Currency movements drive reserve composition

A long-standing puzzle in international finance is the durability of the dollar's share of foreign exchange reserves - which remains above 60%, while the weight of the US economy in global output has fallen to less than a quarter. We argue that the dollar's role may reflect instead the share of global output produced in countries with relatively stable dollar exchange rates - the "dollar zone". If a currency varies less against the dollar than against other major currencies, then a reserve portfolio with a substantial dollar share poses less risk when returns are measured in domestic currency. Time series and cross-sectional evidence supports the link between currency movements and the currency composition of reserves.1

JEL classification: E58, F31, F33.

Observers of international finance have long puzzled over the durability of the dollar's predominance in official foreign exchange reserves. Heller and Knight (1978) found that "on average, the countries in our sample tend to hold 66% of their foreign-exchange reserves in dollars". Some 36 years later, the IMF reports that 61% of allocated aggregate reserves are held in dollars. This is despite the dollar's 18% decline against major currencies and its 62% and 52% depreciations against the Deutsche mark/euro and the yen, respectively. Moreover, the US economy's share of global GDP has shrunk by 6% since 1978. If one takes the size of the US economy to explain the dollar's share, then one might infer that this share would decline only slowly unless and until another economy surpasses the US economy in size.2

This special feature proposes an alternative interpretation based on the size not of the US economy but rather of the "dollar zone". Despite the dollar's decline and the shrinking share of the US economy, the dollar zone still accounts for more than half of the global economy. In countries whose currencies are more stable against the dollar than against the euro, a reserve composition that favours the dollar produces more stable returns in terms of the domestic currency. This alternative interpretation implies that currency shares could shift rapidly, as happened between the world wars (Eichengreen and Flandreau (2010)).

This special feature argues in five sections that currency movements drive the currency composition of reserves. The first section sets out the main explanations that have been put forward for the currency composition of reserves. The second discusses time series evidence, both historically around currencies joining or quitting the sterling zone and since 1990. The third examines current cross-sectional evidence for two dozen economies. Our hypothesis competes with other hypotheses in the fourth section, and the fifth concludes.

Explanations for the currency composition of forex reserves

How should reserve managers choose the currency composition of their reserves? The numeraire that is used to measure risks and returns has a very strong influence on calculated optimal currency allocations (Papaioannou et al (2006), Borio et al (2008a)). Its choice depends on the intended uses of the reserves. If reserves are held mainly to intervene in the currency market, then a plausible numeraire would be the currency against which the domestic currency trades most heavily, especially in the spot market where most central banks operate. If reserves are held mainly to insure purchases of foreign goods and services, then an import basket would be plausible. Or, if reserves are held mainly as a hedge against (or to pay) debt service, the currency composition of outstanding debt would be a plausible choice.

The domestic currency may serve as the numeraire for economic or institutional reasons. Where reserves exceed transaction or insurance needs, their value as domestic wealth can be measured in terms of domestic currency. Or, the domestic currency may be used as numeraire owing to its use in valuing foreign exchange reserves in striking the central bank's accounting profit and reported capital. These may affect a central bank's reputation or even its operational independence.

A survey found a considerable range of choice (Borio et al (2008b)). About a third of central banks used the domestic currency, a fifth a basket of foreign currencies and the rest a single foreign currency. One third used the US dollar. Some central banks used different numeraires for different tranches, which themselves were distinguished by use (eg liquidity versus investment).

The next two sections provide evidence consistent with the use of the domestic currency as numeraire. The share of the dollar in reserves is higher where the domestic currency varies less against the dollar than other major currencies.

The time series evidence

The historical record of changes in the composition of reserves is quite telling. Looking back to the interwar period and the 1960s and 1970s: as economies joined (or left) the sterling area, their reserve composition shifted towards (or away from) sterling. In the period since 1990, the relative stability of the dollar share of reserves reflects the stability of the dollar zone at more than half of global output. In both cases, we observe that reserves are held in the major currencies that move less against the domestic currency.

Entering and leaving the sterling area

Historically, reserve shifts by those authorities whose currencies entered or left the sterling area show this logic at work. After the Scandinavian currencies joined the sterling area in the wake of the UK currency's 1931 floating (Drummond (2008)), central banks shifted their reserves into sterling.3 Similarly, after the yen was pegged to sterling in 1934, sterling's share of Japanese reserves reached 90% in 1935, from just 15% in 1932 (Hatase and Ohnuki (2009), Figure 3).

Conversely, after leaving the sterling area, monetary authorities cut their holdings of sterling. For instance, in the 1968 Basel sterling agreement, the Bank of England guaranteed the dollar value of the 99% of Hong Kong's reserves that were invested in sterling (Schenk (2010), pp 295-6). After Hong Kong replaced its peg to sterling with its first dollar peg in July 1972, the proportion of Hong Kong's reserves held in dollars rose to 20% by September 1974 (Schenk (2009)) - and to 75% now, 31 years after the subsequent peg to the dollar in 1983.

Similar observations hold for less extreme reserve portfolios in the sterling area. In 1968, the Bank of England guaranteed the dollar value of the 70%, 45% and 40% of their reserves that were invested in sterling by New Zealand, Iceland and Australia, respectively. After the Australian and New Zealand dollars were pegged to the US dollar in the Smithsonian Agreement of December 1971, and then both to baskets by July 1973, the sterling share fell to about 20% by 1974 for Australia and by 1977 for New Zealand (Schenk and Singleton (forthcoming)). Today, New Zealand, Iceland and Australia hold 15%, 15% and 0% of their reserves in sterling and 25%, 40% and 55% in dollars, as described below.

The dollar zone and the dollar share of reserves since 1990

The dollar's role as reference for other countries' exchange rates ranges from dollar pegs, at one end, to largely market-driven co-movements under free-floating regimes as influenced by interest rate policies, at the other. By examining the degree of co-movements, and predefining the set of key currencies, we derive a measure of each such currency's zone of influence using simple regression techniques (see Annex for details). We use the euro (before 1999, the Deutsche mark) and yen as the other candidate reference currencies, consistent with their status as the second and third most transacted currencies in the Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity.

We then define not a tightly linked dollar bloc, but rather a fuzzier dollar zone. A given country's GDP contributes to this zone in proportion to its currency's dollar weight. So defined, the dollar zone accounts for more than half of global GDP.4

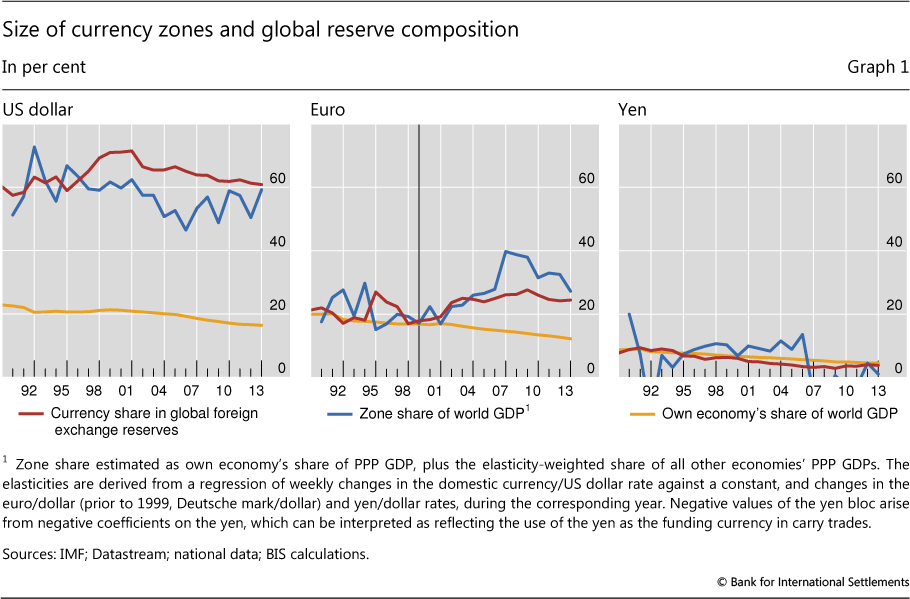

By this measure, the US dollar's pre-eminent influence as a reference currency lines up with its relative role as store of value for official reserves. The dollar zone has been close to 60% of global GDP and has shown little trend since 1990 (Graph 1, blue line in the left-hand panel). This 60% is much closer to the dollar share of reserves than the global share of the US economy (here measured in PPP terms, but the point would still hold at market values). The euro zone share of global GDP is now around 25%, just above the euro's (reduced) share of reserves. The yen trails.

A stable dollar zone share of global GDP is at first puzzling, given that the euro's influence has extended east in Europe (ECB (2014)), to commodity currencies and even as far as emerging Asia. However, Asia's fast growth has offset the euro's wider influence, given the diminished yet still strong dollar linkage of Asian currencies.

In sum, the dollar's share in global forex reserves tracks over time the share of the dollar zone in global output. Together with the cross-sectional evidence to which we now turn, this evidence suggests the importance of portfolio considerations and the domestic currency numeraire.

Cross-sectional evidence

The insight that the way a currency trades against the major currencies guides the choice of the currency denomination of reserves has found only limited use in previous cross-sectional studies. IMF studies of confidential data, whether Heller and Knight (1978), Dooley et al (1989) or Eichengreen and Mathieson (2000), use dummies for pegs. They thus restrict to only extreme cases a test of the connection between currency anchoring and reserve composition.

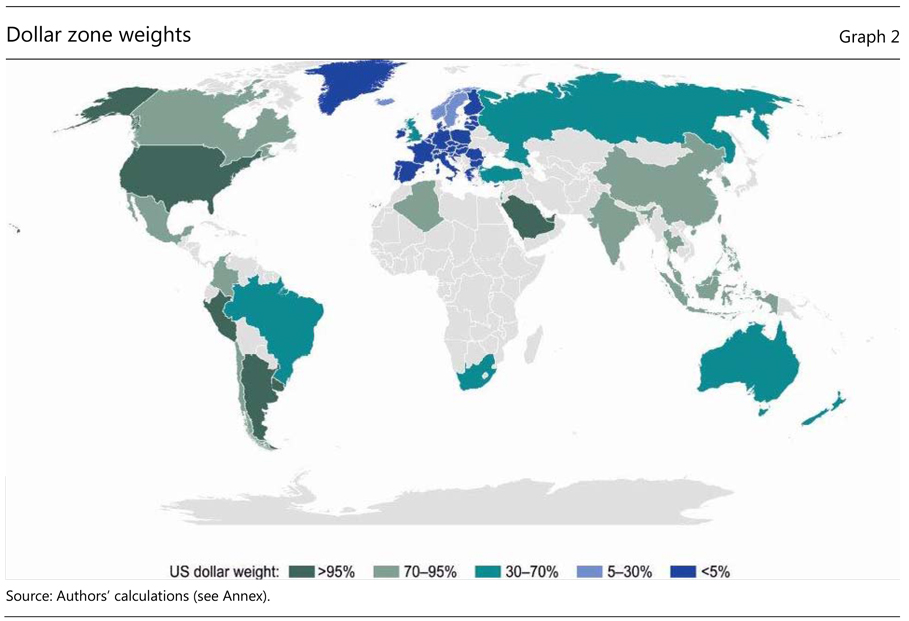

The less restrictive approach sketched above provides quite a different picture. Graph 2 shows the dollar share based on weekly changes over the calendar years 2010-13. Most economies outside the United States, the euro area and Japan are intermediate cases, with dollar zone weights of less than 95% and above 5%.

Intermediate status derives from explicit management or from a combination of policy and market responses. For example, the Central Bank of the Russian Federation (2013, p 75; ECB (2014), p 67) has managed the Russian rouble against a basket of €0.45 and $0.55. And indeed, we compute its weight on the dollar at 0.55. Another intermediate case, the free-floating pound sterling, has a dollar weight of 0.45, as Haldane and Hall (1991) find for the late 1970s.5

The calculation summarised in Graph 2 questions the widespread view that western hemisphere currencies are all firmly attached to the dollar. Other than the currencies of highly dollarised Peru and Uruguay, the co-movement with the euro of the Chilean, Colombian and Mexican pesos, or especially the Brazilian real, contradicts the long-standing notion of a solid dollar zone in the western hemisphere. Similarly, the co-movement of the Australian, New Zealand and, to a lesser extent, Canadian dollars with the euro against the dollar suggests that the "dollar bloc" label, still used by many asset managers, has outlasted its sell-by date.6

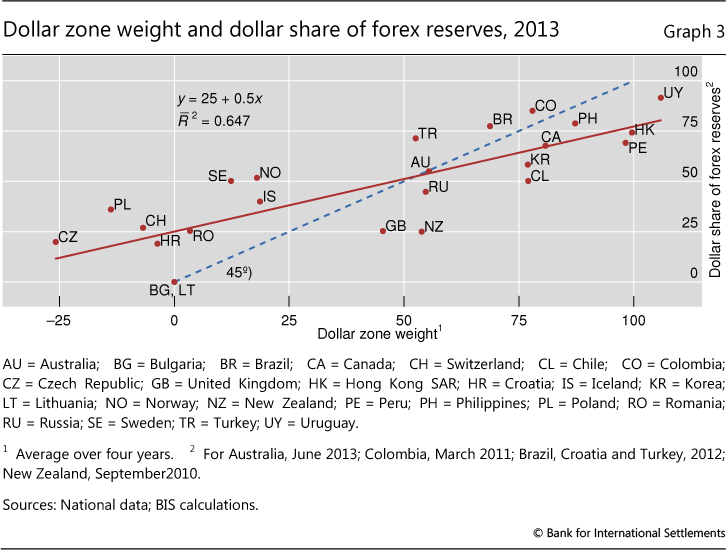

Does a currency's dollar weight influence the share of the US dollar in the corresponding country's official reserves? Yes, the limited cross-sectional evidence strongly suggests (Graph 3). Broadly, central banks in the Americas heavily weight the dollar, which remains the most important influence on their currencies despite the rising importance of the euro. Most European central banks do not hold such a high share of dollars, and Russia, Turkey, the United Kingdom, Australia and New Zealand are in between. Two thirds of the cross-sectional variation in the dollar share in foreign exchange reserves can be accounted for by the currencies' average dollar zone weight in 2010-13.

The slope of the least squares line (in red in Graph 3) is not 1 (dashed blue line), as would be the case if reserve managers on average chose the dollar weight to minimise the variance of their portfolios in domestic currency.7 Instead, the estimate of the slope of one half points to some departure from the minimum variance portfolio, perhaps in some cases to raise expected funds.

The necessary caveat to this strong finding is that the sample may not be representative. At the end of 2013, the 24 economies in Graph 3 accounted for $2.8 trillion of reserves, just 28% of the global total not held by the United States, the euro area and Japan.8 The 24 clearly oversample small and advanced economies. Among the top 20 holders of reserves, emerging market economies Brazil, Hong Kong SAR, Korea, Russia, and Turkey are included, but eight are not: China, Saudi Arabia, Chinese Taipei, India, Singapore, Mexico, Algeria and Thailand.

Given that previous work has used currency pegs, but not behavioural anchors, to explain the currency composition of reserves, it strengthens our result to note that it does not depend on pegs. In particular, if we exclude Bulgaria, Hong Kong and Lithuania, the estimated relationship is indistinguishable statistically from that in Graph 3. Furthermore, if we exclude currencies that the IMF (2013, pp 5-6) characterises as having a "crawl-like" (Croatia) or "other managed arrangement" (Russia and Switzerland), the result does not change much.9 All in all, the relationship does not depend on economies where the currency is heavily managed.

Where might the largest reserve holder, China, place on Graph 3? If its reserve composition was at the average for emerging market economies reported to the IMF (Bénétrix et al (forthcoming)), then China would be the largest outlier: with only 60% of reserves held in the dollar on the vertical axis but a calculated dollar zone weight of 93% on the horizontal axis.10 If market estimates of a lower dollar share are given credence, China would be a larger outlier. But if the medium-term management of the renminbi is interpreted as an upward crawl against China's trade-weighted basket (Ma et al (2012)), then the dollar zone share would be about half, lower than our estimate based on weekly changes.11

Private asset and debt managers also align their portfolios with their home currency's dollar zone weights. This is interesting in its own right and also gives us more confidence in the small-sample relationship between currency movements and the official foreign currency portfolio. Moreover, the tendency of the private sector to denominate its debt in the major currency that is more stable against the domestic currency reinforces the reserve managers' rationale for investing in it.12

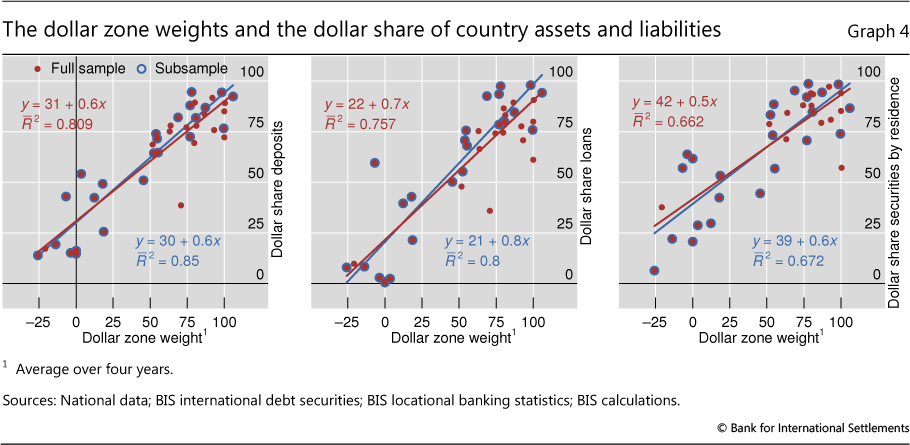

Graph 4 (left-hand panel) relates the share of cross-border dollar deposits by country to the dollar zone share. The blue-circled dots indicate Graph 3's sample of 24 economies; the red dots, an additional 15 economies. Offshore bank deposits include some official holdings, but would usually be dominated by holdings of banks, firms and some households. The relationship is remarkably similar to that between the dollar zone weight and official reserve composition. The dollar share of deposits is somewhat higher (larger estimated intercept) and responds more strongly to the dollar zone share (steeper estimated slope), and overall is more tightly related to the dollar zone weight, with 81% of its variance accounted for.

Corresponding considerations bear on banks and firms - and, in some countries, households - in choosing the currency composition of their foreign currency liabilities. Graph 4 (centre panel) shows the relationship between the dollar share of cross-border bank loans to domestic residents and the dollar zone share, with blue-circled dots again showing Graph 3's sample of 24 countries. The relationship is very strong. The right-hand panel plots the dollar share of outstanding issues of international debt securities by residents against the dollar zone weight. Here, the relationship is similar to that in Graph 3 for official reserves.

Thus, although our sample of disclosed currency compositions of reserves is limited, larger samples measuring the dollar share of economy-wide stocks of assets and liabilities bolster the small-sample results. The co-movement of a currency with the dollar is strongly associated with the dollar share of private assets and liabilities. While Dooley et al (1989) and Eichengreen and Mathieson (2000) use the currency composition of broad external debt stocks to explain the currency composition of official reserves, we consider that both respond to currency movements. In any case, any notion that official reserves hedge or provide for the servicing of foreign currency debt only reinforces the rationale for matching the reserve composition to the dollar zone share.

The dollar share of foreign exchange trading?

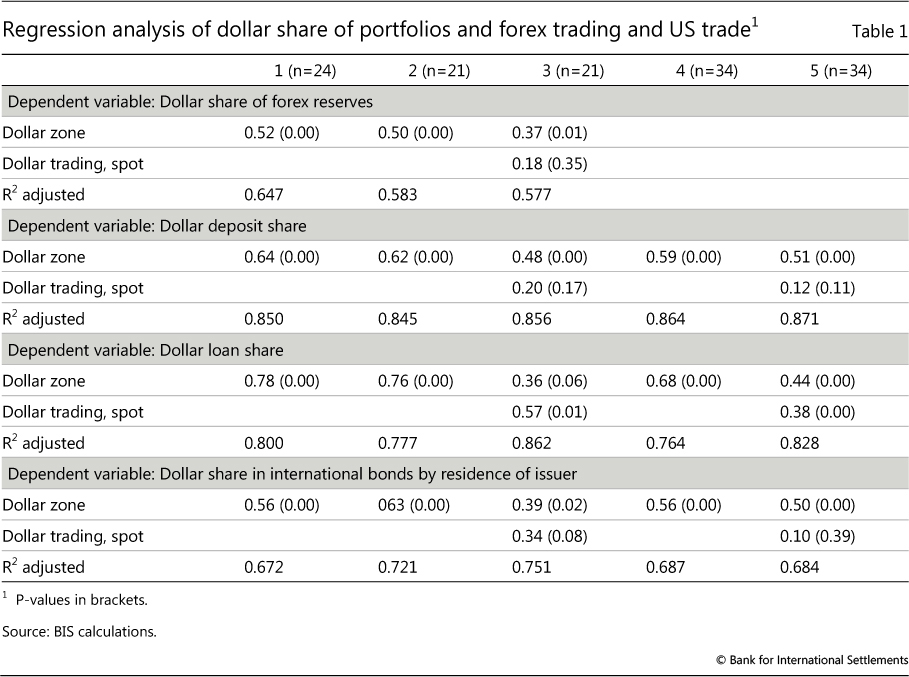

While the various functions of an international money mutually reinforce each other,13 this section allows the dollar's means of exchange function to compete with currency movements in accounting for the dollar share of reserves in the cross section. Particularly if reserves are not large, the share of trading of the domestic currency against the dollar in the foreign exchange market could constrain the choice of the dollar share of reserves. Our measure of the share of dollar trading is derived from the results for spot trading in the Triennial Survey of April 2013, which improved on reporting on a range of emerging market currencies.14

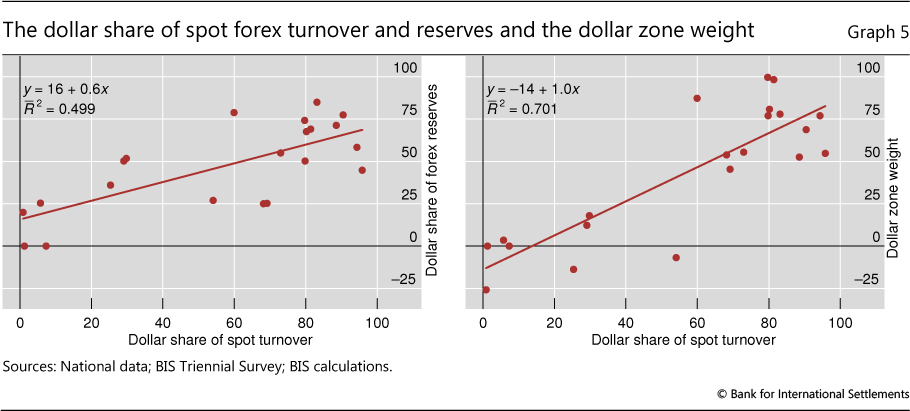

On a bivariate basis, the share of dollar trading in the spot market does fall into line with the share of dollar reserves (Graph 5, left-hand panel). This is not surprising because the share of dollar trading is quite highly correlated with the dollar zone share (Graph 5, right-hand panel). But in a multivariate analysis of the dollar share of reserves, the dollar zone weight dominates the dollar share of trading in the currency market (Table 1, top panel). Portfolio considerations seem more important than trading in the spot market.

For completeness, and as a complementary test given the small size of our sample, the bottom three panels of Table 1 report regressions of the broader stocks of mostly private assets and liabilities on the same factors. Only the dollar zone weight seems to matter for the dollar deposit share (second panel). Alongside the dollar zone weight, the proportion of dollar trading emerges as a significant factor in the dollar share of loans and international bonds (third and fourth panels). However, these wider debt aggregates may themselves give rise to sufficient foreign exchange transactions as to explain the dollar trading share (reverse causation).

All in all, a currency's co-movement with the dollar bears a robust relationship to the dollar share of assets and liabilities. Currency geography is portfolio destiny.

Conclusions

We find that the higher the co-movement of a given currency with the dollar, the higher the economy's dollar share of official reserves. Two thirds of the variation in the dollar share of foreign exchange reserves is related to the respective currency's dollar zone weight.

This association is supported by the currency composition of broader economy-wide balance sheets including the private sector. After all, our sample of official reserves is limited to only 24 economies representing $2.8 trillion or 28% of official foreign exchange reserves outside the G3. As a sort of robustness check, we assess the same relationship between currency movements and portfolio choices for $6 trillion, $6 trillion and $7 trillion in bank deposits, bank loans and international bonds outstanding, respectively. We find - if anything - stronger relationships.

The logic underlying both private and official behaviour is straightforward. The dollar looks less risky as an investment or a borrowing currency the more closely the domestic currency moves with the dollar.

Looking forward, our findings also have implications for the possible evolution of the currency composition of official reserves. They suggest that changes in the co-movement of currencies could result in more rapid than commonly thought shifts in the composition of reserves, potentially eroding the weight of the dollar. By the same token, they indicate that country size alone may be less relevant.

If correct, these findings have implications for the future of the renminbi. The continued relatively rapid growth of the Chinese economy, even if accompanied by developing money and bond markets, opening of the capital account and floating of the renminbi, might not be sufficient for the currency to eclipse the dollar in official reserve holdings. By contrast, if the renminbi at some point showed substantial independent movement against the major currencies and if its neighbours' and trading partners' currencies shared that movement, then it might be said that "the renminbi bloc [ie zone] is here" (Subramanian and Kessler (2013), but see also Kawai and Pontines (2014) and Shu et al (2014)). In that case, official reserve managers might hold a substantial share of renminbi, perhaps not too far from their currencies' renminbi zone weights.

References

Bénassy-Quéré, A, B Cœuré and V Mignon (2006): "On the identification of de facto currency pegs", Journal of the Japanese and International Economies, vol 20, pp 112-27.

Bénétrix, A, P Lane and J Shambaugh (forthcoming): "International currency exposures, valuation effects and the global financial crisis", Journal of International Economics.

Borio, C, J Ebbesen, G Galati and A Heath (2008a): "FX reserve management: elements of a framework", BIS Papers, no 38, March.

Borio, C, G Galati and A Heath (2008b): "FX reserve management: trends and challenges", BIS Papers, no 40, May.

Bracke, T and I Bunda (2011): "Exchange-rate anchoring: is there still a de facto dollar standard?", ECB Working Paper Series, no 1353, June.

Central Bank of the Russian Federation (2013): Annual Report, Moscow, May.

Chinn, M and J Frankel (2007): "Will the euro surpass the dollar as a reserve currency?", in R Clarida (ed), G7 current account imbalances, University of Chicago Press, pp 285-322.

--- (2008): "Why the euro will rival the dollar", International Finance, vol 11, pp 49-73.

Dooley, M (1986): "An analysis of the management of the currency composition of reserve assets and external liabilities of developing countries", in R Aliber (ed), The reconstruction of international monetary arrangements, Macmillan, pp 262-80.

Dooley, M, S Lizondo and D Mathieson (1989): "The currency composition of foreign exchange reserves", IMF Staff Papers, vol 36, pp 385-434.

Drummond, I (2008): The floating pound and the sterling area: 1931-1939, Cambridge University Press.

Eckhold, K (2010): "The currency denomination of New Zealand's unhedged foreign reserves", Reserve Bank of New Zealand Bulletin, vol 73, no 3, September, pp 37-46.

Eichengreen, B and M Flandreau (2010): "The Federal Reserve, the Bank of England and the rise of the dollar as an international currency, 1914-39", BIS Working Papers, no 328, November.

Eichengreen, B and D Mathieson (2000): "The currency composition of foreign exchange reserves: retrospect and prospect", IMF Working Papers, no 00/131, July.

European Central Bank (2014): The international role of the euro, July.

Frankel, J (2009): "New estimates of China's exchange rate regime", Pacific Economic Review, no 14 (3), pp 346-60.

Frankel, J and S-J Wei (1996): "Yen bloc or dollar bloc? Exchange rate policies in East Asian economies", in T Ito and A Krueger (eds), Macroeconomic linkage: savings, exchange rates, and capital flows, University of Chicago Press, pp 295-329.

--- (2007): "Assessing China's exchange rate regime", Economic Policy, July, pp 577-627.

Haldane, A and S Hall (1991): "Sterling's relationship with the dollar and the Deutschemark: 1976-89", Economic Journal, vol 101, no 406, May.

Hatase, M and M Ohnuki (2009): "Did the structure of trade and foreign debt affect reserve currency composition? Evidence from interwar Japan", Bank of Japan Institute for Monetary and Economic Studies, Discussion Paper Series, 2009-E-15.

Heller, H and M Knight (1978): "Reserve currency preferences of central banks", Princeton Essays in International Finance, no 131, December.

International Monetary Fund (2013): Annual Report on exchange arrangements and exchange restrictions, October.

Ito, H and M Chinn (2014): "The rise of the 'redback'", Asian Development Bank Institute Working Paper Series, no 473.

Kawai, M and S Akiyama (1998): "The role of nominal anchor currencies in exchange rate arrangements", Journal of the Japanese and International Economies, vol 12, pp 334-87.

Kawai, M and V Pontines (2014): "Is there really a renminbi bloc in Asia?", Asian Development Bank Institute Working Paper Series, no 467, February.

Ma, G and R McCauley (2011): "The evolving renminbi regime and implications for Asian currency stability", Journal of the Japanese and International Economies, vol 25, no 1, pp 23-38.

Ma, G, R McCauley and L lam (2012): "Narrowing China's current account surplus: the role of saving, investment and the renminbi", in H McKay and L Song (eds), Rebalancing and sustaining growth in China, ANU Press and Social Sciences Research Press (China), pp 65-91.

Papaioannou, E, R Portes and G Siourounis (2006): "Optimal currency shares in international reserves", Journal of the Japanese and International Economies, vol 20(4), December, pp 508-47.

Schenk, C (2009): "The evolution of the Hong Kong currency board during global exchange rate instability, 1967-1973", Financial History Review, vol 16, pp 129-56.

--- (2010): The decline of sterling: managing the retreat of an international currency, 1945-1992, Cambridge University Press.

Schenk, C and J Singleton (forthcoming): "The shift from sterling to the dollar 1965-76: evidence from Australia and New Zealand", Economic History Review.

Setser, B and A Pandey (2009): "China's $1.5 trillion bet: understanding China's external portfolio", Council on Foreign Relations Working Paper, May.

Shu, C, D He and X Cheng (2014): "One currency, two markets: the renminbi's growing influence in Asia-Pacific", BIS Working Papers, no 446, April.

Subramanian, A and M Kessler (2013): "The renminbi bloc is here", Peterson Institute for International Economics Working Paper Series, WP 12-19, August.

Annex: Estimating the US dollar, euro and yen zones

The size of, say, the dollar zone is measured using variants of the methodology developed by Haldane and Hall (1991) and Frankel and Wei (1996). Kawai and Akiyama (1998) and Bénassy-Quéré et al (2006) have similarly applied this method.

The dollar share is calculated in two steps. First, for a given currency, its weekly percentage change against the dollar is regressed on the weekly percentage change of the euro/dollar and yen/dollar rates. The dollar zone weight is calculated as 1 minus the corresponding regression coefficients. For example, for sterling in 2013 the pound's estimated coefficient on the euro/dollar rate is 0.60 and on the yen/dollar is 0.09. So, the dollar weight for the pound is (1 - 0.60 - 0.09), or 0.31. For the Hong Kong dollar, the coefficients would be zero; and hence the dollar zone weight, 1.

Second, across currencies, the dollar share is then calculated using (PPP) GDP weights. Each of the 39 economies' (49 before the euro) dollar zone weight is multiplied by the respective GDP, and the product is added to the US GDP. This sum is then expressed as a share of the total GDP of the 42 major economies analysed, including those of the United States, the euro area and Japan. This analysis produces dollar zone weights of 1 for Hong Kong SAR and Saudi Arabia, and zero for Bulgaria.

There are four issues: three concern the technique and one the results. First, the selection of major currencies is a prior choice. It is grounded in the Triennial Survey finding of the three most traded currencies.15

Second, as regards the choice of numeraire, many analysts seek to avoid a major currency and use the SDR or Swiss franc. Our approach, which uses the dollar, assigns a given currency to the dollar zone if its movements against the dollar have nothing in common with those of the euro or the yen. But, as long as the coefficients are interpreted correctly, the results do not depend on the choice of numeraire (Ma and McCauley (2011), Table 1). Moreover, as a practical matter, use of the SDR may make it more difficult to collect simultaneous observations for the three currencies, which become econometrically more crucial the higher the frequency. Nevertheless, we have re-computed the dollar zone by regressing weekly percentage changes in a given currency's SDR exchange rate on percentage changes in the dollar/SDR, euro/SDR and yen/SDR rates. Except for the polar cases, the dollar weights thus derived tend to be lower, but the correlation is 0.85. As a result, however, the goodness of fit of Graph 2 using these alternative dollar zone estimates is only a bit lower, with an adjusted R2 of 0.56 rather than 0.65.

Third, there is a question of data frequency. Our use of weekly data, as opposed to higher-frequency data, strikes an appropriate balance between estimation precision and reducing the downward bias from non-simultaneous observation of the three exchange rates used. In addition, it may work better with managed exchange rates if the authorities limit daily dollar movements but track a basket over lower frequencies (Frankel and Wei (2011), Ma and McCauley (2011)).

And fourth, the estimation for the last 10 years has often produced negative coefficients on the yen for a range of commodity currencies. For example, these indicate that the Brazilian real falls against the US dollar when the yen rises against the dollar. Thus, in Graph 1, the yen zone becomes negative in some years, as portions of commodity currencies' (that load on the yen) GDPs outweigh Japanese GDP. One way of interpreting these observations is that they reflect carry trades in which the yen is a funding currency. These observations highlight the possibility that conventional measures understate the yen's role in international finance, because hard-to-measure derivatives transactions are important in its use as a funding currency.

1 The authors thank Claudio Borio, Michael Dooley, Marc Flandreau, Guonan Ma, Madhu Mohanty, Denis Pêtre, Catherine Schenk, Jimmy Shek, Hyun Song Shin and Christian Upper for their discussions. The views expressed are those of the authors and do not necessarily reflect those of the BIS.

2 Chinn and Frankel (2007, 2008) ascribe the dollar's high share of reserves to the size of the US economy in an inductively non-linear relationship. This allows reserves in dollars to amount to more than twice those held in euros while the economy of the United States is only a third larger than that of the euro area.

3 Personal communication with Marc Flandreau.

4 Cf Kawai and Akiyama (1998), Bénassy-Quéré et al (2006) and Bracke and Bunda (2011).

5 If most shocks to the euro/dollar exchange rate do not imply a change in the pound's effective exchange rate, then one would expect the dollar zone weight to match the weight of the US and other dollar zone economies in the pound's trade-weighted basket. In fact, the dollar zone weight is close to leaving the effective pound exchange rate unchanged with changes in the euro/dollar rate. Thus dollar zone weights for floating currencies may be grounded in trade shares, and hence the gravity model.

6 Indeed, the recent appeal to reserve managers of the Australian dollar (its IMF-reported share in global reserves was 1.9% in June 2014) might have arisen from its euro co-movement and yield.

7 The biggest outlier is New Zealand, which, like Canada and the United Kingdom, borrows most of its reserves. The currency denomination of borrowed reserves can be matched to the corresponding liabilities to avoid currency exposure. Thus, the domestic currency numeraire may be irrelevant to the choice of the currency composition. However, Graph 3 plots New Zealand's 25% weight on the dollar for the portion of reserves that is "unhedged" (owned outright against the New Zealand dollar), so it really is an outlier. In cash terms, 60% of New Zealand's reserves are held in the US dollar, because "the NZD/USD cross rate is the main traded market [and] intervention aims to influence the value of the NZD through operations in the NZD/USD market" (Eckhold (2010), p 40). Forward sales of 35% of the US dollars against other currencies including the Australian dollar reconcile the 60% cash holding and the 25% ultimate dollar weight. Thus, the need to hold the US dollar as an intervention currency does not determine the ultimate currency composition of reserves.

8 Since the G3 countries cannot hold their own currencies in their reserves, they face a different set of choices from other reserve holders.

9 The slope is slightly flatter at 0.4 and the adjusted R2 falls by little (0.555). If we further exclude the nine currencies classified as merely "floating", and run the regression for only the eight currencies classified as "free-floating", then the slope flattens to 0.3 and the adjusted R2 falls to 0.344. In this sample, the problem of borrowed reserves (Canada and the United Kingdom) is acute (see footnote 7).

10 China could be a still bigger outlier if the dollar zone estimates were based on higher-frequency (daily or intraday) data; see Frankel and Wei (2007) and Frankel (2009). However, it would be a smaller outlier if Setser and Pandey (2009, p 1) were and continue to be correct in their conclusion that "dollar assets constitute at least 65 percent of China's aggregate portfolio", and the reserve portfolio resembled and continues to resemble the aggregate portfolio.

11 The BIS effective renminbi exchange rate features equal one sixth weights for the dollar, euro and yen, with most of the balance accounted for by regional currencies.

12 Dooley (1986) analyses net currency positions.

13 Dollar trade invoicing encourages exporters (especially commodity exporters) to borrow dollars to hedge and importers to borrow dollars for working capital. Servicing dollar debts tilts trading towards the dollar, encouraging reserve managers to hold dollars. Using the limited evidence on the invoicing of imports by 11 of the 24 economies from Ito and Chinn (2014), we found an anomalous negative relationship between the dollar share of trade invoicing and the dollar share of reserves. Following Eichengreen and Mathieson (2000), we tried trade with the United States as a share of trade, but it never entered significantly in the presence of the dollar zone weight.

14 Despite the improvements in the 2013 survey, reporting on the eight smaller currencies among our 24 was less complete. When we exclude the data for BG, CL, CO, CZ, LT, PE, PH and RO (Graph 3), the relationships in Graph 5 are weaker, but the results in Table 1 (top panel) are similar, albeit the R2 is lower.

15 Subramanian and Kessler (2013) find evidence for the existence of a renminbi bloc in Asia, but this is questioned by Kawai and Pontines (2014) and Shu et al (2014).