Vítor Constâncio: Effectiveness of Monetary Union and the Capital Markets Union

Contribution of Mr Vítor Constâncio, Vice-President of the European Central Bank, for the magazine of the Eurofi conference in Malta (5-7 April 2017), 4 April 2017.

The views expressed in this speech are those of the speaker and not the view of the BIS.

The euro area recovery is continuing at a moderate, but firming pace, and is broadening gradually across sectors and countries. The ECB's monetary policy measures have been a key contributor to these positive developments, and the only expansionary macroeconomic policy in support of the recovery.

Real GDP growth has expanded for 15 consecutive quarters, growing by 0.5% during the final quarter of 2016. Dispersion in growth rates across euro area countries has fallen. Economic sentiment is at its highest level in nearly six years. The unemployment rate is back down to single-digit figures and over four million more Europeans are employed now than three years ago.

Since the onset of the crisis, the ECB has put in place a number of conventional and unconventional monetary policy measures to stimulate the economy and rehabilitate the monetary transmission mechanism, which had become impaired at the height of the crisis. This comprehensive range of measures has worked its way through the financial system, leading to a significant easing of financing conditions for consumers and firms. Together with improving financial and non-financial sector balance sheets, this has strengthened credit dynamics and supported domestic demand.

Bank lending rates for both euro area households and non-financial corporations have fallen by over 110 basis points since June 2014. Lending rates for small and medium-sized enterprises, which provide two-thirds of total private sector employment in the euro area, have declined by over 180 basis points.

The sharp reduction in bank lending rates has been accompanied by easier access to funding, as recent ECB surveys on bank lending and access to finance have shown. But it is not just lending rates that are more favourable. Bank lending volumes have also been gradually recovering since early 2014. Annual growth in credit to euro area households increased in January to 2.2% and growth in credit to businesses remained at 2.3% - the highest growth rates in more than four years. Market-based funding conditions, too, have improved significantly in response to the corporate sector purchase programme launched in June 2016.

While monetary policy has been the mainstay of the recovery, there are other potential sources of macroeconomic stabilisation. Given the heterogeneity of countries across the euro area, the lack of synchronisation of business cycles, and the absence of fiscal transfers between Member States, capital markets play an important role in mitigating the income effects of region-specific shocks.

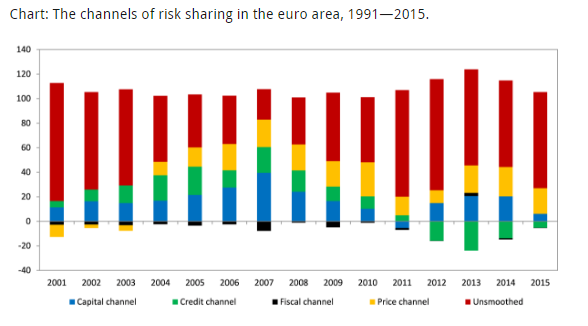

For example, evidence suggests that capital markets and credit markets together help smooth around two-thirds of a shock to regional GDP in the United States, dwarfing the 13% contribution of federal transfers. In comparison, the overall contribution of markets to risk sharing in the euro area has, on average, been limited. There was a brief period in the early-to-mid 2000s when capital markets smoothed between 30 and 40 percent of country-specific shocks to GDP, but this declined substantially during the crisis, and region-specific shocks remain mostly unsmoothed (see Chart).

Given the importance of risk-sharing through capital markets for macroeconomic stability and welfare, we need a Capital Markets Union (CMU) that is ambitious. To be truly effective, CMU will require harmonisation in a number of sensitive areas, including key legislation and policies related to financial products, such as investor protection and bankruptcy procedures.

The CMU should come with a roadmap in terms of goals and milestones to be achieved. Broad objectives such as deepening financial integration and achieving risk sharing should be matched with specific proposals such as facilitating funding for corporates in general and for SMEs in particular.

Chart: The channels of risk sharing in the euro area, 1991-2015.

Note: The Chart summarizes the 5-year cumulative contributions of capital markets, credit markets, fiscal tools, and relative prices to the smoothing, in terms of consumption growth, of a 1-standard-deviation shock to GDP growth. Each bar thus measures the parts of the shock to country-specific GDP that are absorbed by the respective channels. The remainder is interpreted as the unsmoothed portion of a GDP shock, i.e., the part of a shock to country-specific GDP growth that is reflected into country-specific consumption growth. Contributions sum up to 100 percent, and a negative contribution corresponds to dis-smoothing of consumption growth. The respective contributions are estimated over rolling ten-year backward-looking windows, based on annual data and applying the Asdrubali and Kim (2004) approach enhanced for relative price adjustments in the spirit of Corsetti, Dedola, and Viani (2011).