How have central banks implemented negative policy rates?

Since mid-2014, four central banks in Europe have moved their policy rates into negative territory. These unconventional moves were by and large implemented within existing operational frameworks. Yet the modalities of implementation have important implications for the costs of holding central bank reserves. The experience so far suggests that modestly negative policy rates transmit through to money markets and other interest rates for the most part in the same way that positive rates do. A key exception is retail deposit rates, which have remained insulated so far, and some mortgage rates, which have perversely increased. Looking ahead, there is great uncertainty about the behaviour of individuals and institutions if rates were to decline further into negative territory or remain negative for a prolonged period.1

JEL classification: E42, E58, G21, G23.

With policy rates close to zero in the aftermath of the Great Financial Crisis, several central banks around the world have introduced unconventional policies to provide additional monetary stimulus. One example is the decision by five central banks - Danmarks Nationalbank (DN), the European Central Bank (ECB), Sveriges Riksbank, the Swiss National Bank (SNB) and most recently the Bank of Japan (BoJ) - to move their policy rates below zero, traditionally seen as the lower bound for nominal interest rates. The motivations behind the decisions differed somewhat across jurisdictions, leading to differences in policy implementation.

This feature reviews the experience of the four central banks in Europe that have kept their policy rates below zero for more than one year, focusing exclusively on the technical aspects of the implementation of negative policy rates, their impact on the money market and their transmission to other interest rates. The feature does not address the broader question of whether negative rates are desirable as a policy strategy, as this would call for a broader analysis of their impact on the financial system and the macroeconomy. For instance, more recently their debilitating impact on banks' resilience through undermined profitability, coming on the heels of persistently ultra-low interest rates, has emerged as an important constraining factor.

The remainder of the feature is organised as follows. The first section describes the economic context for the introduction of negative policy rates, while the second looks at their technical implementation. The third section assesses the transmission of negative policy rates to money markets and other interest rates. The penultimate section takes stock of the factors that determine the lower bound for nominal interest rates. In concluding, the feature highlights a number of potential risks associated with using negative policy rates going forward.

Context for negative policy rates

While the ECB, SNB, DN and Riksbank all introduced negative interest rates in mid-2014 and early 2015 (Box 1), and all faced a challenging macroeconomic environment, their respective motivations differed somewhat. In some cases the central banks' declared objective was to counter a subdued inflation outlook, while in others they focused on currency appreciation pressures in the context of bilateral pegs or floors on their exchange rates.

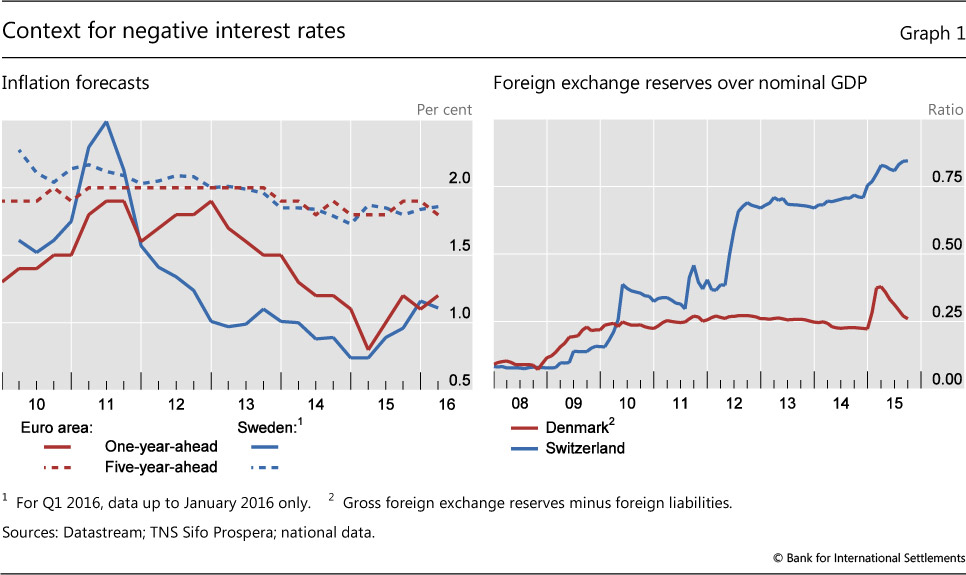

The ECB moved its deposit rate into negative territory in mid-2014 to "underpin the firm anchoring of medium to long-term inflation expectations" (Draghi (2014)). Similar concerns led the Riksbank to implement negative interest rates starting in the first quarter of 2015 (Graph 1, left-hand panel). The aim was "safeguarding the role of the inflation target as a nominal anchor for price setting and wage formation" (Sveriges Riksbank (2015)). Negative interest rates in both cases complemented other unconventional measures. The ECB resumed its purchases of covered bonds and expanded its asset purchase programme to include government bonds and asset-backed securities. It also provided additional term funding to banks through targeted longer-term refinancing operations (TLTROs). The Riksbank began bond purchases that by mid-2016 are set to cover just over 30% of outstanding nominal government bonds, a proportion somewhat larger than the ECB's programme.2

The euro area's new wave of monetary easing added to the appreciation pressure on the Swiss franc, which in 2011 had led the SNB to impose a floor vis-à-vis the euro. To stem the inflow of funds (Graph 1, right-hand panel) and maintain the floor, the SNB announced the introduction of negative interest rates (-0.25%) on sight deposit account balances in December 2014 (effective 22 January 2015). In mid-January, with pressure on the franc unabated, the SNB discontinued the minimum exchange rate and lowered the interest rate on sight deposit accounts further to -0.75%. The goal was to discourage capital inflows and thereby counter the monetary tightening due to the Swiss franc's appreciation. Still, pressure on the currency persisted and the SNB continued to accumulate foreign exchange reserves into the second half of 2015.

Following the SNB decision, DN, which maintains a nearly fixed exchange rate vis-à-vis the euro, saw a surge in demand for Danish kroner and intervened heavily in the FX market (Graph 1, right-hand panel). Moreover, the central bank cut the key monetary policy interest rate from just below zero to -0.75% in early 2015.3 These measures stabilised the krone, and, towards the end of February 2015, the inflow of funds ceased. Over the course of 2015, the situation gradually normalised, and DN sold part of the foreign exchange it had acquired back into the market. In January 2016, DN raised the key policy rate to -0.65%, thus narrowing the policy rate spread vis-à-vis the euro area.

Technical implementation of negative policy rates

The implementation of negative policy rates took place by and large within existing operational frameworks. The SNB had to change its terms of business to implement negative policy rates. Prior to December 2014, remuneration of reserves (positive or negative) was not part of the contractual framework for sight deposit accounts. Moreover, the SNB put in place individual exemption thresholds for sight deposit accounts so that only reserve holdings above the threshold earn negative interest (Box 2).

Even though wholesale changes were not needed at the other central banks, substantial "behind-the-scenes" work took place in every jurisdiction. Each central bank conducted an in-depth review of its IT systems as well as of its documentation and account rules. And several minor adjustments were made. Moreover, the central banks carefully signalled the possibility of negative interest ahead of time in order to prepare both financial institutions and the public at large.

Implementation modalities beyond the negative policy rates themselves have important implications for the costs to banks of holding central bank liabilities. In each case, the marginal remuneration of an additional unit of reserves differs from the average remuneration rate.

Box 1

Moving into negative territory

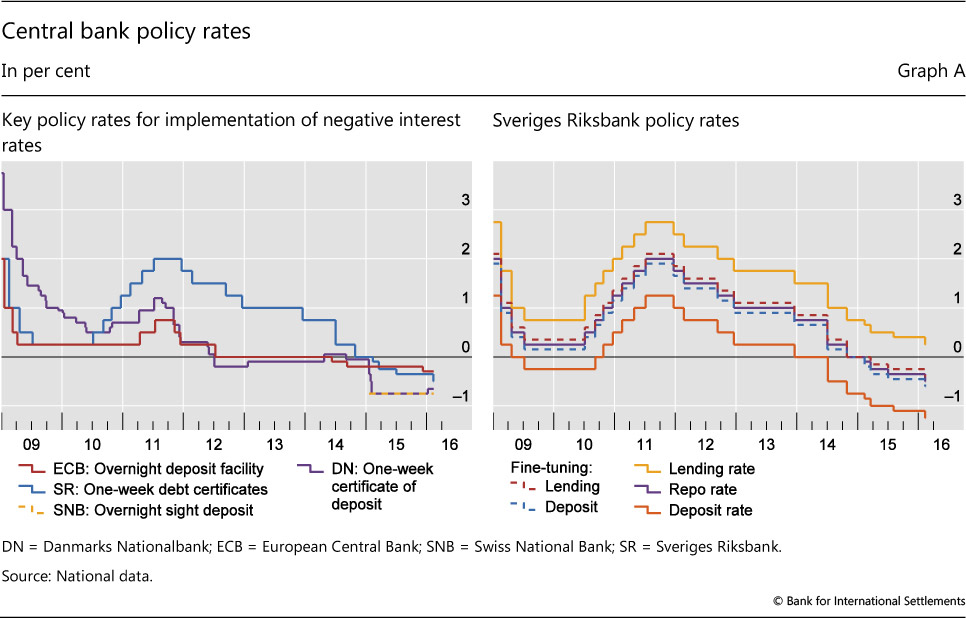

Danmarks Nationalbank (DN), the European Central Bank (ECB), Sveriges Riksbank and the Swiss National Bank (SNB) all cut their key policy rates to below zero over the period from mid-2014 to early 2015 (Graph A, left-hand panel). The ECB moved first, on 11 June 2014, when it cut the deposit rate to -10 basis points after having signalled the possibility for at least a year. DN followed on 5 September 2014, when the rate on certificates of deposit was cut from +5 to -5 bp following a further rate cut by the ECB. The SNB went negative on 18 December 2014 when it announced that sight deposits exceeding a certain threshold would earn -25 bp effective 22 January 2015. The Riksbank cut its repo rate to -10 bp on 18 February 2015, whereas the Bank of Japan announced on 29 January 2016 that it would apply a rate of -10 bp to part of the balances in current accounts.

In Europe, central banks took more than one step into negative territory. The ECB lowered its deposit rate to -20 bp in September 2014 and further to -30 bp in December 2015, while the SNB announced a further 50 bp cut on 15 January 2015 in connection with the discontinuation of the minimum exchange rate vis-à-vis the euro. Appreciation pressure on the Danish krone led to four successive rate cuts over a period of two and half weeks that took DN to -75 bp in early February 2015. A reversal of the pressure on the krone led to an increase to -65 bp in early 2016. For its part, the Riksbank cut to -25 bp in March 2015, and further to -35 bp in July and -50 bp in February 2016.

However, negative policy rates were not entirely new. The Riksbank had flirted with negative policy rates in 2009-10 (Graph A, right-hand panel). The repo rate was cut to 25 bp on 8 July 2009 and the overnight deposit rate was lowered to -25 bp in order to keep the interest rate corridor symmetrical at +/-50 bp. Still, the amount of funds on deposit overnight was minuscule, as the Riksbank typically uses daily fine-tuning operations (at 10 bp below the repo rate) to drain most excess liquidity prior to the close of business. DN had maintained negative certificate of deposit rates from mid-2012 to April 2014.

Box 2

Design of remuneration schedules

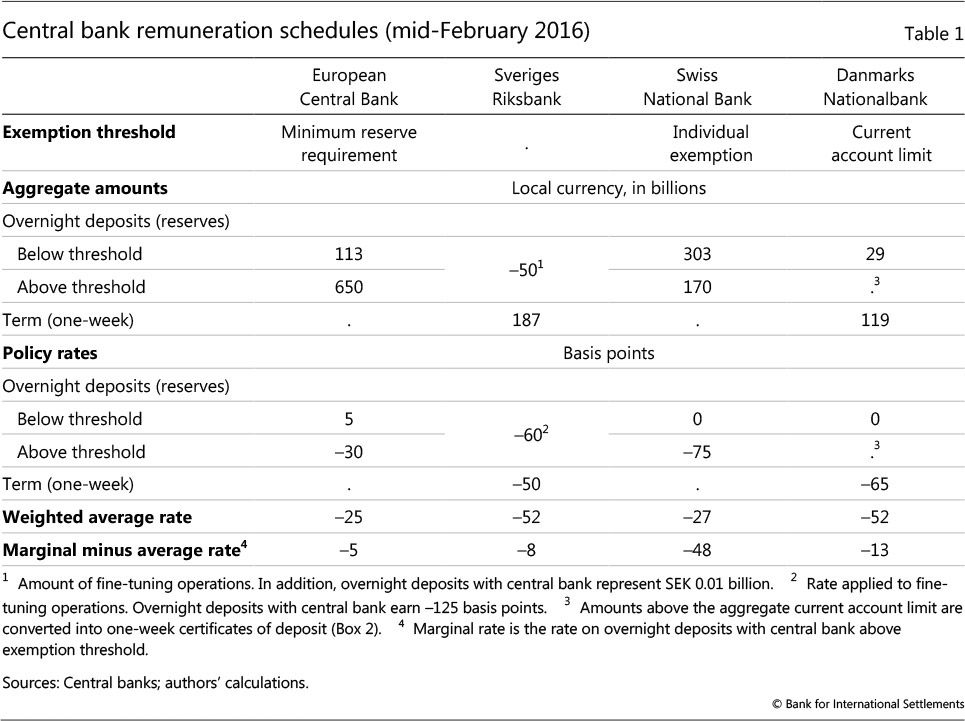

In general, the four central banks are applying negative rates to the majority of accounts on their books with a view to limiting the potential for arbitrage between accounts.

The ECB, DN and SNB use some combination of exemption thresholds in computing the negative remuneration. The design and calibration of the remuneration schedules reflect a combination of the policy goals and the existing implementation frameworks. The SNB's exemption thresholds are determined in one of two ways. The first approach applies to all banks that have to fulfil minimum reserve requirements. This exemption threshold currently corresponds to 20 times the minimum reserve requirement prior to implementation (a static component) minus/plus any increase/decrease in the amount of cash held (a dynamic component). The dynamic component aims to prevent account holders from substituting cash for sight deposits. The second approach defines a fixed exemption threshold for all account holders not subject to the minimum reserve requirement. The minimum fixed threshold is CHF 10 million, a level chosen so as not to inhibit an institution's ability to settle Swiss franc payments.

While new for the SNB, tiered remuneration was already part of the operational framework at the other three central banks. In the Eurosystem, required reserves earn the Main Refinancing Operations (MRO) rate - currently at 5 basis points - whereas excess reserves currently "earn" -30 bp. In Denmark, the central bank offers one-week certificates of deposit funds with a yield currently at -65 bp. In contrast, overnight demand deposits in the current account earn zero. Both an aggregate limit and individual limits have been set on the amount of funds that can be held in the current accounts. If the aggregate limit is exceeded at the end of the day, then deposits exceeding the individual limits are converted into certificates of deposit. In addition to interest rates, DN has actively varied the current account limits - most recently increasing them in March 2015, and then lowering them in August 2015 and January 2016.

In Sweden, the Riksbank currently issues one-week debt certificates. Moreover, daily fine-tuning operations aim to drain any remaining reserves prior to the close of business, and hence banks hold only small amounts as overnight deposits with the central bank. At the moment, one-week debt certificates "yield" -50 bp and fine-tuning operations earn -60 bp, while any residual amounts left in the current account face a negative "remuneration" of -125 bp.

With the move below zero, the Bank of Japan adopted a remuneration schedule that will divide balances in the current accounts of financial institutions into three tiers. The three tiers are remunerated at +10 bp, 0 bp and -10 bp, respectively.

For government deposits, the treatment varies. In Switzerland, the sight deposits of the Federal Administration are exempt but balances are being monitored. In Denmark, government deposits earn negative interest only above a certain threshold; whereas in the euro area, government accounts are de facto subject to negative rates due to de minimis exemptions. In Sweden, the Riksbank has not been the government's bank since 1994.

The structure of liabilities and of their remuneration differs across central banks. In each jurisdiction, the banking system currently holds reserves and other central bank liabilities above required amounts ("liquidity surplus"). In the euro area and Switzerland the liquidity surplus is held as overnight deposits (reserves), whereas in Denmark and Sweden the central banks use a combination of overnight and one-week liabilities. In addition, the ECB, DN and SNB all exempt at least part of the reserve holdings from negative interest rates (Box 2).

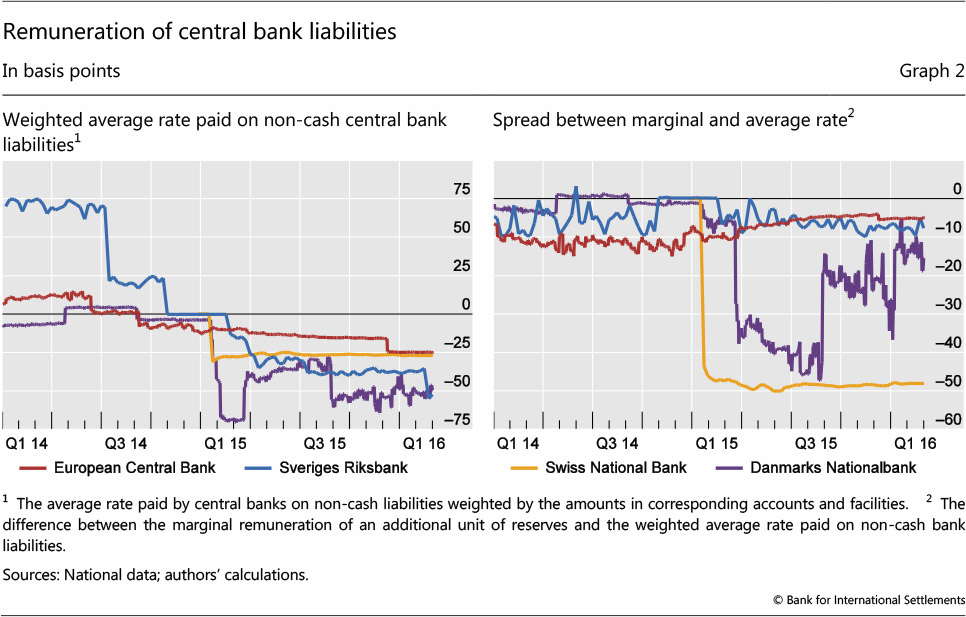

As illustrated in Table 1 and Graph 2 (left-hand panel), the average remuneration rate on central banks' liabilities depends not only on the different policy rates, but also on the exemption thresholds. In mid-February 2016, the average rates were lowest at the Danish and Swedish central banks at just above - 50 basis points. In comparison, the average rates at the SNB and ECB were around - 25 basis points. Thus, the average remuneration was not necessarily the lowest in the jurisdictions with the most negative policy rates.

Since going negative, the spread between marginal and average costs ranged from -11 to -47 basis points in Denmark, as the central bank actively adjusted its policy stance by varying the exemption thresholds. In contrast, the spread was mostly constant for the other three central banks (Graph 2, right-hand panel). For Switzerland, the spread has been around -50 basis points, whereas it was approximately -5 and -8 basis points for the ECB and the Riksbank, respectively.

Market functioning

The experience so far suggests that modestly negative policy rates are transmitted to money market rates in very much the same way as positive rates are. However, questions remain as to whether negative policy rates are transmitted to the wider economy through lower lending rates for firms and households, especially in rates associated with bank intermediation. Institutional and contractual constraints may create a discontinuity at the zero rate and impede the pass-through beyond money markets. Before addressing these broader issues of efficacy, we first examine the transmission of negative policy rates to the money markets.

Money markets

Overall, so far the introduction of modestly negative policy rates does not appear to have affected the functioning of money markets much. The pass-through to short-term money market rates has persisted, and the impact on trading volumes, which are already very low because of the abundant and cheap supply of reserves by central banks, appears in general to have been small.

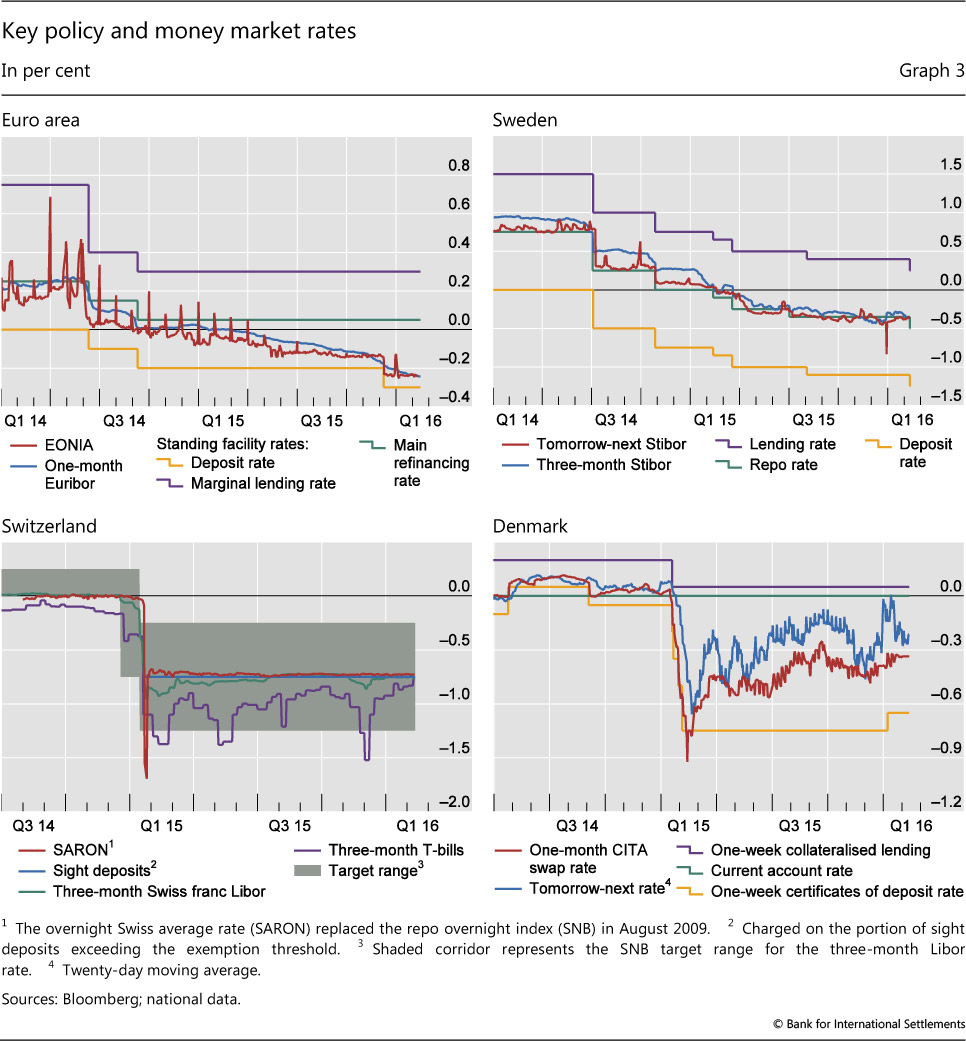

In all four jurisdictions, the overnight rate has followed the policy rate below zero. Moreover, the negative policy rates have passed through to other money market rates (Graph 3).

In the euro area and Switzerland, money market rates track the central bank deposit rate. In Sweden, money market rates closely follow the repo rate. In Denmark, the relationship has been somewhat less tight. On some days the tomorrow-next rate is close to the current account rate of zero, whereas on other days it is closer to (or even below) the certificate of deposit rate. This volatility results from a thin market, where on some days pricing can be driven by banks whose reserve holdings do not exceed their limit and earn a higher current account rate (Andersen et al (2015)).

In terms of money market volumes, experiences vary. In the euro area, money market volumes were stable after the ECB's deposit rate went negative in mid-2014. However, volumes have dropped across all maturities as excess liquidity in the banking system has increased. Anecdotal evidence suggests that banks seek to avoid negative rates by either extending maturities or lending to riskier counterparties. While negative rates may have improved market access for banks in the periphery countries of the euro area, other explanations for increased access are also possible - not least the introduction of the Single Supervisory Mechanism, its efforts to improve the health of balance sheets, and stronger economic and financial conditions. In Denmark, the turnover in the (unsecured) money market has declined since the introduction of negative interest rates. This decrease reflects, in part, the higher amounts that banks were allowed to deposit "on demand" in their current accounts.

In contrast, trading in the Swiss (secured) money market has increased moderately. This increase in activity is a mechanical effect of the new individual exemption thresholds, as banks reshuffle reserves among themselves. Banks that hold levels of reserves below their exemption threshold are willing to borrow reserves up to that threshold, whereas those that hold levels of reserves above theirs are keen to lend. At the outset the exemption thresholds were not fully exploited, but over time a redistribution of reserves has taken place and this has led to a decrease in the non-exploited exemption thresholds. Most of this "reshuffling" is overnight.

Problems with money market instruments designed with only positive interest rates in mind have so far not materialised. For example, there is no evidence that repo market counterparties have strategically failed to deliver collateral to delay receiving cash.4 And constant net asset value (NAV) money market funds in the euro area designed contractual provisions that work around NAV falling below 1 because of the simple pass-through of negative money market rates.5 The returns on these funds remained positive throughout the first half of 2015 as they lengthened the maturity in search of higher yields, but became systematically negative by the end of the year. A further shift from constant to variable NAV may be possible.

Transmission beyond money markets

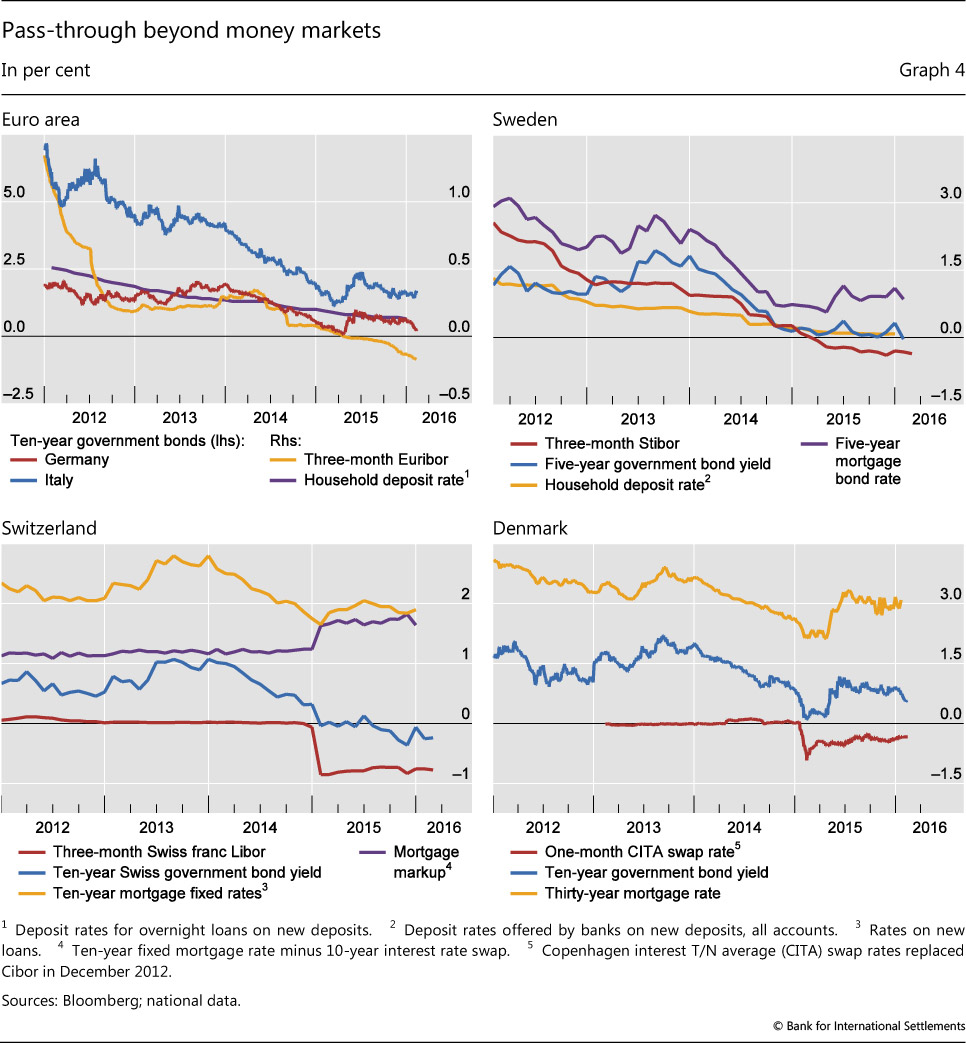

The initial introduction of negative policy rates coincided with a decrease in longer-maturity and higher-risk yields, although simultaneous central bank asset purchase programmes and other factors behind the fluctuations in the risk premium make it difficult to isolate the effect of negative policy rates alone (Graph 4). In terms of operational matters, market participants initially faced some uncertainty related to how negative rates would be treated in connection with outstanding securities or existing contract types. A particular concern was the treatment of negative coupons in floating rate instruments and the ability for market infrastructures to accommodate negative interest rates.

In Switzerland, banks and other financial institutions, in general, adjusted their terms of business or financial contracts prior to the implementation of negative policy rates by, for example, introducing a zero lower bound on Libor-based mortgages. In Denmark, government-led working groups had to clarify both the tax treatment and the mechanics of dealing with negative mortgage bond coupons.6 In Sweden, elements of the clearing and settlement system were not designed to deal with negative coupon payments and had to be modified.

These technical issues have for the most part been resolved, and instances of market operational issues have been limited. In part, this is because, once spreads over the contractual reference rates are added, the resulting interest rates are less likely to be negative at current modestly negative policy rates. Nonetheless, new market practices can vary across individual banks and legal jurisdictions, including within the euro area, creating a risk of market segmentation.

Initially, there was some uncertainty as to how banks would treat their "wholesale" depositors, but they are now passing on the costs in the form of negative wholesale deposit rates. In some cases, banks have used exemption thresholds akin to those that central banks have applied to their reserves.

The key exception in terms of transmission has been banks' reluctance to pass negative rates through to retail depositors. This reaction was motivated by the concern, shared by some central banks, that negative deposit rates would lead to substantial deposit withdrawals. In Switzerland, banks have responded to lower lending margins in some business lines by adjusting other selected lending rates upwards. In particular, Swiss banks have raised the lending rate on mortgages, even as government and corporate bond yields fell in line with the money market rates (Graph 4, bottom left-hand panel).7

The Swiss experience points to a fundamental policy tension if the intention of negative policy rates is to transmit negative interest rates to the wider economy. If negative policy rates do not feed into lending rates for households and firms, they largely lose their rationale. On the other hand, if negative policy rates are transmitted to lending rates for firms and households, then there will be knock-on effects on bank profitability unless negative rates are also imposed on deposits, raising questions as to the stability of the retail deposit base. In either case, the viability of banks' business model as financial intermediaries may be brought into question. The dilemma is less acute if the objective is to influence the exchange rate. In this case, however, other thorny issues arise, not least that of cross-border spillovers.

Institutional constraints may also create a demand for instruments with interest payments floored at zero. Investors, notably insurers, may be unwilling or unable to buy negative cash flow securities, and banks issuing covered bonds have often included an interest floor at zero in the documentation or assumed one implicitly. Such floors can weaken the link between the cash flows of floating rate loans, bonds issued by banks to finance them, and the interest rate swaps that are used to hedge the associated exposures and pass through negative interest payments. The resulting hedging difficulties have led to an increase in the demand for new instruments - for example, Euribor options with 0% strikes that cover the residual risk arising from the floor.

Technically, where is the effective lower bound?

Some other central banks close to the zero bound have adopted or have been considering negative policy rates. At the end of January 2016, the Bank of Japan announced that, "in order to achieve the price stability target of 2 percent at the earliest possible time" (Bank of Japan (2016)), remuneration of -0.10% would apply to any future increases in reserves.8 In December 2015, the Bank of Canada made an explicit reference to this possibility and changed its estimate of the lower bound for its policy rate from 0.25% to -0.50% (Bank of Canada (2015)). Still, questions regarding the specific implementation and the technically effective lower bound remain open.

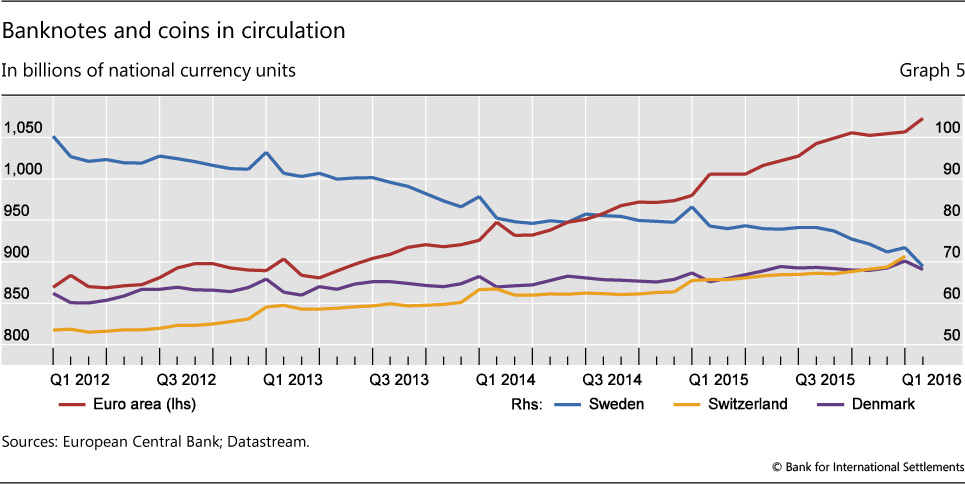

The possibility of earning zero nominal interest by storing value in physical currency is the primary motivation for the concept of the zero lower bound in the academic literature.9 So far, negative policy rates have not led to an abnormal jump in the demand for cash across the four European jurisdictions under review (Graph 5), although this may be due to that fact that retail depositors have been shielded from negative rates so far. In the case of Denmark, the euro area and Switzerland, cash demand had already been on an increasing trend, in part because rates were already very low. Given transport, storage, insurance and other costs associated with holding cash in size, the effective lower bound on nominal interest rates is somewhere below zero.

The effective lower bound is, however, likely to move up if interest rates remain, or are expected to remain, negative for a long time. Agents may start adapting to the new environment and begin to innovate with a view to reducing the costs associated with physical currency use (eg McAndrews (2015)). Moreover, some of the costs of increasing cash usage are fixed, and incurring those may become profitable if interest rates are expected to remain negative for long.

As alluded to above, the fact that retail bank customers have so far been shielded from negative rates has probably played a key role in keeping the demand for cash stable. The ability of the banking sector to limit the pass-through of negative rates is thus an important factor determining the effective lower bound (Alsterlind et al (2015)). Central banks' efforts to limit the cost of negative remuneration on the banking system were in some cases aimed at maintaining this ability. Other institutional factors, such the prevalence of adjustable rate mortgages and more generally floating rate debt, can broaden agents' exposure to negative rates and affect the technical room central banks have to move interest rates into negative territory.

Conclusions

The introduction of moderately negative policy rates by the four central banks under review was by and large achieved within their existing operational frameworks. The experience so far suggests that modestly negative policy rates are transmitted through to money market rates in much the same way as positive rates are. It also appears that they are transmitted to longer-maturity and higher-risk rates, although this assessment is clouded by the impact of complementary monetary policy measures. By contrast, so far retail deposit rates have remained insulated, partly by design. And, at least in Switzerland, negative rates have actually raised, rather than lowered, mortgage rates.

So far, zero has not proved to be a technically binding lower limit for central bank policy rates. Nonetheless, there is great uncertainty about the behaviour of individuals and institutions if rates were to decline further into negative territory or remain negative for a prolonged period. It is unknown whether the transmission mechanisms will continue to operate as in the past and not be subject to "tipping points". Furthermore, an extended period of negative interest rates has so far been limited to the euro area and neighbouring economies. It is not clear how negative policy rates would play out in other institutional settings.

This special feature has examined exclusively the technical aspects of the implementation of negative policy rates. It has not addressed the question of the impact of negative policy rates on the financial system as a whole. Many questions remain. For instance, more recently, the debilitating impact of persistently negative interest rates on the profitability of the banking sector has emerged as an important consideration (BIS (2016)). Even more directly, such rates can weaken the profitability and/or soundness of institutions with long-duration liabilities, such as insurance companies and pension funds, seriously challenging their business models.10 And an assessment of their desirability would necessarily require an evaluation of their effectiveness in achieving the central bank objectives as well as their more general impact on financial and macroeconomic stability.11 This, however, is beyond the scope of this special feature.12

References

Alsterlind, J, H Armelius, D Forsman, B Jönsson and A-L Wretman (2015): "How far can the repo rate be cut?", Sveriges Riksbank, Economic Commentaries, no 11.

Andersen, M, M Kristoffersen and L Risbjerg (2015): "The money market at pressure on the Danish krone and negative interest rates", Danmarks Nationalbank, Monetary Review, 4th Quarter.

Bank of Canada (2015): "Bank of Canada updates framework for unconventional monetary policy measures", press release, 8 December.

Bank for International Settlements (2015): 85th Annual Report, June.

--- (2016): "Uneasy calm gives way to turbulence", BIS Quarterly Review, March, pp 1-14.

Bank of Japan (2016): "Introduction of 'quantitative and qualitative monetary easing with a negative interest rate'", press release, 29 January.

Borio, C (2015): "Revisiting three intellectual pillars of monetary policy received wisdom", speech at the Cato Institute, 12 November, forthcoming in the Cato Journal.

Borio, C, L Gambacorta and B Hofmann (2015): "The influence of monetary policy on bank profitability", BIS Working Papers, no 514, October.

Caruana, J (2016): "Persistent ultra-low interest rates: the challenges ahead", speech at the Bank of France-BIS Farewell Symposium for Christian Noyer, Paris, 12 January.

Committee on the Global Financial System (2011): "Fixed income strategies of insurance companies and pension funds", CGFS Papers, no 44, July.

Domanski, D, H S Shin and V Sushko (2015): "The hunt for duration: not waving but drowning?", BIS Working Papers, no 519, October.

Draghi, M (2014): "Introductory statement to the press conference", 4 December.

Fleming, M and K Garbade (2004): "Repurchase agreements with negative interest rates", Federal Reserve Bank of New York, Current Issues in Economics and Finance, vol 10, no 5, April.

Friedman, M (1969): The optimum quantity of money, Macmillan.

Hicks, J (1937): "Mr Keynes and the 'Classics'; a suggested interpretation", Econometrica, vol 5, no 2, April.

McAndrews, J (2015): "Negative nominal central bank policy rates - where is the lower bound?", Federal Reserve Bank of New York, speech at the University of Wisconsin, 8 May.

Rognlie, M (2015): "What lower bound? Monetary policy with negative interest rates", working paper, 23 November.

Sveriges Riksbank (2015): "Riksbank cuts repo rate to −0.25 per cent and buys government bonds for SEK 30 billion", press release, 18 March.

Working Group on Negative Mortgage Rates (2015): "Negative mortgage rates", Danish Ministry of Business and Growth report.

1 The authors would like to thank Meredith Beechey Österholm, Matthias Jüttner, Benjamin Müller, Holger Neuhaus, Frank Nielsen and Marcel Zimmermann for valuable discussions, and Claudio Borio, Ben Cohen (the editor) and Dietrich Domanski for comments. The views expressed are those of the authors and do not necessarily reflect those of the Bank for International Settlements (BIS) or the Markets Committee.

2 While the Riksbank has no exchange rate operational target, it has stated that it is prepared to intervene on the foreign exchange market if the krona's appreciation threatens price stability. On 4 January 2016, its executive board took a delegation decision enabling immediate intervention on the foreign exchange market as a complementary monetary policy measure.

3 On the recommendation of Danmarks Nationalbank, the Ministry of Finance also temporarily suspended issuance of Danish government bonds.

4 Fleming and Garbade (2004) discuss the strategic fails in the context of negative special repo rates.

5 For example, under the Reverse Distribution Mechanism, investors' shares are cancelled in proportion to the reduction in value due to negative interest rates, allowing the NAV to remain constant.

6 The Danish Ministry of Business and Growth has chaired a working group with the participation of the Danish financial sector to analyse the different aspects related to negative mortgage rates. Its findings were published in Working Group on Negative Mortgage Rates (2015).

7 In Denmark, where mortgage loans are primarily financed with pass-through bonds rather than deposits, mortgage rates fell together with money market rates and government bond yields. However, bank lending rates for new loans to non-financial corporations edged up in 2015.

8 Under its Quantitative and Qualitative Monetary Easing programme, the Bank of Japan is buying assets to increase the monetary base by about ¥80 trillion annually.

9 See eg Hicks (1937): "If the cost of holding money can be neglected, it will always be profitable to hold money rather than lend it out, if the rate of interest is not greater than zero. Consequently the rate of interest must always be positive."

10 For a more detailed analysis, see Borio et al (2015), CGFS (2011) and Domanski et al (2015).

11 In addition, Friedman (1969) argues that non-zero nominal interest rates lead to a suboptimal quantity of money. In the case of negative nominal interest rates, the holders of physical currency, who receive a nominal return of zero, benefit from an implicit subsidy. See also Rognlie (2015).

12 For a sceptical view concerning their desirability, see BIS (2015), Borio (2015) and Caruana (2016).