T Rice, G von Peter and C Boar, On the global retreat of correspondent banks, BIS Quarterly Review, March 2020, pp 37-52.

7 The Covid-19 trends will be available in the 2021 quantitative review of correspondent banking data.