Benoît Cœuré: Convergence matters for monetary policy

Speech by Mr Benoît Cœuré, Member of the Executive Board of the European Central Bank, at the Competitiveness Research Network (CompNet) conference on "Innovation, firm size, productivity and imbalances in the age of de-globalization", Brussels, 30 June 2017.

The views expressed in this speech are those of the speaker and not the view of the BIS.

A few years ago, heterogeneity in the euro area was causing people to question the sustainability of the currency union. The global financial crisis, and later the sovereign debt crisis, led to a destabilising dispersion in interest rates and, ultimately, in real and nominal economic indicators. In the summer of 2013, for example, around half of euro area Member States had inflation rates close to or above our preferred range of below, but close to 2%, while others were flirting with, and in some cases already showing, negative inflation rates.

Today, much of that heterogeneity has disappeared. Importantly, none of the euro area economies are now faced with negative inflation rates, nor with negative growth rates. Indeed, as we at the ECB have highlighted over the past few months, the recovery currently under way in the euro area is increasingly broad-based, with a marked convergence in national GDP growth rates.

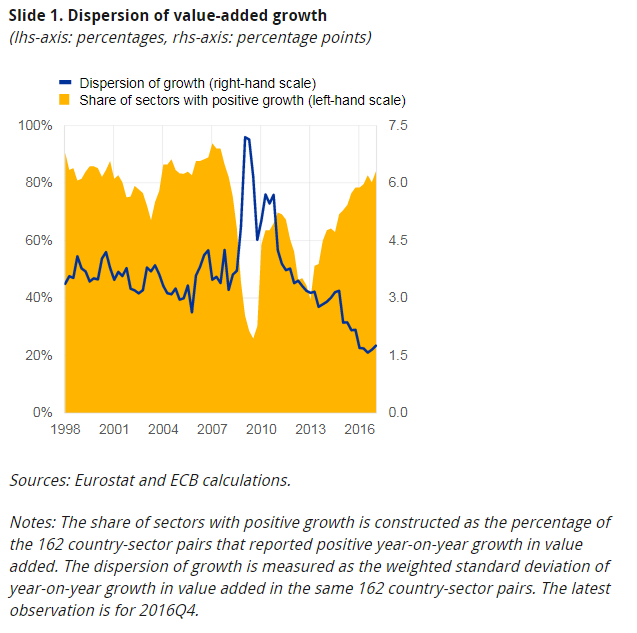

On slide 1 you can see that the dispersion of growth rates across countries and sectors is at its lowest level since the inception of the euro area - this is a remarkable progress from the episode I have just referred to. Over three-quarters of national sectors are currently experiencing positive value-added growth, compared with just a quarter at the height of the crisis. This convergence in output growth rates is also matched by historically low levels of dispersion in employment growth and inflation, including core inflation.

The marked fall in heterogeneity is a welcome development for monetary policymakers. Yet, in my remarks today I will argue that for the euro area to leave the legacy of the crisis truly behind, we need to see not only reduced dispersion in growth rates, but convergence in real income levels - that is, we need growth to accelerate in economies where losses from the crisis have been the largest for real convergence among Member States to take hold. To borrow from the empirical literature on long-term growth, sigma convergence is not enough and we want to see beta convergence taking place between euro area economies.1

For this to happen, I will argue that institutional quality - broadly speaking the range of social and legal frameworks that shape the conditions in which households and businesses operate - needs to improve in many Member States so as to unleash new growth forces and set off a new phase of true convergence. And in doing so, I will draw on the wealth of empirical findings produced by the CompNet project.

Heterogeneity and monetary policy

Let me start with the first set of observations and respond with two counter-questions: why is a low degree of heterogeneity good for monetary policy? And can monetary policy contribute to lowering dispersion?

The simple answer to the first question is that we set policy to ensure that we fulfil our mandate for the entire euro area. The closer countries are to the euro area average, the more likely it is that our policy is appropriate for them.

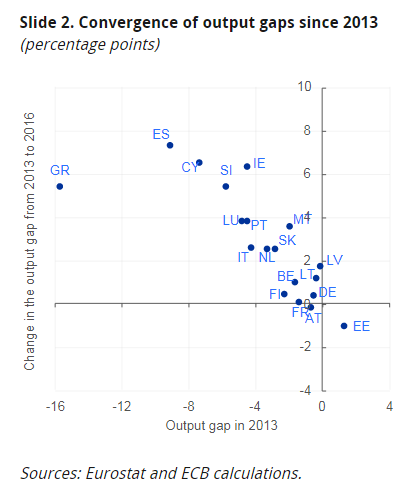

And here we have reason to be optimistic: we have not only seen a growing convergence in GDP growth rates, but also in economic slack, which is a more relevant gauge for monetary policy making given the information it conveys on future price pressures. Specifically, on slide 2 you can see that those countries that had larger output gaps in 2013 have also tended to close them more rapidly than those with smaller initial gaps.

Much of this fall in heterogeneity is due to our policy measures - the answer to my second question. The wide dispersion of growth rates at the height of the crisis was largely related to the fragmentation of financing conditions across euro area countries, amplified by the bank-sovereign "doom loop". In response to this, we have put in place a range of measures, particularly the longer-term refinancing operations (LTRO and TLTRO), and announced our readiness to conduct outright monetary transactions (OMT). Such measures were specifically designed to counter the impairment to monetary transmission caused by this fragmentation.

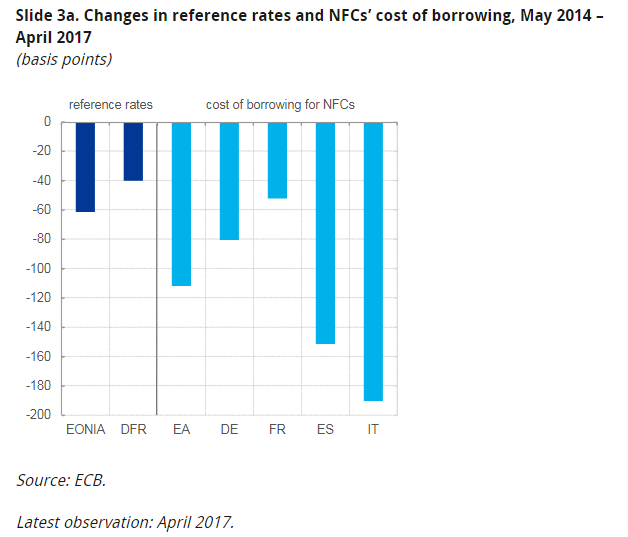

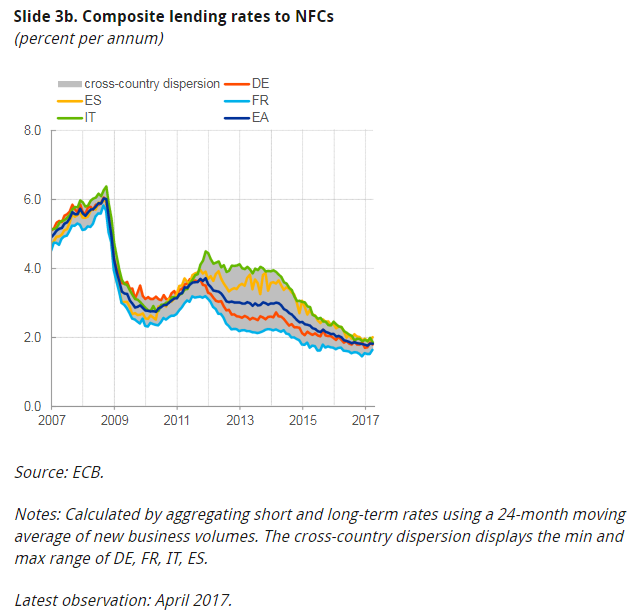

You can see on slide 3 that this was naturally more beneficial to those economies that had suffered more from financial fragmentation. On the left-hand side (slide 3a) you can see that the cost of borrowing for non-financial companies (NFCs) in Italy fell by nearly 200 basis points since May 2014 - that is, since we launched our credit easing package - although the main market reference rate, the EONIA, only fell by around 60 basis points over the same period. As a result, the dispersion of bank lending rates among the four largest euro area Member States - and this you can see on the right-hand side (slide 3b) - is currently at its lowest level since the introduction of the euro. And with the launch of banking union, the link between banks and sovereigns has started to loosen too.

One thought-provoking way of illustrating just how far dispersion has fallen across the euro area is to do a simple exercise: when we compute a standard forward-looking Taylor rule based on next year's inflation and output gap projections from the European Commission, it would suggest an interest rate for Germany and Italy that is, by and large, the same.2

Such an exercise is, of course, overly simplistic - there are good reasons why we do not set policy according to Taylor rules. In particular, policy rules are overly mechanistic and lack a deeper analysis of the underlying forces of growth and inflation, such as whether inflationary shocks are due to supply or demand shocks, which is a key aspect of our monetary policy strategy. Nevertheless, this simple exercise puts into perspective the view of some observers that the ECB's policy is too loose for some Member States and too tight for others.

But it also serves a different purpose. It shows that, while the broadening of the recovery is certainly welcome, a persistent convergence of growth rates is not unconditionally a good thing. For example, although simple policy rules would prescribe a broadly similar monetary policy stance for Germany and Italy, few would disagree that these two economies should ideally be on different growth trajectories, so living standards in Italy could catch up with those in Germany.

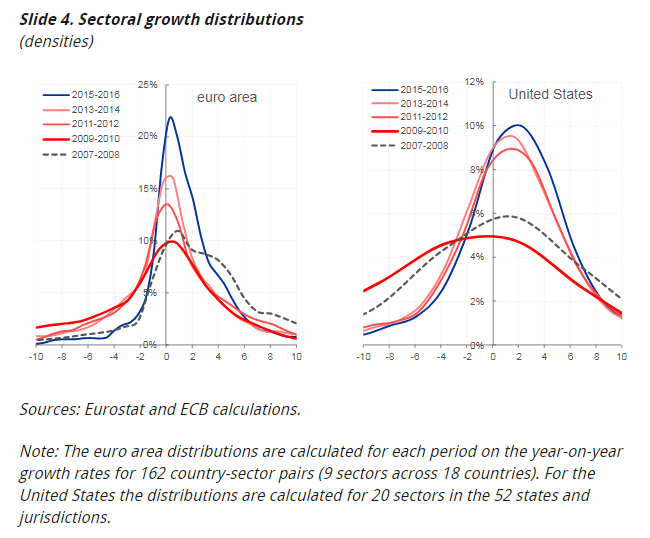

This, however, is not what we are seeing today. Although the left-hand chart of slide 4 shows that the euro area did not converge to growth rates much lower than those we had seen prior to the crisis - a process that some academics have coined "superhysteresis" - it also shows that the distribution of growth rates is pointier with flatter right-hand tails when compared with its pre-crisis pattern.

This implies that, compared to the pre-crisis period, fewer countries are growing at rates faster than the average. In other words, we are seeing little evidence of lower-income countries catching up with higher-income countries. As you can see on the right-hand chart of slide 4, this is not unique to the euro area - we can see a similar shift in the distribution across states in the United States.

Of course, fat right-hand tails before the crisis reflected, to some extent, unsustainable expansions fuelled by lax credit standards, on both sides of the Atlantic. So, while fat right-hand tails are generally a desirable phenomenon in a currency union as they may signal that a number of economies are growing at rates faster than the average - and thereby allow a convergence in income levels - this faster growth also needs to be sustainable and based on sound fundamentals, a point I will come back to later in my remarks.

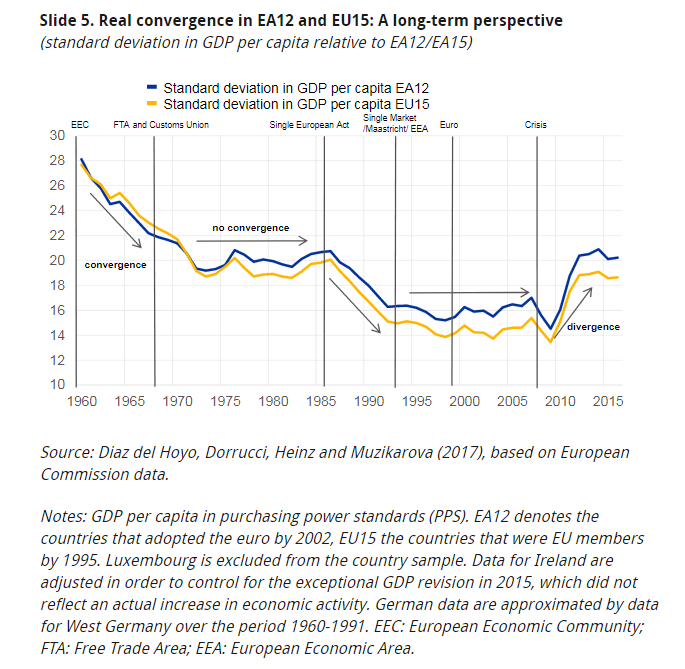

But the current lack of high-growth economies means that cross-country income differences that were already large prior to the crisis may also persist, or potentially even widen, in the future. Hysteresis if you wish. You can see on slide 5 that there has hardly been any convergence - measured in terms of GDP per capita - since the early 1990s among the 12 euro area Member States who joined before 2002. And recently we have even seen real divergence - certainly, a worrisome development for a currency union.

Convergence and monetary policy

We are faced, then, with two facts: first, cyclical dispersion is close to or at historic lows; and, second, structural dispersion - that is, differences in real income levels - remains high and may even be growing.

How should monetary policy respond to such conflicting signals?

The first thing to note is that persistent differences in income levels are not, per se, a problem for monetary policy in a currency union. After all, there are large and persistent differences in GDP per capita levels across regions in the United States that are broadly similar to those in Europe. These differences have not materially affected the Federal Reserve's ability to conduct monetary policy at the federal level, nor prevented the attainment of price stability.

Nor is convergence, or lack thereof, and its impact on Economic and Monetary Union, a particularly new debate. It is well known that the euro area does not meet all of the classic requirements of an optimal currency area.3 The original Maastricht criteria, and the Stability and Growth Pact, were put in place to ensure some nominal and fiscal convergence between Member States before adopting the euro. Yet none of the original members of the euro area have met all the Maastricht criteria in every year since its launch, highlighting the tensions between maintaining desired convergence and potentially centrifugal economic forces.

Similarly, and as I argued recently, hysteresis effects - should they materialise and the jury is still out on this - have the unfortunate consequence of locking in crisis-related income losses and may result in higher rather than lower inflationary pressures.4This is not to say that they are not a source of concern, but the answer should be a structural, not a monetary one.

Yet, despite this, I would argue that a lack of real convergence does matter for our union and the conduct of monetary policy, for three main reasons.

First, and most importantly, the lack of real convergence matters greatly for people in lower-income countries. Without credible prospects of catching up with higher-income countries, some may question the benefits of membership of the currency union. In other words, without real convergence we would not deliver on the promise we made when the euro was introduced, namely that it would bring prosperity and opportunities.

Worse, with the legacy costs of the crisis still clearly visible in many Member States, above-average growth in these economies is needed to at least restore a sense of normality and help bring down both the overhang in debt levels and unacceptably high youth and long-term unemployment. In a union based on shared values, hardship in any one country should be a concern for us all. And a lack of market-based convergence raises the need for individual transfers, which exist at country level but are not part of the social contract on which our monetary union is founded.

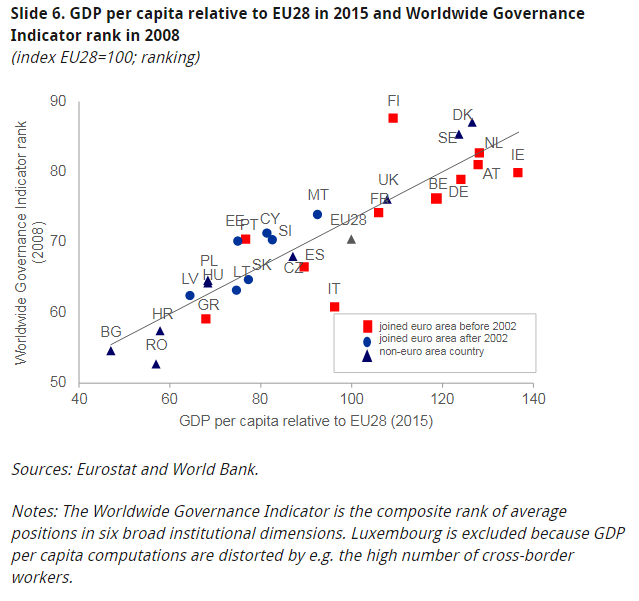

Second, the lack of real convergence in income levels is, more often than not, the result of a lack of convergence in institutional quality. Slide 6 shows that there is a clear relationship (albeit not necessarily causal) in Europe between the quality of institutions and GDP per capita.5 Large differences in institutional quality, in turn, can complicate the conduct of monetary policy.

The reason is that large differences in the way price and wage-setting mechanisms and financial structures are set up can lead to output and inflation responding to shocks in different ways - that is, it leads to the type of cyclical heterogeneity I mentioned earlier that may, as a result, cause the appropriate monetary policy stance to vary across the currency union.6 Such differences in institutional quality are therefore clearly sub-optimal from a monetary policy perspective.

My third reason for why real convergence matters is related to the second point: just as institutional quality matters for monetary policy and closing income level gaps, so do integration and risk-sharing. Deeper integration will help smooth consumption through asymmetric shocks, rather than amplifying those shocks, and will support the process of real convergence.

For example, labour mobility between countries is low and, as we have seen in recent years, is unlikely to be a major source of adjustment once a crisis hits. Although there was an increase in labour mobility in crisis-hit countries, the overall adjustment was limited.

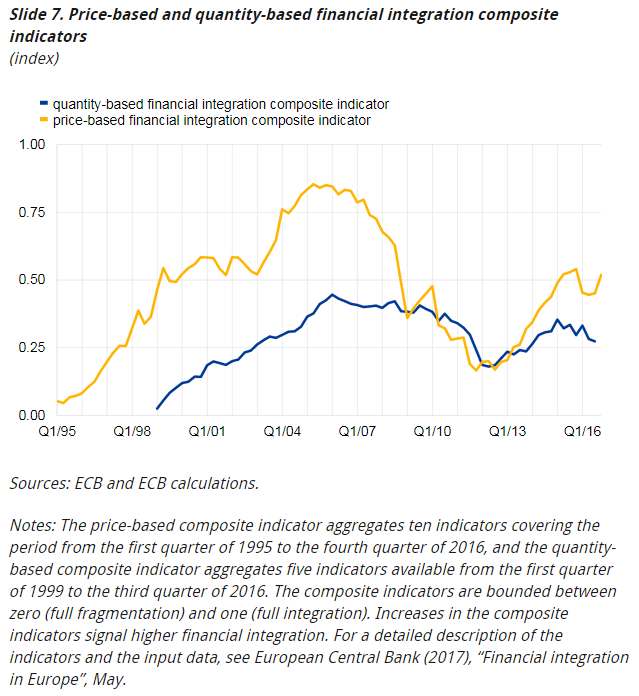

Similarly, financial integration has come to a halt.7 On slide 7 you can see that the latest level of the ECB's quantity-based financial integration composite indicator is comparable to the level in 2004, and the latest level of our price-based composite indicator is roughly comparable to levels observed between 2000 and 2004.

As a result, and in the absence of large-scale fiscal transfers between regions, the degree of risk-sharing in the euro area is lower than in other currency unions. One recent estimate finds that between 1999 and 2014, total risk-sharing through both public and private channels in the United States smoothed 57% of country-specific shocks, compared with just 29% in the euro area.8

This greater degree of risk-sharing derives not just from federal fiscal transfers, but also from greater risk-sharing through credit and financial channels. Credit provision dried up in certain countries during the crisis at precisely the moment when it was needed to smooth income shocks. Clearly, deeper financial integration is needed.

And as I said elsewhere, convergence is also a political prerequisite to engage in a discussion on any new public risk-sharing mechanisms - just like John Rawls pointed out with his concept of the "veil of ignorance".9

Convergence and the need for efficient economic institutions

All this means that if we want to achieve sustainable economic convergence - if we want to reap the full potential of our economies - then we also need to strive for convergence towards high institutional quality and strengthen the integration of our economies and markets. This is also in the interest of monetary policy as I have just explained.

And I want to be clear here, I am talking about convergence in institutional quality, rather than convergence in institutions. In other words, what matters is not the adoption of a single institutional model for Member States, but each Member State adopting a model that delivers the right outcomes while allowing them to find and exploit their comparative advantages in the Single Market and in the Economic and Monetary Union.10

This means that institutions are needed that support and nurture the convergence process, which, broadly speaking, consists of two key elements: accumulating capital and absorbing technological know-how until the frontier is reached. Where institutions are insufficient, there is a risk that capital, rather than being directed to highly productive firms and industries, instead gets siphoned off to ones where productivity is low but economic rents are temporarily high.

Some examples of poor institutions are well known. Product market barriers that protect incumbents from new entrants act as a disincentive to innovate. Low quality education systems starve the economy of the needed technical skills to carry out research and development. Some labour market institutions prevent the reallocation of labour to more productive uses and result in high unemployment and low participation. Supervisory forbearance encourages the evergreening of non-performing loans to non-profitable companies. Politically connected lending prevents the allocation of capital to the most productive firms.

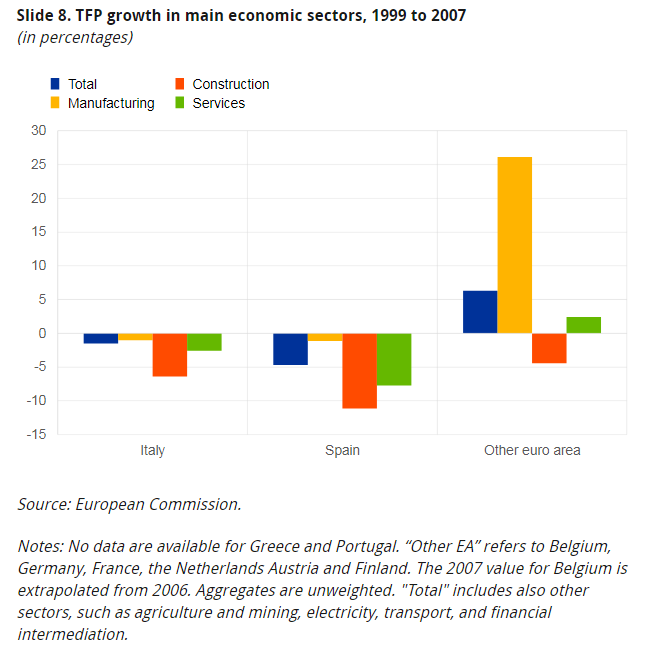

More recently, work with granular data at industry and firm level has helped foster a greater understanding of the interaction between institutions and firm behaviour that ultimately lead to higher total factor productivity (TFP) growth and overall convergence. For example, on slide 8 you can see CompNet data for TFP growth in Italy and Spain between 1999 and 2007. You can see that TFP growth fell across all main economic sectors, in contrast with the overall gain in the rest of the euro area.

These more granular data therefore challenge a popular hypothesis, namely the one that the aggregate TFP slowdown in these economies was primarily driven by a misallocation of cross-border capital flows from higher-income countries to the least productive sectors of the economy, such as construction. If this would be the whole story, why then did TFP growth in the manufacturing sector fall as well?

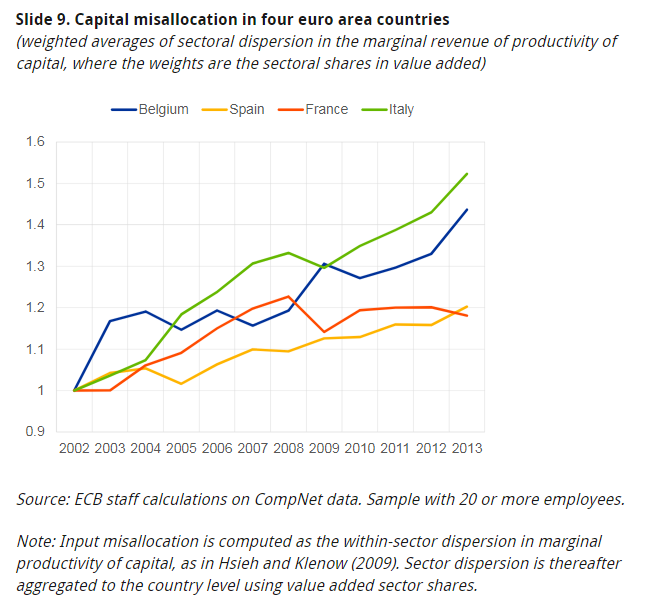

The answer has to do with poor institutions. On slide 9 you can see that the dispersion within sectors of the marginal product of capital has increased, implying that capital was not only allocated inefficiently across sectors, but also within sectors in a number of countries before the crisis.11 This means that a larger proportion of capital within each narrowly defined industry was concentrated in firms that were relatively less productive.

The misallocation of capital, in turn, likely reflects, among other things, a business environment that did not allow productive firms to thrive as well as inefficient legal systems and ineffective government and public administration. This makes one think that, even if capital had flowed to different sectors, it is not certain that relative productivity growth in these countries would have been materially better.

Slide 9 also tells another story, however - namely that capital misallocation (as measured by the dispersion of the marginal product of capital) did not end with the crisis. In fact, in Italy and Spain it is higher today than at any point in time before the crisis. In other words, the process of reallocation of resources from unproductive firms to productive firms during recessions - let's call it the Schumpeterian creative destruction - was not sufficient to boost aggregate productivity during the recovery.

This means that, despite important reform progress, institutional factors in a number of economies with a lower income per capita continue to contribute to protect weaker firms and constrain the creation or growth of more productive ones. The continued operation of weak firms that ought to leave the market - casually called zombie firms - causes a drag on aggregate productivity, impairs the cleansing effects of a recession and thereby stands in the way of allowing these economies to embark on a higher growth path that would help narrow the prevailing income level gaps.

I can already hear those arguing that our low interest rate environment further nurtures the prevalence of zombie firms. But one has to be careful when assessing chains of causality. Low interest rates are primarily caused by an environment of slack in the economy, insufficient expected demand coming from credible structural and institutional reforms and low marginal product of capital. Monetary policy reacts to this in fulfilment of its price stability mandate. If this reaction is associated with undesirable side-effects, such as zombie firms, it is more often than not the lack of proper policies and reforms in other policy areas that are responsible.

Of course, other factors are likely to have temporarily contributed to capital misallocation and hence to poor productivity growth. The crisis, for example, might have restricted access to external finance for financially constrained firms, which sometimes are those with high productivity growth potential.12 Indeed, although the international evidence is somewhat mixed on the impact of credit frictions,13 recent work by ECB staff, again using CompNet data, finds that capital misallocation during the euro area sovereign debt crisis particularly increased among those firms that are more reliant on bank finance, even when taking their level of productivity into account.14

Furthermore, banks typically require loan collateral in the form of tangible assets, such as real estate, machines, etc. This may encourage firms reliant on bank funding to invest more in tangible assets than they would otherwise do. At the same time, research shows that having a greater share of intangible assets is related to a greater ability to create and absorb new technology. These two facts together were shown to have led financially weaker firms to reduce their investment in intangibles assets more than financially stronger firms did during the great recession, and that this effect was greater in countries where credit conditions tightened more.15

But, as I have just said, financial frictions are likely to have been only a temporary factor. With credit supply today no longer a constraining factor, the only major impediment to stronger productivity growth and real convergence is subpar institutions. Therefore, opening up protected sectors, cutting red tape and easing barriers for firm entry would reduce capital misallocation and foster stronger and more sustainable growth.

Conclusions

With this in mind, let me conclude.

The recent broadening of the euro area recovery and the marked drop in cross-country dispersion in a number of economic indicators is an encouraging development. It underscores that our monetary policy measures have materially reduced financial fragmentation and that their positive effects are increasingly spreading more evenly across the euro area. This is a necessary precondition for inflation to move sustainably to levels closer to 2%.

But although growth rates have converged recently, there are still large differences in living standards across euro area countries and, by some measures, they have even increased recently. To a large extent, these differences reflect the quality of national institutions.

Research on granular data that have only recently become available has helped shed light on the underlying microeconomic processes and frictions that govern the aggregate relationship between the quality of institutions and the level of GDP per capita.

That research leads me to my first policy conclusion - that we should facilitate the more widespread availability of granular data to deepen our knowledge of how businesses are performing, as in aggregate this equates to overall macroeconomic performance. I am certain that the insights delivered already by the CompNet project are just the tip of the iceberg.

My second conclusion is that reforms that aim to improve the quality of institutions can help unlock the productive potential of our economies and can provide the basis for a renewed process of real economic convergence - a process that would not only strengthen social cohesion but also the belief in the benefits of our currency union. This is a vitally important goal in and of itself.

In addition, by promoting flexibility and overall living standards in the euro area, improving and harmonising the quality of our institutions also increases countries' ability to cope with adverse shocks, thereby easing the conduct of monetary policy. And by boosting overall potential output it can reduce the current debt overhang in some economies and provide space for fiscal policy to become countercyclical, reducing the overall burden on monetary policy.

Thank you.

1 See Barro, R. and Sala-i-Martin, X. (1992), Convergence, Journal of Political Economy, vol. 100, pp. 223-51.

2 The European Commission's 2018 projections for the output gap (relative to potential GDP) in Germany and Italy are 0.1% and 0% respectively. For HICP inflation, the projections are 1.4% and 1.3% respectively.

3 For a revisitation of this discussion, see Bayoumi, T. and Eichengreen, B. (2017), Aftershocks of Monetary Unification: Hysteresis With a Financial Twist, IMF Working Paper, WP/17/55, March.

4 See Cœuré, B. (2017), Scars or scratches? Hysteresis in the euro area, Speech at the International Center for Monetary and Banking Studies, Geneva, 19 May.

5 See, for example, North, D. (1991), Institutions, institutional change and economic performance, Cambridge University Press, New York; Easterly, W. and Levine, R. (1997), Africa's growth tragedy: policies and ethnic divisions, The Quarterly Journal of Economics, Vol. 112, No 4, pp. 1203-1250; and Hall, R. and Jones, C. (1999), Why do some countries produce so much more output per worker than others, The Quarterly Journal of Economics, Vol. 114, No 1, pp. 83-116. The possible reverse causality from income levels to institutional quality is well known and would deserve further investigation at euro area level, although it is likely to be less significant than between advanced and low-income economies. See Acemoglu, D., Johnson, S. and Robinson, J. (2001), The Colonial Origins of Comparative Development: An Empirical Investigation, American Economic Review, Vol. 91, No 5, pp. 1369-1401.

6 Related to this, see Aghion, P., Farhi, E., and Kharroubi, E. (2017), On the interaction between monetary policy, corporate balance sheets and structural reforms, presented at the ECB Forum on Central Banking, Sintra, June. The authors find that the announcement of Outright Monetary Transactions (OMT) only raised growth in countries where product market regulation is low.

7 See European Central Bank (2017), Financial integration in Europe.

8 Milano, V. and Reichlin, P. (2017), Risk Sharing Across the US and EMU: The Role of Public Institutions, Luiss School of European Political Economy.

9 See Cœuré, B. (2016), Rebalancing in the euro area: are we nearly there yet?, Speech at the Danish Economic Society, Kolding, 15 January. The case for a new convergence process is made by the Five Presidents' Report of June 2015 on Completing Europe's Economic and Monetary Union. See also Coeuré, B. (2015), Towards a political convergence process in the euro area, Speech at the Interparliamentary Conference "Towards a Progressive Europe", Berlin, 16 October.

10 See Draghi, M. (2014), Stability and Prosperity in Monetary Union, Speech at the University of Helsinki, 27 November.

11 Evidence suggests that labour misallocation did not deteriorate much over time. See, for example, Gamberoni, E., Giordano, C. and López-Garcia, P. (2016), Capital and labour (mis)allocation in the euro area: Some stylized facts and determinants, ECB Working Paper No. 1981.

12 See Guillamón, C., Moral-Benito, E. and Puente, S. (2017), High growth firms in employment and productivity: dynamic interactions and the role of financial constraints?, Working Papers, No 1718, Banco de España.

13 See, for example, Barlevy, G. F. (2003), Credit market frictions and the allocation of resources over the business cycle, Journal of Monetary Economics, Vol. 50, Issue 8, pp. 1795-1818; Gopinath, G., Kalemli-Ozcan, S., Karabarbounis, L. and Villegas-Sanchez, C. (2015), Capital allocation and productivity in South Europe, NBER Working Paper 21453.; Osotimehin, S. and Pappadà, F. (2016), Credit frictions and the cleansing effect of recessions, The Economic Journal, Vol. 127, Issue 602; and Gamberoni et al. (2016) op. cit.

14 Bartelsman, E., Lopez-Garcia, P. and Presidente, G. (2017), Factor reallocation in Europe, ECB mimeo.

15 Adler, G. et al. (2017), Gone with the Headwinds: Global Productivity, IMF Staff Discussion Notes, 17/04, International Monetary Fund.