Guy Debelle: Global influences on domestic monetary policy

Address by Mr Guy Debelle, Deputy Governor of the Reserve Bank of Australia, to the Committee for Economic Development of Australia (CEDA) Mid-Year Economic Update, Adelaide, 21 July 2017.

The views expressed in this speech are those of the speaker and not the view of the BIS.

Thanks to Dan Rees and Rachael McCririck for their work on the neutral rate, which this draws directly on.

There are a large number of factors that the Reserve Bank Board takes into consideration in making its interest rate decision each month, both domestic and global. Today I would like to talk about some of the global influences on domestic monetary policy.

As you are well aware, the Australian economy doesn't operate in isolation from the rest of the world. This is also true when it comes to monetary policy. While the goals of monetary policy are very much domestic, in terms of inflation and employment, the influences on the achievement of these goals are both domestic and global.

In talking about the global influences on the setting of monetary policy, I will make the probably obvious point that the policy rate here in Australia is at a historic low, in no small part because policy rates elsewhere in the world are also around historic lows.

Why are global policy rates as low as they are? Part of the explanation is that to meet their policy goals, central banks in other advanced economies have had expansionary policy settings since the start of the global financial crisis. Moreover, in the largest advanced economies, policymakers have provided further monetary stimulus through large asset purchase programs, which have seen central bank balance sheets increase significantly.

Another part of the explanation is that the neutral level of the policy rate has declined in most countries, including here in Australia. That is, the level of the policy rate where monetary policy is neither providing stimulus nor restraint is lower than it used to be. Central banks have had to set their policy rates even lower than that already lower neutral policy rate to provide the appropriate stimulus to their economies.

I will start by talking about four common global factors that have led to the expansionary monetary policy settings seen in most advanced economies for almost a decade. These four factors are present in Australia to varying degrees. I will then discuss the neutral policy rate and its decline over the past decade. I will finish with some comments on the influence of global financial factors on domestic monetary policy considerations.

Four Common Global Factors

The first and most obvious factor influencing monetary policy settings globally is the financial crisis and its aftermath. The large and rapid decline in policy rate settings in most advanced economies occurred in 2007 and 2008. Over this period, many policy rates were reduced to close to zero and subsequently, in some cases, even below zero. The collapse in global output and trade at the end of 2008 was sharp and significant. The severity of the episode was increased by the fact that it was synchronised across the global economy.

It is now ten years since the onset of the crisis, and nearly nine years since its nadir in the last quarter of 2008, yet we still see policy rates at their post-crisis lows. The Federal Reserve in the US has raised its policy rate in recent times, but even then only four times in quarter point increments, so that the policy rate has only just reached 1 per cent. That said, broader measures of financial conditions in the US suggest that financial conditions there aren't tighter since the Fed started increasing its policy rate: longer-term government bond yields and the US dollar exchange rate are both no higher than when the Fed first increased its policy rate. Corporate bond yields remain near historic lows and US equity prices are higher.

The effects of the financial crisis on most parts of the advanced world have been very long-lasting. Global economic growth has mostly fallen a little short of expectations for the past decade. As a result, even with the expansionary monetary policy settings, aggregate global growth has been average over this time, but not better than average, which would be desirable given the large loss of output in 2008/09.

As I'm sure you all know, Australia did not suffer from the same decline in output that many other advanced economies underwent. The level of GDP in Australia is 27 per cent higher than it was in 2007. In comparison, in the US, it is 13 per cent; in the UK, 10 per cent; while in the euro area, the pre-crisis level of GDP was only regained in 2015.

It is only quite recently that forecasts for the global economy have been revised higher for the first time in many years. This has reflected an upswing in industrial production and exports across a broad swathe of the global economy. A critical question is whether this upswing will be sustained.

One of the reasons that global growth after the financial crisis has been only moderate is the second common factor I'd like to highlight: the low level of corporate investment over the past decade.1 Many of the preconditions that historically led to a pick-up in business investment have been in place: low policy interest rates, low borrowing costs for business, strong corporate debt markets. Something has clearly been missing that has prevented these positive preconditions from generating an upswing in business investment. One obvious candidate is uncertainty about future demand or, as it is often referred to, animal spirits. To some extent, this lack of animal spirits is self-fulfilling. If businesses are not confident about whether there will be enough demand in the future to justify more investment, they hold off spending on investment, which means that, indeed, there isn't enough demand in the future. As the global economy has become more integrated, there seems to be a more important common global element in animal spirits. One driver of this may well be multinational firms making investment decisions across a number of economies.

In Australia, the investment dynamics have been clearly different. In marked contrast to the rest of the world, business investment in Australia has been at historic highs in recent years, largely as a result of investment in the resources sector. But now resource investment has fallen most of the way back to its pre-boom levels. Investment outside the resources sector in Australia has remained at a low level, as in other countries, though it has grown modestly in the past couple of years.

In recent months, there have been some positive signs on investment spending in a number of countries. If this is sustained, then it is possible animal spirits switch from being self-fulfillingly negative to self-fulfillingly positive. As we see signs of investment picking up this year in some other countries, there is an increased chance this will be reflected in Australia. A gradual pick-up in investment is embodied in the RBA's growth forecast.

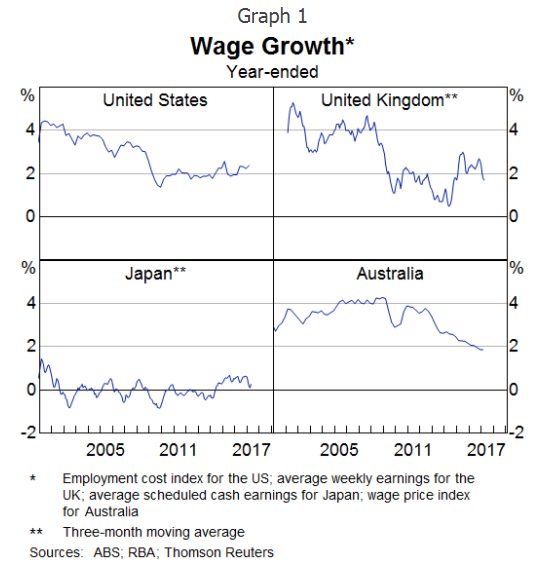

The third common global element is low wage growth (Graph 1). This is occurring despite very low unemployment rates in countries such as the US, Germany, Japan and the UK. The unemployment rates in these countries are at levels that have historically been associated with an acceleration in wage growth. The Governor talked about this in a speech late last year.2 Andy Haldane at the Bank of England recently discussed some of the possible explanations for this stubbornly low wage growth and concluded that, in the end, we don't yet have a particularly persuasive explanation.3 That said, we know that the labour supply curve ultimately does slope upwards. So if unemployment rates continue to decline in these countries, we must get closer to the point where wage pressures materialise.

Wage growth in Australia is subdued, as it is elsewhere. One noteworthy difference in Australia is that labour productivity growth has generally been higher than it has been in other countries over recent years. As a result, there has been no growth in unit labour costs (that is, wages adjusted for productivity) in Australia for five years, whereas in other countries, unit labour cost growth has been quite a bit higher.

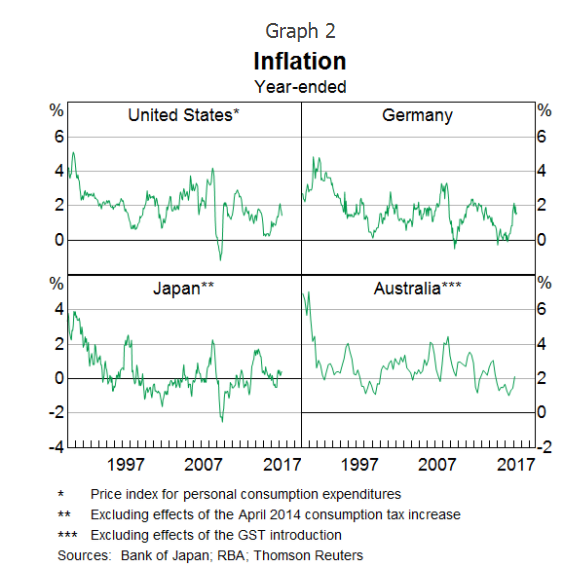

The fourth and last common factor is the sustained low inflation that has been evident globally for the past decade (Graph 2). This is a direct consequence of the three previous factors I have just talked about. In addition to those influences, there has been a continuation of the disinflationary pressure resulting from the integration of China into the global economy. There are signs that this latter force might be waning, with producer prices in China actually growing, following many years of continual, often quite substantial, declines. Throughout the past decade, expectations about future inflation have remained broadly anchored, which, at times, has helped stave off a shift towards deflation, but currently may be dampening the prospects of a sustained pick-up in global inflation.

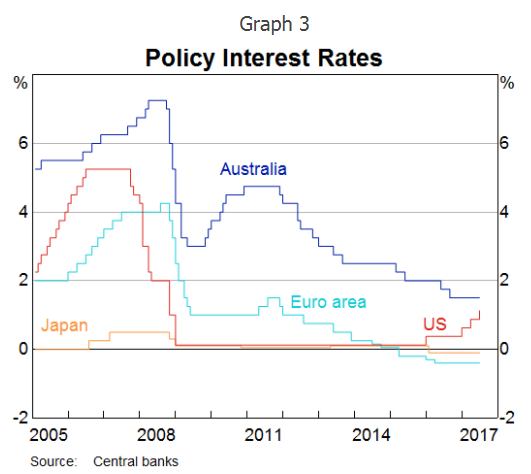

These four factors - the subdued global recovery, low investment, subdued wages growth despite low unemployment rates and low inflation - are the primary explanation for the very stimulatory policy settings in place globally (Graph 3). The fact that they are at such low levels has a material influence on why the policy interest rate in Australia is also at a historically low level.

Beyond these factors that I have just discussed, another significant factor contributing to the low level of policy rates globally is that the neutral policy rate in many countries has declined over the past decade.

The Neutral Interest Rate

The neutral interest rate provides a benchmark for assessing the current stance of monetary policy. If the real policy rate - that is, the cash rate less inflation expectations - is below the neutral rate, then monetary policy is exerting an expansionary influence on the economy. If the real policy rate is above the neutral rate, then monetary policy is exerting a contractionary influence on the economy. The neutral rate is often associated with the turn of the 20th century Swedish economist Knut Wicksell and was picked up by Keynes.4 The previous Governor Glenn Stevens discussed the neutral rate in the Australian context more than a decade ago.5

There was a discussion of the neutral rate at the most recent Board meeting, as detailed in the minutes of the meeting released earlier this week. No significance should be read into the fact the neutral rate was discussed at this particular meeting. Most meetings, the Board allocates some time to discussing a policy-relevant issue in more detail, and on this occasion it was the neutral rate.

The neutral interest rate aligns the amount of saving and investment in the economy at a level that is consistent with full employment and stable inflation. That is, the neutral rate is where the policy rate would settle down in the medium term when the goals of monetary policy are being achieved. Accordingly, most explanations of the neutral interest rate start with the factors that influence saving or investment. Developments that increase saving will tend to lower the neutral interest rate; developments that increase investment will tend to raise the neutral interest rate.

There are three main factors that, in my view, affect the neutral rate in Australia:

- the economy's potential growth rate

- the degree of risk aversion

- international factors.

One of the major determinants of the neutral interest rate is the economy's potential growth rate. In an economy with a high potential growth rate, because it has strong productivity or population growth, the expectation of increased future demand provides a strong incentive for firms to invest and the prospect of higher real incomes reduces the incentives of households to save. Both of these forces will tend to raise the neutral interest rate. The economy's potential growth rate tends to evolve quite slowly, and hence we should expect the neutral interest rate also to change only very gradually as a result of this influence.

Another influence on the neutral rate is the risk appetite of firms and households and the way risk has been priced into market interest rates. This influence can move rapidly. When risk aversion rises, firms require more compensation to make long-term investments with an uncertain return. At the same time, the increased risk aversion will cause households to save more. This lowers the neutral interest rate, as any given level of the policy rate is less expansionary because of the increased risk aversion. If there is an increase in risk aversion, it is also likely that there will be a widening in the spreads between the policy rate and market interest rates that determine the behaviour of households and firms. A given market interest rate will correspond to a lower policy rate if spreads widen. This will further lower the neutral interest rate.

Finally, in an open economy, where capital can move reasonably freely across borders, global interest rates will also influence domestic interest rates. This means that trends in overseas productivity growth, demographics and risk appetite will affect the neutral interest rate in Australia.

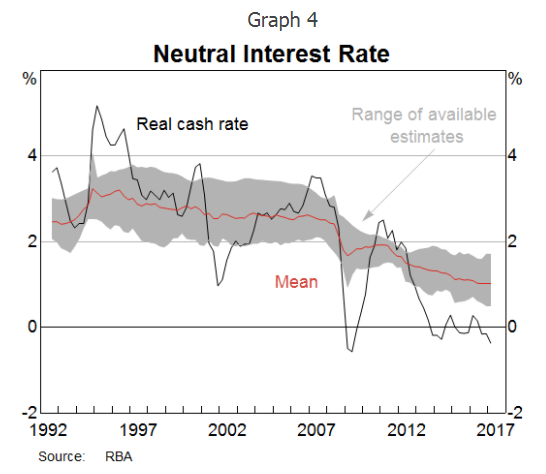

So how do we calculate the neutral interest rate? It is not directly observable. There are a number of different ways of estimating it from the behaviour of market interest rates and other economic variables6. The shaded area in Graph 4 shows a range of plausible estimates for the neutral real interest rate obtained using a number of different approaches. As you can see, there is a reasonable amount of uncertainty about the exact level of the neutral rate.

Graph 4 also shows the (ex post) real cash rate calculated by deducting the trimmed mean inflation rate from the cash rate.7 When the real cash rate is above the neutral rate, the monetary policy stance is contractionary. When it is below, the stance is expansionary. As you look at the graph, you can see that this lines up with most assessments of the stance of monetary policy over the past 25 years. It suggests that monetary policy was clearly expansionary in the early 2000s, in 2008 and for the past five years or so.

The estimates of the neutral rate suggest that it was fairly stable for much of the 1990s up until 2007. In Glenn Stevens' speech that I mentioned earlier, he noted that the neutral real cash rate at the time (2004) was probably somewhere between 2½ per cent and 3¾ per cent. This is consistent with the estimates shown here.

The graph shows a clear step down in all the estimates of the neutral rate in 2007/08 and that it has probably drifted lower since. It suggests that Australia's neutral interest rate is currently around 150 basis points lower now than in 2007. This decline can largely be accounted for by a slowdown in potential growth and an increase in risk aversion.

The Bank estimates that Australia's long-run potential growth rate has declined by around ½ percentage point from the mid 1990s.8 Part of the decline reflects slower labour force growth. The rest of the decline reflects a slowdown in trend productivity growth, which is common to many advanced economies. This slowdown in potential growth has probably translated about one-for-one into a decline in the neutral rate, though the decline has been gradual.

The sharper decline in the neutral rate in 2007/08 can be most easily related to the sharp increase in risk aversion with the onset of the financial crisis. This increased risk aversion probably accounts for most of the large fall in estimated neutral interest rates in Australia and abroad that occurred at this time. This heightened risk aversion has also contributed to an increase in spreads between the cash rate and market interest rates, which should have a roughly one-for-one effect on the neutral interest rate.9

At the same time, increased risk aversion means that companies are investing less than one would expect given financing conditions and the economic outlook. Households are less willing than in the past to borrow in order to fund consumption. Although these effects are hard to quantify, they would both lower the neutral interest rate.

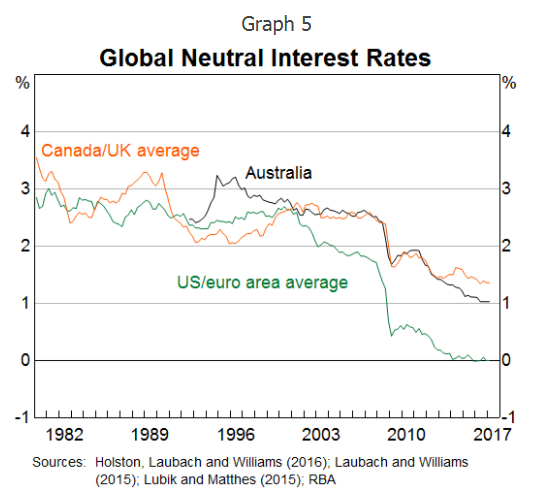

To return to a global perspective, Graph 5 compares the average estimate of the neutral interest rate for Australia to a range of international estimates. On average, the neutral interest rate estimates for Australia are similar to those of the United Kingdom and Canada, but higher than those for the United States and the euro area.

As is the case for Australia, estimates of neutral interest rates in other developed economies were fairly stable until around the mid 2000s and have fallen since then. The decline in the neutral rate was particularly sharp in 2007/08 and, again, most likely reflects the increase in risk aversion at the onset of the financial crisis.

Because trends in determinants of the neutral interest rate, such as productivity growth and risk appetite, tend to be highly correlated across advanced economies, it is hard to distinguish between international influences and domestic influences. But it is very likely that global factors have contributed to a decline in Australia's neutral policy rate.

So in short, the policy rate in Australia is low because the neutral rate is lower than it used to be as a result of both international and domestic developments. This means that the current (nominal) cash rate setting of 1½ per cent today is not as expansionary as a cash rate of 1½ per cent would have been in the 1990s or the first half of the 2000s.

Looking ahead, the neutral policy rate both here in Australia as well as in other advanced economies is likely to remain lower than it was in the past. It is plausible that the degree of risk aversion might abate in time, which would see the neutral rate rise from its current low level. But other developments contributing to the lower neutral rates, particularly lower potential growth rates, could be more permanent.

Global Financial Influences

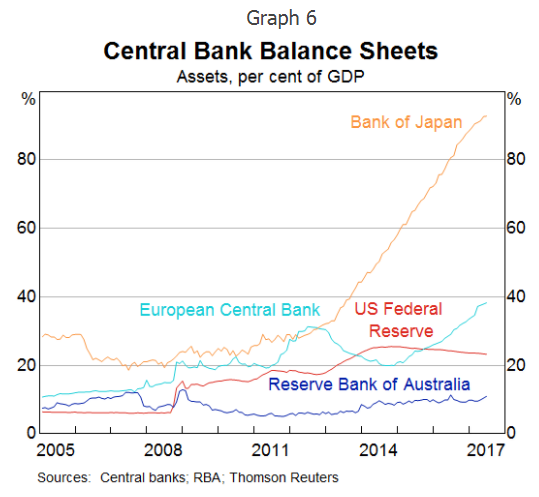

In addition to the neutral rate declining, policy rates in other countries have been set even lower to provide the appropriate stimulus. On top of that, in a number of the major economies, policy is more expansionary than indicated by just the level of the policy interest rate. Central bank balance sheets have expanded considerably as the central banks have purchased assets, in large part government debt (Graph 6). This program of asset purchases has finished in the US and the UK, but is still ongoing in the euro area and Japan.

The fact that monetary policy settings are more expansionary in the rest of the world than in Australia, both through lower policy rates and balance sheet expansion, puts upward pressure on the Australian dollar. Capital is attracted by the higher rates of returns on offer here, which is likely to lead to an appreciation of the exchange rate. So, while an easier monetary policy elsewhere in the world should lead to faster growth in the world economy, which is good for the Australian economy, an appreciating exchange rate works against this. To put it in economic terms, there are offsetting income and substitution effects for the Australian economy. Whether this is positive or negative in net terms for Australia is an empirical issue.10 Generally, the evidence suggests that widening interest rate differentials do lead to an appreciation of the Australian dollar. So that does counteract the benefit to the Australian economy of faster global growth.

It is conceivable that unconventional monetary policy may have a larger financial impact than movements in interest rates.11 That is, the effect of unconventional policy through the exchange rate channel may be larger while the effect in terms of higher output may be smaller. Again, it is an empirical issue.

Central bank asset purchases generate cross-border capital flows from investors seeking higher returns. Some of that we see directly in a higher Australian dollar exchange rate. But some of those cross-border flows are not quite so obvious. Investors often tend to hedge their exchange rate exposures to protect their offshore investments from exchange rate movements. As these investments increase there is more demand for such hedges, which causes the cost of hedging to increase. A direct measure of this is the cross-currency basis, which I spoke about recently.12 For example, the relatively wide yen basis in part reflects the increased capital flows out of Japan.13

If fewer of these investments were hedged, we would see more of these capital flows reflected in the exchange rate. If there was less hedging in the example I just used, the yen may well have depreciated further and currencies where Japanese investors have placed their funds, such as the Australian dollar, would have appreciated by more. So hedging, which is reflected in the wider cross-currency basis, has served as something of a shock absorber for these cross-border flows.

But this aside, the expansionary settings of monetary policy globally clearly have had a material influence on domestic policy settings through the impact of capital flows on the exchange rate.

Hélène Rey has recently described this state of affairs as a monetary dilemma: 'Independent monetary policies are possible if and only if the capital account is managed-'14 That is, we can only set the monetary policy we want if we impose controls on the flow of capital in and out of the country. I don't think the situation is quite as stark as that. There is still a substantial degree of flexibility to set domestic monetary policy appropriately for domestic conditions. But I would certainly agree that the monetary policy decisions of other central banks are a significant factor to be taken into account in our monetary policy deliberations.15 Another way of stating this is that we don't have the independence to set the neutral rate, which is significantly influenced by global forces, but we do have the independence as to where we set our policy rate relative to the neutral rate.

Conclusion

To conclude, I have outlined today a number of the channels of influence that global developments have on domestic monetary policy settings. Some of these global forces are transmitted through the real economy, some through financial channels.

The effects of these global influences on the Australian economy have been material. The global economic environment and global policy settings that have been in place for the past decade have contributed significantly to the monetary policy settings in Australia that we have today and will likely continue to do so for the foreseeable future.

Currently, financial markets don't expect any further lowering of policy rates in the major economies, nor any further expansion in policy settings. Hence the downward pressure on domestic policy settings from this source does not look like it will intensify in the foreseeable future. But the four common factors that are highlighted in the first half of my speech are still present. While there are some tentative signs that they are abating, the evidence is inconclusive at this stage.

As I said earlier, the Federal Reserve has raised its policy rate very gradually four times over the past two years. And last week the Bank of Canada increased its policy rate to 0.75 per cent. Just as the policy rate in Australia did not need to decline to the very low levels seen in other parts of the world, the fact that other central banks increase their policy rates does not automatically mean that the policy rate here needs to increase. The policy rates in both the US and Canada still remain below that in Australia.

Ultimately, in Australia as is the case elsewhere, policy rates are set at the level assessed to be appropriate to achieve the domestic policy objectives. While global influences, including monetary policy settings in other economies, have a significant impact on that assessment, they are, in the end, only one of a number of considerations to be taken into account.

1 See also Carney M (2017), 'Investment and Growth in Advanced Economies', Remarks at 2017 ECB Forum on Central Banking, Sintra, 28 June. Available at <http://www.bankofengland.co.uk/publications/Documents/speeches/2017/speech986.pdf>.

2 Lowe P (2016), 'Inflation and Monetary Policy', Address to Citi's 8th Annual Australian & New Zealand Investment Conference, Sydney, 18 October.

3 Haldane A (2017), 'Work, Wages and Monetary Policy', Speech at the National Science and Media Museum, Bradford, 20 June. Available at <http://www.bankofengland.co.uk/publications/Documents/speeches/2017/speech984.pdf>.

4 Given I am speaking in Adelaide, it is appropriate to thank my former macro/money professor at Adelaide University, Colin Rogers, for getting me to read Wicksell's Interest and Prices in my honours year.

5 Stevens G (2004), 'Recent Issues for the Conduct of Monetary Policy', Address to the Australian Business Economists and the Economic Society (NSW Branch), Sydney, 17 February.

6 See Laubach T and J Williams (2016), 'Measuring the Natural Rate of Interest Redux', Finance and Economics Discussion Series 2016-011. Washington: Board of Governors of the Federal Reserve System, <http://dx.doi.org/10.17016/FEDS.2016.011>.

7 Note that is an ex post measure of the real cash rate as I am using actual inflation rather than expected inflation.

8 The Treasury has very similar estimates in the Commonwealth Budget.

9 The Bank has noted on many occasions over the past decade that it has taken account of this widening in spreads in the setting of monetary policy.

10 Adler G and CO Buitron (2017), 'Tipping the Scale? The Workings of Monetary Policy through Trade' IMF Working Paper 17/142. Available at <http://www.imf.org/~/media/Files/Publications/WP/2017/wp17142.ashx>.

11 Ferrari M, J Kearns and A Schrimpf (2017), 'Monetary Policy's Rising FX Impact in the Era of Ultra-low Rates', BIS Working paper No 626, April. Available at <http://www.bis.org/publ/work626.pdf>.

12 Debelle G (2017), 'How I Learned to Stop Worrying and Love the Basis', Dinner Address at the BIS Symposium: CIP-RIP? Basel, 22 May.

13 The yen basis refers to the cost for a Japanese investor of hedging a US dollar or Australian dollar investment, say, back into yen.

14 Rey H (2013), 'Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence', Proceedings of a symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming, 23-24 August, pp 285-333. Available at <https://www.kansascityfed.org/publicat/sympos/2013/2013rey.pdf>.

15 See also Obstfeld M and A Taylor (2017), 'International Monetary Relations: Taking Finance Seriously', NBER Working paper No 23440. Available at <http://www.nber.org/papers/w23440>.