How does US monetary policy affect policy rates in emerging market economies?

(Extract from pages 6-7 of BIS Quarterly Review, March 2014)

Monetary policy in advanced economies, especially in the United States, appears to have a significant influence on the conduct of monetary policies in many emerging market economies (EMEs). During the global "search for yield", many EMEs were concerned that large interest rate differentials vis-à-vis advanced economies would lead to destabilising capital inflows and overvalued exchange rates. In recent years, this seems to have kept EME policy rates lower than what purely domestic conditions would have implied. Conversely, the beginning of the normalisation of US monetary policy has already started to induce upward adjustments in policy rates, amplified by a turn in investor sentiment, a reversal of capital flows and strong downward pressure on exchange rates.

One way to assess the factors driving EME policy rates is to estimate a Taylor equation. The standard Taylor equation uses two domestic variables to explain policy rates: inflation (or its deviation from the target) and the output gap. The intuition is straightforward: countercyclical monetary policy should raise rates if inflation is rising or the economy is overheating - and lower rates if inflation is declining or output falls short of its potential. We augment this standard Taylor equation with an additional term in order to assess the impact of US monetary policy. Formally, we estimate the equation below for each EME:

Formally, we estimate the equation below for each EME:

where rEME denotes the monetary policy rate of the EME in question, π the inflation rate and y the output gap; rUS denotes the "shadow" policy rate of the United States. As usual, ε denotes the error term and t is the quarterly time index. The sample covers 20 EMEs over the Q1 2000-Q3 2013 period.

As usual, ε denotes the error term and t is the quarterly time index. The sample covers 20 EMEs over the Q1 2000-Q3 2013 period.

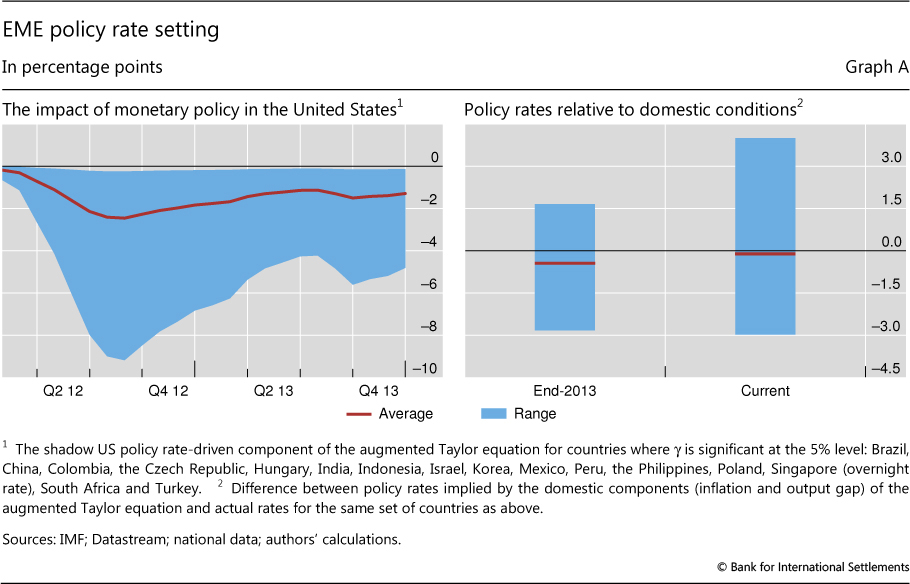

The results confirm that the augmented Taylor equation is broadly consistent with the evolution of EME policy rate setting, ie the regression fits the observed policy rates well. They confirm that US monetary policy has a significant effect over and above domestic conditions: US monetary policy, captured by parameter γ, is statistically significant for most emerging markets (16 out of 20). More specifically, the results indicate that in these economies US monetary policy is associated with on average 150 basis points lower policy rates since 2012 (Graph A, left-hand panel, red line), albeit with substantial heterogeneity across countries and time (blue shaded band). This is consistent with recent findings suggesting that EME monetary policy tended to be more accommodative than the Taylor rule prescription. For example, even at the end of 2013, after the adjustments induced by the May sell-off, EME policy rates tended to be lower by an average of 50 basis points than the levels suggested by the domestic components of the Taylor equation estimates (Graph A, right-hand panel, red line on the first column). The recent policy tightening in EMEs helped to eliminate this gap on average (red line on the second column). However, these averages hide a substantial increase in dispersion (blue bars), which reflects some sudden and concentrated shifts as opposed to a broad-based realignment of policy rates

For example, even at the end of 2013, after the adjustments induced by the May sell-off, EME policy rates tended to be lower by an average of 50 basis points than the levels suggested by the domestic components of the Taylor equation estimates (Graph A, right-hand panel, red line on the first column). The recent policy tightening in EMEs helped to eliminate this gap on average (red line on the second column). However, these averages hide a substantial increase in dispersion (blue bars), which reflects some sudden and concentrated shifts as opposed to a broad-based realignment of policy rates

Of course, a comparison of policy rates with a simple benchmark should be interpreted with caution. Measuring unobservable variables, such as the output gap, is fraught with difficulties. Even the policy rate might not be an accurate measure of monetary conditions, because EMEs have increasingly used non-interest rate monetary policy measures and macroprudential tools to affect monetary conditions. And the results, even if representative for EMEs as a group, should not be seen to apply to all individual EMEs. That said, the finding of unusually accommodative conditions in EMEs seems rather robust. It would survive the use of other benchmarks, such as the growth rate of the economies. And it is consistent with the presence of strong credit and asset price booms in several countries. In particular, recent evidence suggests that potential output tends to be overestimated when such booms are under way.

For more details on the estimation, see E Takáts and A Vela, "International monetary policy transmission", BIS Papers, 2014 (forthcoming), available upon request. The paper shows that the standard Taylor rule does not fully capture the development of policy rates in most EMEs, and that including a measure of the US policy rate improves the estimates significantly. The shadow policy rate was developed in M Lombardi and F Zhu, "Filling the gap: a factor based shadow rate to gauge monetary policy", 2014 (mimeo), in order to account for the impact of unconventional US monetary policies once the zero lower bound was reached. Naturally, this shadow rate can be negative. See further in B Hofmann and B Bogdanova, "Taylor rules and monetary policy: a global 'Great Deviation'?", BIS Quarterly Review, September 2012. C Borio, P Disyatat and M Juselius, "Rethinking potential output: embedding information about the financial cycle", BIS Working Papers, no 404, February 2013.