The money flower with selected examples

(Extract from pages 61-62 of BIS Quarterly Review, September 2017)

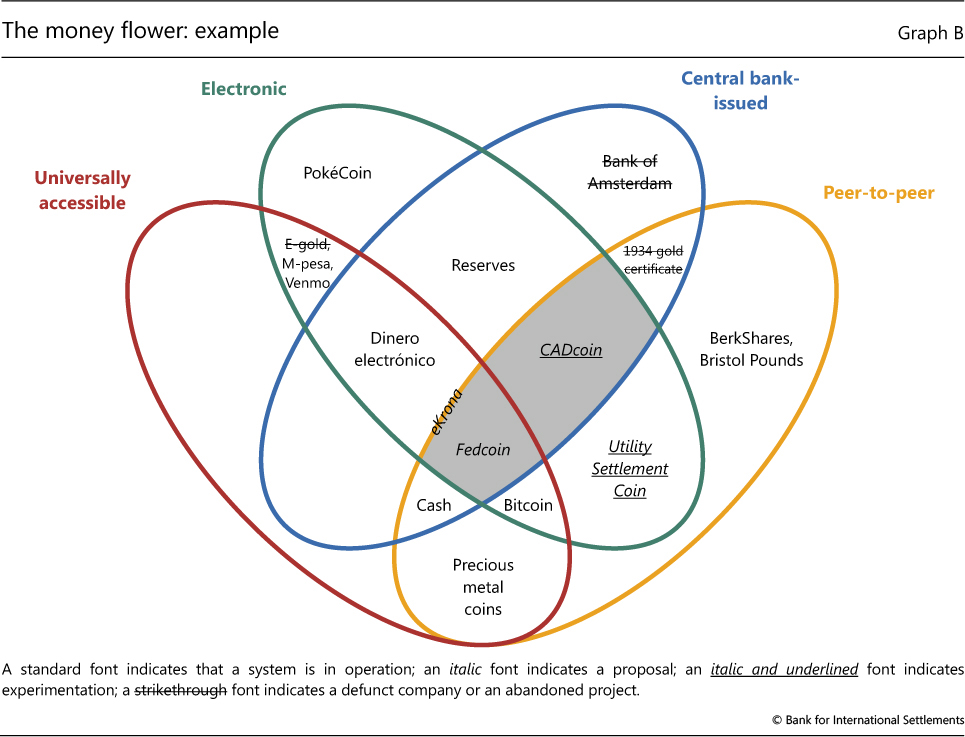

Graph B fills out the money flower with examples of money from the past, present and possibly the future. Starting at the centre, we have Fedcoin, as an example of a retail CBCC. The concept, which was proposed by Koning (2014) and has not been endorsed by the Federal Reserve, is for the central bank to create its own cryptocurrency. The currency could be converted both ways at par with the US dollar and conversion would be managed by the Federal Reserve Banks. Instead of having a predetermined supply rule, as is the case with Bitcoin, the supply of Fedcoin would, much like cash, increase or decrease depending on the desire of consumers to hold it. Fedcoin would become a third component of the monetary base, alongside cash and reserves. Unlike Bitcoin, Fedcoin would not represent a competing, private "outside money" but would instead be an alternative form of sovereign currency (Garratt and Wallace (2016)).

Instead of having a predetermined supply rule, as is the case with Bitcoin, the supply of Fedcoin would, much like cash, increase or decrease depending on the desire of consumers to hold it. Fedcoin would become a third component of the monetary base, alongside cash and reserves. Unlike Bitcoin, Fedcoin would not represent a competing, private "outside money" but would instead be an alternative form of sovereign currency (Garratt and Wallace (2016)).

CADcoin is an example of a wholesale CBCC. It is the original name for digital assets representing central bank money used in the Bank of Canada's proof of concept for a DLT-based wholesale payment system. CADcoin has been used in simulations performed by the Bank of Canada in cooperation with Payments Canada, R3 (a fintech firm), and several Canadian banks but has not been put into practice.

In Sweden, the demand for cash has dropped considerably over the past decade (Skingsley (2016)). Already, many stores do not accept cash and some bank branches no longer disburse or collect cash. In response, the Riksbank has embarked on a project to determine the viability of an eKrona for retail payments. No decision has yet been taken in terms of technology (Sveriges Riksbank (2017)). Hence, the eKrona is located on the border between deposited currency accounts and retail CBCCs.

Dinero electrónico is a mobile payment service in Ecuador where the central bank provides the underlying accounts to the public. Citizens can open an account by downloading an app, registering their national identity number and answering security questions. People deposit or withdraw money by going to designated transaction centres. As such, it is a (rare) example of a deposited currency account scheme. As Ecuador uses the US dollar as its official currency, accounts are denominated in that currency.

Bitcoin is an example of a non-central bank digital currency. It was invented by an unknown programmer who used the pseudonym Satoshi Nakamoto and was released as open-source software in 2009 along with a white paper describing the technical aspects of its design (see Box A for further details).

PokéCoin is a currency used for in-game purchases in the Pokémon Go game and an example of a virtual currency.

Utility Settlement Coin (USC) is an attempt by the private sector to provide a wholesale cryptocurrency. It is a concept proposed by a collection of large private banks and a fintech firm for a series of digital tokens representing money from multiple countries that can be exchanged on a distributed ledger platform (UBS (2016)). The value of each country's USC on the distributed ledger would be backed by an equivalent value of domestic currency held in a segregated (reserve) account at the central bank.

The Bank of Amsterdam (the Amsterdamse Wisselbank) was established in 1609 by the City of Amsterdam to facilitate trade. It is often seen as a precursor to central banks. A problem at the time was that currency, ie coins, was being eroded, clipped or otherwise degraded. The bank took deposits of both foreign and local coinage at their real intrinsic value after charging a small coinage and management fee. These deposits were known as bank money. The Wisselbank introduced a book-entry system that enabled customers to settle payments with other account holders. The Dutch central bank was established in 1814 and the Bank of Amsterdam was closed in 1820 (Smith (1776), Quinn and Roberds (2014)).

The 1934 series gold certificate was a $100,000 paper note issued by the US Treasury and used only for official transactions between Federal Reserve Banks. This was the highest US dollar-denominated note ever issued and did not circulate among the general public. It is an example of non-electronic, restricted-use, government-backed, peer-to-peer money.

Examples of privately issued local currencies include the Bristol Pound and BerkShares, located in the right-hand petal. Stores in Bristol, United Kingdom, give a discount to people using Bristol Pounds, whereas BerkShares are purchased at 95 cents on the dollar and are accepted at retail stores in the Berkshires region of Massachusetts at face value.

Precious metal coins are examples of commodity money. They can be used as an input in production or for consumption and also as a medium of exchange. This is in contrast to fiat money, which has no intrinsic use. Although commodity money is largely a thing of the past, it was the predominant medium of exchange for more than two millennia.

E-gold account holders used commercial bank money to purchase a share of the holding company's stock of gold and used mobile phone text messages to transfer quantities of gold to other customers. Payments between e-gold customers were "on-us" transactions that simply involved updating customer accounts. E-gold ultimately failed. But before it shut down in 2009, it had accumulated over 5 million account holders. Many current private mobile payment platforms, such as Venmo (a digital wallet with social media features popular with US college students) and M-pesa™ (a popular mobile money platform in Kenya and other East African countries), employ a similar "on-us" model. Users transfer either bank deposits or cash to the operator, who gives them mobile credits. These credits can be transferred between platform participants using their mobile devices or redeemed from the operator for cash or deposits. The daily number of M-pesa transactions dwarfs those conducted using Bitcoin. However, in terms of value, worldwide Bitcoin transfers have recently overtaken those conducted on the M-pesa platform (Graph 1, right-hand panel).

Many current private mobile payment platforms, such as Venmo (a digital wallet with social media features popular with US college students) and M-pesa™ (a popular mobile money platform in Kenya and other East African countries), employ a similar "on-us" model. Users transfer either bank deposits or cash to the operator, who gives them mobile credits. These credits can be transferred between platform participants using their mobile devices or redeemed from the operator for cash or deposits. The daily number of M-pesa transactions dwarfs those conducted using Bitcoin. However, in terms of value, worldwide Bitcoin transfers have recently overtaken those conducted on the M-pesa platform (Graph 1, right-hand panel).

Straightforward arguments derived from Friedman (1959) and Klein (1974) suggest that if the Federal Reserve were to maintain one-to-one convertibility with Fedcoin, it would also need to control the supply of Fedcoins. The company ran into trouble with the authorities over anti-money laundering violations and for operating a money transmitter business without the necessary state licence; see http://legalupdate.e-gold.com/2008/07/plea-agreement-as-to-douglas-l-jackson-20080721.html. E-gold account statistics can be found at http://scbbs.net/craigs/stats.html.