Treatment of sovereign risk in the Basel capital framework

(Extract from pages 10-11 of BIS Quarterly Review, December 2013)

It is sometimes asserted that the Basel capital framework prescribes a zero risk weight for bank exposures to sovereigns. This is incorrect. Basel II and Basel III call for minimum capital requirements commensurate with the underlying credit risk, in line with the objective of ensuring risk sensitivity. This is the basic philosophy of the framework.

In most jurisdictions, the treatment of sovereign exposures in the banking book follows the Basel II framework, which Basel III has not changed.

in the banking book follows the Basel II framework, which Basel III has not changed. Jurisdictions may adopt one of two (or both) methodologies: the Standardised Approach, which relies on external credit ratings; and the Internal Ratings-Based (IRB) approach, which relies on banks' own risk assessments.

Jurisdictions may adopt one of two (or both) methodologies: the Standardised Approach, which relies on external credit ratings; and the Internal Ratings-Based (IRB) approach, which relies on banks' own risk assessments.

The most relevant standard for internationally active banks is the IRB approach. This approach has been designed bearing in mind the world's largest banks, including global systemically important banks (G-SIBs). The IRB approach requires banks to assess the credit risk of individual sovereigns using a granular rating scale, accounting for all relevant differences in risk with a bespoke risk weight per sovereign. Risk weights are primarily determined by banks' own estimates of probability of default (PD) and loss-given-default (LGD) for a given exposure. The approach does not prescribe minimum levels of PD or LGD for sovereign exposures, but it includes detailed qualitative minimum requirements. In particular, the framework requires a "meaningful differentiation" of risk.

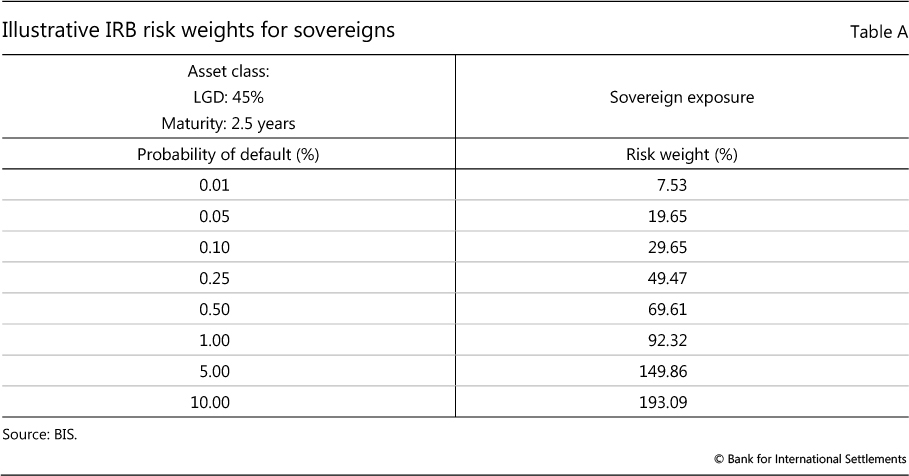

For illustrative purposes, Table A below sets out PDs and their associated risk weights for banks using the Foundation IRB approach. This variant of the IRB, in contrast to its advanced counterpart, allows banks to rely on their risk assessments for PDs but requires them to use a standard LGD of 45% set by supervisors. The PDs are subject to supervisory validation. Data collected by the Basel Committee covering 201 large banks show a weighted mean PD for sovereign exposures subject to the IRB approach of 0.1%.

The Basel framework is based on the premise that banks use the IRB approach across the entire banking group and across all asset classes. It recognises, however, that it may not be practicable for banks to implement the IRB approach across all asset classes and business units at the same time. Therefore, it allows national supervisors to permit their banks to phase in the approach across the banking group. And, subject to strict conditions, it also allows them to keep some exposures in the Standardised Approach indefinitely. For this to be the case, however, these exposures have to be in non-significant business units or in asset classes that are immaterial in terms of size and perceived risk. As a result, banks adopting the IRB approach are expected, over time, to move all material exposures to the IRB framework.

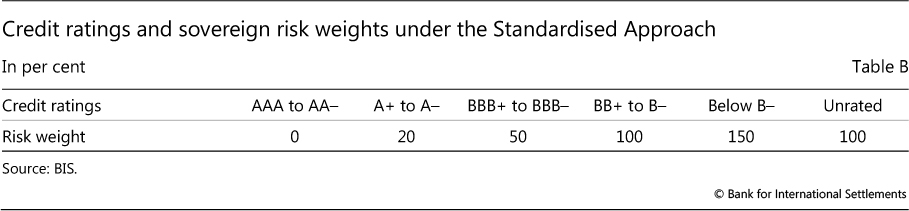

The Standardised Approach, as a rule, also prescribes positive risk weights. As shown below, based on external credit ratings, it assigns a positive risk weight to all but the highest-quality credits (AAA to AA). That said, national supervisors are allowed to exercise discretion and set a lower risk weight provided that the exposures are denominated and funded in the currency of the corresponding state.

There are significant differences in the application of the Basel rules across jurisdictions. For instance, in the United States, internationally active banks are required to implement the IRB approach; a parallel run is under way and the process is not yet finalised. As a result, for the time being, they continue to use the local version of the Standardised Approach. In the European Union (EU), authorities have allowed supervisors to permit banks that follow the IRB approach to stay permanently on the Standardised Approach for their sovereign exposures. In applying the Standardised Approach, in turn, EU authorities have set a zero risk weight not just to sovereign exposures denominated and funded in the currency of the corresponding Member State, but also to such exposures denominated and funded in the currencies of any other Member State.

For instance, in the United States, internationally active banks are required to implement the IRB approach; a parallel run is under way and the process is not yet finalised. As a result, for the time being, they continue to use the local version of the Standardised Approach. In the European Union (EU), authorities have allowed supervisors to permit banks that follow the IRB approach to stay permanently on the Standardised Approach for their sovereign exposures. In applying the Standardised Approach, in turn, EU authorities have set a zero risk weight not just to sovereign exposures denominated and funded in the currency of the corresponding Member State, but also to such exposures denominated and funded in the currencies of any other Member State.

As a consequence of these differences, applied sovereign risk weights vary considerably for large international banks, including global systemically important ones. In fact, the variation in sovereign risk weights is an important source of the variability in risk-weighted assets across banks. It is the national authorities' responsibility to implement the IRB approach in a manner consistent with the Basel framework so as to achieve appropriate risk weights for sovereigns.

Sovereign exposures comprise those to the central government and corresponding central bank. Basel I's treatment of sovereign risk was based on the distinction between OECD and non-OECD members. Under Basel I, banks assigned a 0% risk weight to exposures to OECD member countries; exposures to non-OECD countries were assigned a 100% risk weight. The Basel I framework remains the minimum standard in some jurisdictions. See Basel Committee on Banking Supervision, Regulatory consistency assessment programme (RCAP) - Analysis of risk-weighted assets for credit risk in the banking book, July 2013. Where this discretion is exercised, and in order to ensure a level playing field, bank supervisory authorities in other jurisdictions may also permit their own banks to apply the same risk weights to the given sovereign under the same conditions, ie as long as those exposures are denominated and funded in the corresponding currency. Basel Committee on Banking Supervision, Progress report on implementation of the Basel regulatory framework, October 2013. This provision will be phased out gradually between 2017 and 2020. The new framework, governed by the Capital Requirements Directive IV (CRD IV) and coming into force from January 2014, supersedes the treatment enshrined in CRD III. It requires that, following the phasing-out, the corresponding exposures rely on credit rating agencies' assessments.