Accounting for FX swaps, forwards and repurchase agreements: a simple analysis

(Extract from page 39 of BIS Quarterly Review, September 2017)

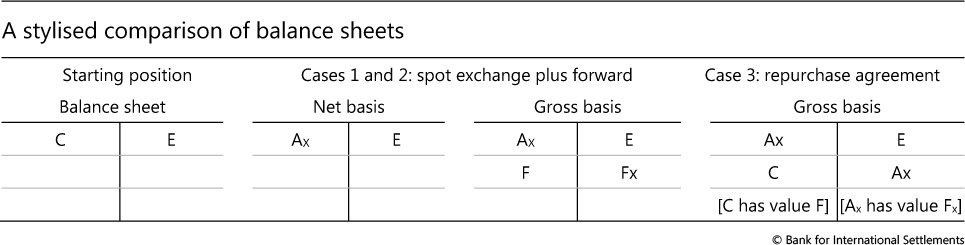

This box explains how the accounting treatment of borrowing and lending through the FX swap and related forward market gives rise to missing debt. It does so with the help of simplified T-accounts. In the process, it also shows what would happen if FX swaps were treated the same as repurchase agreements (repos) - two transactions that can be considered to be forms of collateralised lending/borrowing. The table shows the corresponding balance sheets, with the subscript X denoting foreign currency positions.

Assume that an agent wishes to purchase a foreign currency asset, A, and hedge the corresponding FX risk. The agent begins with holdings of local currency C, and no debt, ie C equals net worth, E (left-hand panel).

One option (case 1) is for the agent to use the available cash to buy foreign currency in the FX market, purchase the foreign asset and at the same time enter an outright forward contract, committing to sell an equivalent amount of foreign currency for domestic currency at an agreed price at maturity. The forward creates an obligation to come up with foreign currency (a liability), matched by the right to receive the domestic currency (an asset), both equal to the current value of the foreign currency asset. The obligation to repay is a form of debt.

Table A also shows two possible ways of recording the transaction in the accounts: on a net basis, ie the way it is currently done, and on a gross basis, with the rights and obligations being explicitly shown as assets and liabilities, denoted by F (for forward). Recording on a net basis shows an apparent currency mismatch: the asset is in foreign currency, Ax, and the equity in domestic currency, E. This apparent mismatch disappears if the transaction is recorded on a gross basis, as the forward foreign currency liability, Fx, offsets the foreign currency asset, Ax.

Next, imagine that the agent entered an FX swap instead (case 2). The accounts would be identical to those in case 1. This is because an FX swap consists of two legs: the exchange today (or spot leg) and the commitment to exchange in the future - precisely the forward leg. The only difference from case 1 is that two transactions become one contract with the same counterparty.

Now assume that the agent decided to avoid the FX risk by keeping the cash in domestic currency and financing the foreign security in the foreign repo market (case 3). That is, the agent finances the security at purchase by immediately selling it while committing to buy it forward at an agreed price. (Here we abstract from the haircut so that the security is altogether self-financing.) Current accounting principles require that this be reported on a gross basis, so that the balance sheet doubles in size. Yet the position is functionally equivalent to that of an FX swap or forward. There is no FX risk, and the agent needs to finance the future obligation (debt) by coming up with the corresponding foreign currency to settle the forward leg (cases 1 and 2) or to repurchase the foreign currency-denominated asset (case 3). The only difference is that in case 3 the agent has the freedom to use the domestic currency cash to buy another domestic currency asset rather than having it tied up in a forward claim.

Why such a difference in accounting treatment? One reason is that forwards and swaps are treated as derivatives, so that only the net value is recorded at fair value, while repurchase transactions are not. Since the value of the forward claim exchanged at inception is the same, the fair value of the contract is zero and it changes only with variations in exchange rates. Yet, unlike with most derivatives, the full notional amount, not just a net amount as in a contract for difference, is exchanged at maturity. That is, the notional amounts are not purely used as reference for the income streams to be exchanged, such as in interest rate derivatives. Another reason is the definition of control, which for cash requires control over the cash itself (eg a demand deposit) but for a security just the right to the corresponding cash flows. This determines what is recognised and not recognised on the balance sheet.