John Iannis Mourmouras: The political economy of Europe's monetary union - an update

Speech by Professor John Iannis Mourmouras, Deputy Governor of the Bank of Greece, at the European Public Law Organization, Sounio, 30 August 2017.

Introduction

It is my great pleasure to be here with you today at the EPLO Academy, near Cape Sounion, where the famous ancient Temple of Poseidon, the god of the sea, rests (built in the 5th century BC). I am grateful to the President of EPLO Professor Spyridon Flogaitis for his kind invitation to deliver this inaugural lecture.

It seems that Poseidon is in no good mood today, it's quite windy in Sounio!

My speech today will be structured in three sections: I will firstly talk about the political economy of the European Union, giving a more detailed picture of the EU's political, institutional and economic landscape, as it has been shaped so far. In the second section, I intend to take a brief look into the EU's major policies including monetary policy, with particular reference to the role of the ECB and the debate on an exit strategy from the ECB's ongoing accommodative policies. Finally, I will offer some brief remarks about Greece's place in the eurozone in the post-MoU era.

As most of the participants in the EPLO's Academy are of purely legal background, it is my intention to keep to the legal and institutional aspects of the topics of my speech and spare you the economic and financial ins and outs of the EU's economic policies, which, as you may imagine, abound in technical complexity.

1. The political economy of the European Union

1.1 Incomplete architecture - institutional

The euro area is emerging from a deep crisis that has challenged the ability of its macroeconomic policy framework to deliver stability and prosperity. The setup of the Economic and Monetary Union, as initially conceived and laid down in the 1997 Maastricht Treaty, has proven unsustainable and unstable. The global financial crisis which began 10 years ago and led to the European Union's worst recession in its six-decade history, did not start in Europe, but EU institutions and Member States had to take unprecedented action to counter its impact and address the shortcomings of the original design of the Economic and Monetary Union. Important lessons have been drawn as a result of the crisis, with new legislation, policy instruments and institutions put in place to strengthen the governance of the euro area, as we will examine in more detail in the following sections of my speech.

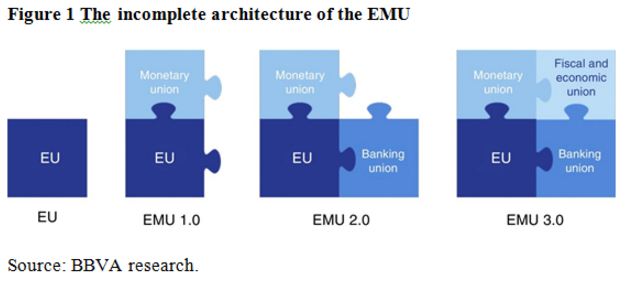

As robust as it may be today, the EMU remains incomplete. The "monetary" component of the EMU is successfully developed, as illustrated by the role of the European Central Bank (ECB). However, the "economic" component is still lagging behind, with less integration at EU level hampering its ability to support fully the euro area's single monetary policy, but also national economic policies. There is a need to strengthen the political will across the board, among Member States, between Member States and EU institutions, and restore the confidence of the general public. There should be no complacency about the need to strengthen EMU architecture.

1.2 Union in diversity

First and foremost, we need to remind ourselves that the political economy of the EU concerns a Union of 28 Member Stateswith different economic histories, diverse financial systems, credit and regulatory philosophies. Yet, the integration of financial markets and their corresponding regulation have been considered central to achieving a European single market since at least the 1980s. In this context, the governance of EU financial services has gradually moved from the national to the European level under the complementary dynamic of the effective internationalisation of capital. As banking and finance progressively internationalised, EU member state governments have had to open up to pan-European initiatives; otherwise, it was feared that European economies would become increasingly marginalised in global capital markets. Another force that pushed towards European financial integration is a recurrent theme in the history of the EU: crisis-driven regulatory responses, i.e. when Member State governments and economic actors look to Europe for solutions to comparative problems affecting them all. Under extraordinary circumstances such as the recent crisis that the EU experienced, the supranational regulation of financial services represents the best solution to deal with the challenges posed by the internationalisation of capital.

Allow me here to make a small digression to remind you how important European law, and the contribution of legal experts such as yourselves, is for further integration in the creation of new law based on the two cornerstones of EU action. Indeed, any integratory step towards a fiscal and economic union must take heed of the subsidiarity and proportionality principles, which regulate the exercise of powers by EU. More specifically, in areas in which the European Union does not have exclusive competence, the principle of subsidiarity, as laid down in Article 5.3 TEU, defines the circumstances in which it is preferable for action to be taken by the Union, rather than the Member States. The criteria for applying those two principles are set out in Protocol No 2 on the application of the principles of subsidiarity and proportionality annexed to the Treaties.

Article 5.3 of the Treaty on European Union (TEU)

"The Union shall act only if and in so far as the objectives of the proposed action cannot be sufficiently achieved by the Member States, either at central level or at regional and local level, but can rather, by reason of the scale or effects of the proposed action, be better achieved at Union level."

Like the principle of subsidiarity, the principle of proportionality seeks to set actions taken by EU institutions within specified bounds. Under this rule, the action of the EU must be limited to what is necessary to achieve the objectives of the Treaties.

Article 5(4) of the Treaty on European Union (TEU)

"Under the principle of proportionality, the content and form of Union action shall not exceed what is necessary to achieve the objectives of the Treaties."

1.3 Unemployment - growth

In what follows I will give you very briefly some figures and charts about the current macroeconomic conditions in the euro area, more specifically about growth, investment and unemployment in the euro area.

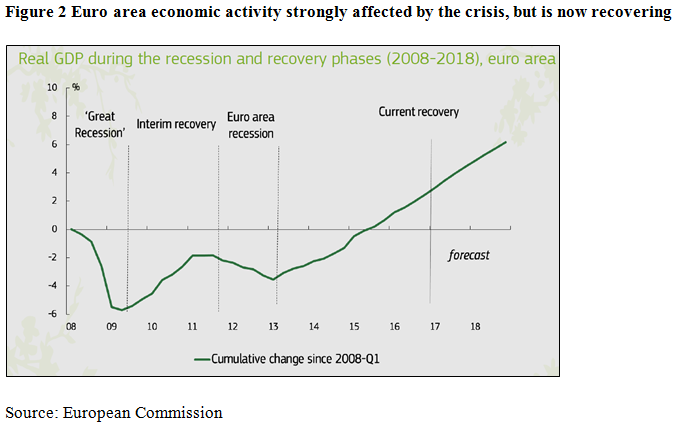

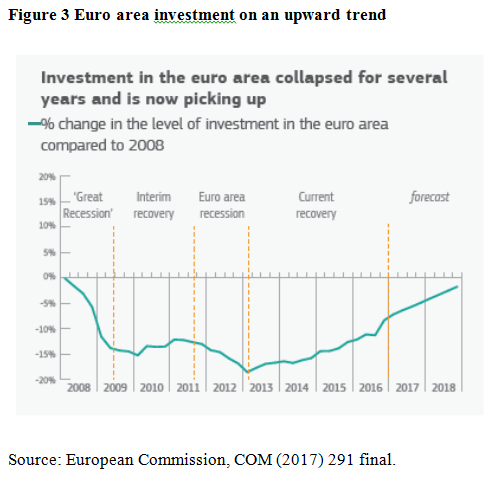

Today, the EU economy is expanding for the fifth consecutive year. Employment is getting close to its pre-crisis peak, as more than 5 million jobs have been created since early 2013 in the euro area. Banks are now stronger and better capitalised, investment is picking up, and public finances are in better shape. Eurozone growth reached an annualized pace of 2.1% in the last quarter, its best level in 5 years, which is considered high by recent standards.

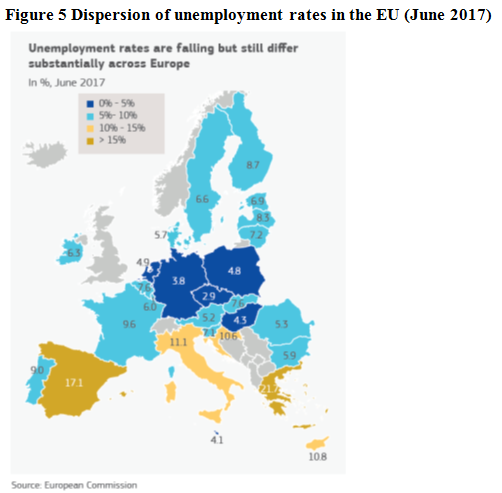

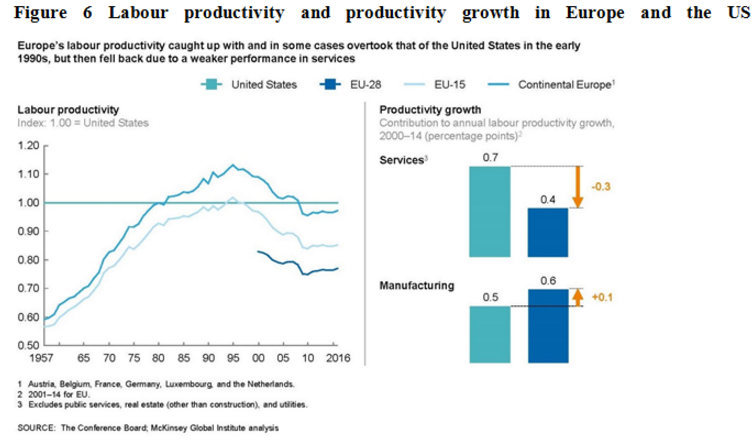

The unemployment rate has been slowly reduced and now stands at its lowest level since 2009 (at around 9% in the eurozone), compared with 12% after the region's debt crisis (see Figures 4 and 5).

.png)

It is true that the protracted economic downturn and divergences between euro area countries have been the result of pre-crisis imbalances and shortcomings in the way the EMU responded to major shocks. The diverging experiences of the Member States after the crisis have renewed the focus on achieving convergence across the EU. Convergence may indeed be important for the cohesion of the monetary union, as it helps to ensure that the gains from economic integration are shared. Countries such as Germany are now well above their pre-crisis GDP levels, but for other countries such as Italy, GDP is only expected to return to its pre-crisis level in the mid-2020s (last quarter GDP 1.5% on a yearly basis).

While recent economic developments are indeed encouraging, a lot remains to be done to overcome the legacy of the crisis years. The euro area is finally witnessing a decent economic recovery, but it would be wrong to be complacent. The single currency remains vulnerable in its institutional architecture, and faces many unresolved problems at the national level. A lack of productivity catch-up - lower productivity growth in countries with lower initial per capita income and productivity - explains much of the lack of income convergence within the euro area. Countries with lower initial productivity levels can have larger productivity gains from labour and product market reforms than countries with higher initial productivity. In light of the above, structural reforms are critical to reducing productivity gaps to foster real income convergence.

All in all, the current situation is much improved, but economic reforms in the goods, capital and labour markets which remove barriers to competition and increase market flexibility are essential for the smooth functioning of the Economic and Monetary Union (EMU). Such reforms are key to raising productivity and employment in the euro area, thereby supporting the growth potential of the euro area in the long run. What is also needed is investment in talent and human resources, on which the European Union is currently lagging behind its major competitors.

1.4 The political landscape: where is Europe headed?

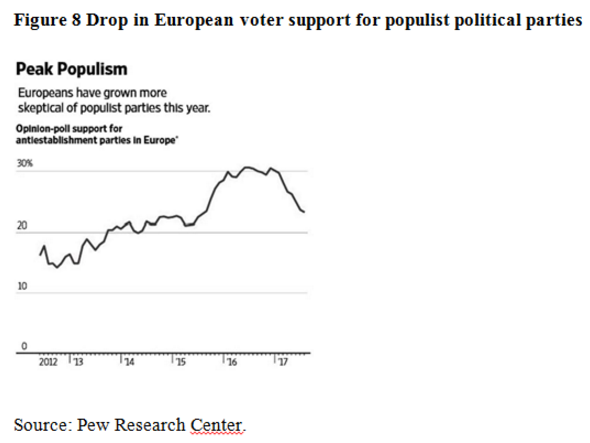

Unlike earlier in the year, when the prospect of a populist far-right turn of the French electorate in the presidential elections in May was a serious cause for concern, political instability is no longer at the top of the agenda for the Member States of the EU. Global markets have been nervous lately, but the source of their worries this time isn't in the eurozone. Instead, political uncertainty has risen around the US, as the White House under President Trump is in turmoil. The UK, meanwhile, is struggling after the 2016 upset vote of the British people to leave the European Union to address the political and economic challenges of Brexit. From an economic point of view, such uncertainty tends to support the euro against the dollar and the sterling pound. From a political point of view, the centre electorate seems to have been unsettled by what is happening in the UK and US and has been frightened off the extremist-populist parties.

There are of course seminal elections ahead in the European continent, in Germany, Europe's biggest economy and the eurozone's dominant power, in September. The likelihood that no major political upsets will come from Germany in September is indeed among a number of forces combining to generate fresh optimism for the European project, which has seen quite a few lows in the past few years.

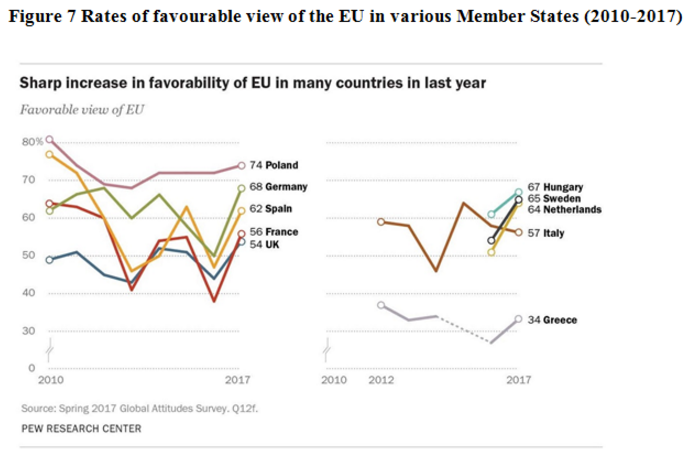

Of course, the German electoral result will influence everything from European relations with the US, China, Russia and Turkey and, certainly, the future course of the European Union and, in particular, the success of French President Emmanuel Macron's initiative to reboot the eurozone through his proposals for a common budget and finance minister for the region. Macron is openly pro-European and keen to bolster support for the EU - reinforcing the idea that the bloc can help its citizens secure a better life - as a key part of his strategy to counter populism and Euroscepticism. Support for the EU, battered by long crises over debt and migration, has begun to recover. The EU's own latest Eurobarometer report on public opinion, published this month, found that trust in the EU has risen to 42%, from 36% a year ago and 32% in late 2015 (see Figure 7).

Outside the UK, dissatisfaction with the EU doesn't translate into support for leaving. This is not to say that European citizens suddenly disregard the EU's dysfunctional nature and efficiency problems. A survey of 10 EU countries published in June by the Pew Research Center found that Europeans remain critical of the bloc. A median of 46% disapproved of the EU's handling of its long economic crisis, while 66% disapproved of its management of the refugee crisis.

Any talk of Frexit, Dexit (and so on) is now definitely off the cards. Although support for the euro area is now higher, it is highest in countries with high income levels. Indeed, countries that have experienced high growth since the introduction of the single currency are more likely to have seen an increase in citizen support for the euro. Brexit will certainly bring a major upheaval in the EU's economy, which cannot as yet be predicted.

Improving economic growth in much of Europe, especially in the 19-country euro currency zone, has helped blunt some of the discontent of European citizens with the European Union, creating a unique opportunity to take action to make the institutional changes that are required if the EU wants to prosper. Improved opinion of the EU coincides with renewed economic confidence in most of the European countries surveyed. In recent years, many Europeans have been dispirited about economic conditions in their country. Now, as the economy in a number of nations has begun to recover, the public mood is brightening.

There is now positive momentum for the EU and its Member States. The Franco-German axis is once again set to enter into operation and push ahead with reforms that will help the EU stand on its own two feet or "take [its] destiny into [its] own hands", as Angela Merkel recently put it. After the Brexit decision, France and Germany seem to agree that a medium-term roadmap for deepening the EU, and eurozone governance in particular, is needed. French President Macron has proposed a "new deal" to help address Europe's economic dilemmas to entice Germany and other northern eurozone countries to allow the currency bloc to pool financial resources to shield members from future crises. (Of course, President Macron first has to go through necessary labour reforms in his own country). Northern EU countries -which have long called for structural overhauls in France-may be unwilling to sign on to his proposals for the currency area, including increased spending by Germany and other wealthy economies and a shared crisis budget.

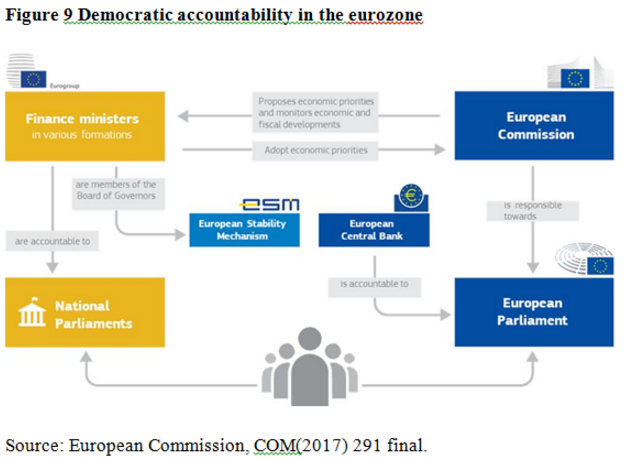

Democratic accountability

The EMU setup and the operation of the euro area has thus far been characterised by low democratic accountability, as it is based on "output legitimacy", that is, legitimacy that depends on a system's capacity to achieve the citizen's goals and solve their problems effectively and efficiently. The higher its capacity, the more legitimate the system. Its operation prioritises results and output effectiveness over an input-oriented democratic decision-making (legitimacy derived from the way in which decisions are made and not by the results of these decisions produce) architecture that might be less effective.

One of the lessons drawn from the crisis is that there is a need for more transparency to bolster support for the European integration project on behalf of the citizens. Europeans reacted to all the opaque decision-making made at the height of the crisis by unelected officials and technocrats away from the democratic center by massively and repeatedly turning to populist, anti-European parties.

Accountability in EMU governance can indeed be improved through more transparency, but in order to fully address the existing shortcomings of EMU governance and thus set the conditions for the European economy to work, a political union and European federal-type institutions are needed. At the moment, there is little appetite on the part of member states for relinquishing their national sovereignty in fiscal matters and transfer it to the EU level, which would require a major institutional change in the European Union. So far, the European Commission's proposed short-term measures to improve the democratic accountability of EMU are: setting up a strengthened and more formalised dialogue with the European Parliament, a proposal to integrate the fiscal compact into the EU legal framework and progress towards a stronger external representation of the euro area. Over the long term, steps towards ensuring the democratic accountability of EMU governance and decision-making could include: a full-time permanent chair of the Eurogroup, the Eurogroup established as an official council configuration, a fully unified external representation of the Euro area, the setting up of a euro area Treasury and a common finance minister (i.e. a common fiscal capacity), the setting up of a European Monetary Fund and the integration of remaining intergovernmental arrangements in the EU.

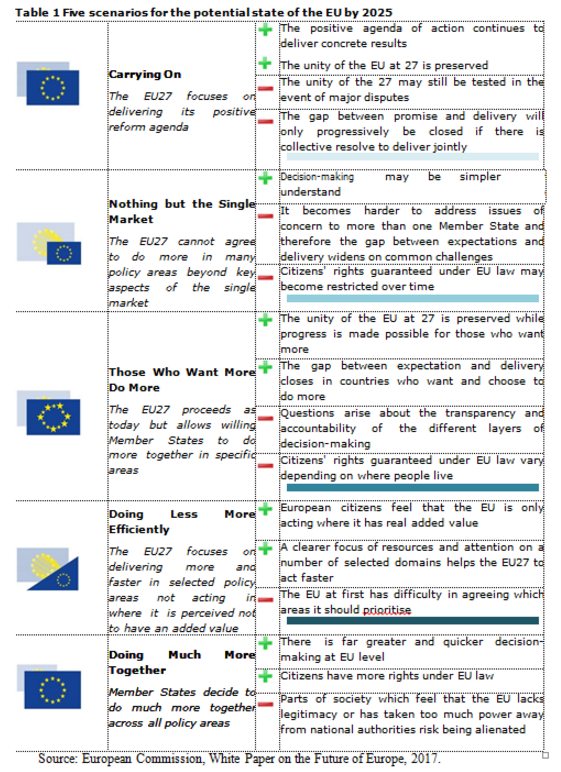

Apart from the proposed agenda by French President Macron, who has argued that without institutional change, the euro could fail within 10 years, reform proposals have also been put forward by the European Commission in its White Paper on the Future of Europe under President Juncker. As there is still no political support for a fully federalised European Union, the European Commission's five alternative scenarios reflect the current realistic choices that stand before the European Union.

The table below shows the five alternative scenarios proposed by the European Commission in this White Paper, which focus on differentiated degrees of "deepening" cooperation. It should be pointed out that the "Those Who Want More Do More" scenario formally recognises for the first time the model of differentiated/multi-speed integration (already endorsed by the leaders of the four biggest Member States, i.e. Germany, France, Spain and Italy), an idea dating back to German Chancellor Willy Brandt in 1974. This White Paper reflects a significant shift in the European integration debate, since a "Europe at many speeds" had been mainly advanced by intergovernmentalist forces, but stumbled on the adamant opposition of pro-Europeans (federalists), in favour of centralised/supranational EU governance.

Further progress on European integration issues will of course be slow ahead of the German elections on 24 September that will be decisive in many ways for the future path that the European Union, but the question is now all about whether EU affairs will take a turn for the better thereafter. In any event, the European Commission is set to present its first set of conclusions on the roadmap for the future of the EU at the December 2017 European Council.

As should be expected from the European Union, there will not be any radical changes overnight, but rather a process ofincremental change to improve the political economy and governance of the EU and the eurozone. In my view, this is the best chance to restore faith in the European integration project and show that it is capable of protecting its citizens.

2. Towards a complete economic and monetary union/ an update of economic policies

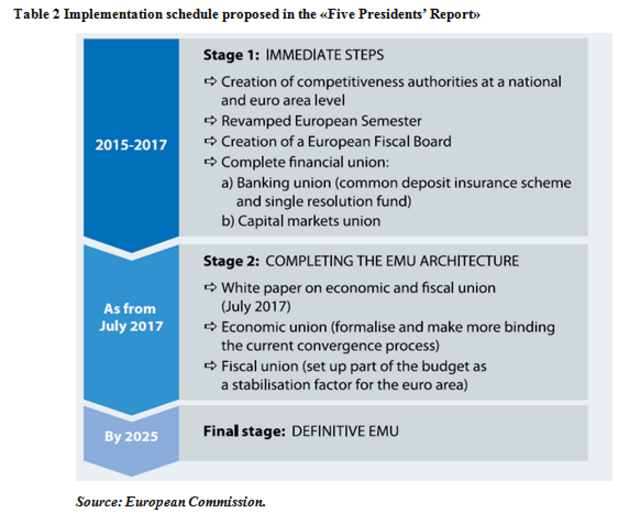

Future steps towards the completion of the EMU have been laid down in the well-known "Five Presidents' report", divided into two stages (short-term and long-term steps), as shown in the table below.

2.1 Monetary policy: towards an exit strategy

According to Article 127 of the Treaty on the Functioning of the European Union (TFEU), the primary objective of the European System of Central Banks (Eurosystem) is "to maintain price stability. Without prejudice to the objective of price stability, the ESCB supports the general economic policies of the Union with a view to contributing to the achievement of the objectives of the Union as laid down in Article 3 of the Treaty on European Union". This wording suggests that the Treaty assigns overriding importance to price stability, as the most significant contribution that monetary policy can make to achieve the objectives of the European Union, i.e. favourable economic environment and high level of employment.

Under the extraordinary circumstances of the crisis, the ECB went beyond its "price stability" mandate and already since 2008 used unconventional monetary policy tools such as large liquidity injections and the securities markets program to ensure that debt markets remain functional. Faced with the EU's worst recession in its six-decade history, the ECB needed to act resolutely to counter its impact and address the shortcomings of the initial setup of the economic and monetary union. In 2012, ECB President Draghi pledged to do "whatever it takes to preserve the euro" and announced the Outright Monetary Transactions (OMTs) programme to allow the ECB to buy sovereign bonds of euro area countries. Apart from OMTs, the ECB launched a quantitative easing (QE) programme in 2015 (asset purchases of public sector bonds), which was expanded to asset purchases of corporate sector bonds in 2016 (now worth €2 trillion). We are now entering a debate on how to orchestrate the exit from the ECB's QE, in terms of its timing and its sequencing. Against this background, last month's ruling by the German constitutional court to refer to the European Court of Justice (ECJ) the case with regard to the ECB's €2 trillion quantitative easing programme is of seminal importance. The action perpetuates legal ambiguity for at least another year - even though the ECJ is expected to decide in the ECB's favour.

Clearly at some point in time, sooner or later, there will be an end to these unconventional monetary policies. The crucial question will revolve then around timing and sequencing, namely 'when these policies will end' and 'if tapering should come first and then be followed by a rate hike' or the reverse. On the other hand, a premature normalisation of monetary policy (just like in 2008 and 2011), either in terms of interest rate hikes or in terms of proper tapering or according to the ECB's preferred wording "orderly adjustment", entails the following two risks: the first is the risk of a relapse, namely the ECB shouldn't abruptly stop loose monetary policy as a result, for instance, of a temporary inflation spike and not supported by the economic fundamentals. The second risk is the risk of financial instability, once interest rates start to rise.

2.2 Fiscal Policy

The idea of a Fiscal Union has gained new impetus and is again on the table and there seems to be a future towards integrated fiscal policies in the eurozone. It is true that integration within the eurozone has somewhat stalled since the creation of a Banking Union in 2014 (which I will analyse in the following section). However, the relevant debate has been given new impetus by the election in France of Emmanuel Macron, who has publicly advocated a common eurozone budget and a Finance Minister. Encouraging signs have been coming from the German side as well, as there is likely to be indeed readiness of the newly elected German government to push forward the European integration process. However, Germany has been accused of seeing fiscal union as a vehicle to achieve more austerity in the eurozone! It has in fact been argued that Germany has 'no alternative' to a revival of the Franco-German axis to reboot EMU governance and that is why it has put forward proposals for advancing European integration of its own, such as the proposal for transforming the European Stability Mechanism into a European Monetary Fund, as it builds expertise and takes on a continuous fiscal surveillance of Member States. This would understandably suit the German agenda which has long criticised the more lenient supervision of eurozone countries' compliance with fiscal discipline rules (under the revised Stability and Growth Pact).

The latest on the field of common fiscal policy in the eurozone is a proposal from the European Commission called European safe bond. The point is the following: investors can buy government debt into the euro area as a whole, rather than into one particular member state. This is different from a pooling of national government debt issuance, known as common Eurobond, which remains a political taboo in Germany. Sovereign debt across the eurozone could be bundled into a new financial instrument (ESB) and sold, if you like as a European brand, to investors. Such an idea could have potential benefits to many stakeholders, including the ECB. As you know, the ECB is a major buyer in the secondary market of the europeriphery. Issuing bonds backed by all 19 eurozone countries would be the best way to keep borrowing costs down if the ECB were to taper or indeed to end its QE programme at some point in time. Moreover, the ECB itself may want to replace national government bonds in its own balance sheet with European safe bonds.

2.3 Banking Union

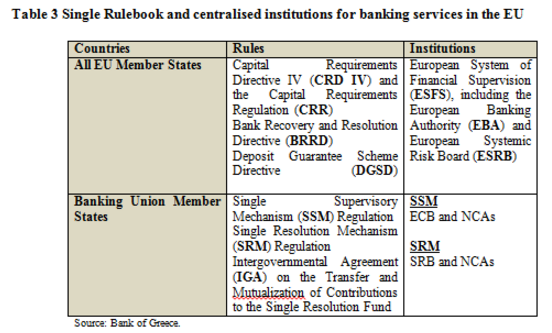

The crisis paved the way for a major paradigm change in the regulation of banks, i.e. the introduction of common prudential rules to create a level playing field for all the financial institutions of the EU (some 8,300 banks across the EU), also known as the Single Rulebook, comprising secondary law (Directives, Regulations, Decisions), regulatory and implementing technical standards drafted by the European Supervisory Authorities (ESAs) and soft-law rules such as guidelines and recommendations.

The Single Rulebook applies to all 28 EU member states and marks a shift from the previously predominant regulatory philosophy of minimum harmonization of national rules and the provision of a European passport based on mutual recognition across the EU to maximum harmonization. Three of the most important single-rulebook pieces are directly related to banking. These are the Capital Requirements Directive IV (CRD IV) and the Capital Requirements Regulation (CRR), the Bank Recovery and Resolution Directive (BRRD) and the Deposit Guarantee Scheme Directive (DGSD), which lay down capital requirements for banks and create regulation to the prevention and management bank failures, including a minimum level of protection for depositors.

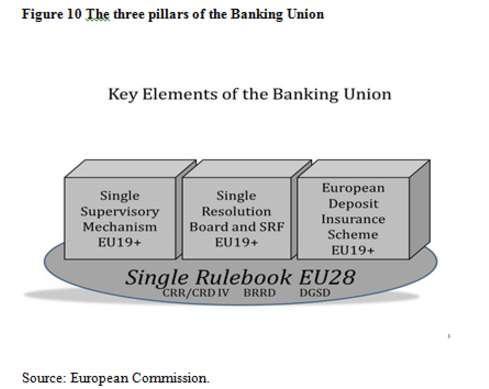

To this end, along with the major regulatory change in the banking sector, there was swift progress towards institutional change with the creation of the Banking Union (BU): pan-European centralised bodies for the supervision and resolution of banks, indispensable to ensure financial stability in the euro area.

The creation of the Banking Union comprises three pillars based on the single rulebook as the foundation (see Figure 10 below): a Single Supervisory Mechanism (SSM), a Single Resolution Mechanism (comprising a Single Resolution Board and a Single Resolution Fund) and a common deposit insurance scheme (yet to be approved).

Under the first pillar, the Single Supervisory Mechanism (SSM) was established without treaty change. By unanimous vote the Council decided to confer "specific tasks concerning policies relating to the prudential supervision of credit institutions" on the European Central Bank, in accordance with Article 127(6) of the Treaty on the Functioning of the European Union (TFEU). But a treaty change in the future should not be ruled out. The European Central Bank now directly supervises 123 systemically significant banks and, at the same time, national supervisors work closely together within an pan-European supervisory system to supervise the so-called "less significant institutions" (around 5,500) in the 19 Member States of the euro area.

A Single Resolution Mechanism (SRM) is the necessary complement of the first pillar. The rationale behind it is to avoid the risk of bank bail-outs by national governments, and for the private sector to bear the cost rather than the taxpayer. In the case of failing banks, the Single Resolution Board may decide on resolution, to be covered by funds drawn from a Single Resolution Fund (€55 billion by 2023) that banks themselves pay into. Any residual fiscal burden on sovereigns should be contained through a federal fiscal backstop.

The missing link from the Banking Union structure is its third pillar. The Commission's 2015 proposal for a European Deposit Insurance Scheme (EDIS) builds on the existing framework under the Deposit Guarantee Scheme Directive (2014/49/EU) which provides for a more uniform degree of deposit guarantee for all retail depositors.

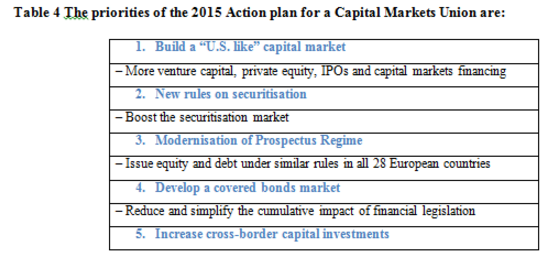

2.4 Capital markets union

Since 2015, the European Commission's new flagship project is the creation of a Capital Markets Union to build a single integrated capital market for all 28 Member States. The Capital Markets Union (CMU) is a plan of the European Commission consisting of a mix of regulatory and non-regulatory reforms (33 measures in total), aiming to better connect savings to investments based on a single rulebook that will create a level-playing field for the provision of investment services and offer private firms the possibility to raise capital through issuance of equity and debt anywhere in the EU.

I should remind you that the European economy has been traditionally bank-based. It is indicative that 70% of capital raised in the EU comes from the banking system, compared with just 20% in the US. So, the idea is to provide alternative sources of financing and more opportunities for consumers and institutional investors. For companies, especially SMEs and start-ups, the CMU means accessing more funding opportunities, such as venture capital and crowdfunding. The CMU also puts a strong focus on sustainable and green financing: as the financial sector begins to help sustainability-conscious investors to choose suitable projects and companies, the Commission is determined to lead global work on supporting these developments.

A well-functioning, diversified and deeply integrated capital market is of key relevance for the European Central Bank for three reasons: first of all, the integration of capital markets facilitates the transmission of single monetary policy in the euro area, secondly it contributes to macroeconomic and financial stability and thirdly, it supports risk-sharing in the private sector across the EU.

3. Greece in the eurozone in the post-MoU era

Finally, turning to my country Greece, this is a fortunate moment in the following sense. Greece today is again at a crossroads, but this time may be different. Under some preconditions, a case could be made for a strong turnaround of the economy. If the Greek authorities remain vigilant with no complacency (no delays, no back-tracking) and we ALL roll up our sleeves and stick to structural reforms and the privatisation agenda, and, on the other hand, our lenders, deliver on their promises about debt relief sooner rather than later, i.e pacta sunt servanda principal should apply to both lenders and borrowers, then, I'm quite optimistic that the return to European normality after the completion of the current programme in August next year is within reach.

The Greek economy's progress during the last eight years of adjustment has been unprecedented, both in terms of fiscal and external adjustment of more than 15 percentage points of GDP. The huge twin deficits turned into surpluses. Last year, the primary surplus was 4.2% of GDP, outperforming the target of 0.5%. The current account during the last two years had effectively been in balance from a 15% deficit eight years ago.

At the same time, sweeping structural reforms have been implemented, covering the pensions system, the health system, labour markets, product markets, the business environment, public administration, etc. Recapitalisation and restructuring have taken place in the banking system and significant institutional reforms have been initiated aiming at reducing the volume of NPLs. Moreover, there is evidence that the economy has been undergoing a rebalancing towards tradable, export-oriented sector: the share of exports of goods and services in GDP increased from 19% in 2009 to 28.2% in 2016, with most of the increase coming from exports of goods.

In closing, I would like to stress that Greece belongs to the core of Europe. Its future is within the eurozone, within the group of solidary countries, to the people of whom we, the Greeks are grateful for their financial support. Despite all these years of uncertainty and austerity, this is the overwhelming wish of the majority of the Greek people still today, within the core of Europe. This is our legacy as a nation that goes back to our history and our tradition and, more recently, expressed by a visionary Greek politician, a great European statesman, who stood above political parties, late President Konstantinos Karamanlis, who showed the Greek people the way forward, the European way.

Concluding remarks

The sovereign debt crisis in the Eurozone revealed how vulnerable the euro area's economic and monetary framework was to external shocks, especially taking into account the constraints of no bail-out and no debt restructuring. The euro area was not equipped to tackle large crises and did not have the safety nets and institutions to respond promptly to the severe challenges that such crises entail. So it had to buy time and resort to quick fixes that would bring it back on a more table footing. The response to the crisis focused on the need to strengthen the fiscal rules, to prevent macro-imbalances and reinforce economic policy coordination and surveillance between Member States.

Furthermore, there is an imperative need to deepen euro area economic governance (i.e. complete the Economic and Monetary Union) in order to strengthen the convergence of economic performances of Member States and reduce the degree to which financial fragmentation spreads in times of crisis.

It is worrying somehow Europe's declining international standing over the last twenty years. Today, Europe is no longer the world's largest economy, it has been overtaken by China and, by 2025, the IMF predicts that China's share will reach 16.5%, while the EU's share will be almost halved. In the area of security and defence, the EU's international role is also diminishing and it seems that Europe's greatest and most sustainable source of political power is of the soft kind. But of course, Europe's geostrategic outlook is essential in shaping the global order. Specifically with regard to global security, Europe must rise to the occasion and help address the modern-day challenges of instability and turbulence in Islamic countries. In terms of world trade, as an open market economy, the EU has been a major player in efforts to bolster multilateralism and trade cooperation in the global system. It is worth mentioning the effort to promote global trade (for instance, by means of the TTIP).

Over its long history, the EC/EU has traditionally managed to find consensus on the burning issues facing it. In the current juncture, and under the spectre of a -previously inconceivable-exit of a Member State, the EU needs to smooth over disputes between Member States and establish mechanisms to address heightened uncertainty and unpredictable political developments, and also find solutions to ensure an evenly distributed economic recovery across its territory.

There is an old saying in Brussels that the European project only advances in times of crisis, and Europe's leaders are known to have a tried and- tested method for coming up with policy fixes when forced to cope with emergency situations. I only hope that this time is not different. As they say: "Times will tell".

Thank you very much for your attention.