From wealth management products to the bond market

(Extract from page 13 of BIS Quarterly Review, March 2017)

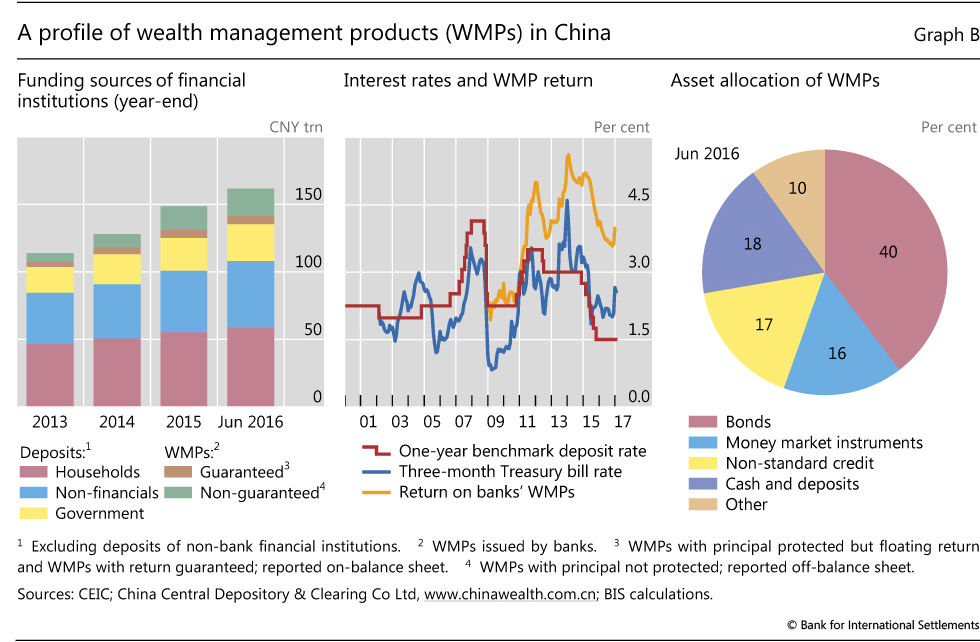

Over the past few years, banks' funding models in China have increasingly relied on wealth management products (WMPs) and corporate deposits (Graph B, left-hand panel). WMPs are saving products, issued by banks or other financial institutions, which offer relatively high returns compared with traditional bank deposits or Treasury bonds (centre panel). Some of these instruments carry principal and even return guarantees from the issuers, and are reported on-balance sheet. But the vast majority do not offer either, and are kept off the issuer's balance sheet. Despite carrying no explicit guarantees, the instruments are widely considered as safe by investors. As of end-June 2016, WMPs issued by banks totalled CNY 26.3 trillion, almost 40% of 2015 GDP. The proliferation of these instruments demonstrates that the traditional demarcations between banks and securities markets are not always clear-cut, and that any regulatory structure needs to take account of the connected nature of the system.

Banks are not only issuers but also buyers of WMPs. Reportedly, large banks often provide wholesale funding to small banks by purchasing their WMPs. Of the above total of CNY 26.3 trillion, about CNY 4 trillion was purchased by other banks. Moreover, large banks provide liquidity to small banks through interbank loans funded with the proceeds of their own issuance of WMPs. These loans made up the bulk of the 16% of money market instruments in the portfolio allocation of WMPs as of the first half of 2016 (Graph B, right-hand panel). These two channels could overlap, as the interbank loans sometimes involve the purchase of WMPs or the pledging of these as collateral.

In order to be able to keep WMPs off their balance sheets, banks often turn to securities firms to manage the funds collected through WMPs. As of last June, around 40% of the aggregate WMP portfolio was invested in the bond market (Graph B, right-hand panel). In order to enhance capital returns, and on the back of ample liquidity, securities firms reportedly leverage up their bond investments by using repurchase agreements. A significant part of these repurchase agreements take place through informal verbal agreements between market players and are not regulated. The upshot is the proliferation of fixed income portfolios with high leverage ratios.

The unwinding of these leveraged portfolios while the wholesale funding market was frozen appears to have led to the bond market stress in mid-December. As bond prices fell while liquidity tightened, the securities firms were forced to sell bonds in order to pay back the small banks, which in turn were facing pressure to repay the loans from larger banks. This eventually led to bond prices falling further as the liquidity squeeze moved through the funding chain.