Understanding globalisation

Abstract

Economic globalisation has contributed to a substantial rise in living standards and falling poverty over the past half-century. Tighter trade and financial integration are deeply intertwined: international trade not only relies on, but also generates, financial linkages. Together, international trade and finance have enhanced competition and spread technology, driving efficiency gains and aggregate productivity. Like any other form of far-reaching economic change, globalisation poses challenges. For example, globalisation has coincided with rising withincountry income inequality in some countries, although the evidence indicates that technology has been the main driver. Moreover, financial openness exposes economies to destabilising external influences. Properly designed domestic policies can enhance the gains from globalisation and mitigate the adjustment costs. And international cooperation must supplement such policies in order to address global linkages. Completing international financial reforms is one priority. Global currencies call for international cooperation, effective crisis management and more systematic consideration of cross-border spillovers and spillbacks.

Full text

Globalisation has had a profoundly positive impact on people's lives over the past half-century. Nevertheless, despite its substantial benefits, it has been blamed for many shortcomings in the modern economy and society. Indeed, globalisation has faced more severe criticism than technological innovation and other secular trends that have potentially had even more profound consequences. This chapter outlines how increased economic globalisation - tighter trade and financial integration - has contributed to a remarkable increase in living standards. Adjustment costs and financial risks need to be carefully managed, but they do not justify a backlash against globalisation. 1

Trade and financial openness are deeply symbiotic. Trade integration not only relies on, but generates, financial linkages. Banks with international operations underpin trade financing and follow their customers into foreign markets. Trade denominated in a foreign currency can require hedging, with counterparties accumulating international positions. Firms may build capacity in a foreign country with an attractive skill or resource base in order to export from there. Managing the financial asset and liability positions built up through trade induces still deeper financial linkages, including international trade in financial services.

Tighter global economic integration has been hugely beneficial. Globalisation has been instrumental in raising living standards and has helped lift large parts of the world population out of poverty. Trade openness has greatly enhanced productive efficiency and vastly improved consumption opportunities. Financial openness, in addition to supporting international trade, allows greater scope for diversifying risks and earning higher returns. It also makes funding more readily available and facilitates the transfer of knowledge and know-how across countries.

Globalisation has also posed well known challenges. Gains from trade have not been evenly distributed at the national level. Domestic policies have not always succeeded in addressing the concerns of those left behind. The requisite structural adjustment has taken longer, and been less complete, than expected. Furthermore, unless properly managed, financial globalisation can contribute to the risk of financial instability, much like domestic financial liberalisation has. And, not least through financial instability, it can increase inequality. But globalisation has also often been made a scapegoat. For instance, there is ample evidence that globalisation has not been responsible for the majority of the concurrent increase in within-country income inequality.

Attempts to roll back globalisation would be the wrong response to these challenges. Globalisation, like technological innovation, has been an integral part of economic development. As such, it should be properly governed and managed. Countries can implement domestic policies that boost resilience. These include flexible labour and product markets and policies that enhance adaptability, such as retraining programmes. Close cross-country linkages imply that policies and actions of individual countries inevitably affect others. Hence, international cooperation must supplement domestic policies. In particular, a global regulatory framework should be the basis for a sound and resilient international financial system.

This chapter first outlines the deep interconnectedness of trade and financial openness and sets out a stylised framework to analyse globalisation. It then maps out the historical path of globalisation - from the "first wave" leading up to World War I, through the "great reversal" of the interwar years, to the revival and surge in globalisation post-World War II in the "second wave". The chapter argues that recent suggestions of "peak globalisation" are misleading. Next, it reviews how the structure of trade and financial integration has evolved in the second wave. It then discusses the impact of globalisation on welfare, noting its contribution to the substantial growth in incomes and the dramatic decline in poverty as well as the risks to financial stability linked with financial openness. The final section makes some concluding observations, discussing policy measures that can further enhance the benefits of globalisation and minimise the adjustment costs.

Trade and financial openness are intertwined

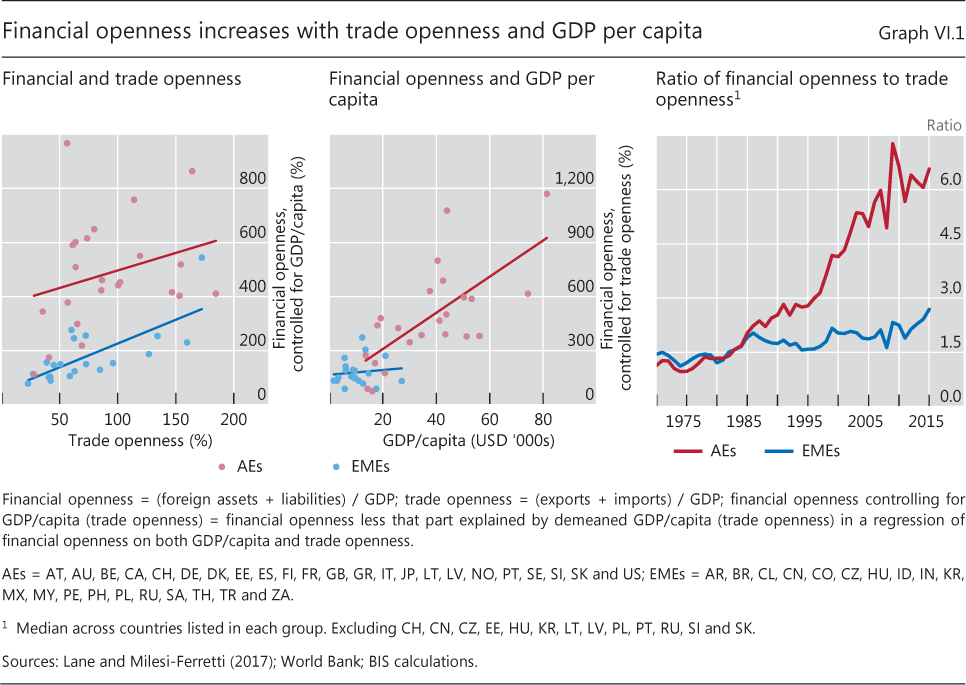

International trade and financial openness go hand in hand. Trade is facilitated by financial links, such as international payments and credit, and in turn results in financial links, such as the accumulation of international assets and liabilities. As a result, it is not surprising that countries that are more open to trade also tend to have higher financial openness (Graph VI.1, left-hand panel).

The relationship between real and financial openness, however, evolves with the degree of integration and development. Conceptually, one can think of three globalisation layers. The first, most basic layer is trade of commodities and finished goods and the corresponding simple international financial links, such as cross-border payments. The second layer involves more complex trade and financial connections. It includes trade in intermediate goods and services associated with the efficiency-driven fragmentation of production across countries and the corresponding financing arrangements. The third layer concerns the financial transactions increasingly used to actively manage balance sheet positions. These positions include the stocks of assets and liabilities, and exposures more generally, created by the first two layers, as well as the allocation and diversification of savings, not necessarily related to trade. The third layer thus introduces some decoupling between real and financial openness.

The links between trade and financial openness are most immediate in the first globalisation layer. Trade in this layer is mostly driven by resource endowments and is directly supported by a range of international financial services. Trade is settled with international payments, which almost always involve foreign exchange transactions. Indeed, trade payments are generally denominated in a global currency rather than that of either the exporter or importer: around half of all international trade is invoiced in US dollars and close to a quarter in euros (even excluding the trade of the United States and euro area countries, respectively). 2 Furthermore, as international transactions take time to complete given shipping time and customs processing, they require extra financing. Banks' trade finance facilitates around one third of international trade, with large global banks providing between one quarter and one third of this. 3 Letters of credit, where a bank guarantees payment upon delivery of goods, underpin around one sixth of trade.

In the second globalisation layer, international financial linkages support a greater degree of specialisation in trade and production, notably in the trade of intermediate goods. Production can occur through ownership of foreign facilities established by foreign direct investment (FDI), outsourcing to foreign firms, or fragmented production in a global value chain (GVC). This more complex trade can go hand in hand with the growth of multinational corporations that serve multiple markets, often through production-focused foreign affiliates while concentrating research and development in the parent. 4 These more intricate production structures require more, and often more complex, financing. GVC-related investments may call for cross-border financing, often in foreign currency. And longer production chains may involve more working capital and larger foreign currency exposures. 5 Finance can promote trade by reducing these risks, for instance through derivatives or borrowing in foreign currency to match corresponding income streams.

The third globalisation layer is characterised by intricate financial links established solely for financial purposes. This layer builds upon the first two to the extent that trade has generated stocks of assets and liabilities that need to be managed financially. More generally, the demand for, and supply of, more sophisticated financial products and services increases with the wealth of businesses and households. In a sense, trade also supports this third layer of globalisation through its contribution to higher income growth. Indeed, financial openness tends to increase strongly with income levels (Graph VI.1, centre panel). However, gross foreign asset and liability positions grow much larger than net positions, underlining the more independent nature of financial linkages: financial openness has substantially outpaced real openness since the late 1980s, most notably for advanced economies (Graph VI.1, right-hand panel).

The three layers share some common elements. One is the use of global currencies. As the dominant global currency, the US dollar is used to denominate not only around half of trade, but also roughly half of global cross-border bank claims and more than 60% of central banks' foreign exchange assets, and features in 90% of foreign exchange transactions. Consequently, the dollar plays a central role in determining global financial conditions (see also Chapter V). Another is globally active financial institutions. They operate in many countries across multiple continents. Through their international presence and sophistication, they facilitate the global transfer of funding and financial risks. Balance sheets that are managed at a consolidated level create close international financial linkages.

The evolution of globalisation

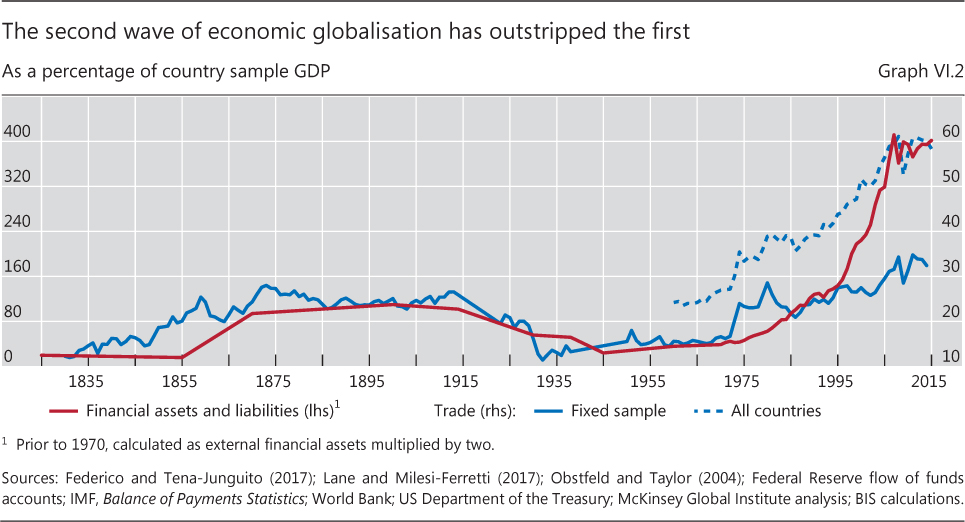

The first globalisation wave, which died out with World War I and the Great Depression, saw a substantial increase in both real and financial cross-border linkages. Trade openness for the then major economies, measured as the ratio of imports plus exports to GDP, more than doubled from the early 1800s to be close to 30% by the turn of the century (Graph VI.2). 6 The increase in financial openness, measured as investment assets held by foreigners as a share of GDP, was no less dramatic, with capital flows to colonies particularly notable. However, the first globalisation wave was relatively simple: most transactions were in the first, or second, layer. The collapse of the first wave was as remarkable as its build-up: the "great reversal" in the interwar period witnessed an almost complete unwinding. Many factors contributed, not least increased protectionism, responsible for around half of the decline in global trade in the Great Depression. 7

The second globalisation wave, starting after World War II, has far outstripped the first. Trade openness surged beyond its prewar peak as countries traded more, and more countries traded. For the world as a whole, trade openness has doubled since 1960 (Graph VI.2). Improvements in transport and communication have again played a role, but trade liberalisation has been a much more important factor than in the first wave. 8 Trade growth in the two decades up to the mid-2000s was particularly rapid: China and former communist countries re-entered global trade and the second globalisation layer expanded quickly. The specialisation through the division of production stages across national borders resulted in the unprecedented expansion of GVCs.

Financial openness increased with trade openness in both waves, but its rise has been much more marked in the second. Available estimates, while highly imperfect, suggest that financial openness is more than triple its prewar peak. External financial assets and liabilities have soared, from around 36% of GDP in 1960 to around 400% ($293 trillion) in 2015.

The rapid expansion in financial openness from the mid-1990s has been concentrated in advanced economies. Relative to GDP, the external positions of advanced economies and emerging market economies (EMEs) were roughly equal up until the early 1990s. Since then, the cross-border financial assets and liabilities of advanced economies have surged, from roughly 135% to over 570% of GDP. In contrast, the increase for EMEs during the same period was more modest, from approximately 100% to 180% of GDP.

Trade

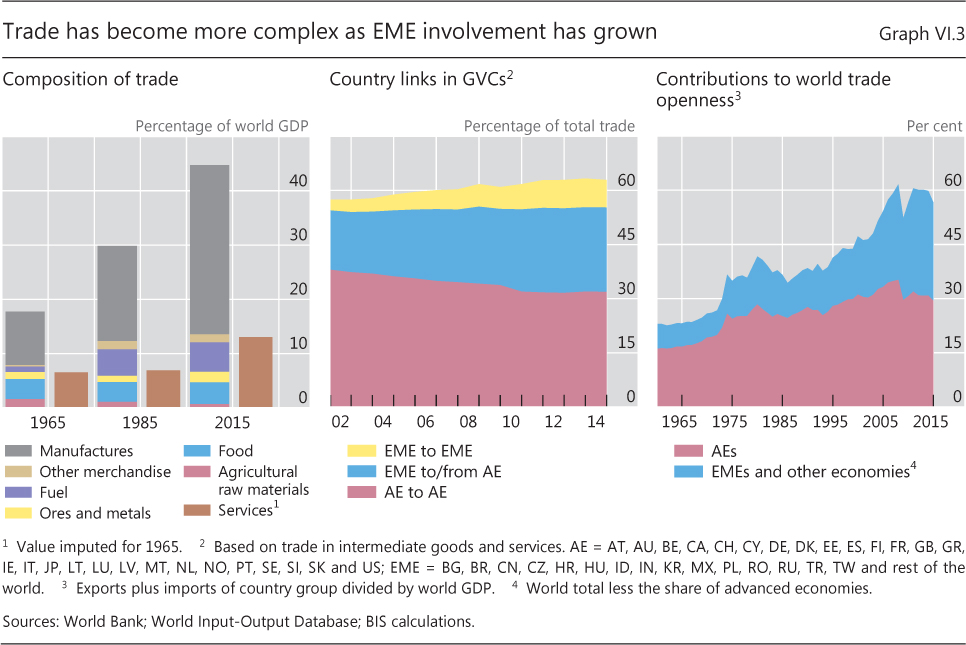

The nature of trade has changed markedly during the second globalisation wave. Economic development, greater market access, and improvements in transportation and in information and communication technology have broadened the range of items traded. Natural resource endowments were an important determinant of trade flows 50 years ago, with much of trade in the first globalisation layer. Now, the location of skilled and unskilled labour and relative expertise has become more important, with the second globalisation layer becoming dominant. In the early 1960s, food accounted for nearly one quarter of traded goods; today, its share is less than 10% (Graph VI.3, left-hand panel). Similarly, trade in fuel and that in metals and ore are little changed as a share of GDP, abstracting from the large price swings in those commodities. In contrast, trade in services, including financial, has surged over the past three decades, from 7% of global GDP to 13%. And by far the biggest change has been the growth in the trade of manufactured goods: they now constitute over half of global trade.

GVCs have been a key driver of trade growth, especially in manufactured goods, facilitated by the improvements in market access, transport and technology. 9 The process started in the mid-1980s, with high- and low-skill tasks increasingly being located in different countries. As a result, trade in intermediate goods and services now accounts for almost two thirds of total global trade.

EME participation in GVCs has increased dramatically. In 2014, EMEs were involved in half of GVC trade, as measured by trade in intermediate goods and services, up from around one third in 2001 (Graph VI.3, centre panel). The share of GVC trade between EMEs has more than doubled. China alone is now responsible for 19% of GVC trade, up from 7%. And in the process, intra-EME trade integration has increased at a faster rate than that of advanced economies, alongside EMEs' greater heft in the world economy (Box VI.A; Graph VI.3, right-hand panel).

Large multinational corporates dominate global trade. These firms, with operations in multiple countries, often play a prominent role in GVCs. For example, in the United States around 90% of trade involves multinationals, and half is between related entities within a multinational. 10 Despite the expansion in EME trade, multinationals remain more prevalent in advanced economies.

Finance

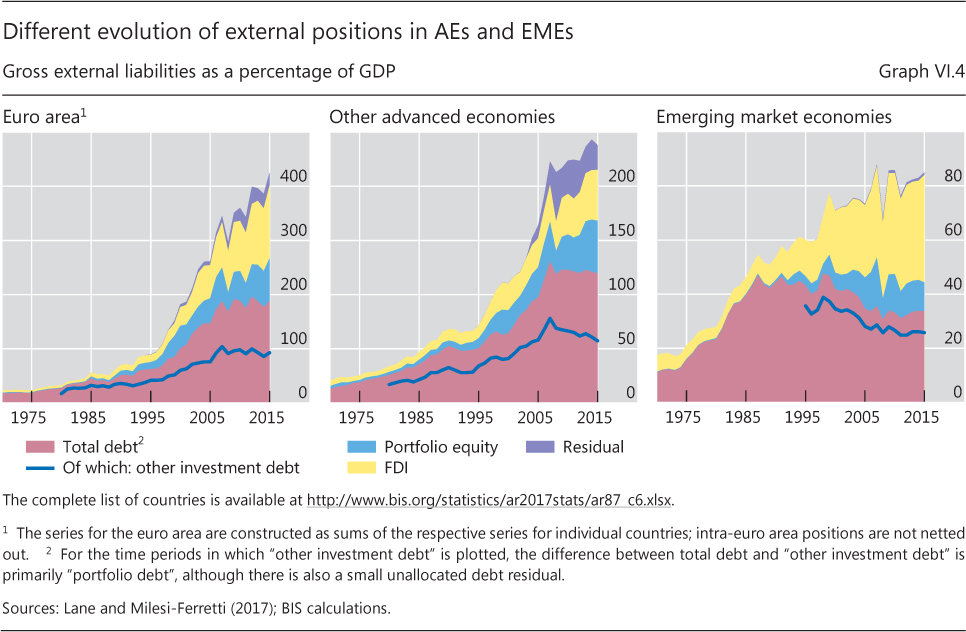

Advanced economies' financial openness accelerated markedly from the mid-1990s. International assets and liabilities soared as financial liberalisation and innovation provided new opportunities to manage positions and risk. Advanced economies' external liabilities surged from under 80% of GDP in 1995 to over 290% in 2015. Every major component of external liabilities at least doubled as a share of GDP. Highlighting the prominence of the third globalisation layer, portfolio debt liabilities quadrupled and portfolio equity liabilities more than quintupled.

Tighter financial integration was most evident in advanced Europe, where the introduction of the euro helped boost cross-border transactions (Graph VI.4, left-hand panel). Between 2001 and 2007, 23 percentage points of the increase in the ratio of advanced economies' external liabilities to GDP was due to intra-euro area financial transactions and another 14 percentage points to non-euro area countries' financial claims on the area.

Just as multinational corporations play a key role in trade, large internationally active financial institutions increasingly dominate global finance, particularly in advanced economies. These giants have subsidiaries and branches in countries across several continents. They engage not only in cross-border financial transactions, but also in local borrowing and lending, not classified as international transactions in the balance of payments (BoP) accounting framework. As a result, standard BoP-based measures of financial openness tend to underestimate the degree of global interconnectedness (Box VI.B), just as they do for the non-financial sector, where multinationals' subsidiaries produce for their local market.

For EMEs, overall financial openness has grown only slightly faster than trade openness, but the composition of external liabilities has changed substantially to support greater risk-sharing (Graph VI.4, right-hand panel). The share of equity (portfolio equity and the equity component of FDI) has risen considerably since the early 1980s.

A couple of factors have contributed to the growing share of equity liabilities in EMEs. First, tighter EME trade integration has stimulated equity flows, such as through GVCs. Second, improvements in institutional quality and governance and in macroeconomic conditions have whetted investors' appetite for long-run EME exposures. These factors have been particularly important for FDI, given its dependence on longer-run macroeconomic considerations. 11

However, the increase in risk-sharing is not as great as the rising total FDI share in global capital flows suggests. First, FDI flows consist not only of equity but also of debt, which engenders less risk-sharing. The debt component captures (non-financial) intra-company flows, driven by non-financial corporates' offshore issuance and investment activity. 12 As a result, FDI debt tends to behave more like portfolio debt than like the more stable FDI equity. Second, a large part of the recent rise reflects positions vis-à-vis financial centres. To this extent, it mirrors mainly the greater complexity of multinational corporations' corporate structure rather than traditional greenfield investment. 13

The composition of EMEs' external assets is very different from that of their liabilities. This reflects how EMEs have responded to the increase in third-layer globalisation among advanced economies. The greater size and range of global financial interactions have made EMEs more susceptible to financial shocks, as witnessed by the financial crises in the 1980s and 1990s. These crises prompted many EME governments to accumulate substantial foreign exchange reserves. Also, the combination of EMEs' rising incomes, high saving and limited availability of domestic safe assets increased the private sector's demand for advanced economy assets.

Has globalisation peaked?

The rise in globalisation has been in check since the Great Financial Crisis (GFC) of 2007-09. 14 International trade collapsed during the GFC and, despite a rapid rebound, has remained relatively weak (Graph VI.3, right-hand panel). 15 In real terms, global trade has barely grown in line with global GDP. This is striking given that trade has consistently outpaced GDP since the mid-1800s, with the exception of the interwar years. In nominal terms, trade appears even weaker, failing to keep up with GDP growth owing to the fall in the relative prices of traded goods and services, particularly commodities. The GFC also brought to a halt the rapid rise in standard BoP-based measures of financial openness. The global stock of external assets and liabilities in 2015 was little changed from its 2007 peak of just over 400% of global GDP, in sharp contrast to the nearly 190 percentage point rise between 2000 and 2007 (Graph VI.2).

Box VI.A

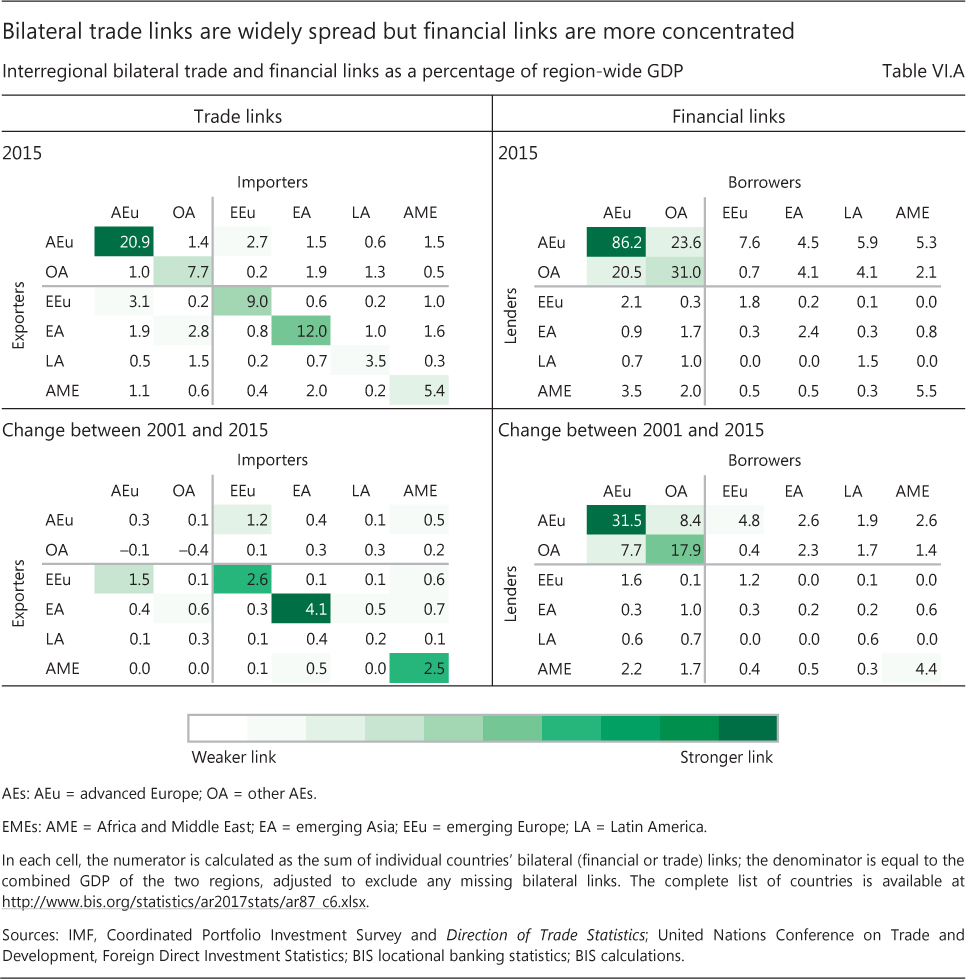

A globalisation map

Trade and financial connections are not evenly spread across countries. Geographically close and economically similar countries tend to have higher bilateral trade openness (Table VI.A, top left-hand panel). As a result, intraregional trade openness (diagonal elements in top left-hand panel) tends to be greater than interregional trade openness (off-diagonal elements). Advanced Europe is by far the most internally open region. That said, over the past 15 years, intraregional trade openness has changed little among advanced economies, but has grown noticeably among EMEs (Table VI.A, bottom left-hand panel). This has coincided with increased trade between advanced economies and EMEs, driven primarily by the growth and development of EMEs.

As a result, intraregional trade openness (diagonal elements in top left-hand panel) tends to be greater than interregional trade openness (off-diagonal elements). Advanced Europe is by far the most internally open region. That said, over the past 15 years, intraregional trade openness has changed little among advanced economies, but has grown noticeably among EMEs (Table VI.A, bottom left-hand panel). This has coincided with increased trade between advanced economies and EMEs, driven primarily by the growth and development of EMEs.

Highlighting the imprints of the first two layers of globalisation, in which real and financial openness are closely linked, there are clear similarities between the patterns of bilateral financial and trade links. Similar to trade links, the strongest bilateral cross-border financial links are among and within advanced economy regions (Table VI.A, top right-hand panel). Furthermore, just as in the case of international trade, there are strong financial linkages between advanced and emerging Europe, between North and Latin America, and between all advanced economy groups and emerging Asia. These similarities between the real and financial linkage maps reflect the first two globalisation layers.

Similar to trade links, the strongest bilateral cross-border financial links are among and within advanced economy regions (Table VI.A, top right-hand panel). Furthermore, just as in the case of international trade, there are strong financial linkages between advanced and emerging Europe, between North and Latin America, and between all advanced economy groups and emerging Asia. These similarities between the real and financial linkage maps reflect the first two globalisation layers.

Nevertheless, in line with the third layer of globalisation, there are also important differences between the patterns of real and financial linkages. For example, the bilateral financial links are more narrowly concentrated than their trade equivalents. The strongest links, those within advanced Europe, are substantially deeper than those between advanced economies and EMEs, or within EMEs.

The evolution of financial and trade linkages has differed considerably over the past couple of decades. While there has been a marked increase in intra-EME trade, particularly among EMEs in the same regions, the same is not true for financial flows, with the exception of Africa and the Middle East (Table VI.A, bottom panels). The much larger increases for financial flows between advanced economies than EMEs suggest that, despite the global financial crisis, the pace of financial innovation and development is still much higher in advanced economies (top left-hand quadrant of bottom right-hand panel). This is a clear manifestation of the third layer of globalisation.

This is a long-standing finding in the international trade literature; see eg J Bergstrand, "The gravity equation in international trade: some microeconomic foundations and empirical evidence", The Review of Economics and Statistics, vol 67, no 3, pp 474-81, 1985. The three layers of globalisation, as outlined in the main text, relate to an increasing degree of sophistication in the links between economies. They are (i) trade of commodities and finished goods and associated simple international financial links such as cross-border payments; (ii) more complex trade and financial connections, including the efficiency-driven fragmentation of production across countries and corresponding financing arrangements; and (iii) financial transactions increasingly used to actively manage balance sheet positions, including the stocks of assets and liabilities created by the first two layers.

The interaction of real and financial factors within the first two globalisation layers in part explains the easing in both trade and financial openness. In the early stages of the GFC, tighter financial conditions amplified the sharp fall in trade. 16 Exports of more financing-dependent consumer durable and capital goods plummeted, and the desire to borrow and availability of funds diminished. Other common factors have been more important since then. The demand-induced weakness in trade-intensive physical investment has also depressed the corresponding international financing flows. The weak economic recovery in Europe - an especially trade-intensive and financially open region - has been another element. More generally, the pullback in trade and financial openness reflects a desire to reduce risk, most obviously by financial institutions, but also by non-financial companies, as seen in the decline in disruption-sensitive GVCs.

However, at least on the financial side, the apparent pause in globalisation needs to be interpreted with caution. First, conventional measures somewhat overstate the reduction in openness. Despite being stagnant at the global level, the ratio of external liabilities to GDP has continued to grow for both advanced economies and EMEs post-crisis (Graph VI.4). This seeming anomaly reflects that the level of financial globalisation is much lower for EMEs than for advanced economies, and so EMEs' growing share of global GDP depresses the global measure of financial globalisation. The expansion of financial openness for advanced economies has slowed considerably since the crisis; by contrast, that for EMEs has continued unabated.

Second, the pullback in finance has been limited to some types of flows. It has been concentrated in cross-border bank loans, a component that had fuelled the rapid pre-crisis expansion in the highly procyclical third globalisation layer. 17 Thus, at least part of the current contraction reflects a healthy unwinding of unsustainable pre-crisis positions. 18 Furthermore, the contraction in cross-border loans has been partly offset by a pickup in portfolio debt flows. Bond markets and asset managers, spurred by low and sometimes negative yields, have largely filled the gap left by banks - what has been termed the "second phase of global liquidity". 19 FDI and portfolio equity have also continued to grow.

Finally, the contraction in bank lending is not as severe when measured using alternative metrics of financial openness. The above figures are based on the residence of the economic units, which is how the BoP statistics are constructed. A complementary measure is based on the location of those units' headquarters, or nationality basis, and consolidates the corresponding balance sheet. This better captures the decision-making unit and is especially relevant for internationally active banks, as it includes the operation of their offices abroad. As the BIS international banking statics (IBS) indicate, this transnational component has been much more stable post-crisis (Box VI.B). Furthermore, there is some evidence that EME banks, many of which are not captured by the IBS, have substantially increased their international presence through foreign offices. This trend is especially pronounced at the regional level. 20

Box VI.B

Financial deglobalisation in banking?

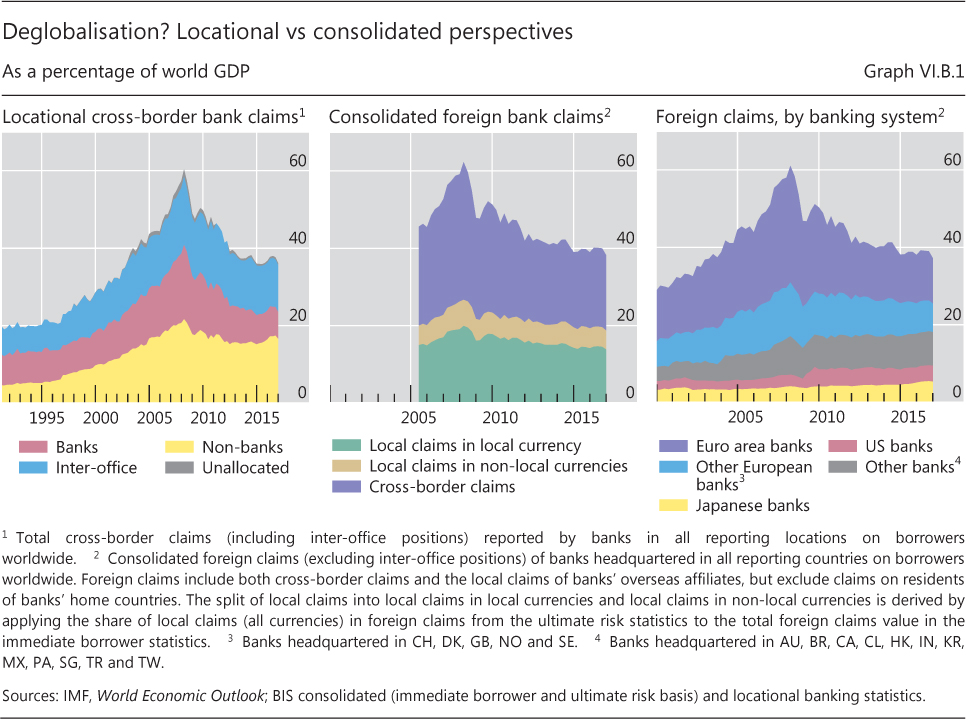

"Peak trade" denotes the hypothesis that global trade is no longer growing faster than global GDP, which may preclude the strategy of trade-led economic growth. A parallel thesis, perhaps global "peak finance", asserts that the world has seen the peak of global finance and that financial deglobalisation has begun. In particular, observers have interpreted international banking data as showing financial deglobalisation. This box argues against this inference.

BIS data on cross-border banking positions give the appearance that banking deglobalisation set in during the Great Financial Crisis (GFC) of 2007-09 and has continued since. Graph VI.B.1 (left-hand panel) shows that the cross-border claims reported by banks in more than 40 jurisdictions declined from a peak of 60% of global GDP in 2007 to less than 40% since 2013. These data are compiled on a balance of payments (locational) basis. Such stocks of external assets are frequently used to measure international financial integration.

A limitation of using external assets is that these double-count some positions, and ignore other relevant ones. Giving priority to where the banking business is conducted can be useful in a discussion of macroeconomic aggregates, such as employment and value added. But cross-border claims are perhaps not the best way to analyse globalisation trends in banking. They double-count positions in which a bank's headquarters funds its branch in a financial centre like London (left-hand panel, blue area) before lending abroad. At the same time, banks' local positions, ie those booked by a foreign affiliate on host country residents, are not captured in the external positions of either the banks' home country or the affiliates' host country. On a consolidated view, these are foreign positions - the bank has a claim on a borrower outside the home country, also if it is booked and even funded locally.

The BIS consolidated banking statistics, organised by nationality (on the basis of the location of banks' headquarters), provide a clearer perspective on banking deglobalisation. First, local positions have not contracted nearly as much as cross-border ones (Graph VI.B.1, centre panel). True, subtracting inter-office claims just about offsets adding local claims - as a result, the centre panel tells a similar story to the left-hand panel. But the consolidated perspective also makes clear that the shrinkage of international banking is largely confined to European banks (Graph VI.B.1, right-hand panel).

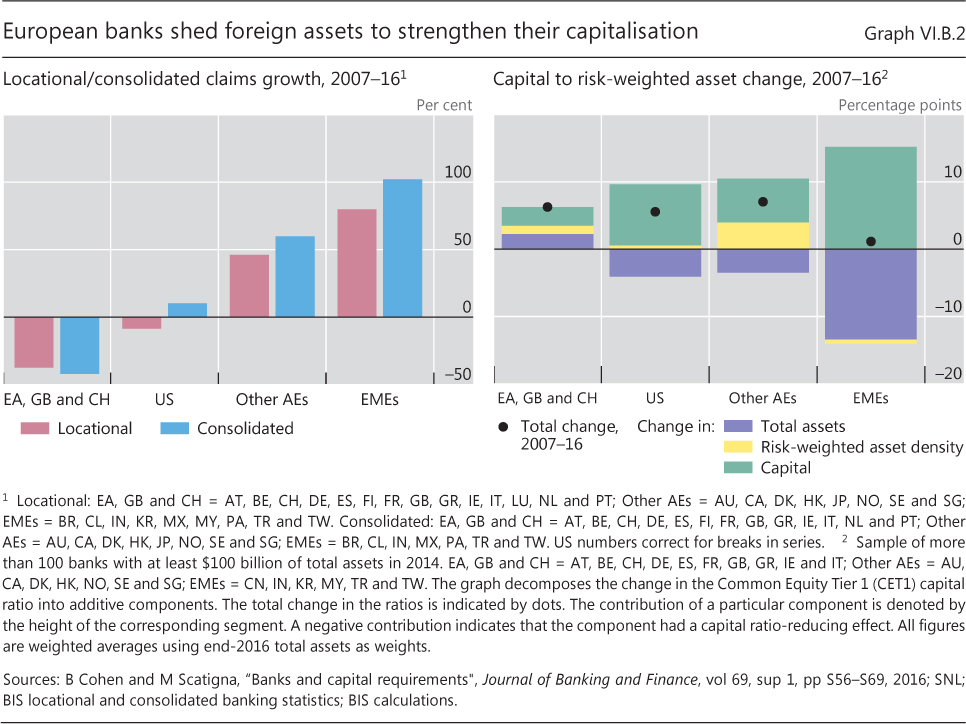

That the apparent deglobalisation is more regional than global can be seen by contrasting asset growth by booking location with that by bank nationality (Graph VI.B.2, left-hand panel). Banks headquartered in Europe accounted for more than all of the global decline - that is, these banks' foreign claims declined by more than $9 trillion, while those of US banks and banks from other advanced countries and EMEs grew. The strength of the apparent deglobalisation in banking reflects the size of European banks before the GFC and their subsequent contraction.

The shrinkage of European banks' foreign claims is better interpreted as (cyclical) deleveraging after a banking glut than as a structural deglobalisation trend. While there has been a common move among big banks to raise the ratio of capital to risk-weighted assets since the GFC (Graph VI.B.2, right-hand panel, black dots), European banks uniquely did so in part by reducing total assets (a positive violet bar). Big banks elsewhere raised enough equity through retained earnings and equity issuance while expanding total assets. Put differently, European banks did not raise enough capital to achieve the 5 percentage point improvement in their weighted capital ratio without also shedding assets. Given European banks' extensive overseas operations, their retrenchment was felt around the globe. Indeed, apart from Spanish banks, home bias tended to spare claims at home from the asset shedding.

A retreat to the home market when a bank has suffered losses can reflect lower expected returns abroad or increased risk aversion, especially given losses abroad. But it can also reflect policy choices in the context of widespread government support for banks and unconventional monetary policy that targets domestic lending. On this view, the home bias evident in the European bank deleveraging may partly reflect policies. In any case, consolidated banking data identifies the regional origin of the apparent trend in global aggregates.

On this view, the home bias evident in the European bank deleveraging may partly reflect policies. In any case, consolidated banking data identifies the regional origin of the apparent trend in global aggregates.

P Lane and G Milesi-Ferretti, "International financial integration in the aftermath of the global financial crisis", IMF Working Papers, no WP/17/115, 2017. R McCauley, A Bénétrix, P McGuire and G von Peter, "Financial deglobalisation in banking?", BIS Working Papers, forthcoming. K Forbes, D Reinhardt and T Wieladek, "The spillovers, interactions, and (un)intended consequences of monetary and regulatory policies", Journal of Monetary Economics, vol 85, pp 1-22, 2016.

Globalisation and welfare

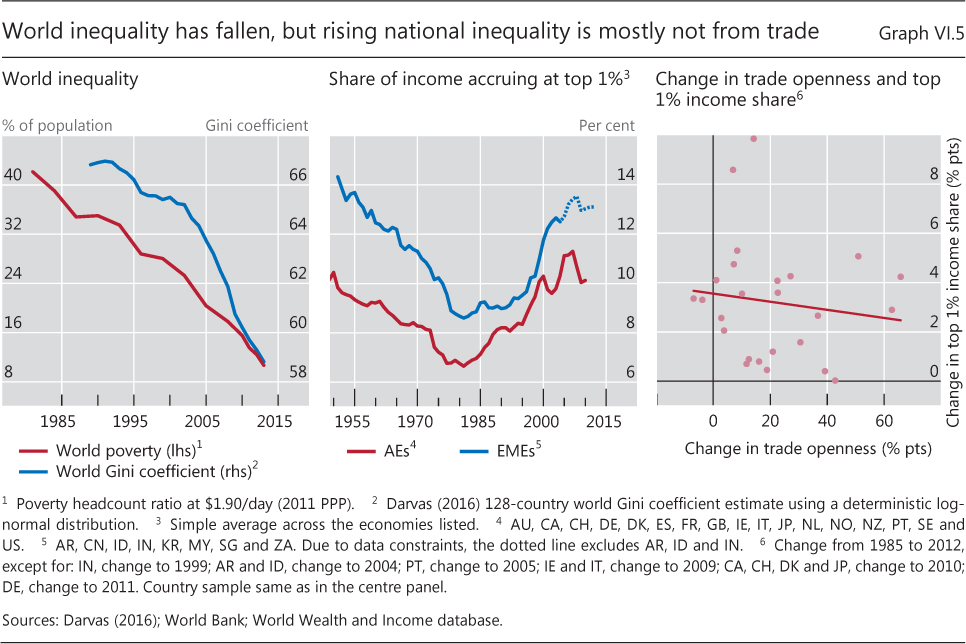

Globalisation has greatly contributed to higher living standards worldwide and boosted income growth. Over the past three decades, it has been an important factor driving the large decline of the share of the world population living in significant poverty, and of income inequality across countries (Graph VI.5, left-hand panel). 21 For example, poverty has fallen markedly in China, where the development of export industries has been a key force behind the rapid growth of GDP and incomes.

Over the same period, the income gains have not been evenly spread. The biggest gains have accrued to the middle classes of fast-growing EMEs and the richest citizens of advanced economies. In contrast, the global upper middle class has experienced little income growth. 22 This has seen within-country income inequality increase in advanced economies and even many EMEs. The share of income accruing to the top 1% of income earners has increased substantially since the mid-1980s (Graph VI.5, centre panel). 23 This contrasts with the fall in the interwar period, attributed to capital destruction and regulatory and fiscal policies, and for several decades thereafter. 24 Some degree of income inequality resulting from returns to effort can enhance growth by creating incentives for innovation. But high inequality appears to be harmful to growth and has undermined public support for globalisation. 25

There is strong empirical evidence that globalisation is not the main cause of increased within-country income inequality; technology is. 26 Still, the critics of globalisation have often confounded the challenges that it poses with the main drivers of many economic and social ills.

Globalisation and growth

Both trade and financial openness can be expected to increase the rate of economic growth. Trade between nations increases the marketplace's size and the competition between firms. This improves efficiency as production is concentrated in the most productive firms, wherever they may be. The most productive ones expand, achieving greater scale economies and further enhancing their efficiency, while the least efficient firms contract, increasing aggregate productivity. Overall, trade has been found to boost growth in many economies. Trade also directly benefits consumers, as they can choose from a greater variety of higher-quality products. 27

Financial openness should also boost growth, by enabling a more efficient allocation of capital and facilitating the transfer of technology and know-how. The ability to hold foreign financial assets increases opportunities for higher returns and for risk diversification. The injection of foreign capital can provide funding for previously capital-constrained firms, increasing real competition and efficiency. FDI can yield even greater benefits through the transfer of knowledge and technology and the spread of best practices.

Empirical work has not universally identified increases in income or growth from increased financial openness. One reason could be that the relationship is non-monotonic: the benefits may materialise only if certain thresholds are met regarding the recipient country's financial market development, institutional quality, governance framework, macroeconomic policies and international trade integration. It has also been suggested that the benefits from capital account deregulation may be less direct and take time to detect. 28 Last but not least, many of the existing empirical studies treat trade openness and financial openness as independent variables, thus implicitly assuming that trade integration could take place without financial integration. Yet, as discussed above, trade and financial openness tend to go hand in hand.

Globalisation and inequality

National income undoubtedly increases with trade. However, the gains are unevenly distributed - a general feature of economic dynamism. Less efficient firms facing new competition contract, and it may take time for new ones to enter the market, for instance because of regulatory or financial constraints. The winners and losers are unevenly distributed across skills, income levels and location. Trade between advanced economies and EMEs generally increases the return to advanced economy skilled labour, which is relatively scarce globally. In contrast, the returns to unskilled labour in advanced economies may well diminish because of the greater competition from the large pool of unskilled EME labour. Conversely, unskilled labour in EMEs may benefit. At the same time, trade also leads to relative price falls for goods disproportionately consumed by lower-income households, boosting their relative purchasing power. 29 Given these offsetting effects, the net effect on inequality from trade openness is uncertain in economic models.

There are also opposing channels through which financial openness could affect income inequality. If financial openness increases the ability of low-income individuals to borrow, it can enhance their opportunities for income generation. Indeed, there is evidence that greater access to (domestic) finance can increase incomes of the poor. 30 Alternatively, if financial openness, and FDI in particular, increases capital intensity and the returns to skill, the benefits could accrue to higher-income individuals. Financial openness could also increase income inequality if domestic institutions are not strong enough to prevent special interest groups from capturing the associated gains. 31

Trade and financial openness can also increase inequality by favouring income from capital sources. Greater international mobility of goods and capital, relative to labour, can reduce labour's "pricing" power, putting downward pressure on wages, and constrain the feasibility of taxing capital, contributing to higher taxes on labour income. 32 Since lower-income households rely primarily on labour income, these effects are likely to increase inequality.

In practice, trade and financial openness appear to have made only a fairly small contribution to the increase in income inequality (Graph VI.5, right-hand panel). For financial globalisation, this effect is likely to have been somewhat larger in low-income countries. 33 Rather, technology appears to have been the dominant factor: the returns to skilled labour, which uses technology more intensely, have increased substantially. 34

While declining labour shares have been linked to globalisation, the evidence indicates that it is not the only driver. Declines have not occurred in some highly open countries, such as France and the United Kingdom, and industries, including agriculture and financial and business services. Moreover, labour shares in many economies decreased the most in previously regulated services and utilities, many of which are not traded, where returns fell as a result of structural reforms. In a number of other countries, the decline in labour shares was mainly due to surging housing rents (including imputed rents of homeowners). 35

Importantly, the impact of trade on inequality depends on obstacles to adjustment. In some cases, there have been persistent localised economic contractions in areas adversely affected. Falls in employment and wages in import-competing firms have been compounded by these firms' reduced purchases from their suppliers, who are often located nearby. This spills over to spending more broadly in the local community. 36 These effects can be persistent if labour is immobile across regions and industries.

Globalisation and financial stability

One specific mechanism through which globalisation can affect economic growth, poverty and inequality is its impact on financial stability. Financial crises can result in a permanent loss of income, have a devastating effect on poverty and increase inequality. 37

Just like poorly managed domestic financial liberalisation, unfettered financial openness can contribute to financial instability unless sufficient safeguards are in place. It is no coincidence that, after financial crises were relatively common in the first globalisation wave, there were few in the following era of financial repression which lasted into the 1970s. The EME financial crises of the 1980s and 1990s involved sharp reversals of international capital flows. And the GFC saw large spillovers between national financial systems. In addition, financial openness may adversely affect financial stability if it constrains the effectiveness of independent domestic monetary policy. 38

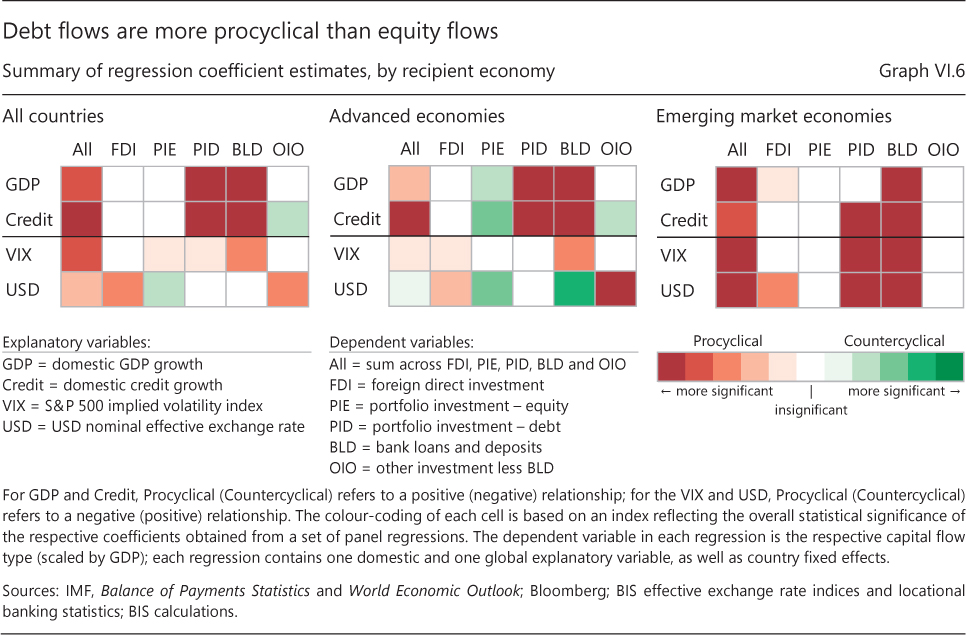

Past episodes of financial instability have demonstrated the importance of three international propagation mechanisms. First, highly mobile international capital can behave in a very procyclical manner, amplifying financial upswings and reversals. Second, foreign currency exposure, in particular in dollars, transmits tighter global financial conditions and exposes countries to foreign exchange losses. And third, close financial linkages between globally active financial institutions can spread financial stress, although they may also act as a buffer when problems have a domestic origin.

International credit has been a key source of procyclicality. Such flows tend to be procyclical with respect to the recipient economy's business and financial cycles. Cross-border bank loans and portfolio debt flows are both positively correlated with domestic business and credit cycles. 39 FDI flows tend to be acyclical, while portfolio equity flows into advanced economies even appear to be slightly countercyclical.

The close link between cross-border and domestic credit may add to financial stability risks. Cross-border credit tends to amplify domestic credit booms, as it acts as the marginal funding source: the cross-border component typically outgrows its domestic counterpart during financial booms, especially those that precede serious financial strains. 40

Debt flows are also sensitive to global factors. In particular, loan and bond flows to EMEs have been sensitive to global risk aversion and the US dollar's strength (Graph VI.6, centre and right-hand panels). In fact, global risk aversion, or at least its historical proxy (the VIX), has had a non-negligible impact on bank lending even to advanced economies. This sensitivity, however, appears to have declined of late. 41 By contrast, there is evidence that the sensitivity of cross-border bank lending and portfolio debt flows to US monetary policy has increased considerably since the GFC. 42

The high sensitivity of capital flows to US monetary policy is a manifestation of the "excess elasticity" of the international monetary and financial system - its ability to amplify financial booms and busts and thereby cause serious macroeconomic costs. 43 There are two main channels through which monetary policy regimes interact to create this excess elasticity. In the first, monetary policy settings in core economies are spread to the rest of the world through resistance to exchange rate appreciation, typically based on concerns about the loss of competitiveness (on the real side) and the possibility of surges in capital flows (on the financial side). The second channel is related to the fact that the domains of major international currencies extend well beyond their respective national jurisdictions. 44

This global currency channel is especially powerful in the case of the US dollar - the dominant international currency. The outstanding stock of US dollar-denominated credit to non-bank borrowers outside the United States, a key indicator of global liquidity conditions, stood at $10.5 trillion as of end-2016. This outsize external role means that changes in the US monetary policy stance have a substantial influence on financial conditions elsewhere (Box VI.C). And since monetary policymakers, including those in control of major international currencies, are focused on domestic conditions, they could unintentionally end up contributing to financial imbalances well beyond their national borders. Notably, against the backdrop of the exceptionally accommodative US monetary policy stance, US dollar credit to non-bank EME borrowers roughly doubled between 2008 and 2016, reaching $3.6 trillion at the end of that period.

One of the key channels through which US monetary policy impacts financial conditions elsewhere is the US dollar exchange rate. In the so-called "risk-taking channel of currency fluctuations", the depreciation of a global funding currency flatters the balance sheets of currency-mismatched borrowers and boosts lenders' risk-taking. This channel is especially relevant for external debt flows to EMEs (Graph VI.6, right-hand panel). The channel may also influence, in particular, manufactured trade through the GVCs, which are especially sensitive to financing conditions. 45

The intermediation of global currencies, especially the dollar, also creates close linkages between globally active banks. The GFC demonstrated how such interconnectedness propagated funding stress between the world's largest banks and forced them to deleverage internationally. Thus, the regulatory reforms in the aftermath of the GFC have focused on strengthening the resilience of international banks that are the backbone of global financial intermediation.

Getting the most from globalisation

The globalisation surge over the past half-century has brought many benefits to the world economy. Openness to trade has enhanced competition and spread technology, driving efficiency gains and aggregate productivity. The resulting stronger income growth has supported a remarkable decline in global poverty and cross-country income inequality. The ability to source cheaper, and better-quality, goods and services from all over the world has also directly increased households' living standards. And the benefits do not just relate to trade. Financial openness is inextricably intertwined with trade openness: financial linkages both support trade, and are created by trade. Financial openness, properly managed, can also independently enhance living standards through a more efficient allocation of capital and know-how transfers.

While globalisation increases living standards, it does create challenges. First, the gains are not equally distributed. The distributional implications of trade and financial openness need to be addressed to ensure fair outcomes within societies and continued support for growth-enhancing policies and economic frameworks, including global commerce. That said, other factors - most notably technology - have played a dominant role in the increase in income inequality. Just as there is no suggestion to wind back technology, reversing globalisation would be greatly detrimental to living standards.

Second, financial openness exposes economies to potentially destabilising external forces. This risk can be managed by designing appropriate safeguards, just as in the case of risks associated with domestic financial liberalisation. Since international trade and finance are inextricably intertwined, particularly in the first two globalisation layers, reaping the benefits of trade would be impossible without international finance. That is why the policy solution is not to reduce financial openness, but rather to carefully address the associated risks.

The challenges of managing economic change are not unique to globalisation. As with other secular trends, well designed policies can offset the adjustment costs associated with globalisation and enhance the gains from it.

On the domestic front, countries can implement policies that boost resilience. Just as in the case of technology, flexible labour and product markets and measures that enhance adaptability, such as retraining programmes, can reduce any trade-induced dislocations. Well targeted policies may also help counteract the sometimes persistent losses experienced by segments of society, for example region-specific employment initiatives. 46

Strong policy and institutional frameworks designed to make financial systems sounder are critical to reaping the full benefits of financial openness. The domestic financial stability policy toolkit is important. 47 This calls for well articulated macroprudential frameworks on a firm microprudential base. And it also requires the capacity to address directly any debt overhang and asset quality problems that might arise during financial busts, in order to repair balance sheets and improve overall creditworthiness.

Indeed, EMEs have been taking important steps in this direction since the mid-1990s. And this has gone hand in hand with a better external balance sheet structure, helping to reduce their vulnerability to external factors, including through considerably stronger net international investment positions, substantial increases in their foreign exchange reserves and a higher FDI share. 48

International cooperation that addresses global linkages must supplement domestic policies. The special roles of global financial institutions and global currencies transcend international trade and the financial interactions directly linked to it in the first two layers. An internationally agreed joint regulatory approach is needed to ensure that policymakers properly manage global financial risks, not least those associated with the highly procyclical third layer. Because policies and actions of individual countries affect others, multilateralism is key for delivering the best outcomes for all.

As regards global financial institutions, the first priority is to complete the international financial reforms already under way. These reforms will go a long way to boosting the resilience of the global financial system. An agreed global regulatory framework is the basis for effective supervision of internationally active banks, including mechanisms for cross-border information-sharing. And it fosters a level playing field, a precondition for efficiency and soundness at the global level.

As regards global currencies, effective crisis management mechanisms remain important, and naturally require international cooperation. Central banks have built on the successful cooperation during the GFC. Among the central banks of major currency areas, foreign currency swap lines exist or could be established quickly as needed. And there may be some room to strengthen these mechanisms further, even though risk management and governance issues loom large. However, a greater emphasis on preventing the build-up of financial imbalances appears desirable. At a minimum, this would mean taking more systematic account of spillovers and spillbacks when setting policies. 49

International cooperation is also needed beyond finance to ensure a level playing field in trade and areas such as tax. Multilateral trade agreements provide the largest common markets to maximise efficiency. Trade and financial linkages enable companies, particularly large multinationals, to make decisions regarding production and profit declaration to minimise their taxes. Avoiding this can ensure that highly mobile capital can share the tax burden with less mobile labour, and so address income inequality. Together, such well designed domestic and international actions can ensure that globalisation continues to be a greatly beneficial force for the world economy and people's living standards.

Box VI.C

Globalisation and interest rate spillovers

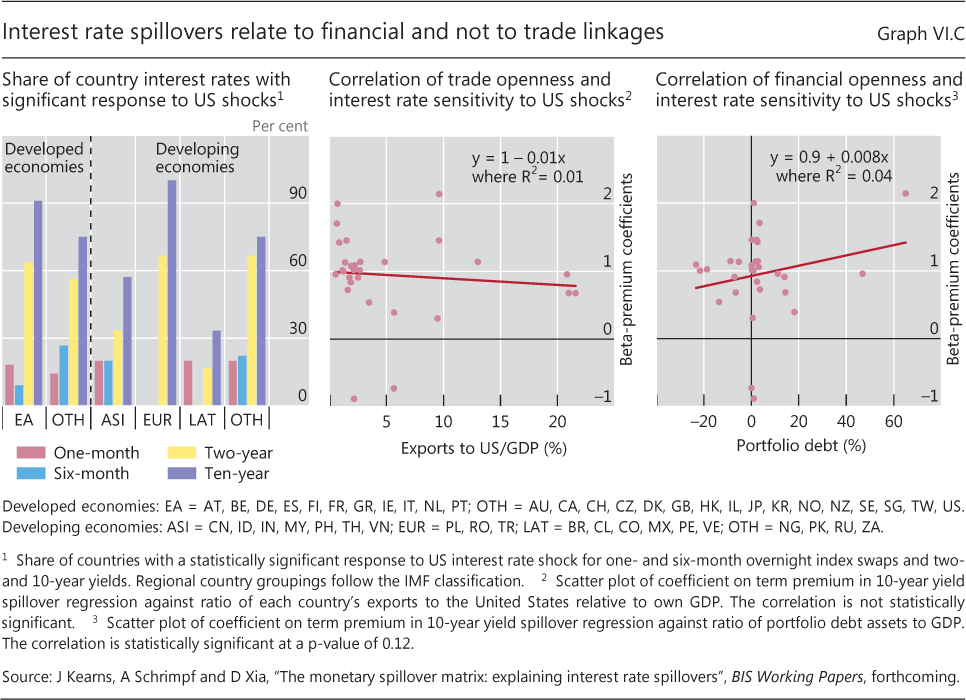

Increased globalisation has coincided with a significant rise in the co-movement of global asset prices. For example, the correlation of advanced economy sovereign 10-year yields in the past two decades more than doubled relative to the previous two. Given the myriad of changes in real and financial linkages between countries, it is difficult to assess whether asset price co-movement reflects common factors or spillovers from specific countries. One way to disentangle this is to examine the response of international asset prices to an unexpected development ("shock") that clearly emanates from one country.

A useful shock is monetary policy announcements, as they are primarily related to domestic conditions. Because asset prices incorporate all expected developments, the shock must be measured as the unexpected change in monetary policy and include information about the future policy path. The response of interest rates to a monetary policy shock in a foreign country is assessed by regressing the daily change in the domestic interest rate on the foreign policy shock, which is identified from the change in short- and long-term foreign interest rates in a 25-minute window around a policy announcement. The response of one- and six-month and two- and 10-year interest rates is analysed for a panel of 47 advanced economies and EMEs.

The results point to significant spillovers across countries, in particular for longer-term interest rates and from the United States. For example, 10-year bond yields in 34 of the 47 countries display a statistically significant response to US shocks, compared with around half this number for euro interest rate shocks and only five to eight countries for shocks from five other advanced economy central banks. These responses are also economically significant: for the median country, long-term yields rise 4 basis points in response to a 10 basis point increase in the US term premia. The prominence of US monetary policy announcements relates to the pre-eminent role of the US dollar in international financial markets. The international spillovers are also clearly larger for longer-term interest rates. For one- and six-month interest rates, only eight countries display significant spillovers from US interest rates. In contrast, for two- and 10-year bond yields, 23 and 34 countries have significant responses, respectively (Graph VI.C, left-hand panel).

Interest rate spillovers are more closely related to financial openness than trade openness. The intensity of interest rate spillovers shows no relationship with trade openness, measured as the trade-to-GDP ratio (Graph VI.C, centre panel). In contrast, it correlates with measures of financial openness. For example, there is a statistically significant relationship between the intensity of interest rate spillovers and financial openness, measured by the ratio of international portfolio debt assets to GDP (Graph VI.C, right-hand panel).

The shocks used are from M Ferrari, J Kearns and A Schrimpf, "Monetary policy's rising FX impact in the era of ultra-low rates", BIS Working Papers, no 626, 2017. The response of interest rates to foreign monetary policy shocks from seven central banks is outlined in J Kearns, A Schrimpf and D Xia, "The monetary spillover matrix: explaining interest rate spillovers", BIS Working Papers, forthcoming. Three shocks are used to capture the full extent of information in the central bank's policy announcement: (i) the change in the one-month overnight index swap interest rate (referred to as the "target shock"); (ii) the change in the two-year bond yield that is orthogonal to the first shock (referred to as the "path shock"); and (iii) the change in the 10-year bond yield that is orthogonal to the first two shocks (referred to as the "term premium shock").

Endnotes

1 This chapter does not deal with migration flows across national borders, another important dimension of globalisation. Borjas (2015) reviews the potential gains to GDP that could accrue from migration. Obviously, there would be many practical impediments to realising these gains. Furthermore, this chapter uses de facto measures of real and financial openness, which are based on observed outcomes, rather than de jure measures, which are based on rules and legal restrictions. De facto measures generally provide a better indicator of actual openness, as de jure measures fail to take into account the effectiveness of controls or implicit protection.

2 This is more prominent in EMEs, where the proportion rises to around two thirds compared with around one third in advanced economies, based on calculations from the data used by Casas et al (2016). See also Ito and Chinn (2015).

3 See CGFS (2014). Foreign banks are found empirically to assist exports from EMEs by helping to provide external finance and guarantees of payment (Claessens et al (2015)).

4 For example, the sales of US multinationals' subsidiaries are spread wide, going to: their home market (over half), third countries (one third) and the United States (11%) (Antràs and Yeaple (2014)). Multinationals not only engage in more FDI and trade, but also spread technology by concentrating research and development in the parent and production in subsidiaries (Keller (2010)). In this second layer, transfer of knowledge and ideas can promote trade, but also act as a substitute for trade, an idea taken up by Baldwin (2016).

5 See Kim and Shin (2016) on the connection between the length of the production chain and the intensity of external finance required.

6 The exact level of trade openness differs somewhat across estimates, but the profile is similar; see Federico and Tena-Junguito (2016), Klasing and Milionis (2014) and Estevadeordal et al (2003).

7 Irwin (2002) attributes half of the decline in world trade in 1929-32 to higher tariffs, import quotas and foreign exchange controls.

8 For example, Constantinescu et al (2017) argue that trade agreements have boosted trade growth by 2 percentage points per annum since 1995, while Meissner (2014) argues that episodes of strong growth have seen trade grow faster than GDP.

9 For an overview of global value chains, see Elms and Low (2013), Kowalski et al (2015), WTO (2014) and the references therein.

10 See Antràs and Yeaple (2014) and Bernard et al (2009).

11 On the factors contributing to the growth of equity-type investment and FDI in particular, see Kose et al (2009) and Koepke (2015).

12 See Avdjiev et al (2014) and Gruić et al (2014).

13 See Lane and Milesi-Ferretti (2017).

14 See the discussion and references contained in Caruana (2017).

15 There are many studies of the fall and subsequent weakness in trade. A selection includes Baldwin (2009), Constantinescu et al (2015, 2017), ECB (2016), Hoekman (2015), IMF (2016) and Haugh et al (2016).

16 Amiti and Weinstein (2011), Ahn et al (2011), Chor and Manova (2012) and Cheung and Guichard (2009) find evidence of a role of tightening credit conditions in the fall in trade, while Paravisini et al (2015) and Levchenko et al (2010) argue the contrary.

17 See Milesi-Ferretti and Tille (2011).

18 See eg Borio (2014) and Caruana (2017).

19 See Shin (2013).

20 See Claessens and van Horen (2015) and CGFS (2014).

21 For overviews of global income inequality, see Bourguignon (2015), Lakner and Milanović (2015), Deaton (2013) and Milanović (2013). See also Pereira da Silva (2016).

22 See Milanović (2013).

23 A similar trend is also apparent in the top 10%, but the data prior to the 1980s are less comprehensive for this measure.

24 See Piketty and Saez (2014).

25 Dabla-Norris et al (2015) find that a higher income share for the top 20% reduces growth (but a higher share for the bottom 20% boosts growth), while Ostry et al (2014) come to the same conclusion using a Gini coefficient to measure inequality. Halter et al (2014) suggest that inequality boosts growth in the short run but not in the long run.

26 See Cline (1997) and IMF (2007).

27 On trade and growth there are many papers, including Frankel and Romer (1999), Irwin and Terviö (2002), Lee et al (2004) and Noguer and Siscart (2005). Broda and Weinstein (2006) show that increased variety of goods is an important source of gains from trade.

28 Kose et al (2006) provide an extensive review and conclude that the benefits are indirect and difficult to measure. Rodrik and Subramanian (2009) and references therein summarise the lack of firm evidence for substantive benefits from financial globalisation. Some research, however, does find that financial and capital market liberalisation boosts growth, eg Alfaro et al (2004), Bekaert et al (2005) and Klein and Olivei (2008).

29 See Faijgelbaum and Khandelwal (2016).

30 Beck et al (2007) conclude that greater access to finance increased incomes of the poor. This has been confirmed recently by Ben Naceur and Zhang (2016) for most measures of financial development, but not for financial liberalisation. Reduced restrictions on bank operations can also boost incomes of poorer households, as shown in Beck et al (2010).

31 See Claessens and Perotti (2007) for a summary.

32 Autor et al (2017) find evidence that the fall in the labour share is driven largely by between-firm reallocation rather than by a fall in the unweighted mean labour share within firms. They link this finding to the evidence that the most productive firms in each industry are the biggest beneficiaries of globalisation.

33 That financial openness increases income inequality is a fairly uniform finding in the literature. On this topic, see eg Cabral et al (2016), Figini and Görg (2011), IMF (2007) and Jaumotte et al (2013). This finding is not dominated by EMEs. For example, even for OECD countries, Denk and Cournède (2015) find that financial expansion increased income inequality and there is no evidence that this results from financial crises.

34 While many studies find that trade openness has reduced inequality (Jaumotte et al (2013), IMF (2007)), and probably lowered unemployment (Görg (2011)), this contrasts with the review of country studies by Goldberg and Pavcnik (2007). These opposing conclusions may reflect that other factors influence the relationship between trade and inequality. For example, Milanović (2005) finds that trade openness reduces the income share of the poor at low income levels, but raises it at higher country income levels.

35 For an overview of the decline in the labour share, see ILO and OECD (2014) and Karabounis and Neiman (2014).

36 See Autor et al (2013).

37 Borio et al (2011) outline the role that international capital can play in facilitating domestic financial excess. Most studies find that financial crises increase inequality: see Bazillier and Héricourt (2014), de Haan and Sturm (2017), Atkinson and Morelli (2011), Baldacci et al (2002) and Li and Yu (2014); although others do not: see Denk and Cournède (2015), Honohan (2005) and Jaumotte and Osorio Buitron (2015). In part, these differences may reflect the fact that the impact of crises on inequality is seemingly greater for EMEs than for advanced economies; see Galbraith and Jiaqing (1999) and Agnello and Sousa (2012). Chen and Ravallion (2010) note the significant impact that financial crises have on poverty.

38 See Rey (2015).

39 For additional empirical evidence on the procyclicality of capital flows with respect to domestic GDP growth, see Broner et al (2013), Contessi et al (2013), Bluedorn et al (2013), Hoggarth et al (2016) and Avdjiev et al (2017b). Hoggarth et al (2016) also examine the procyclicality of capital flows with respect to domestic credit. For additional empirical evidence on the procyclicality of capital flows with respect to global factors, see Koepke (2015), Nier et al (2014) and Eichengreen et al (2017).

40 See Borio et al (2011), Avdjiev et al (2012) and Lane and McQuade (2014).

41 See Shin (2016).

42 See Avdjiev et al (2017a).

43 See Borio (2014, 2016) and Caruana (2015).

44 See Shin (2015).

45 On the risk-taking channel of currency fluctuations, see Bruno and Shin (2015, 2017) and Hofmann et al (2016).

46 For a recent review of policies that can make trade reform more equitable, see IMF-World Bank-WTO (2017).

47 See Borio (2014).

48 Caballero et al (2005) demonstrate benefits of risk-sharing with a comparison of Australia and Chile in the Asian financial crisis.

49 See Agénor et al (2017).

References

Agénor, P-R, E Kharroubi, L Gambacorta, G Lombardo and L A Pereira da Silva (2017): "The international dimensions of macroprudential policies", BIS Working Papers, no 643, June.

Agnello, L and R Sousa (2012): "How do banking crises impact on income inequality?", Applied Economics Letters, vol 19, issue 15, pp 1425-9.

Ahn, J, M Amiti and D Weinstein (2011): "Trade finance and the great trade collapse", American Economic Review, vol 101, no 3, pp 298-302.

Alfaro, L, A Chanda, S Kalemli-Ozcan and S Sayek (2004): "FDI and economic growth: the role of local financial markets", Journal of International Economics, vol 64, no 1, pp 89-112.

Amiti, M and D Weinstein (2011): "Exports and financial shocks", The Quarterly Journal of Economics, vol 126, no 4, pp 1841-77.

Antràs, P and S Yeaple (2014): "Multinational firms and the structure of international trade", Handbook of International Economics, vol 4, ch 2, pp 55-130.

Atkinson, A and S Morelli (2011): "Economic crises and inequality", United Nations Human Development Research Paper 2011/06.

Autor, D, D Dorn and G Hanson (2013): "The China syndrome: local labor market effects of import competition in the US", American Economic Review, vol 103, no 6, pp 2121-68.

Autor, D, D Dorn, L Katz, C Patterson and J Van Reenen (2017): "Concentrating on the fall of the labor share", American Economic Review: Papers & Proceedings, vol 107, no 5, pp 180-5.

Avdjiev, S, M Chui and H S Shin (2014): "Non-financial corporations from emerging market economies and capital flows", BIS Quarterly Review, December, pp 67-77.

Avdjiev, S, L Gambacorta, L Goldberg and S Schiaffi (2017a): "The shifting drivers of global liquidity", BIS Working Papers, no 644, June.

Avdjiev, S, B Hardy, S Kalemli-Ozcan and L Servén (2017b): "Gross capital inflows to banks, corporates and sovereigns", NBER Working Papers, no 23116.

Avdjiev, S, R McCauley and P McGuire (2012): "Rapid credit growth and international credit: challenges for Asia", BIS Working Papers, no 377, April.

Baldacci, E, L de Mello and G Inchauste (2002): "Financial crises, poverty, and income distribution", IMF Working Papers, no WP/02/4.

Baldwin, R (ed) (2009): The great trade collapse: causes, consequences and prospects, CEPR e-book.

----- (2016): The great convergence, Harvard University Press.

Bazillier, R and J Héricourt (2014): "The circular relationship between inequality, leverage, and financial crises: intertwined mechanisms and competing evidence", CEPII Working Papers, no 2014-22.

Beck, T, A Demirgüç-Kunt and R Levine (2007): "Finance, inequality and the poor", Journal of Economic Growth, vol 12, no 1, pp 27-49.

Beck, T, R Levine and A Levkov (2010): "Big bad banks? The winners and losers from bank deregulation in the United States", The Journal of Finance, vol 65, no 5, pp 1637-67.

Bekaert, G, C Harvey and C Lundblad (2005): "Does financial liberalization spur growth?", Journal of Financial Economics, vol 77, no 1, pp 3-55.

Ben Naceur, S and R X Zhang (2016): "Financial development, inequality and poverty: some international evidence", IMF Working Papers, no WP/16/32.

Bergstrand, J (1985): "The gravity equation in international trade: some microeconomic foundations and empirical evidence", The Review of Economics and Statistics, vol 67, no 3, pp 474-81.

Bernard, A, J Bradford Jensen and P Schott (2009): "Importers, exporters, and multi-nationals: a portrait of firms in the US that trade goods", in T Dunne, J Bradford Jensen and M Roberts (eds), Producer dynamics: new evidence from micro data, National Bureau of Economic Research, pp 513-52.

Bluedorn, J, R Duttagupta, J Guajardo and P Topalova (2013): "Capital flows are fickle: anytime, anywhere", IMF Working Papers, no WP/13/183.

Borio, C (2014): "The financial cycle and macroeconomics: what have we learnt?", Journal of Banking & Finance, vol 45, issue C, pp 182-98.

----- (2016): "More pluralism, more stability?", presentation at the Seventh High-level Swiss National Bank-International Monetary Fund Conference on the International Monetary System, Zurich, 10 May.

Borio, C, R McCauley and P McGuire (2011): "Global credit and domestic credit booms", BIS Quarterly Review, September, pp 43-57.

Borjas, G (2015): "Immigration and globalization: a review essay", Journal of Economic Literature, vol 53, no 4, pp 961-74.

Bourguignon, F (2015): The globalization of inequality, Princeton University Press.

Broda, C and D Weinstein (2006): "Globalization and the gains from variety", The Quarterly Journal of Economics, vol 121, no 2, pp 541-85.

Broner, F, T Didier, A Erce and S Schmukler (2013): "Gross capital flows: dynamics and crises", Journal of Monetary Economics, vol 60, no 1, pp 113-33.

Bruno, V and H S Shin (2015): "Capital flows and the risk-taking channel of monetary policy", Journal of Monetary Economics, vol 71, pp 119-132.

----- (2017): "Global dollar credit and carry trades: a firm-level analysis", Review of Financial Studies, vol 30, pp 703-49.

Caballero, R, K Cowan and J Kearns (2005): "Fear of sudden stops: lessons from Australia and Chile", The Journal of Policy Reform, vol 8, no 4, pp 313-54.

Cabral, R, R García-Díaz and A Varella Mollick (2016): "Does globalization affect top income inequality?", Journal of Policy Modeling, vol 38, no 5, pp 916-40.

Caruana, J (2015): "The international monetary and financial system: eliminating the blind spot", speech at the IMF conference Rethinking macro policy III: progress or confusion?, Washington DC, 16 April.

----- (2017): "Have we passed 'peak finance'?", speech at the International Center for Monetary and Banking Studies, Geneva, 28 February.

Casas, C, F Diez, G Gopinath and P-O Gourinchas (2016): "Dominant currency paradigm", NBER Working Papers, no 22943.

----- (2017): "Dominant currency paradigm: a new model for small open economies", mimeo.

Chen, S and M Ravallion (2010): "The developing world is poorer than we thought, but no less successful in the fight against poverty", The Quarterly Journal of Economics, vol 125, no 4, pp 1577-1625.

Cheung, C and S Guichard (2009): "Understanding the world trade collapse", OECD Economics Department Working Papers, no 729.

Chor, D and K Manova (2012): "Off the cliff and back? Credit conditions and international trade during the global financial crisis", Journal of International Economics, vol 87, no 1, pp 117-33.

Claessens, S, O Hassib and N van Horen (2015): "The role of foreign banks in trade", Federal Reserve Board, Maastricht University, Netherlands Bank.

Claessens, S and E Perotti (2007): "Finance and inequality: channels and evidence", Journal of Comparative Economics, vol 35, no 4, pp 748-73.

Claessens, S and N van Horen (2015): "The impact of the global financial crisis on banking globalization", IMF Economic Review, vol 63, no 4, pp 868-918.

Cline, W (1997): Trade and income distribution, Institute for International Economics, Washington DC.

Cohen, B and M Scatigna (2016): "Banks and capital requirements", Journal of Banking and Finance, vol 69, sup 1, pp S56-S69.

Committee on the Global Financial System (2014): "EME banking systems and regional financial integration", CGFS Publications, no 51.

Contessi, S, P De Pace and J Francis (2013): "The cyclical properties of disaggregated capital flows", Journal of International Money and Finance, 32, pp 528-55.

Constantinescu, C, A Mattoo and M Ruta (2015): "The global trade slowdown: cyclical or structural?", IMF Working Papers, no WP/15/6.

----- (2017): "Trade developments in 2016: policy uncertainty weighs on world trade", Global Trade Watch, World Bank, Washington DC.

Dabla-Norris, E, K Kochhar, N Suphaphiphat, F Ricka and E Tsounta (2015): "Causes and consequences of income inequality: a global perspective", IMF Staff Discussion Note 15/13.

Darvas (2016): "Some are more equal than others: new estimates of global and regional inequality", Bruegel Working Paper 8.

Deaton, A (2013): The great escape, health, wealth and the origins of inequality, Princeton University Press.

de Haan, J and J-E Sturm (2017): "Finance and income inequality: a review and new evidence", European Journal of Political Economy.

Denk, O and B Cournède (2015): "Finance and income inequality in OECD countries", OECD Economics Department Working Papers, no 1224.

Eichengreen, B, P Gupta and O Masetti (2017): "Are capital flows fickle? Increasingly? and does the answer still depend on type?", World Bank, Policy Research Working Paper 7972.

Elms, D and P Low (eds) (2013): Global value chains in a changing world, World Trade Organization, Geneva.

Estevadeordal, A, B Frantz and A Taylor (2003): "The rise and fall of world trade, 1870-1939", The Quarterly Journal of Economics, vol 118, no 2, pp 359-407.

European Central Bank (2016): "Understanding the weakness in global trade. What is the new normal?", IRC Trade Task Force, Occasional Paper Series, no 178.

Fajgelbaum, P and A Khandelwal (2016): "Measuring the unequal gains from trade", The Quarterly Journal of Economics, vol 131, no 3, pp 1113-80.

Federico, G and A Tena-Junguito (2017): "A tale of two globalizations: gains from trade and openness 1800-2010", Review of World Economics, pp 1-25.

Ferrari, M, J Kearns and A Schrimpf (2017): "Monetary policy's rising FX impact in the era of ultra-low rates", BIS Working Papers, no 626, April.

Figini, P and H Görg (2011): "Does foreign direct investment affect wage inequality? An empirical investigation", The World Economy, vol 34, no 9, pp 1455-75.

Forbes, K, D Reinhardt and T Wieladek (2016): "The spillovers, interactions, and (un)intended consequences of monetary and regulatory policies", Journal of Monetary Economics, vol 85, pp 1-22.

Forbes, K and F Warnock (2012): "Debt- and equity-led capital flow episodes", NBER Working Papers, no 18329.

Frankel, J and D Romer (1999): "Does trade cause growth?", American Economic Review, vol 89, no 3, pp 379-99.

Galbraith, J and L Jiaqing (1999): "Inequality and financial crises: some early findings", University of Texas Inequality Project, Working Paper 9.

Goldberg, P and N Pavcnik (2007): "Distributional effects of globalization in developing countries", Journal of Economic Literature, vol 45, no 1, pp 39-82.

Görg, H (2011): "Globalization, offshoring and jobs", in M Bacchetta and M Jansen (eds), Making globalization socially sustainable, World Trade Organization, pp 21-48.

Gruić, B, C Upper and A Villar (2014): "What does the sectoral classification of offshore affiliates tell us about risks?", BIS Quarterly Review, December, pp 20-1.

Halter, D, M Oechslin and J Zweimüller (2014): "Inequality and growth: the neglected time dimension", Journal of Economic Growth, vol 19, no 1, pp 81-104.

Haugh, D, A Kopoin, E Rusticelli, D Turner and R Dutu (2016): "Cardiac arrest or dizzy spell: why is world trade so weak and what can policy do about it?", OECD Economic Policy Papers, no 18.

Hoekman, B (ed) (2015): The global trade slowdown: a new normal?, VoxEU.org eBook, CEPR.

Hofmann, B, I Shim and H S Shin (2016): "Sovereign yields and the risk-taking channel of currency appreciation", BIS Working Papers, no 538, revised May 2017.

Hoggarth, G, C Jung and D Reinhardt (2016): "Capital inflows - the good, the bad and the bubbly", Bank of England, Financial Stability Paper no 40.

Honohan, P (2005): "Banking sector crises and inequality", World Bank, Policy Research Working Paper 3659.

International Labour Organization and Organisation for Economic Co-operation and Development (2015): The labour share in G20 economies, report prepared for the G20 Employment Working Group.

International Monetary Fund (2007): "Globalization and inequality", World Economic Outlook, October, Chapter 4.

----- (2016): "Global trade: what's behind the slowdown?", World Economic Outlook, October, Chapter 2.

International Monetary Fund, World Bank and World Trade Organization (2017): Making trade an engine of growth for all: the case for trade and for policies to facilitate adjustment.

Irwin, D (2002): "Long-run trends in trade and income", World Trade Review, vol 1, no 1, pp 89-100.

Irwin, D and M Terviö (2002): "Does trade raise income? Evidence from the twentieth century", Journal of International Economics, vol 58, no 1, pp 1-18.

Ito, H and M Chinn (2015): "The rise of the redback: evaluating the prospects for renminbi use in invoicing", in B Eichengreen and M Kawai (eds), Renminbi internationalization: achievements, prospects, and challenges, Brookings Institution Press and the Asian Development Bank Institute, pp 111-58.

Jaumotte, F, S Lall and C Papageorgiou (2013): "Rising income inequality: technology, or trade and financial globalization?", IMF Economic Review, vol 61, no 2, pp 271-309.

Jaumotte, F and C Osorio Buitron (2015): "Inequality and labor market institutions", IMF Staff Discussion Note 15/14.

Karabarbounis, L and B Neiman, (2014): "The global decline of the labor share", The Quarterly Journal of Economics, vol 129, no 1, pp 61-103.

Kearns, J, A Schrimpf and D Xia (forthcoming): "The monetary spillover matrix: explaining interest rate spillovers", BIS Working Papers.